European Business Club

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

EUROCAR GROUP Global Factors That Determine the Low Cost Production

Ukraine as extended production facility for global car and components manufacturers Elena Chepizhko Head of Government & External Relations EUROCAR GROUP Global factors that determine the low cost production Low cost of Ukraine can integrate production YES into the global value Integration into chains as the “second High added global value value: China” in low cost chains production. YES, > 70% Potential LOW COST Global production using PRODUC high-tech developments TION Low logistics and the world's leading High level of costs “know-how” under employment: YES, 1=6 Industry 4.0 approach Presence of YES own and participation in manufacturing global value chains base / proximity to sources of raw materials YES 2 Global automotive trends: Ukrainian choices Alternative 1 Global production using the Added value resource base and low-skilled up to 14% labor Alternative 2 Ukraine – the second China in low Added value cost production Global production using high-tech >50% developments and the world's leading “know-how” under Industry 4.0 approach 3 * World Bank data 2013 Exemplary case 74 factories around the world extended production facilities built under low cost 37 production principle 4 Ukraine as low cost production site Developers of automotive Extended production facilities technologies (OEMs) Germany China Slovakia Czech Republic USA France Turkey Romania Japan South Korea China Ukraine? 5 Competitive advantages of Ukraine Logistics international 4 transport corridors seaports 18 (including Crimea) 11 river ports 22 kilometers of k. railways -

Business Herald International Law&Business Business New S in T E R

1 digest nationaL economic reLations Law&business business news internationaL ter n i s w e n s s e n i s u b s s e n i s u b & w a E L C STRY U ND I CHAMBER COMMER OF AND UKRAINIAN INTERNATIONAL BUSINESS HERALD business news ing for the new markets, the Klei UKRAINE AND SAUDI ARABIA struction cost is estimated at 700-800 Adhesive Machinery implements the WILL JOINTLY CONSTRUCT AIR- mln dollars. international quality standards, ISO PLANES The Ukrlandfarming structure 9001 including, and develops pro- includes 111 horizontal grain storage duction. «Taqnia Aeronotics», a daughter facilities, 6 seed plants, 6 enimal feed entity of the Saudi company for de- plants, 6 sugar plants and 2 leather The main field of the company activity – supply of hi-tech equipment velopment and investments and «An- producing plants as well as an egg to glue various materials. The com- tonov» State company have signed products plant «Imperovo Foods», 19 pany designers develop machines the agreement on development and poultry-breeding plants, 9 hen farms, according to the client requirements production of the light transport plane 3 poultry farms, 3 selection breeding and their high-class specialists ma- An- 132 in Saudi Arabia. The main farms, 3 long-term storage facilities terialize their ideas in metal. That’s goal of the agreement is to fulfill a and 19 meat-processing plants. number of tasks in aviation construc- why the company machines meet tion and technology transfer to Saudi the world requirements. But they are Arabia as well as to train Saudi per- much cheaper. -

European Business Club

ASSOCIATION АССОЦИАЦИЯ OF EUROPEAN BUSINESSES ЕВРОПЕЙСКОГО БИЗНЕСА РОССИЙСКАЯ ФЕДЕРАЦИЯ, RUSSIAN FEDERATION 127473 Москва ул. Краснопролетарская, д. 16 стр. 3 Ulitsa Krasnoproletarskaya 16, bld. 3, Moscow, 127473 Тел. +7 495 234 2764 Факс +7 495 234 2807 Tel +7 495 234 2764 Fax +7 495 234 2807 [email protected] http://www.aebrus.ru [email protected] http://www.aebrus.ru 12th May, 2012 Moscow PRESS RELEASE The Year Continues Strong for New Cars and Light Commercial Vehicles in Russia • Sales of new passenger cars and LCVs in Russia increased by 14% in April, 2012 • Among the top ten bestselling models so far, ten are locally produced According to the AEB Automobile Manufacturers Committee (AEB AMC), April, 2012 saw the sales of new cars and light commercial vehicles in Russia increase by 14% in comparison to the same period in 2011. This April, 266,267 units were sold; this is 33,189 units more than in April, 2011. From January to April, 2012 the percentage sales of new cars and light commercial vehicles in Russia increased by 18% in comparison to the same period in 2011 or by 135,066 more sold units. David Thomas, Chairman of the AEB Automobile Manufacturers Committee commented: "The solid growth of the Russian automotive market continues into the second quarter. Although the pace of the year on year growth is stabilising to less than 15% in recent months, we still feel that the AEB full year forecast for passenger cars and light commercial vehicles should be increased by 50,000 units to 2.85 mln." -------------------------------------------------------------- Attachments: 1. -

Impact of Political Course Shift in Ukraine on Stock Returns

IMPACT OF POLITICAL COURSE SHIFT IN UKRAINE ON STOCK RETURNS by Oleksii Marchenko A thesis submitted in partial fulfillment of the requirements for the degree of MA in Economic Analysis Kyiv School of Economics 2014 Thesis Supervisor: Professor Tom Coupé Approved by ___________________________________________________ Head of the KSE Defense Committee, Professor Irwin Collier __________________________________________________ __________________________________________________ __________________________________________________ Date ___________________________________ Kyiv School of Economics Abstract IMPACT OF POLITICAL COURSE SHIFT IN UKRAINE ON STOCK RETURNS by Oleksii Marchenko Thesis Supervisor: Professor Tom Coupé Since achieving its independence from the Soviet Union, Ukraine has faced the problem which regional block to integrate in. In this paper an event study is used to investigate investors` expectations about winners and losers from two possible integration options: the Free Trade Agreement as a part of the Association Agreement with the European Union and the Custom Union of Russia, Belarus and Kazakhstan. The impact of these two sudden shifts in the political course on stock returns is analyzed to determine the companies which benefit from each integration decisions. No statistically significant impact on stock returns could be detected. However, our findings suggest a large positive reaction of companies` stock prices to the dismissal of Yanukovych regime regardless of company`s trade orientation and political affiliation. -

![Pdf [2019-05-25] 21](https://docslib.b-cdn.net/cover/2261/pdf-2019-05-25-21-742261.webp)

Pdf [2019-05-25] 21

ISSN 1648-2603 (print) VIEŠOJI POLITIKA IR ADMINISTRAVIMAS ISSN 2029-2872 (online) PUBLIC POLICY AND ADMINISTRATION 2019, T 18, Nr. 3/2019, Vol. 18, Nr. 3, p. 46-58 The World Experience and a Unified Model for Government Regulation of Development of the Automotive Industry Illia A. Dmytriiev, Inna Yu. Shevchenko, Vyacheslav M. Kudryavtsev, Olena M. Lushnikova Department of Economics and Entrepreneurship Kharkiv National Automobile and Highway University 61002, 25 Yaroslav Mudriy Str., Kharkiv, Ukraine Tetiana S. Zhytnik Department of Social Work, Social Pedagogy and Preschool Education Bogdan Khmelnitsky Melitopol State Pedagogical University 72300, 20 Hetmanska Str., Melitopol, Ukraine http://dx.doi.org/10.5755/j01.ppaa.18.3.24720 Abstract. The article summarises the advanced world experience in government regulation of the automotive industry using the example of the leading automotive manufacturing countries – China, Japan, India, South Korea, the USA, and the European Union. Leading approach to the study of this problem is the comparative method that has afforded revealing peculiarities of the primary measures applied by governments of the world to regulate the automotive industry have been identified. A unified model for government regulation of the automotive industry has been elaborated. The presented model contains a set of measures for government support for the automotive industry depending on the life cycle stage (inception, growth, stabilisation, top position, stagnation, decline, crisis) of the automotive industry and the -

Statistical Testing of Key Effectiveness Indicators of the Companies (Case for Ukraine in 2012)

1 Vladimir Ponomarenko ГОДИНА XXIII, 2014, 4 Iryna Gontareva2 Oleksandr Dorokhov3 STATISTICAL TESTING OF KEY EFFECTIVENESS INDICATORS OF THE COMPANIES (CASE FOR UKRAINE IN 2012) The system efficiency of the company functioning depends on the quality potential, level of functional organization and operativeness of management decisions. All these aspects need to be shown results indicators of enterprises. Under effectiveness is to be understood the degree of achieve of the strategic goals of the enterprises. The most well-known base of the company functioning evaluating is model of balanced scorecard (BSC) of R. Kaplan and D. Norton. This system includes four aspects: financial, customer, internal business processes, training and development of staff. The purpose of this paper is the statistical testing of possibility to separate key effectiveness indicators for these groups and determination of their composition. With the use of multivariate factor analysis was identified the most significant indicators of the effectiveness of engineering companies. The hypothesis of R. Kaplan and D. Norton about the allocation of the four groups of key effectiveness indicators has been confirmed. JEL: C4; D2; O25 1. Introduction The system efficiency of the company functioning depends on the quality potential, level of functional organization and operativeness of management decisions. All these aspects need to be shown in results indicators of enterprises [1]. Effectiveness of enterprises depends on the level of conformity the real or possible results and goals, i.e. the degree of achievement of the strategic goals of enterprise functioning. For any company the result has the life cycle and goes through three phases: a) the desired result, , i.e. -

EAVEX Daily ENG Oct 13.Indd

Market Monitor October 13, 2011 Market Update STOCK MARKET PERFORMANCE Equity UX Index RTS Index* WIG 20 Index* 2,500 Local stocks again lagged strong gains seen on European bourses on 2,250 Wednesday (Oct 12), as Ukraine continued to receive a dressingdown from EU leaders over the conviction of former PM Yulia Tymoshenko. 2,000 The approval by Slovakia’s parliament of an increase in the EU’s bank 1,750 bailout fund fueled a rise of more than 2% in Frankfurt and Paris, 1,500 while the UX index managed a gain of only 0.5% to 1,327 points. The 1,250 11-Jul 25-Jul 8-Aug 22-Aug 5-Sep 19-Sep 3-Oct day’s best performer was volume leader Motor Sich, which added * rebased 1.5% on turnover of UAH 13mn. Other top liquid names, including CentrEnergo, Alchevsk Steel, Azovstal, and Ukrsotsbank, were up MARKET INDEXES by between 0.5% and 1%. In London, Ferrexpo continued its strong Last 1D ch 1M ch YTD rebound on fading global recession fears, picking up another 7.9% to UX 1326.4 0.7% 12.7% 45.7% RTS 1407.8 3.9% 13.4% 20.5% USD 3.30. WIG20 2316.7 2.4% 3.0% 15.6% MSCI EM 923.2 1.5% 7.0% 19.8% Fixed Income S&P 500 1207.3 1.0% 4.6% 4.0% Ukrainian sovereign Eurobonds saw a broad rebound on Wednesday. Ukrainian midterm Eurobonds added 2.0p.p. 84.0/88.0 UX INTRADAY OCTOBER 12, 2011 (10.70%/9.58%), while longterms rose by 4.0p.p. -

Automotive Market in Russia and the CIS Industry Overview February 2010 Contents

Automotive market in Russia and the CIS Industry overview February 2010 Contents Opening statement .............................................................................. 1 Russian economy ..................................................................................2 Russian automotive market in a global context ...................................... 4 Russian automotive industry ................................................................ 6 Light vehicle market ............................................................................. 7 Commercial vehicle (CV) market ......................................................... 10 Automotive components market ..........................................................11 Passenger car loan market .................................................................. 12 Dealership networks ........................................................................... 13 Automotive logistics ........................................................................... 14 CIS automotive markets ...................................................................... 15 Ukraine ......................................................................................... 15 Kazakhstan ................................................................................... 16 Belarus ......................................................................................... 17 Uzbekistan .................................................................................... 18 Ernst & Young’s involvement -

2 General Description of the Russian-Made Vehicle Fleet

;-.. ; : s -- 0--21297 .4 { Public Disclosure Authorized VehicleFle'et Public Disclosure Authorized Characterizationin CentralAsia and, the Caucasus Public Disclosure Authorized Reportfor the RegionalStudy on: CleanerTransportation FuelIs for UrbanAir QualityImprovement Public Disclosure Authorized inCentralAsia -and the Caucasus Vehicle Fleet Characterization in Central Asia and the Caucasus Report for the Regional Study on: Cleaner Transportation Fuels for Urban Air Quality Improvement in Central Asia and the Caucasus Canadian International Development Agency Joint UNDPlWorld Bank Energy Sector ManagementAssistance Programme (ESMAP) Contents Acknowledgments ............................................... vii Abbreviations and Acronyms ............................................... ix Executive Summary ............................................... xi Vehicle Technology in Central Asia and the Caucasus........................................ xii Fleet Octane Requirements ........................................ xiii Inspection and Maintenance Programs ........................................ xiv Uzbekistan's Natural Gas Conversion Program ........................................ xvi Conclusions and Recommendations ....................................... xvii 1 Introduction ................................................ 1 1.1 Objectives .1 1.2 Background .2 Impact of Fuel on Vehicle Emissions .2 Long Range Effects of Emissions .2 Climate Change and Greenhouse Gases .2 Impact of Fuel on Vehicle Technology. 3 1.3 Study Methodology.3 -

2017 Annual Report Çâ³ò

Annual 2017 report 2017 2 UKRGASBANK 3 ANNUAL REPORT TABLE OF CONTENTS 1. Brand Identity ................................................................................................................. 7 1.1. Composition of the Supervisory Board of UKRGASBANK .....................................8 1.2. Composition of the Board (as of 01.01.2018) .....................................................9 1.3. Bank Executives, Non-Members of the Board (as of 01.01.2018) .....................11 1.4. Mission. Strategic Goals. Strategy for 2018 .......................................................12 1.5. ECO-Banking Implementation ............................................................................13 1.6. Licences and Permits .........................................................................................17 1.7. Affiliated Persons ...............................................................................................19 1.8. Organizational Framework (as of 01.01.2018) ..................................................20 1.9. Personnel ...........................................................................................................22 1.10. Our History ..........................................................................................................23 1.11. Ratings ...............................................................................................................31 1.12. Financial Indicators Overview for 2017 ..............................................................34 1.13. Membership -

Lutsk Intercultural Profile

City of Lutsk Intercultural Profile This report is based upon the visit of the CoE expert team on 1-4 July 2017, comprising Kseniya Khovanova-Rubicondo and Phil Wood. It should ideally be read in parallel with the Council of Europe’s response to Odessa’s ICC Index Questionnaire but, at the time of writing, the completion of the Index by the City Council is still a work in progress. 1. Introduction Lutsk lies in northwestern Ukraine not far from the borders with Poland and Belarus, and has a population of 217,103 (2015 est.). It was the main centre of the historic region of Volhynia and is now the administrative centre of the Volyn Oblast (population 1,036,891[2005]). Lutsk has the status of a city of oblast significance. A complex history of conquest and shifting borders has seen it part of Lithuania, Russia, Poland, the Soviet Union as well as Ukraine, giving the area a rich cultural heritage. Lutsk itself is built upon an appreciation of migration and diversity. King Vytautas the Great founded the town itself by importing colonists (mostly Jews, Tatars, and Karaims). The town grew rapidly, and by the end of the 15th century there were 19 Orthodox and two Catholic churches. In 1939 Lutsk was a prosperous city with a multiethnic population of which Jews and Poles were the largest groups, but invasion by the Soviet Union and then by Germany proved a disaster, with mass deportations and murders over almost a decade, by the end of which Lutsk was ethnically an almost exclusively Ukrainian city. -

Project Document

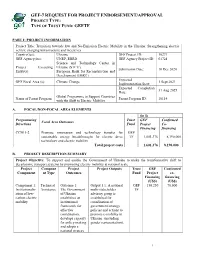

GEF-7 REQUEST FOR PROJECT ENDORSEMENT/APPROVAL PROJECT TYPE: TYPE OF TRUST FUND: GEFTF PART I: PROJECT INFORMATION Project Title: Transition towards low and No-Emission Electric Mobility in the Ukraine: Strengthening electric vehicle charging infrastructure and incentives Country(ies): Ukraine GEF Project ID: 10271 GEF Agency(ies): UNEP, EBRD GEF Agency Project ID: 01724 Science and Technology Center in Project Executing Ukraine (STCU), Submission Date: 10 Dec 2020 Entity(s): European Bank for Reconstruction and Development (EBRD) Expected GEF Focal Area (s): Climate Change 1 Sept 2021 Implementation Start: Expected Completion 31 Aug 2025 Date: Global Programme to Support Countries Name of Parent Program Parent Program ID: 10114 with the Shift to Electric Mobility A. FOCAL/NON-FOCAL AREA ELEMENTS (in $) Programming Trust GEF Confirmed Focal Area Outcomes Directions Fund Project Co- Financing financing CCM 1-2 Promote innovation and technology transfer for GEF sustainable energy breakthroughs for electric drive TF 1,601,376 8,190,000 technology and electric mobility Total project costs 1,601,376 8,190,000 B. PROJECT DESCRIPTION SUMMARY Project Objective: To support and enable the Government of Ukraine to make the transformative shift to decarbonize transport systems by promoting electric mobility at national scale Project Compone Project Project Outputs Trust GEF Confirmed Component nt Type Outcomes Fund Project co- Financing financing (US$) (US$) Component 1: Technical Outcome 1: Output 1.1: A national GEF 150,250 70,000 Institutionaliz Assistance The Government multi-stakeholder TF ation of low- of Ukraine advisory group is carbon electric establishes an established for mobility institutional coordination of framework for government strategy, effective policies and actions to coordination, promote e-mobility in develops capacity Ukraine.