Hong Kong Monthly

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

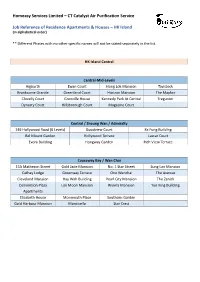

CT Catalyst Air Purification Service Job Reference of Residence

Homeasy Services Limited – CT Catalyst Air Purification Service Job Reference of Residence Apartments & Houses – HK Island (in alphabetical order) ** Different Phases with no other specific names will not be stated separately in the list. HK Island Central Central-Mid-Levels Aigburth Ewan Court Hong Lok Mansion Tavistock Branksome Grande Greenland Court Horizon Mansion The Mayfair Clovelly Court Grenville House Kennedy Park At Central Tregunter Dynasty Court Hillsborough Court Magazine Court Central / Sheung Wan / Admiralty 149 Hollywood Road (6 Levels) Goodview Court Ka Fung Building Bel Mount Garden Hollywood Terrace Lascar Court Evora Building Hongway Garden Rich View Terrace Causeway Bay / Wan Chai 15A Matheson Street Gold Jade Mansion No. 1 Star Street Sung Lan Mansion Cathay Lodge Greenway Terrave One Wanchai The Avenue Cleveland Mansion Hay Wah Building Pearl City Mansion The Zenith Convention Plaza Lok Moon Mansion Riviera Mansion Yue King Building Apartments Elizabeth House Monmouth Place Southorn Garden Gold Harbour Mansion Monticello Star Crest Happy Valley / East-Mid-Levels / Tai Hang 99 Wong Nai Chung Rd High Cliff Serenade Village Garden Beverly Hill Illumination Terrace Tai Hang Terrace Village Terrace Cavendish Heights Jardine's Lookout The Broadville Wah Fung Mansion Garden Mansion Celeste Court Malibu Garden The Legend Winfield Building Dragon Centre Nicholson Tower The Leighton Hill Wing On Lodge Flora Garden Richery Palace The Signature Wun Sha Tower Greenville Gardens Ronsdale Garden Tung Shan Terrace Hang Fung Building -

OFFICIAL RECORD of PROCEEDINGS Wednesday, 15

LEGISLATIVE COUNCIL ─ 15 December 2010 3775 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 15 December 2010 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. THE HONOURABLE LEE CHEUK-YAN DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG 3776 LEGISLATIVE COUNCIL ─ 15 December 2010 DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TIMOTHY FOK TSUN-TING, G.B.S., J.P. THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, S.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. THE HONOURABLE AUDREY EU YUET-MEE, S.C., J.P. -

Hong Kong Monthly

This report analyses the performance of Hong Kong’s office, residential and retail property markets Hong Kong Monthly knightfrank.com/research February 2020 OFFICE Tenants defer expansion plans amid the COVID-19 outbreak Hong Kong Island delaying their real estate decisions. There were two significant cases of The coronavirus (COVID-19) outbreak At this point, we expect leasing demand consolidation and expansion at The has posed a new threat to Hong Kong’s to remain weak, at least in the next Quayside in Kwun Tong during the month. Grade-A office market, which has already month or so. One was Manulife’s lease of a 52,000 sq been subdued in the wake of social unrest ft space at an effective rent of HK$28 per and trade disputes before the outbreak. Kowloon sq ft per month for expansion purposes. Premium Central office space was the Kowloon saw a significant decrease The other was Adidas’ lease of a 72,000 hardest hit, with rents dropping by 20% in the number of office on-site sq ft space at HK$28.5 per sq ft per month YoY in January. Many companies have inspections and in tenant movement. to consolidate its Kwun Tong and Taikoo cautiously put their expansion plans on Many companies have deferred their offices. hold. Bracing for more pressure on rents, expansion or relocation plans to save many landlords are warming to the idea for contingencies. In contrast, renewal Subdued demand combined with of offering rental concessions to secure cases were on the rise, though most substantial supply has weakened the renewals. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Wan Chai St. Regis Hong Kong 230, 264 Eastern Hang Tsui Court, Tsui Ying House 238, 268 Yuen Long Yiu Foo House, Tin Yiu Estate 258, 259 Wan Chai Block A, Viking Villas 260 Central & Western Shun On Building, 2 Sands Street 261 Kowloon City Cheong Shing Court 262 Kwai Tsing Yam Heng House, Shek Yum Estate 263 Wan Chai Sakura Court 264 Central & Western Silvercrest, 24 Macdonnell Road 265 Southern Repulse Bay Garden 266 Central & Western SOHO 189 267 Eastern Block Q, Kornhill 269 Sham Shui Po Block 23, Phase 1, Mei Foo Sun Cheun 270 Island Tower 12, Caribbean Coast 271 Yau Tsim Mong Block 4, Prosperous Garden 272 Yau Tsim Mong Block B, Hoi Lam House, Hoi Fu Court 273 Kwun Tong Dorsett Kwun Tong 274 Wong Tai Sin Block 2, Kai Tak Garden 275 Wan Chai Hang Shun Mansions 276 Wan Chai 307 Jaffe Road 277 Wan Chai Tagus Residences 278 Islands Woodland Court, Parkvale Village 279 Central & Western Chi Residences 120 281 Central & Western 208 Hollywood Road 282 Southern L'Hoel Island South 283 Sha Tin Block 6, Bayshore Towers 284 1 Related confirmed / probable District Building name case number Yau Tsim Mong Tower 7, The Long Beach 285 Sai Kung Pak Kong Au Road 286 Tsuen Wan Indi Home 287 Kwai Tsing On Hoi House, Cheung On Estate 287 Eastern Block 6, Provident Centre -

Building for Tomorrow's Communities

Annual Report 2012 BUILDING FOR TOMORROW’S COMMUNITIES Annual Report 2012 Annual Report Commercial growth and corporate social responsibility are equally important imperatives for Henderson Land. With more than three decades of development excellence behind us, we continue to build on our strengths, creating vibrant projects for the communities of tomorrow in partnership with some of the world’s most renowned architects and designers. Contents 2 Corporate Profile 4 Awards & Accolades 6 Group Structure 7 Highlights of 2012 Final Results 21 10 Chairman’s Statement Wong The Review of Operations Chuk Business in Hong Kong Hang Gloucester 38 Land Bank 41 Property Development Road 48 Property Investment 56 Property Related Businesses Business in Mainland China 60 Land Bank 64 Progress of Major Development Projects 75 Major Investment Properties 82 Subsidiary & Associated Companies 94 Business Model and Strategic Direction 96 Financial Review artist’s impression artist’s impression Double Cove 104 Five Year Financial Summary 108 Sustainability and CSR artist’s impression 122 Corporate Governance Report The H Collection 133 Report of the Directors 150 Biographical Details of Directors and Senior Management 158 Report of the Independent Auditor 159 Accounts 254 Corporate Information The Arch of 257 Notice of Annual General Meeting Triumph 260 Financial Calendar Forward-Looking Statements This annual report contains certain statements that are forward- looking or which use certain forward-looking terminologies. Henderson These forward-looking statements are based on the current beliefs, assumptions and expectations of the Board of Directors of the Company regarding the industry and markets in which 688 it operates. These forward-looking statements are subject to The risks, uncertainties and other factors beyond the Company’s control which may cause actual results or performance to differ materially from those expressed or implied in such forward- artist’s impression artist’s impression artist’s impression Reach looking statements. -

Hansard (English)

LEGISLATIVE COUNCIL ─ 26 January 2011 5291 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 26 January 2011 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. THE HONOURABLE LEE CHEUK-YAN DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. 5292 LEGISLATIVE COUNCIL ─ 26 January 2011 THE HONOURABLE WONG YUNG-KAN, S.B.S., J.P. THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TIMOTHY FOK TSUN-TING, G.B.S., J.P. THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, S.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. -

List of Projects Used in HKIA/ARB Professional Assessment 2007 - 2013

List of projects used in HKIA/ARB Professional Assessment 2007 - 2013 Date of Occupation No Year Name of Company Project Title Address Lot No BD File Ref. Permit / Practical Special Topic Completion (month/year) 1 2007 Aedas Ltd Satellite Earth Station Dai Hei Street at Tai Po Industrial Estate Section G Tai Po Town Lot BD 2/9141/01 (P) Jan 04 IL7076, IL7077, IL971, IL970 Proposed Hotel Development at 31E - 39 Wyndham 31E, 31F, 33-39 Wyndham Street, 2 2007 AGC Design Ltd SARP, IL970RP, BD3/2058/94 PT IV Jul 04 Street, Central Central, Hong Kong IL970SBSS1 RP Extension to the Church of Jesus Christ of Latter Day Tseung Kwan O Lot 45, Area II, Po Lam 3 2007 Aedas Ltd Tseung Kwan O Lot 45 BD 9106/04 31 Oct 2006 Saints at Tseung Kwan O Lane 4 2007 P & T Architects & Engineers Ltd Residential Development At 2 Lok Kwai Path Shatin, 2 Lok Kwai Path, Shatin, N.T. STTL 526 BD 9067/02 Jan 06 / May 06 5 2007 Leung King Partners Ltd Villa Rosa Residents 82 Peak Road, Hong Kong RBL 742 BD 2014/98 Aug 00 6 2007 Dennis Lau & Ng Chun Man Architects & Engineers (HK) Ltd Tuen Mun Area 4C, TMTL 384 King Fung Path, Tuen Mun, N.T. Lot No. 384, Area 4C BD 6/9260/97H (P) Aug 02 Service Apartment Building at Nos. 116-122, Yeung Uk 116-122 Yeung Uk Road, Tsuen Wan, 7 2007 MLA Architects (HK) Ltd TWTL 407 9325/93 28 Aug 06 Road (H-Cube) N.T. -

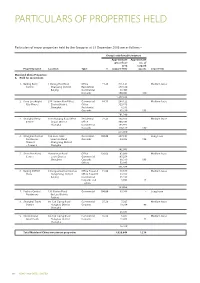

Particulars of Properties Held

PARTICULARS OF PROPERTIES HELD Particulars of major properties held by the Group as at 31 December 2006 are as follows:– Group’s attributable interest Approximate Approximate gross floor no. of area carpark Property name Location Type % (square feet) spaces Lease term Mainland China Properties A. Held for investment 1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium lease Centre Chaoyang District Residential 277,330 Beijing Commercial 98,406 Carparks 190,806 430 1,277,663 2. Kerry Everbright 218 Tianmu Road West Commercial 64.35 286,122 Medium lease City Phase I Zhabei District Office 323,675 Shanghai Residential 6,333 Carparks 85,250 155 701,380 3. Shanghai Kerry 1515 Nanjing Road West Residential 74.25 142,355 Medium lease Centre Jingan District Office 308,584 Shanghai Commercial 103,971 Carparks 118,129 180 673,039 4. Shanghai Central 166 Lane 1038 Residential 100.00 287,101 Long lease Residences Huashan Road Carparks 54,982 154 Phase II Changning District – Tower 3 Shanghai 342,083 5. Shenzhen Kerry Renminnan Road Office 100.00 82,099 Medium lease Centre Lowu District Commercial 107,256 Shenzhen Carparks 88,319 193 Others 53,885 331,559 6. Beijing COFCO 8 Jianguomennei Avenue Office Tower A 15.00 49,649 Medium lease Plaza Dongcheng District Office Tower B 53,895 Beijing Commercial 86,592 Carparks and 3,892 25 others 194,028 7. Fuzhou Central 139 Gutian Road Commercial 100.00 63,986 – Long lease Residences Gu Lou District Fuzhou 8. Shanghai Trade 88-128 Siping Road Commercial 55.20 7,567 Medium lease Square Hongkou District Carparks 19,264 48 Shanghai 26,831 9. -

Major Transaction

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Kerry Properties Limited, you should at once hand this circular to the purchaser(s) or the transferee(s) or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or the transferee(s). The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this circular, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. website: www.kerryprops.com (Stock Code: 00683) MAJOR TRANSACTION A letter from the board of directors of Kerry Properties Limited is set out on pages 5 to 25 of this circular. * For identification purpose only 29 December 2004 CONTENTS Page Definitions ........................................................ 1 Letter from the Board ............................................... 5 Appendix I – Accountants’ Report on Treasure Lake................ 26 Appendix II – Accountants’ Report on Eas HK .................... 33 Appendix III − Accountants’ Report on the Eas PRC Group ........... 51 Appendix IV – Financial Information -

Name of Buildings Awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (As at 8 February 2018)

Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (as at 8 February 2018) Name of Building Type of Building District @Convoy Commercial/Industrial/Public Utilities Eastern 1 & 3 Ede Road Private/HOS Residential Kowloon City 1 Duddell Street Commercial/Industrial/Public Utilities Central & Western 100 QRC Commercial/Industrial/Public Utilities Central & Western 102 Austin Road Commercial/Industrial/Public Utilities Yau Tsim Mong 1063 King's Road Private/HOS Residential Eastern 11 MacDonnell Road Private/HOS Residential Central & Western 111 Lee Nam Road Commercial/Industrial/Public Utilities Southern 12 Shouson Hill Road Private/HOS Residential Central & Western 127 Repulse Bay Road Private/HOS Residential Southern 12W Commercial/Industrial/Public Utilities Tai Po 15 Homantin Hill Private/HOS Residential Yau Tsim Mong 15W Commercial/Industrial/Public Utilities Tai Po 168 Queen's Road Central Commercial/Industrial/Public Utilities Central & Western 16W Commercial/Industrial/Public Utilities Tai Po 17-19 Ashley Road Commercial/Industrial/Public Utilities Yau Tsim Mong 18 Farm Road (Shopping Arcade) Commercial/Industrial/Public Utilities Kowloon City 18 Upper East Private/HOS Residential Eastern 1881 Heritage Commercial/Industrial/Public Utilities Yau Tsim Mong 211 Johnston Road Commercial/Industrial/Public Utilities Wan Chai 225 Nathan Road Commercial/Industrial/Public Utilities Yau Tsim Mong Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) -

Review of Operations

REVIEW OF OPERATIONS Sales of the joint venture developments at Tai Kok Apart from the exceptional location and quality of Tsui Phases 1 and 2, are also progressing well with its properties, the Group also strives to provide its the developments being approximately 86% and 46% residents with the best professional building sold, respectively, as at 31 December 2000. At the management services through Kerry Property year end, Island Harbourview, Park Avenue and Management Services Limited. These include a wide Central Park had 303, 513 and 1,068 units, array of home services such as insurance, daily respectively, remaining available for sale in the newspaper, housekeeping services and experienced coming year. licensed technicians to look after repairs and maintenance needs of the apartments. Security in the INVESTMENT PROPERTIES Group’s developments is also enhanced by the use Gross rental revenue from investment properties in of advanced CCTV system and a computerised 2000 amounted to HK$465 million (1999: HK$476 security checking schedule whenever possible. million). In accordance with its accounting policies, the Group conducted a revaluation of its investment properties at the year end. The addition of Aigburth, a luxury development located adjacent to Tavistock II, to the Group’s investment portfolio has helped to reinforce its recurrent income base. Aigburth comprises sixty standard apartments measuring between 2,980 square feet and 3,080 square feet. It has four single floor apartments and a top floor duplex penthouse. It is leasing well with the building being approximately 89% leased as at 31 December 2000. Construction of Olympian Tower and Olympian City 1, being the office block and the commercial podium in the Phase 1 development of the Tai Kok Tsui project, was also completed during the year. -

Hong Kong Property Transaction Analysis Report

August-2005 Vol. 91 Hong Kong Property Transaction Analysis Report Report Date: 2005/9/28 Page Top 10 Mortgage Bank July 2 Domestic and Non-domestic Transaction Analysis 3 1'st and 2'nd Hand Residential Transaction Analysis 4 - Private Sector 4 - Home Ownership Scheme 4 Top 10 Private Estate Transaction Analysis 5 Top 10 H.O.S. Estate Transaction Analysis 6 Top 10 Transaction 7 - Office Transaction 7 - Shop Transaction 7 - Residential Transaction 8 - Industrial Transaction 8-9 This report was conducted by Land Search Online Limited. www.landsearch.com.hk Unit 1513-16, 15/F, Grand City Plaza No. 1 Sai Lau Kok Road, Tsuen Wan Hong Kong Tel: 24298333 Fax: 24233008 [email protected] * All information provided by this report is for reference only and shall not be deemed to be any advice given to the subscribers. Land Search Online Limited shall not be responsible for any legal consequence arising therefrom. * Source of transaction is based on the registration data from the daily diskette by the Land Registry of HKSAR and Land Search Online database. P.1/9 Hong Kong Property Transaction Analysis Report ▼ Top 10 Mortgage Bank Market Sharing Bank July Market Sharing % - Counting include new mortgage loan and BANK OF CHINA (HK) LIMITED 19.7% refinancing mortgage loan. THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITE 10.0% HANG SENG BANK LIMITED 9.6% STANDARD CHARTERED BANK 8.4% THE BANK OF EAST ASIA LIMITED 6.6% BANK OF COMMUNICATIONS 5.2% WING LUNG BANK LIMITED 3.7% DAH SING BANK LIMITED 2.5% GE CAPITAL (HONG KONG) LIMITED 2.2% Others