Kofola Holding (Slovakia)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TRADITIONAL Slovak MEALS SOUPS OUR DELICIOUS

STarters SOUPS (1, 9) Tartare steak (1, 3, 6, 10) . 100g 12,50 € Chicken Soup . 0,33l 3,90 € Finely shredded beef sirloin with chili, onion, Chicken Soup with chicken, carrots and egg and mustard home-made egg noodles (0) Mozarella di bufala (1, 7, 8) . 125g 9,90 € Kapustnica (Slovak Sauerkraut Soup) . 0,33l 4,90 € Mozzarella di Bufala with rocket spinach salad, Kapustnica (Slovak Sauerkraut Soup) with roasted sausage, grilled cherry tomatoes and crispy pesto baguette boletus and smoked pork (7) Marinated Camembert (7) . 120g 5,90 € Toscana Tomato Soup . 0,33l 4,20 € Camembert cheese marinated in garlic, chili Toscana Tomato Soup with peeled tomatoes, pieces of onions, and green spices garlic, sliced parmesan and fresh basil ASPIC (1) . 250g 6,90 € Aspic with meat and carrots, served with onions and homemade bread It‘s not recommended for the non-heat treated dishes to be consumed by children, pregnant women, nursing women and people with impaired immunity . Grapefruit - orange Lemonade with orange OUR DELICIOUS with ginger and grenadine syrup LEMONADES Lime Elderberry cucumber 1l - 6,50€, 0,5l - 3,50€ with mint lemonade with mint TRADITIONAL sLOVAK MEALS Chicken Liver roasted on butter (1, 7) . 120g 8,90 € Strapačky (1, 3) . 250g 8,50 € Thin slices of roasted chicken liver with onion, Potato dumplings with barrel sauerkraut and bacon served with home-made bread, tomatoes and rucola Bavarian “Schweinshaxe“ (pork knee) (0) . 400g 12,90 € Dumplings with sheep cheese and bacon (1, 3, 7) 250g 8,90 € Oven roasted pork drumstick with a crispy crust served Potato dumplings with sheep cheese and crisp bacon on a wooden plate with horseradish and cabbage salad For each 100 grams of cooked food plus is extra charge 3,00 € Dumplings with sheep cheese, . -

Vysoká Škola Báňská – Technická Univerzita Ostrava Ekonomická Fakulta

CORE Metadata, citation and similar papers at core.ac.uk Provided by DSpace at VSB Technical University of Ostrava VYSOKÁ ŠKOLA BÁŇSKÁ – TECHNICKÁ UNIVERZITA OSTRAVA EKONOMICKÁ FAKULTA KATEDRA MANAGEMENTU Výzkum známosti značky „Kofola“ Research on Brand-Consciousness of „Kofola“ Student: Jana Krpcová Vedoucí bakalářské práce: Dr. Ing. Hana Svobodová Ostrava 2010 Prohlášení Místopřísežně prohlašuji, že jsem bakalářskou práci Výzkum známosti značky „Kofola“ vypracovala samostatně pod vedením Dr. Ing. Hany Svobodové, a uvedla jsem v seznamu literatury všechny použité literární a odborné zdroje. V Kozlovicích dne 7. 5. 2010 ____________________________ vlastnoruční podpis autora Obsah 1. Úvod .........................................................................................................................5 2. Teorie známosti značky .............................................................................................6 2.1 Popis značky........................................................................................................6 2.2 Historie značky....................................................................................................7 2.3 Práce se značkou..................................................................................................9 2.4 Posuzování značky a úrovně značky ..................................................................14 2.5 Strategie používání značky ................................................................................14 2.5.1 Rozpínání v rámci výrobkové -

Royal Crown Bottling Company Of

ROYAL CROWN BOTTLING COMPANY OF WINCHESTER, INCORPORATED 10/17/12 TELEPHONE NUMBER (540) 667-1821 FAX NUMBER (540) 667-8040 Wholesale Price List ROYAL CROWN BOTTLING COMPANY OF CHARLES TOWN, INCORPORATED TELEPHONE NUMBER(304) 725-8100 FAX NUMBER (304) 725-9413 PRODUCT/PACKAGE/UPC CODES WHOLESALE PRICE SUGGESTED RETAILS Mt Dew Energy Drinks (plastic) AMP Focus Mixed Berry 16 oz can (12 loose) $19.20 $1.99 012000126338 Item: 133540 VA , MD & WV 20% Margin of Profit AMP Boost Grape 16 oz can (12 loose) $19.20 $1.99 012000382505 Item: 133541 VA, MD & WV 20% Margin of Profit AMP Boost Cherry 16 oz can (12 loose) $1.99 19.20 012000126352 Item: 133542 VA , MD & WV 20% Margin of Profit AMP Boost Original 16 oz 12 pk $1.99 $19.20 012000016431 Item: 133505 20% Margin of Profit VA,MD&WV AMP Boost Original16 oz. 6-4pks $7.89 $38.00 012000017568 Item:133510 VA,MD&WV 20% Margin of Profit PRODUCT/PACKAGE/UPC CODES WHOLESALE PRICE SUGGESTED RETAILS DEER PARK NATURAL SPRING WATER 20 oz Non-Returnable (24-loose) $19.80 $1.19 each 082657077215 Item: 129950 VA, MD & WV 20% Margin of Profit PRODUCT/PACKAGE/UPC CODES WHOLESALE PRICE SUGGESTED RETAILS VINTAGE WATER 1 Liter Non-Returnable (12 per case) $11.00 $1.19 072521051021 Item: 129710 VA, MD & WV 20% Margin of Profit 20 oz Non-Returnable (24 loose) $12.00 $.69 072521051014 Item 129700 VA, MD & WV 20% Margin of Profit PRODUCT/PACKAGE/UPC CODES WHOLESALE PRICE SUGGESTED RETAILS 10 oz Non-Returnable Glass Bottles $10.25 6/$3.19 (4-6 pack) 20% Margin of Profit VA , MD & WV 078000001686 Item: 103100 Canada -

Le Cas Du Marché Des Colas Philippe Robert-Demontrond, Anne Joyeau and Christine Bougeard-Delfosse

Document generated on 09/28/2021 4:33 a.m. Management international Gestiòn Internacional International Management La sphère marchande comme outil de résistance à la mondialisation : le cas du marché des colas Philippe Robert-Demontrond, Anne Joyeau and Christine Bougeard-Delfosse Volume 14, Number 4, Summer 2010 Article abstract Day after day, the world is becoming more and more globalized. Financial URI: https://id.erudit.org/iderudit/044659ar movements, transports, means of communication facilitate the emergence of DOI: https://doi.org/10.7202/044659ar this phenomenon. Nevertheless, globalization is not without consequences on the local populations who perceive this evolution as a threat for their identity See table of contents and their culture. Through the creation or resurgence of an offer of foodstuffs, and more particularly through a world and plethoric offer of local colas, the consumer is showing resistance and refuses to standardize his consumption. Publisher(s) The commercial success of those altercolas cannot be denied and many dimensions are bound to their consumption. HEC Montréal et Université Paris Dauphine ISSN 1206-1697 (print) 1918-9222 (digital) Explore this journal Cite this article Robert-Demontrond, P., Joyeau, A. & Bougeard-Delfosse, C. (2010). La sphère marchande comme outil de résistance à la mondialisation : le cas du marché des colas. Management international / Gestiòn Internacional / International Management, 14(4), 55–68. https://doi.org/10.7202/044659ar Tous droits réservés © Management international / International This document is protected by copyright law. Use of the services of Érudit Management / Gestión Internacional, 2010 (including reproduction) is subject to its terms and conditions, which can be viewed online. -

A Neoconventional Trademark Regime for "Newcomer" States

KHOURYFINALIZED_TWO 3/31/2010 2:02:20 AM A NEOCONVENTIONAL TRADEMARK RÉGIME FOR "NEWCOMER" STATES Amir H. Khoury* INTRODUCTION This research constitutes a (natural) follow-up to an earlier published research paper in which I assessed, through data analysis, the effects of the Paris-TRIPS Conventional Trademark Régime (“CTR”) on countries.1 In that research I devised and applied the Trademark Potential concept. Using that concept I demonstrated that if a country has an inherent Trademark Deficit because of the structure of its industry, the CTR cannot effectively benefit that country's economy. My empirically-based research has shown that the Trademark Potential of a country is not contingent upon its laws’ compatibility with CTR. I have established that CTR compliant laws do not necessarily facilitate market entry for newcomers originating in developing countries. Thus, in that research I have refuted the existence of some of the benefits that are generally associated with CTR. This present research is geared towards considering various avenues for remedying the pitfalls of the CTR by introducing a NeoConventional Trademark Régime (“NCTR”). The aim of this proposed régime would be to facilitate the creation and market entry of brands originating in developing countries into their respective national markets and beyond. In this regard, this research constitutes the culmination of my earlier research because it transcends the diagnostic role pertaining to the CTR and ventures into the realm of offering workable solutions thereto. * Lecturer, Tel Aviv University, Faculty of Law. This article was written while I was a Cegla Fellow. My sincere thanks go to the Cegla Center for Interdisciplinary Research of the Law at the Faculty of Law, Tel Aviv University, for its support of this research project. -

Drink Menu MIXED ALCOHOLIC BEVERAGES

Drink Menu MIXED ALCOHOLIC BEVERAGES Devín Signatures 140 ml Dunaj a Morava 13,90 € Apple juice, sparkling wine, edible gold, grapefruit bitters, pink grapefruit peel, honey syrup 130 ml Limes Romanus 14,90 € Borovička DOMOVINA, elderberry syrup, buckthorn juice, salty bitters 110 ml Rastislav 14,90 € RON SANTIAGO DE CUBA Rum Añejo Superior 11 AÑOS, Bentiana, chocolate bitters, apple juice, apple chips, bitter chocolate 295 ml Grand Reserva Tea 13,90 € Lepanto solera gran reserva brandy, Pimente d´Espelette liqueur, lemon juice, cascara infuse tonic, soda, tortilla chips, mango-chilli sauce 90 ml Prezident 8,90 € RON SANTIAGO DE CUBA Carta Blanca rum, La Copa Blanco white sweet vermouth, triple sec curacao liqueur, strawberry syrup, orange peel Domovina Signatures 150 ml Detvan 9,90 € Borovička DOMOVINA, rosemary, black juniper berry, natur light tonic 70 ml Živý Bič 8,90 € Borovička DOMOVINA, white dry vermouth La Copa Extra Seco 90 ml Nox et Solitudo 8,90 € Pear brandy DOMOVINA, red sweet vermouth La Copa Rojo, DARK 150 ml Odsúdený k večitej žízni 8,90 € Plum brandy DOMOVINA, mirabelle syrup, dried plum, tonic 300 ml Hájnikova Žena 7,90 € Apricot brandy DOMOVINA, almond syrup, lime juice, sparkling water 1 Spritz Drinks 340 ml Albarizo 12,90 € Tio Pepe sherry fino, lime, Indian tonic, Tio Pepe Palomino Fino sherry, Triple sec curacao liqueur, sparkling wine, grapefruit peel 170 ml Americana 11,90 € La Copa Rojo red sweet vermouth, Demänovka Bitter, orange bitters, Indian tonic, orange peel, mint Gin & Tonic 250 ml G&T of Love 9,90 € -

CPY Document

THE COCA-COLA COMPANY 795 795 Complaint IN THE MA TIER OF THE COCA-COLA COMPANY FINAL ORDER, OPINION, ETC., IN REGARD TO ALLEGED VIOLATION OF SEC. 7 OF THE CLAYTON ACT AND SEC. 5 OF THE FEDERAL TRADE COMMISSION ACT Docket 9207. Complaint, July 15, 1986--Final Order, June 13, 1994 This final order requires Coca-Cola, for ten years, to obtain Commission approval before acquiring any part of the stock or interest in any company that manufactures or sells branded concentrate, syrup, or carbonated soft drinks in the United States. Appearances For the Commission: Joseph S. Brownman, Ronald Rowe, Mary Lou Steptoe and Steven J. Rurka. For the respondent: Gordon Spivack and Wendy Addiss, Coudert Brothers, New York, N.Y. 798 FEDERAL TRADE COMMISSION DECISIONS Initial Decision 117F.T.C. INITIAL DECISION BY LEWIS F. PARKER, ADMINISTRATIVE LAW JUDGE NOVEMBER 30, 1990 I. INTRODUCTION The Commission's complaint in this case issued on July 15, 1986 and it charged that The Coca-Cola Company ("Coca-Cola") had entered into an agreement to purchase 100 percent of the issued and outstanding shares of the capital stock of DP Holdings, Inc. ("DP Holdings") which, in tum, owned all of the shares of capital stock of Dr Pepper Company ("Dr Pepper"). The complaint alleged that Coca-Cola and Dr Pepper were direct competitors in the carbonated soft drink industry and that the effect of the acquisition, if consummated, may be substantially to lessen competition in relevant product markets in relevant sections of the country in violation of Section 7 of the Clayton Act, as amended, 15 U.S.C. -

Kofola Group | Sustainability

Kofola Group WE OPERATE WITH RESPECT TO NATURE, SOCIETY AND INDIVIDUALS CONTENTS Sustainability is not a new issue at Kofola. Because we are not fond of fashionable words, however, you will hear us speak rather of consideration and respect for nature. Since 2010, CARBON FOOTPRINT we have been focusing intently on major issues, such as water protection, minimization of waste and carbon neutrality, which we would like to achieve by the end of the decade. WATER PROTECTION Of course, the life of each of our products starts at a more basic level – with the ingredients. We prefer local suppliers; ideally those whom we know personally. Thanks to INGREDIENTS AND PRODUCTS them, we are able to guarantee first-class product quality for our customers and, at the same time, support the economic ecosystem in the place where we live and do business. WASTE-MANAGEMENT POLICY We enjoy the constant search for new ways to create healthy beverages and to do business in symbiosis with nature. Therefore, we do not undertake one-off projects. My major goal is to bring sustainable thinking into the day-to-day running of the company, into every single LOCALISM decision – from limiting single-serve milk for coffee to protecting water sources. This is the only way to ensure that we at Kofola can be consistently proud of the things we do. PEOPLE Jannis Samaras Kofola Group CEO CARBON FOOTPRINT WATER PROTECTION INGREDIENTS AND PRODUCTS WASTE-MANAGEMENT POLICY LOCALISM PEOPLE SUMMARY A COMPREHENSIVE APPROACH IS THE CORNERSTONE OF OUR We process We preferentially ingredients purchase healthy SUSTAINABILITY PHILOSOPHY with environmentally friendly local ingredients production processes We strive to find We strive to limit our sensible uses for carbon footprint in the Sustainable initiatives affect the entire lifecycle THE IDEAL IS THE the waste generated transport of products of our products, from ingredients, through production by our activities circular technology, to the means of transport. -

Soda Handbook

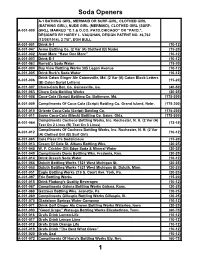

Soda Openers A-1 BATHING GIRL, MERMAID OR SURF-GIRL, CLOTHED GIRL (BATHING GIRL), NUDE GIRL (MERMAID), CLOTHED GIRL (SURF- A-001-000 GIRL), MARKED “C.T.& O.CO. PATD.CHICAGO” OR “PATD.”, DESIGNED BY HARRY L. VAUGHAN, DESIGN PATENT NO. 46,762 (12/08/1914), 2 7/8”, DON BULL A-001-001 Drink A-1 (10-12) A-001-047 Acme Bottling Co. (2 Var (A) Clothed (B) Nude) (15-20) A-001-002 Avon More “Have One More” (10-12) A-001-003 Drink B-1 (10-12) A-001-062 Barrett's Soda Water (15-20) A-001-004 Bay View Bottling Works 305 Logan Avenue (10-12) A-001-005 Drink Burk's Soda Water (10-12) Drink Caton Ginger Ale Catonsville, Md. (2 Var (A) Caton Block Letters A-001-006 (15-20) (B) Caton Script Letters) A-001-007 Chero-Cola Bot. Co. Gainesville, Ga. (40-50) A-001-063 Chero Cola Bottling Works (20-25) A-001-008 Coca-Cola (Script) Bottling Co. Baltimore, Md. (175-200) A-001-009 Compliments Of Coca-Cola (Script) Bottling Co. Grand Island, Nebr. (175-200) A-001-010 Oriente Coca-Cola (Script) Bottling Co. (175-200) A-001-011 Sayre Coca-Cola (Block) Bottling Co. Sayre, Okla. (175-200) Compliments Cocheco Bottling Works, Inc. Rochester, N. H. (2 Var (A) A-001-064 (12-15) Text On 2 Lines (B) Text On 3 Lines) Compliments Of Cocheco Bottling Works, Inc. Rochester, N. H. (2 Var A-001-012 (10-12) (A) Clothed Girl (B) Surf Girl) A-001-065 Cola Pleez It's Sodalicious (15-20) A-001-013 Cream Of Cola St. -

Scotch Whisky, They Often Refer to A

Catalogue Family Overview Styles About the Font LL Catalogue is a contemporary a rising demand for novels and ‘news’, update of a 19th century serif font of these fonts emerged as symptom of Catalogue Light Scottish origin. Initially copied from a new culture of mass education and an old edition of Gulliver’s Travels by entertainment. designers M/M (Paris) in 2002, and In our digital age, the particularities Catalogue Light Italic first used for their redesign of French of such historical letterforms appear Vogue, it has since been redrawn both odd and unusually beautiful. To from scratch and expanded, following capture the original matrices, we had Catalogue Regular research into its origins and history. new hot metal types moulded, and The typeface originated from our resultant prints provided the basis Alexander Phemister’s 1858 de- for a digital redrawing that honoured Catalogue Italic sign for renowned foundry Miller & the imperfections and oddities of the Richard, with offices in Edinburgh and metal original. London. The technical possibilities We also added small caps, a Catalogue Bold and restrictions of the time deter- generous selection of special glyphs mined the conspicuously upright and, finally, a bold and a light cut to and bold verticals of the letters as the family, to make it more versatile. Catalogue Bold Italic well as their almost clunky serifs. Like its historical predecessors, LL The extremely straight and robust Catalogue is a jobbing font for large typeface allowed for an accelerated amounts of text. It is ideally suited for printing process, more economical uses between 8 and 16 pt, provid- production, and more efficient mass ing both excellent readability and a distribution in the age of Manchester distinctive character. -

Online Izdanje Priručnika

online izdanje priručnika Udruga Žmergo jedi lokalno, misli globalno priručnik globalnog obrazovanja za nastavnike online izdanje priručnika kovačić marko | kovačić diana | traub helena Udruga Žmergo Opatija, 2017. IMPRESSUM | Naslov publikacije: Jedi lokalno, misli globalno Priručnik globalnog obrazovanja za nastavnike online izdanje priručnika | Nakladnik: Udruga Žmergo V. C. Emina 3, 51410 Opatija | e-mail: [email protected] | tel: (051) 271 459 www.zmergo.hr | Autori: Kovačić Marko | Kovačić Diana | Traub Helena | Urednice: Kovačić Diana | Traub Helena | Recenzentice: Ćulum Bojana | Košutić Iva | Prijevod materijala s engleskog jezika: Marković Ana | Lektura: Marković Ana | Grafčko oblikovanje: Širola Borka / Wanda | Opatija, 2017. ISBN 978-953-59747-1-0 Posebna zahvala Alessiu Surianu, Micheleu Curamiu, Sari Marazzini, Valentini Rizzi, Sa- nji Albaneže za doprinos u razvoju priprema nastavnih jedinica globalnog obrazovanja. U ovoj publikaciji uporabljeni su izrazi napisani u muškom rodu, a odnose se kao neu- tralni na sve osobe, neovisno o njihovu spolu ili rodu. Ovaj priručnik ostvaren je uz fnancijsku potporu Europske unije. Za sadržaj priručnika odgovorni su isključivo autori i izdavač te ne odražava nužno stavove Europske unije. Stajališta izražena u ovoj publikaciji ne odražavaju nužno stajalište Ureda Vlade Repu- blike Hrvatske za udruge. Europsku uniju čini 28 država članica, koje su odlučile postupno spajati svoje znanje, resurse i sudbine. Zajedno su, tijekom 50 godina širenja, stvorile područje stabilnosti, demokracije i -

Munduko Kola-Freskagarriak

08 IKAS UNITATEA Herrialdea austria munduko kola-freskagarriak Edari komertzialak, Kontsumo arduratsua, Elikagaien merkataritza multina- Landutako edukiak zionala. Gomendatutako adina 13-15 urte. Balio etikoak eta Ekonomia. Geografia, Historia, eta Biologia ere zeharka Ikasgaiak lantzen dira. Metodologiak Talde-lana, Ideia-zaparrada, Jolasa, Eztabaida gidatua, Ikerketa autonomoa. Egilea Südwind elkartea (Euskal Fondoak egokitua). Oinarrizko gaitasunak 1, 2, 3, 4, 5 / C, E • Gazteen gustuko diren edari-freskagarriak era kritikoan aztertzea. • Edarien merkatu globalaren egiturei eta kontzentrazioari buruzko ezagutzak lortzea. • Markek duten indarrari eta kontsumitzaile gisa dugun portaeraren garrantziari buruz hausnartzea. Ikasketa-helburuak • Kola-edarien osagaiei buruzko eta munduko historian izan duten eginkizunari buruzko ezagutzak lortzea. • Ekoizpen- eta merkataritza-bide alternatiboak ezagutzea. • Informazio-iturri desberdinak ulertzea eta aztertzea. • Informazioa norbere kabuz bildu, prestatu eta aurkeztea. • Argudioak eta ikuspuntu desberdinak formulatu eta adieraztea. ELIKADURA ETA HEZKUNTZA GLOBALA HEZKUNTZA FORMALEAN eathink 55 IKAs-UNITATeAReN gARApeNA 1. saioa (60’) KOLA-FRESKAGARRIEN KONTSUMOA EKonomiA 10’ 1.1 FRESKAGARRIAK ETA GU Gaia kokatzeko ikasleek galdera hauei buruz eztabaidatuko dute binaka: • Zer edari duzue gustukoen? ? • Zenbat freskagarri edaten duzue astean? ? • Gazteek freskagarri gehiegi edaten duzue? ? • Freskagarri bat edatean, ba ote dakigu zer hartzen ari garen? Emaitzak txarteletan idatzi eta ikasgelan