Kerry Properties Limited Annual Report 2006 Annual

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Interim Report 2019 Corporate Information & Key Dates

20201919 QUICK FACTS 53 countries & territories 46,000+ employees worldwide 70M ft² land & facilities 10,000+ self-owned operating vehicles CONTENTS 02 Corporate Information & Key Dates 03 Financial Highlights 05 Management Discussion and Analysis Results Overview 05 Business Review 06 Financial Review 12 Staff and Remuneration Policies 12 GLOBAL NETWORK 13 Corporate Governance and Other Information 25 Independent Auditor’s Review Report 27 Interim Financial Statements 54 Definitions CHINA FOCUS ASIA SPECIALIST 1 INTERIM REPORT 2019 CORPORATE INFORMATION & KEY DATES KERRY LOGISTICS NETWORK LIMITED COMPANY SECRETARY (Incorporated in the British Virgin Islands and continued Ms LEE Pui Nee into Bermuda as an exempted company with limited liability) AUDITOR PricewaterhouseCoopers BOARD OF DIRECTORS Executive Directors LEGAL ADVISER Mr KUOK Khoon Hua (Chairman) Davis Polk & Wardwell Mr MA Wing Kai William (Group Managing Director) Mr NG Kin Hang REGISTERED OFFICE Victoria Place, 5th Floor, 31 Victoria Street Non-executive Director Hamilton HM 10, Bermuda Ms TONG Shao Ming CORPORATE HEADQUARTERS AND Independent Non-executive Directors PRINCIPAL PLACE OF BUSINESS IN HONG KONG Ms KHOO Shulamite N K 16/F, Kerry Cargo Centre, 55 Wing Kei Road Ms WONG Yu Pok Marina Kwai Chung, New Territories, Hong Kong Mr YEO Philip Liat Kok Mr ZHANG Yi Kevin PRINCIPAL SHARE REGISTRAR AND TRANSFER AGENT AUDIT AND COMPLIANCE COMMITTEE Estera Management (Bermuda) Limited Ms WONG Yu Pok Marina (Chairman) Victoria Place, 5th Floor, 31 Victoria Street Ms TONG Shao Ming -

Final Report

Transport and Housing Bureau The Government of the Hong Kong SAR FINAL REPORT Consultancy Services for Providing Expert Advice on Rationalising the Utilization of Road Harbour Crossings In Association with September 2010 CONSULTANCY SERVICES FOR PROVIDING EXPERT ADVICE ON RATIONALISING THE UTILISATION OF ROAD HARBOUR CROSSINGS FINAL REPORT September 2010 WILBUR SMITH ASSOCIATES LIMITED CONSULTANCY SERVICES FOR PROVIDING EXPERT ADVICE ON RATIONALISING THE UTILISATION OF ROAD HARBOUR CROSSINGS FINAL REPORT TABLE OF CONTENTS Chapter Title Page 1 BACKGROUND AND INTRODUCTION .......................................................................... 1-1 1.1 Background .................................................................................................................... 1-1 1.2 Introduction .................................................................................................................... 1-1 1.3 Report Structure ............................................................................................................. 1-3 2 STUDY METHODOLOGY .................................................................................................. 2-1 2.1 Overview of methodology ............................................................................................. 2-1 2.2 7-stage Study Methodology ........................................................................................... 2-2 3 IDENTIFICATION OF EXISTING PROBLEMS ............................................................. 3-1 3.1 Existing Problems -

Hong Kong Monthly

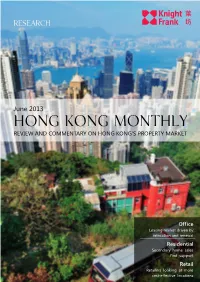

Research June 2013 Hong Kong Monthly REVIEW AND COMMENTARY ON HONG KONG'S PROPERTY MARKET Office Leasing market driven by relocation and renewal Residential Secondary home sales find support Retail Retailers looking at more cost-effective locations1 June 2013 Hong Kong Monthly Market in brief The following table and figures present a selection of key trends in Hong Kong‟s economy and property markets. Table 1 Economic indicators and forecasts Latest 2013 Economic indicator Period 2011 2012 reading forecast GDP growth Q1 2013 +2.8% +4.9% +1.4% +3.0% Inflation rate Apr 2013 +4.0% +5.3% +4.1% +4.4% Feb 2013- Unemployment 3.5%# 3.4% 3.1% 3.2% Apr 2013 Prime lending rate Current 5.00–5.25% 5.0%* 5.0%* 5.0%* Source: EIU CountryData / Census & Statistics Department / Knight Frank # Provisional * HSBC prime lending rate Figure 1 Figure 2 Figure 3 Grade-A office prices and rents Luxury residential prices and rents Retail property prices and rents Jan 2007 = 100 Jan 2007 = 100 Jan 2007 = 100 250 190 350 230 170 300 210 190 150 250 170 130 150 200 130 110 150 110 90 90 100 70 70 50 50 50 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 Price index Rental index Price index Rental index Price index Rental index Source: Knight Frank Source: Knight Frank Source: Rating and Valuation Department / Knight Frank Note: Provisional figures from Oct 2012 to Mar 2013 2 2 KnightFrank.com.hk Monthly review Property sales were quiet in May, due to the implementation of the Double Stamp Duty on all property sectors in February and the Residential Properties (First-hand Sales) Ordinance on the residential sector in April. -

Property Management Revenue from Property Management for 2003 Increased by 11.0% Over 2002 to HK$94 Million

032 Executive management’s report Property review This caused revenue from investment properties for the year of our properties further and establishing them as a to decline slightly by 1% over 2002 to HK$888 million. benchmark for the industry in Hong Kong. Our staff performed outstandingly during the period of SARS For Two IFC, the quality of the office building and its to ensure shoppers’safety and mitigate the effects of the management enabled MTR to attract tenants despite the outbreak on public confidence. We also supported tenants lingering cautious sentiment resulting from SARS, the war in through aggressive promotion campaigns, including an Iraq and the weak economy. Considerable effort was taken attractive rebate promotion. Within this context, we took full to explain to potential tenants, agents and the business advantage of the relaxation of travel restrictions on tourists community the merits of the building, which is ideally suited from Mainland China through proactive, tailor-made to the sophisticated needs of multi-national corporations. programmes, such as organising shopping tours, designed The decision by Swiss banking giant UBS to lease seven floors to bring high spending Mainland visitors to our shopping represented one of the largest and highest profile relocations centres. These programmes proved successful in boosting of an office tenant in Hong Kong in 2003. UBS joined a growing the business turnover of our tenants. list of leading institutions in the building, including the Hong The Total Quality Service Regime, our pioneering customer Kong Monetary Authority, reinforcing Two IFC’s position as the service enhancement programme, and our computerised building of choice for top-tier corporations. -

CT Catalyst Air Purification Service Job Reference of Residence

Homeasy Services Limited – CT Catalyst Air Purification Service Job Reference of Residence Apartments & Houses – HK Island (in alphabetical order) ** Different Phases with no other specific names will not be stated separately in the list. HK Island Central Central-Mid-Levels Aigburth Ewan Court Hong Lok Mansion Tavistock Branksome Grande Greenland Court Horizon Mansion The Mayfair Clovelly Court Grenville House Kennedy Park At Central Tregunter Dynasty Court Hillsborough Court Magazine Court Central / Sheung Wan / Admiralty 149 Hollywood Road (6 Levels) Goodview Court Ka Fung Building Bel Mount Garden Hollywood Terrace Lascar Court Evora Building Hongway Garden Rich View Terrace Causeway Bay / Wan Chai 15A Matheson Street Gold Jade Mansion No. 1 Star Street Sung Lan Mansion Cathay Lodge Greenway Terrave One Wanchai The Avenue Cleveland Mansion Hay Wah Building Pearl City Mansion The Zenith Convention Plaza Lok Moon Mansion Riviera Mansion Yue King Building Apartments Elizabeth House Monmouth Place Southorn Garden Gold Harbour Mansion Monticello Star Crest Happy Valley / East-Mid-Levels / Tai Hang 99 Wong Nai Chung Rd High Cliff Serenade Village Garden Beverly Hill Illumination Terrace Tai Hang Terrace Village Terrace Cavendish Heights Jardine's Lookout The Broadville Wah Fung Mansion Garden Mansion Celeste Court Malibu Garden The Legend Winfield Building Dragon Centre Nicholson Tower The Leighton Hill Wing On Lodge Flora Garden Richery Palace The Signature Wun Sha Tower Greenville Gardens Ronsdale Garden Tung Shan Terrace Hang Fung Building -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

Directors and Senior Management

Directors and Senior Management Executive Directors Mr KUOK Khoon Chen, aged 55, Mr HO Shut Kan, aged 61, has been has been an Executive Director of the an Executive Director of the Company Company, the Chairman of the Board since 1998. Mr Ho is an executive and the chairman of the Remuneration director of Kerry Properties (H.K.) Committee of the Company since Limited, the principal Hong Kong 2008. He has been a senior executive property company of the Group, and of the Kuok Group since 1978. He is is responsible for the Group’s property currently the deputy chairman and developments and infrastructure managing director of Kerry Group investments. Mr Ho is also responsible Limited, the chairman and managing for overseeing the operation of the director of Kerry Holdings Limited project companies and the projects of and a director of a number of Kuok the Group in Shenzhen, Chengdu and Group companies. Both Kerry Group Nanchang. Mr Ho is a non-executive Limited and Kerry Holdings Limited director of Eagle Asset Management are the controlling shareholders of the (CP) Limited, the manager of Company. Mr Kuok is an executive Champion Real Estate Investment director of China World Trade Center Trust, which is listed in Hong Kong. Co., Ltd. which is listed on the Shanghai Stock Exchange. Mr Kuok holds a Bachelor’s degree in Economics Mr MA Wing Kai, William, aged from Monash University in Australia. 48, has been an Executive Director Mr Kuok is the brother-in-law of Mr of the Company since 2004. Mr Bryan Pallop Gaw whose biography is Ma is the deputy chairman and the set out in the section headed “Senior managing director of Kerry Logistics Management” of this annual report. -

Financial Review

REVIEW OF OPERATIONS Financial Review TURNOVER PROFIT ATTRIBUTABLE TO SHAREHOLDERS Turnover for the Group for the year ended 31 HK$ MILLION December 2001 increased by 58% to HK$5,036 1,575 million (2000: HK$3,196 million). Turnover from both 1,600 rental and sales registered increases during the year. 1,400 Gross property sales income increased from 1,203 1,233 HK$1,664 million in 2000 to HK$3,159 million in 1,200 2001. Property rental income also increased to 1,000 HK$885 million (2000: HK$820 million) whilst 728 income from warehouse and logistics amounted to 800 HK$744 million (2000: HK$481 million). The 600 396 Group’s hotel operations contributed HK$204 million 400 to turnover during the year (2000: HK$176 million). 200 BREAKDOWN OF KPL’S TOTAL TURNOVER 0 HK$ MILLION 1997 1998 1999 2000 2001 5,500 5,036 decrease in the Group’s earnings in 2001 is due to losses incurred from the sales of Ocean Pointe, Kerry 5,000 Everbright City, Yuen Long 2 warehouse and a 4,500 specific provision of HK$360 million in respect of its 3,159 Constellation Cove project in Tai Po Kau. The Group’s 4,000 75% share of the provision amounted to HK$270 3,500 3,054 3,196 million. The Group also recorded a profit of 2,907 approximately HK$112 million from the disposal of 3,000 its 19.6% interest in the Hu-Ning Expressway in 1,664 2,500 2,342 December 2001. 1,921 1,747 2,000 44 FUNDING AND FINANCING 1,238 426 1,500 55 In order to achieve better control of treasury 410 318 74 47 operations and lower the average cost of funds, KPL 1,000 63 71 204 176 402 410 356 has centralised funding for all its operations at the 11 35 500 Group level. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Wan Chai St. Regis Hong Kong 230, 264 Eastern Hang Tsui Court, Tsui Ying House 238, 268 Yuen Long Yiu Foo House, Tin Yiu Estate 258, 259 Wan Chai Block A, Viking Villas 260 Central & Western Shun On Building, 2 Sands Street 261 Kowloon City Cheong Shing Court 262 Kwai Tsing Yam Heng House, Shek Yum Estate 263 Wan Chai Sakura Court 264 Central & Western Silvercrest, 24 Macdonnell Road 265 Southern Repulse Bay Garden 266 Central & Western SOHO 189 267 Eastern Block Q, Kornhill 269 Sham Shui Po Block 23, Phase 1, Mei Foo Sun Cheun 270 Island Tower 12, Caribbean Coast 271 Yau Tsim Mong Block 4, Prosperous Garden 272 Yau Tsim Mong Block B, Hoi Lam House, Hoi Fu Court 273 Kwun Tong Dorsett Kwun Tong 274 Wong Tai Sin Block 2, Kai Tak Garden 275 Wan Chai Hang Shun Mansions 276 Wan Chai 307 Jaffe Road 277 Wan Chai Tagus Residences 278 Islands Woodland Court, Parkvale Village 279 Central & Western Chi Residences 120 281 Central & Western 208 Hollywood Road 282 Southern L'Hoel Island South 283 Sha Tin Block 6, Bayshore Towers 284 1 Related confirmed / probable District Building name case number Yau Tsim Mong Tower 7, The Long Beach 285 Sai Kung Pak Kong Au Road 286 Tsuen Wan Indi Home 287 Kwai Tsing On Hoi House, Cheung On Estate 287 Eastern Block 6, Provident Centre -

Annual Report 2018 Corporate Information & Key Dates

QUICK FACTS 53 countries & territories 40,000+ employees worldwide 60M ft² land & facilities 10,000+ self-owned operating vehicles CONTENTS 02 Corporate Information & Key Dates 03 Financial Highlights 05 2014-2018 Financial Summary 06 Logistics Facilities GLOBAL NETWORK 13 Chairman’s Statement 14 Management Discussion and Analysis 14 Results Overview 15 Business Review 20 Financial Review 20 Staff and Remuneration Policies 21 Environmental, Social and Governance Report 33 Awards and Citations CHINA FOCUS 39 Corporate Governance Report 57 Directors and Senior Management 73 Report of Directors 99 Independent Auditor’s Report 108 Statement of Accounts 198 Definitions ASIA SPECIALIST 1 ANNUAL REPORT 2018 CORPORATE INFORMATION & KEY DATES BOARD OF DIRECTORS COMPANY SECRETARY Executive Directors Ms LEE Pui Nee Mr YEO George Yong-boon (Chairman) Mr MA Wing Kai William (Group Managing Director) AUDITOR Mr KUOK Khoon Hua PricewaterhouseCoopers Mr NG Kin Hang LEGAL ADVISER Non-executive Director Davis Polk & Wardwell Mr CHIN Siu Wa Alfred REGISTERED OFFICE Independent Non-executive Directors Canon’s Court, 22 Victoria Street Ms KHOO Shulamite N K Hamilton HM12, Bermuda Mr WAN Kam To Ms WONG Yu Pok Marina CORPORATE HEADQUARTERS AND Mr YEO Philip Liat Kok PRINCIPAL PLACE OF BUSINESS IN HONG KONG Mr ZHANG Yi Kevin 16/F, Kerry Cargo Centre, 55 Wing Kei Road AUDIT AND COMPLIANCE COMMITTEE Kwai Chung, New Territories, Hong Kong Ms WONG Yu Pok Marina (Chairman) PRINCIPAL SHARE REGISTRAR AND Mr CHIN Siu Wa Alfred Mr WAN Kam To TRANSFER AGENT Mr ZHANG Yi -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Sha Tin Block 1, La Costa 5915 Block 2, Lotus Tower, Kwun Tong Garden Kwun Tong 5916 Estate Tai Po Po Sam Pai Village 5917 Kowloon City Duchy Heights 5918 Kowloon City Duchy Heights 5919 Eastern Tower 8, Pacific Palisades 5920 Sham Shui Po Ping Yuen, Yau Yat Chuen 5921 Kowloon City Block C, On Lok Factory Building 5922 Kwai Tsing On Hoi House, Cheung On Estate 5923 Yau Tsim Mong Skyway Mansion 5924 Kowloon City Block C, On Lok Factory Building 5925 Sha Tin Kau To Village 5927 Kowloon City 61 Maidstone Road 5928 Kowloon City The Palace 5929 Kwai Tsing Tower 3A, Phase 1, Tierra Verde 5930 Eastern Tsui Shou House, Tsui Wan Estate 5931 Tuen Mun Lok Sang House, Kin Sang Estate 5932 Sham Shui Po Man Lok House, Tai Hang Sai Estate 5933 Yau Tsim Mong Lee Kwan Building 5934 Wan Chai Wing Way Court 5935 Eastern Hang Ying Building 5936 Sai Kung Block 2, Radiant Towers 5937 Central & Western 23 Wilmer Street 5938 Yau Tsim Mong Block 4, Metro Harbour View 5939 Kwun Tong Chi Tai House, On Tai Estate 5940 Kowloon City Tower 2, K City 5941 Tuen Mun Block 6, Po Tin Estate 5943 Yau Tsim Mong Wai Fat Building 5944 Tsuen Wan Tak Tai Building 5945 Sham Shui Po Tower 2, Nob Hill 5946 1 Related Confirmed / District Building Name Probable Case(s) Tsuen Wan Tower 6, Bellagio 5947 -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Islands Hong Kong SkyCity Marriott Hotel 11101 North Block 6, Belair Monte 11105 Kowloon City iclub Ma Tau Wai Hotel 11106 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11107 Wan Chai Best Western Hotel Causeway Bay 11108 Kowloon City Metropark Hotel Kowloon 11109 Kwun Tong IW Hotel 11110 Kwai Tsing Dorsett Tsuen Wan Hong Kong 11111 Eastern Ramada Hong Kong Grand View 11112 Kowloon City iclub Ma Tau Wai Hotel 11113 North Block 1, Dawning Views 11114 Islands Block 1, Coastal Skyline 11115 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11116 Central & Western Sing Fai Building 11118 Eastern Hoi Sing Mansion, Taikoo Shing 11120 Eastern Hoi Sing Mansion, Taikoo Shing 11121 Sai Kung Tak On House, Hau Tak Estate 11123 Sham Shui Po 15 Fuk Wing Street 11124 Kowloon City iclub Ma Tau Wai Hotel 11125 Yau Tsim Mong Dorsett Mongkok, Hong Kong 11127 Kwai Tsing Block 1, Regency Park 11128 Central & Western True Light Building 11129 Islands Hong Kong SkyCity Marriott Hotel 11130 Central & Western Yukon Court 11131 Central & Western Bishop Lei International House 11132 Central & Western 40 Conduit Road 11132 Sham Shui Po 15 Fuk Wing Street 11133 Central & Western May Tower I 11134 Kwai Tsing Yat King House, Lai King Estate 11135 Central & Western Yip Cheong Building,