Full-Year 2020 Results Stadler Rail

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Half-Year Report 2021 Half-Year Results 2020 at a Glance

STADLER HALBJAHRESBERICHT 2020 HALF-YEAR REPORT 2021 HALF-YEAR RESULTS 2020 AT A GLANCE HALF-YEAR RESULTS 2021 AT A GLANCE 1.4 48.9 BILLION CHF MILLION CHF NET REVENUE EBIT Previous year: 0.9 Previous year: 5.0 3.5% 35,158 EBIT MARGIN REGISTERED SHAREHOLDERS AS AT 30 JUNE 2021 Previous year: 0.5% 31 December 2020: 34,912 3.1 BILLION CHF ORDER INTAKE 12,851 Previous year: 3.1 EMPLOYEES WORLDWIDE (average FTE 1 January to 30 June 2021) Previous year: 12,156 17.9 BILLION CHF STADLER – THE SYSTEM PROVIDER OF SOLUTIONS IN ORDER BACKLOG RAIL VEHICLE CONSTRUCTION WITH HEADQUARTERS 31 December 2020: 16.1 IN BUSSNANG, SWITZERLAND. Stadler Half-Year Report 2021 3 THIS IS WHERE FACTS AND FIGURES COME IN CONTENTS STADLER HALF-YEAR REPORT 2021 2 _ Half-Year Results 2021 at a glance 4 _ Locations at a glance 5 _ Key figures 6 _ Letter to our Shareholders CONSOLIDATED HALF-YEAR FINANCIAL STATEMENTS 10 _ Consolidated income statement 11 _ Consolidated balance sheet 12 _ Consolidated cash flow statement 13 _ Consolidated statement of changes in equity NOTES TO THE CONSOLIDATED HALF-YEAR FINANCIAL STATEMENTS 14 _ 1. The Stadler Rail Group 14 _ 2. Basis for the preparation of the financial statements 14 _ 3. Management assumptions and estimates 15 _ 4. Seasonal and other influences 15 _ 5. Segment reporting 16 _ 6. Gross margin 17 _ 7. Operating result (EBIT) 17 _ 8. Financial result 17 _ 9. Non-operating result 17 _ 10. Income taxes 18 _ 11. -

Media Release a First for Stadler: Trams for the Czech Republic

HOLD -BACK Media release PERIOD 18. Januar 2017 PAGES 3 ATTACHMENTS 1 image Bussnang, Ostrava, 18 January 2017 A first for Stadler: trams for the Czech Republic Stadler won the tender to develop and build 40 trams for the Dopravní podnik Ostrava a.s. (DPO) operating company in Ostrava. The order is worth a total of approximately CHF 45 million. The Ostrava trams are being planned and constructed by Stadler Prague. Stadler will work closely with Czech suppliers. This is the first time that Stadler has received an order for trams from the Czech Republic. Daniel Morys, Executive Director of Dopravní podnik Ostrava a.s., and Peter Jenelten, Executive Vice President Marketing & Sales at Stadler, signed the contract for the delivery of 40 adapted Tango trams. The contract between DPO and Stadler covers the delivery of 30 + 10 2-car low-floor uni-directional trams for normal gauges. The order is worth a total of approximately CHF 45 million. The trams are based on the tried- and-tested Tango design, but have been tailored to DPO requirements in Ostrava with low-floor technology and other customised adaptations to fit their unique intended purpose. Stadler Praha is overseeing project planning and engineering. Signing the contract in Ostrava, Executive Director Daniel Morys emphasised the importance of the project: “I am very satisfied with the course of this public contract, and I believe that the Swiss quality of the new trams in Ostrava will bring higher comfort for travelling, which we really request, and our passengers will be happy about the new trams.” Peter Jenelten, Executive Vice President Marketing & Sales at Stadler, added: “We are proud to be able to deliver the first trams to the Czech Republic, and we are looking forward to providing passengers in Ostrava with a very high degree of comfort and a thoroughly pleasant ride. -

ANNUAL REPORT 2020 2020 RESULTS at a GLANCE 16.1 ORDER BACKLOG in CHF BILLION NET REVENUE Previous Year: 15.0 in Thousands of CHF

ANNUAL REPORT 2020 2020 RESULTS AT A GLANCE 16.1 ORDER BACKLOG IN CHF BILLION NET REVENUE Previous year: 15.0 in thousands of CHF 3,500,000 2,800,000 2,100,000 3,200,785 3,084,948 34,912 REGISTERED SHAREHOLDERS AS AT 31.12.2020 1,400,000 Previous year: 30 419 2,000,806 700,000 0 2018 2019 2020 NET REVENUE BY GEOGRAPHICAL MARKET in thousands of CHF Germany, Austria, Switzerland: 1,502,759 4.33 Western Europe: 963,548 ORDER INTAKE Eastern Europe: 457,488 IN CHF BILLION CIS: 68,207 Previous year: 5.12 America: 83,909 Rest of the world 9,037 % 12,303 5.1 EBIT MARGIN EMPLOYEES WORLDWIDE Previous year: 6.1% (average FTE 1.1. – 31.12.2020) Previous year: 10 918 156.1 EBIT IN CHF MILLION Previous year: 193.7 STADLER – THE SYSTEM PROVIDER OF SOLUTIONS IN RAIL VEHICLE CONSTRUCTION WITH HEADQUARTERS IN BUSSNANG, SWITZERLAND. Stadler Annual Report 2020 3 SUSTAINABLE MOBILITY – 16.1 ORDER BACKLOG TRAIN AFTER TRAIN IN CHF BILLION Previous year: 15.0 Stadler has been building rail vehicles for over 75 years. The company operates in two reporting segments: the “Rolling Stock” segment focuses on the development, design and production of high-speed, intercity and re gional trains, locomotives, metros, light rail vehicles and passenger coaches. With innovative signalling solutions Stadler supports the interplay be tween vehicles and infrastructure. Our software engineers in Wallisellen develop Stadler’s own solutions in the areas of ETCS, CBTC and ATO. The “Service & Components” segment offers customers a variety of services, ranging from the supply of individual spare parts, vehicle repairs, mod erni- sation and overhauls to complete full-service packages. -

The Spanish Railway Industry Faces the New Safe, Sustainable and Connected Mobility Strategy

Mafex corporate magazine Spanish Railway Association Issue 25. November 2020 The Spanish railway industry faces the new Safe, Sustainable and Connected Mobility Strategy SPECIAL MAFEX INFORMS INTERVIEW Vitual Rail Live!1st and 2nd December 2020 Mafex held its annual General Meeting on José Luis Ábalos, Ministry of Transport, November, 11st 2020 Mobility and Urban Agenda A FONDO MAFEX ◗ Sumary 05 / EDITORIAL 06 / MAFEX INFORMS RAILACTIVATION PROJECT This initiative, led by Mafex, drives the innovative transformation of twenty European railway SMEs. EPROMAT PROJECT New cell of composites manufacturing of high efficiency in productivity and materials. 44/ SPECIAL STAFFER PROJECT SAFE, SUSTAINABLE AND CONNECTED Mafex is a member of the Railway Alliance MOBILITY STRATEGY 2030 to define the working skills required to The Safe, Sustainable and Connected promote a single European railway space. Mobility Strategy 2030, published on 17th September 2020, constitutes the EXXTRA PROJECT framework that will guide the debate The initiative seeks the professionalisa- on mobility in Spain, enriched by the tion of the competencies and services contributions of the different stakeholders of clusters towards world-class cluster in the mobility ecosystem. consolidation. THE SPANISH RAILWAY INDUSTRY MAFEX 2020 GENERAL MEETING IN THE FACE OF THE NEW STRATEGY The Association informed the Annual OF SAFE, SUSTAINABLE AND Members Meeting about last year’s CONNECTED MOBILITY progress, the incorporation of new Contribution of the railway industry to companies and the evolution of their the Mobility Strategy. more than 200 actions last year. Mafex companies’ representatives provides MAFEX INNOVATION COMMITTEE us with their view on the role of railway as The new membership of the Innovation the main character of sustainable mobility Committee consists of 20 companies and what they expect from the Public and technology centres. -

Stadler Sells Gauge Changing Facility for the City of Akhalkalaki in Georgia

Media release HOLD-BACK PERIOD 6 June 2018 DOCUMENT 2 pages ENCLOSURES None Bussnang, 6 June 2018 Stadler sells gauge changing facility for the city of Akhalkalaki in Georgia Stadler today signed a contract in Bussnang with the Georgian company Marabda-Kartsakhi-Railway LCC for the delivery of a gauge changing facility. The system will be installed in the Georgian city of Akhalkalaki near the border with Turkey and will form part of the Baku-Tbilisi-Kars Railway, which links the countries of Azerbaijan, Georgia and Turkey. Special tracks need to be fitted over a distance of 30 metres to enable trains to switch from the European standard gauge to the broad gauge used in the countries of the former Soviet Union. The gauge changing facility is suitable for rail vehicles with DB AG/Rafil Type V wheelsets produced by Bochumer Verein Verkehrstechnik GmbH in Ilsenburg. This technology was authorised by the German Federal Railway Authority (EBA) in 2006. In 2014 Stadler received an order for the delivery of 30 sleeper and dining cars from Azerbaijan national railways (ADY). These cars are intended for use on the Baku-Tbilisi-Kars-Istanbul route and are therefore equipped with DB AG/Rafil Type V wheelsets. Installing this gauge changing facility is the only way to allow completion of the journey from Baku to Istanbul without interruption. Regular services are scheduled to start in the summer of 2019. Follow Stadler on Linkedin und Facebook Page 1 | 2 About Stadler International rail vehicle construction company, Stadler, is headquartered in Bussnang in Eastern Switzerland. Founded in 1942, it has a workforce of over 7,600 based in various production, service and engineering locations across Switzerland, Germany, Spain, Poland, Hungary, the Czech Republic, Belarus and the United States. -

Reference List / Glas Trösch Ag Rail

02.10.2017/JG REFERENCE LIST / GLAS TRÖSCH AG RAIL Train Identification Train Identification Homologation Impact Speed Country of Year of the first Train Manufacture Operator / Owner Continent Other information Photo from Manufacture from Operator Standard (Test projectile) operation delivery TSI Rolling Stock Front windscreen with film Stadler Rail KISS NORDIC -- 520 km/h Sweden EUROPA 2017 Norm: heating system EN 15152 AB Transitio Regional Train Front windscreen with film Skoda Several EUROPA MSV Norm: UIC 651 440 km/h Czech Republic 1996 heating system Czech Railways Regional Train EBA Front windscreen with Bombardier 763 until 767 EUROPA DO 2010 DB Norm: 410 km/h Germany 2012 wire heating system EN 15152 Regional Train EBA Front windscreen with film Stadler Rail Several EUROPA Flirt 3 DB Norm: 410 km/h Germany 2013 heating system EN 15152 Regional Train EBA Front windscreen with film Stadler Rail -- EUROPA Flirt 3 PKP Intercity Norm: 410 km/h Poland 2013 heating system EN 15152 Regional Train TSI Rolling Stock Front windscreen with film Stadler Rail Flirt 3 Dutch Railways -- 410 km/h Netherlands EUROPA 2015 Norm: heating system EN 15152 Regional Train page 1 of 17 02.10.2017/JG REFERENCE LIST / GLAS TRÖSCH AG RAIL Train Identification Train Identification Homologation Impact Speed Country of Year of the first Train Manufacture Operator / Owner Continent Other information Photo from Manufacture from Operator Standard (Test projectile) operation delivery EBA KISS Front windscreen with film Stadler Rail WESTbahn -- Norm: 410 km/h Austria -

Delivery of EURO4000 Locomotives: Alpha Trains Consolidates Its Market Position in Spain and Portugal

Media release HOLD-BACK PERIOD 8 June 2017 DOCUMENT 2 pages ENCLOSURES 3 photos Luxembourg/Spain, 8 June 2017 Delivery of EURO4000 locomotives: Alpha Trains consolidates its market position in Spain and Portugal On 31st May 2017, the six new EURO4000 locomotives were delivered by Stadler to Alpha Trains. Four of them will be operated under a long-term leasing agreement by Medway. The acquisition of the new locomotives builds on Alpha Trains’ market position as rolling stock lessor in Spain and Portugal. The locomotives were built at the Stadler Valencia’s Albuixech plant. To perform cross-border freight transport between Spain and Portugal, the assets are equipped with the specific Spanish and Portuguese Signalling System and Radio. The EURO4000 is a proven, reliable and trusted locomotive in the Iberian market. “It is the first time that Medway has leased locomotives from Alpha Trains and we hope to continue providing Medway with our services and to support their business success,” says Fernando Pérez, Managing Director of Alpha Trains Locomotives Division. The investment in new freight assets is also an investment in a sustainable future: “Our broad portfolio of rolling stock for various needs and customer-tailored leasing solutions facilitates modal shift from road to rail and hence, reduces CO2 emissions. This contributes to the achievement of the European Union´s greenhouse gas reduction targets,” explains Shaun Mills, CEO of the Alpha Trains Group. “Stadler has successfully delivered more than 100 EURO4000 locomotives to different European rail freight operators. The robust and reliable six-axle locomotives offer high flexibility and hauling capacity, low energy consumption and reduced operational costs contributing to the profitability of the rail freight transport”, says Iñigo Parra, CEO of Stadler Valencia. -

Spectacular Transport of Double-Decker Trains for Aeroexpress

MEDIA RELEASE Bussnang/Altenrhein, 9 September 2014 Spectacular transport of double-decker trains for Aeroexpress The first six-carriage double-decker train for railway company Aeroexpress has begun its ship journey from Muttenz BL via Amsterdam to the Baltic Sea right on time. The trains will be used on the lines running from the city centre of Moscow to the three airports. The first four of a total of 25 trains are being built by Stadler Rail in Altenrhein SG on Lake Constance. They need to be transported as part of a well-planned exercise via Basel (Muttenz), Amsterdam and Sassnitz on the Baltic Sea to the Stadler factory in Minsk. As the trains in all CIS countries are essentially taller and wider than in the rest of Europe, rail transport is not an option. Even the first leg from Altenrhein SG to the river harbour at Muttenz BL provided a few challenges for the companies involved. In consultation with the authorities and the police in all the cantons passed through, a road route needed to be found which was even accessible with a vehicle of such massive proportions. Not only did height have to be considered, for example in order to prevent getting stuck when passing under a bridge, but width and length also had to be factored in. The latter two were most often an issue at crossroads. After 13 months of planning, the transport project went ahead in mid-August, and the six carriages of the first train reached Muttenz BL in good time for the scheduled loading date last Saturday. -

RAIL GROUP [email protected] Stadler Algérie Eurl Stadler US Inc

STADLER – FACTS & FIGURES 2018 FACTS & FIGURES 2018 – STADLER Stadler Rail AG Stadler Pankow GmbH Stadler Rail Valencia S.A.U. Ernst-Stadler-Strasse 1 Lessingstrasse 102 Pol. Ind. del Mediterráneo, Mitjera, nº.6 9565 Bussnang, Switzerland D-13158 Berlin, Germany ES-46550 Albuixech Valencia, Spain T +41 71 626 21 20 T +49 30 9191 1616 T +34 96 141 5000 [email protected] [email protected] [email protected] Stadler Polska Sp. z o.o. CJSC Stadler Minsk Stadler Trains Magyarország Kft. ul. Targowa 50 Zavodskaja Str. 47 Városligeti fasor 47-49 PL-08-110 Siedlce, Poland 222750 Fanipol, Dzerzhinsk County H-1071 Budapest, Hungary 01 – STADLER T +48 25 746 45 00 Region Minsk, Belarus T +36 1 327 40 60 [email protected] T +375 17 16 22 410 [email protected] RAIL GROUP [email protected] Stadler Algérie Eurl Stadler US Inc. Stadler Praha s.r.o. 14bis Rue de l’ALN, Caroubier 900 North 500 West Kutvirtova 339/5 DZ-16005 Alger, Algeria Salt Lake City, UT 84116, USA CZ-150 00 Prague, Czech Republic T +213 21 498 329 T +1 801 854 7771 T +420 257 404 900 [email protected] [email protected] [email protected] Stadler Service AG Medienstelle Stadler Rail Group Ernst-Stadler-Strasse 4 Ernst-Stadler-Strasse 1 9565 Bussnang, Switzerland 9565 Bussnang, Switzerland T +41 71 626 20 20 T +41 71 626 21 20 [email protected] [email protected] Complete addresses of all locations can be found at: www.stadlerrail.com 2018 FACTS & FIGURES -

Best Practices and Strategies for Improving Rail Energy Efficiency

U.S. Department of Transportation Best Practices and Strategies for Federal Railroad Improving Rail Energy Efficiency Administration Office of Research and Development Washington, DC 20590 DOT/FRA/ORD-14/02 Final Report January 2014 NOTICE This document is disseminated under the sponsorship of the Department of Transportation in the interest of information exchange. The United States Government assumes no liability for its contents or use thereof. Any opinions, findings and conclusions, or recommendations expressed in this material do not necessarily reflect the views or policies of the United States Government, nor does mention of trade names, commercial products, or organizations imply endorsement by the United States Government. The United States Government assumes no liability for the content or use of the material contained in this document. NOTICE The United States Government does not endorse products or manufacturers. Trade or manufacturers’ names appear herein solely because they are considered essential to the objective of this report. REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burden for this collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing this burden, to Washington Headquarters Services, Directorate for Information Operations and Reports, 1215 Jefferson Davis Highway, Suite 1204, Arlington, VA 22202-4302, and to the Office of Management and Budget, Paperwork Reduction Project (0704-0188), Washington, DC 20503. -

Meetings with Stakeholders

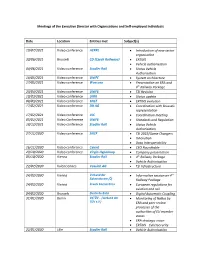

Meetings of the Executive Director with Organisations and Self-employed Individuals Date Location Entities met Subject(s) 19/07/2021 Video conference AERRL • Introduction of new sector organisation 30/06/2021 Brussels CD (Czech Railways) • ERTMS • Vehicle authorisation 04/06/2021 Video conference Stadler Rail • Status Vehicle Authorisation 18/05/2021 Video conference UNIFE • System architecture 17/05/2021 Video conference Wascosa • Presentation on ERA and 4th Railway Package 23/04/2021 Video conference UNIFE • TSI Revision 10/03/2021 Video conference UIRR • Status update 08/03/2021 Video conference SNCF • ERTMS evolution 17/02/2021 Video conference DB AG • Coordination with Brussels representation 17/02/2021 Video conference UIC • Coordination meeting 05/02/2021 Video Conference UNIFE • Standards and Regulation 18/12/2021 Video conference Stadler Rail • Status Vehicle Authorisation 27/11/2020 Video conference SNCF • TSI 2022/Game Changers • Innovation • Data Interoperability 16/11/2020 Video conference Cyient • CEO Roundtable 29/10/2020 Video conference Virgin Hyperloop • Company presentation 05/10/2020 Vienna Stadler Rail • 4th Railway Package • Vehicle Authorisation 22/07/2020 Valenciennes Vossloh AG • TSI Infrastructure 24/02/2020 Vienna Verband der • Information session on 4th Bahnindustrie (Ö) Railway Package 24/02/2020 Vienna Create Connections • European regulations for aviation and rail 04/02/2020 Brussels Deutsche Bahn • Digital Automatic Coupling 31/01/2020 Berlin VdTÜV – (Verband der • Monitoring of NoBos by TÜV e.V.) ERA and peer review processes of the authorities of EU member states • ERA strategic vision • ERTMS - Cybersecurity 22/01/2020 Lille Stadler Rail • Vehicle Authorisation 16/01/2020 Lille Ricardo Rail • 4th Railway Package • CSM 14/01/2020 Brussels ALLRAIL (Alliance of • 4th Railway Package New Rail Entrants) • ERTMS • Breaking down barriers 10/12/2019 Brussels UIP (International • Update on Transition to Union of Wagon the 4th Railway Package Keepers) 03/12/2019 St. -

Two for the Long Haul

ProgressiveThe Information Leader for the Railroad Industry JANUARY 2013 TWO FOR THE LONG HAUL A NEW LINE FOR Crude oil and PORTLAND'S domestic intermodal TRIMET business pose the greatest long-term EASTERN growth potential SHALES for BNSF as long as STILL A enough capacity’s GROWTH DRIVER in place OUR 14TH ANNUAL GRADE CROSSING UPDATE WEB EXCLUSIVE: Michael DePallo, the new CEO at Metrolink, cites challenges and priorities www.progressiverailroading.com/cover www.ProgressiveRailroading.com C1_PR_0113 cover.indd C1 1/3/13 11:35 AM The Secret is Coming Down the Track... POWERRAIL IS CELEBRATING 10 YEARS OF EXCELLENCE! Celebrating 10 Years of Excellence! 10 Years of Delivering Results! We would like to sincerely THANK all of our loyal customers and friends for their support over the past 10 years. Without you, we would not be who we are today - An AAR M-1003 Quality Corporation offering a full line of Locomotive Parts and Components. We are Unique Manufacturer and full-service stocking company with multiple locations throughout North America offering a full range of New or Our Proven True Blue™ Remanufactured-Unit Exchange Components. We will continue to strive to exceed your expectations, while delivering products and services that meet exemplary standards of Quality, Service, Delivery and Value! www. powerrail.com™ | 570.883.7005 FREE INFO: Circle 101 C2_PR_0113_lr PowerRail.indd C2 12/27/12 11:21 AM PROGRESSIVE RAILROADING Volume 56, No. 1 January 2013 | CONTENTS | 1 COVER STORY • PAGE 16 TWO FOR THE LONG HAUL Crude oil and domestic intermodal business pose the greatest long-term growth potential for BNSF as long as enough capacity’s in place FEATURES 14 Deconstructing the North American rail industry Short-term caution and long-term bullishness ruled at RailTrends 2012 23 Connecting the dots TriMet’s Portland-Milwaukie light-rail line will be the latest in a series of corridors linking key employment, tourist destinations Photo courtesy of BNSF Railway Co.