Committed to Sustainable Value Creation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Premium Thresholds for Equity Options Traded at Euronext Amsterdam Premium Based Tick Size

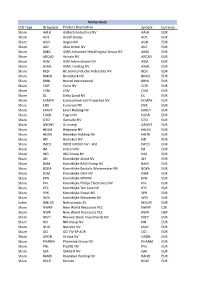

Premium Based Tick Size Premium thresholds for equity options traded at Euronext Amsterdam Trading Trading Premium Company symbol symbol threshold Underlying American European €0.50 €5.00 1 Aalberts AAI x 2 ABN AMRO Bank ABN x 3 Accell Group ACC x 4 Adidas ADQ x 5 Adyen (contract size 10) ADY x 6 Aegon AGN x 7 Ageas AGA x 8 Ahold Delhaize, koninklijke AH AH9 x 9 Air France-KLM AFA x 10 Akzo Nobel AKZ x 11 Allianz AZQ x 12 Altice Europe ATC x 13 AMG AMG x 14 Aperam AP x 15 Arcadis ARC x 16 ArcelorMittal MT MT9 x 17 ASM International ASM x 18 ASML Holding ASL AS9 x 19 ASR Nederland ASR x 20 BAM Groep, koninklijke BAM x 21 Basf BFQ x 22 Bayer REG BYQ x 23 Bayerische Motoren Werke BWQ x 24 BE Semiconductor Industries BES x 25 BinckBank BCK x 26 Boskalis Westminster, koninklijke BOS x 27 Brunel International BI x 28 Coca-Cola European Partners CCE x 29 CSM CSM x 30 Daimler REGISTERED SHARES DMQ x 31 Deutsche Bank DBQ x 32 Deutsche Lufthansa AG LUQ x 33 Deutsche Post REG DPQ x 34 Deutsche Telekom REG TKQ x 35 DSM, koninklijke DSM x 36 E.ON EOQ x 37 Euronext ENX x 38 Flow Traders FLW x 39 Fresenius SE & CO KGAA FSQ x 40 Fugro FUR x 41 Grandvision GVN x 42 Heijmans HEY x 43 Heineken HEI x 44 IMCD IMD x 45 Infineon Technologies NTQ x 46 ING Groep ING IN9 x 47 Intertrust ITR x 48 K+S KSQ x 49 Kiadis Pharma KDS x 50 Klépierre CIO x 51 KPN, koninklijke KPN x 52 Marel MAR x 53 Muenchener Rueckver REG MRQ x 54 NIBC Holding NIB x 55 NN Group NN x 56 NSI NSI x 57 OCI OCI x 58 Ordina ORD x 59 Pharming Group PHA x 60 Philips Electronics, koninklijke PHI -

Annual Report 2016 22 March 2017 Table of Contents

Annual report 2016 22 March 2017 Table of contents Overview 5 Highlights 5 Message from the chairman 6 About Delta Lloyd 8 Our brands 8 Our strategy 9 Our environment 12 How we create value 14 Value creation model 14 Delta Lloyd’s contribution to the UN SDGs 16 Stakeholders and materiality 17 Materiality assessment 20 Delta Lloyd in 2016 23 Capital management 27 Financial and operational performance 29 Life Insurance 31 General Insurance 34 Asset Management 37 Bank 39 Corporate and other activities 41 Investor relations and share developments 41 Human capital 46 Risk management and compliance 50 Risk management 50 Risk management philosophy 50 Risk governance 51 Risk management responsibilities 52 Risk processes and systems 53 Risk culture 54 Risk taxonomy 55 Top five risks 58 Compliance 61 Fraud 62 Corporate governance 64 Executive Board and Supervisory Board 64 Executive Board 64 Supervisory Board 64 Supervisory Board committees 65 Report of the Supervisory Board 66 Role of the Supervisory Board 67 Strategy 67 Key issues in 2016 68 Other issues 69 Supervisory Board composition 70 Supervisory Board meetings 70 Supervisory Board committees 71 Financial statements and profit appropriation 75 A word of thanks 76 Remuneration report 2016 77 Remuneration policy 77 Governance of the remuneration policy 77 Remuneration received by Executive Board members 81 Remuneration of the Supervisory Board 93 Corporate governance 96 Corporate governance statement 104 EU directive on takeover bids 104 In control statement 106 Management statement under Financial -

Trade Credit Insurance

Trade Credit Insurance Peter M. Jones PRIMER SERIES ON INSURANCE ISSUE 15, FEBRUARY 2010 NON-BANK FINANCIAL INSTITUTIONS GROUP GLOBAL CAPITAL MARKETS DEVELOPMENT DEPARTMENT FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY www.worldbank.org/nbfi Trade Credit Insurance Peter M. Jones primer series on insurance issue 15, february 2010 non-bank financial institutions group global capital markets development department financial and private sector development vice presidency www.worldbank.org/nbfi ii Risk Based Supervision THIS ISSUE Author Peter M. Jones was the Chief Executive Officer of the African Trade Insurance Agency (ATI) from 1 February, 2006 up until 31 July, 2009 when he retired. During his time as CEO of ATI, Peter successfully implemented a legal and capital restructuring, including the expansion of the Agency’s product offering to ensure that it meets the full needs of the private and public sector in Africa. Prior to joining ATI, Peter held various positions at the Multilateral Investment Guarantee Agency (MIGA). He was also a Vice-President at Export Development Canada (EDC), where he was responsible for all of EDC’s business operations in the Transportation sector, as well as for the establishment, development and management of its equity investment program. This experience, together with his senior positions at the Canadian Imperial Bank of Commerce (CIBC) and ANZ/Grindlays Bank, has provided him with wide ranging skills and experience in identification of viable equity opportunities, including successful exits. Peter is a Fellow of the Institute of Chartered Secretaries and Administrators. Series editor Rodolfo Wehrhahn is a senior insurance specialist at the World Bank. -

Report International Conference on Inclusive Insurance 2020 Digital Edition

Report International Conference on Inclusive Insurance 2020 Digital Edition Edited by Zahid Qureshi and Dirk Reinhard Report International Conference on Inclusive Insurance 2020 — Digital Edition Conference documents and This report is the summary of the Inter- presentations are available online: national Conference on Inclusive Insur- ance — Digital Edition, which took place from 2 to 6 November 2020. Individual summaries, in various styles, were contributed by a team of international www.inclusiveinsurance.org rapporteurs. Readers, authors and organisers might not share all opinions expressed or agree with the recommen- dations given. These, however, reflect the rich diversity of the discussions. Over 70 speakers participated in the conference. Report International Conference on Inclusive Insurance 2020 — Digital Edition 1 Contents 1 Contents 31 Agenda 61 Agenda 2 Foreword Day 3—4 November 2020 Day 5—6 November 2020 3 Acknowledgements How to reach scale and develop Lessons learnt and next steps 4 Participant overview inclusive insurance markets 62 Session 16 5 Agenda 32 Session 8 Technology driving Day 1—2 November 2020 Integrated risk inclusive insurance Inclusive insurance management solutions amidst a pandemic 65 Session 17 36 Session 9 The ups and downs of 6 Session 1 How digitisation can inclusive insurance: Opening of the conference — spur market growth Learning from experience The landscape of inclusive insurance 2020 39 Session 10 68 Session 18 Lessons learnt from Outlook: What will be the next 9 Keynote national strategies milestones -

Successful NLII Business Loan Fund Continues to Grow

Successful NLII business loan fund continues to grow Another € 480 million available for Dutch SMEs through institutional investors Amsterdam/Rotterdam, 8 March 2017 – Dutch investment institution Nederlandse Investeringsinstelling N.V. (NLII) and Robeco today announce that the SME corporate lending fund Bedrijfsleningenfonds (BLF), created by NLII with Robeco acting as fund manager, has raised € 480 million in the second funding round, bringing the fund total to € 960 million. This will make extra funding from institutional investors available to larger Dutch SMEs. An amount of € 195 million has already been lent to Dutch SMEs since the fund was established. The parties participating in this second round of funding are NN Group, Pensioenfonds Metaal & Techniek (PMT), Pensioenfonds van de Metalektro (PME), a.s.r. and the European Investment Fund (EIF). Most of these parties also participated in the first funding round. NLII CEO Loek Sibbing: “The success of the BLF is clearly highlighted by this second round of funding. Our objective is to enable institutional investors such as pension funds and insurers to invest directly in the Dutch economy and that is exactly what the BLF offers investors. The fund has already enabled a number of Dutch companies to continue to grow. Expanding the fund increases the lending opportunities for SMEs significantly.” Robeco BLF fund manager Erik Hylarides: “The BLF was established to bring about a change in the funding landscape by offering companies access to multiple sources of finance. The current expansion of the fund and the pipeline of transactions we are working on prove that this has been a success. -

Vzor Závěrečné Práce

Masarykova univerzita Ekonomicko-správní fakulta Studijní obor: Regionální rozvoj a správa INOVAČNÍ PROSTŘEDÍ A POLITIKA V NIZOZEMSKÝCH REGIONECH Innovation environment and innovation policy in the Dutch regions Diplomová práce Vedoucí diplomové práce: Autor: Ing. Viktorie Klímová, Ph.D. Bc. Soňa RASZKOVÁ Brno, 2018 Jméno a příjmení autora: Soňa Raszková Název diplomové práce: Inovační prostředí a politika v nizozemských regionech Název práce v angličtině: Innovation environment and innovation policy in the Dutch regions Katedra: Regionálního rozvoje a správy Vedoucí diplomové práce: Ing. Viktorie Klímová, Ph.D. Rok obhajoby: 2018 Anotace Cílem diplomové práce „Inovační prostředí a politika v nizozemských regionech” je analyzovat a determinovat prvky, které ovlivňují úspěšnost a efektivitu regionálních inovačních systémů na příkladu vybraných regionálních inovačních systémů v Nizozemsku. První část práce je zaměřena na popis inovačních systémů, jejich koncept, strukturu, prvky, funkce a typologii, regionální inovační politiku a její nástroje. Druhá část práce analyzuje nizozemský národní inovační systém, jeho aktéry a nástroje. Posléze se práce zaměřuje na popis jednotlivých regionů a u třech vybraných regionů (Severní Holandsko, Jižní Holandsko a Severní Brabantsko) analyzuje a charakterizuje jejich regionální inovační systém. Toto srovnání je zaměřeno na socioekonomické charakteristiky, infrastrukturu a aktivitu výzkumu a vývoje, inovační politiku a její nástroje. Tyto determinanty úspěšnosti jsou podrobeny hlubší analýze. Annotation The aim of the diploma thesis "Innovation environment and innovation policy in the Dutch regions" is to analyse and determine the elements that influence the success and effectiveness of regional innovation systems on the example of selected regional innovation systems in the Netherlands. The first part of the thesis focuses on definition of innovation systems, their concept, structure, elements, functions and typology, regional innovation policy and its tools. -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

Annual Report and Accounts 2012

Towards a stronger Aviva Aviva plc Annual report and accounts 2012 | Retirement | Investments | Insurance | Health | Aviva is a life, general and health insurance business and provides asset management services. We are the largest insurer in the UK* and we have strong businesses in selected international markets. Our products help 34 million customers** enjoy the peace of mind that comes from managing the risks of everyday life. With us, they can save for a more comfortable retirement and protect – with insurance – the people and things that are important to them. We’re here to help people, businesses and communities get back on their feet when the unexpected happens. It is therefore our responsibility to make sure that our 317-year-old business will be there for our customers long into the future. 2012 was a year of change for Aviva. In this annual report you can read more about how we’re taking steps to create a stronger Aviva. View our reports online 2012 Annual report 2012 Corporate and accounts responsibility report We provide our annual Find out more about our report online which allows commitment to acting us to reduce the paper we as a responsible member print and distribute. of the international business community. Visit Aviva plc View our CR report here www.aviva.com/ www.aviva.com/ * Based on aggregate 2011 UK life and pensions sales (PVNBP) reports/2012ar reports/2012cr and general insurance gross written premiums ** On an ongoing basis 1 Aviva plc Annual report and accounts 2012 What’s inside Inside the essential read Our plan to change Aviva Chairman’s statement 04 Group chief executive In July 2012, we announced a plan designed officer’s statement 06 to strengthen our capital position and transform Chief financial officer’s Aviva: Focus, Strengthen, Perform. -

CFD Type IB Symbol Product Description Symbol Currency Share

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV -

Eindhoven University of Technology MASTER De Ontwikkeling Van Een

Eindhoven University of Technology MASTER De ontwikkeling van een sourcing strategie voor direct schade herstel Welle, S.H. Award date: 2007 Link to publication Disclaimer This document contains a student thesis (bachelor's or master's), as authored by a student at Eindhoven University of Technology. Student theses are made available in the TU/e repository upon obtaining the required degree. The grade received is not published on the document as presented in the repository. The required complexity or quality of research of student theses may vary by program, and the required minimum study period may vary in duration. General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. • Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain ARW versiteil eindhoven f/ j / ::; l 2007 delta lloyd groep BDK 'De Ontwikkeling van een Sourcing Strategie voor Direct Schade Herstel'. , ................ ,,, .. ,~,:' ... .•·; ' ·.· .• t I ', ,_; ~; ~ .. " • ....... _.. ,~.· : . / .... ' .. ' . ... , ,._ .... '":' ~·:•' ' .. !,},{' ·1 ,,r;4 ·-.. www.skyscrapercity.com Steven H. Welle Januari 2007 delta lloyd groep TBM 'De Ontwikkeling van een Sourcing Strategie voor Direct Schade Herstel'. Datum Dinsdag 9 januari 2007 Student S.H. Welle Frans Halsstraat 5, III 1072 BJ Amsterdam +316 4176 4435 [email protected] Onderwijsinstelling Technische Universiteit Eindhoven Den Dolech 2 5600 MB Eindhoven Faculteit Technologie en Management Studie Technische Bedrijfskunde Afstudeerbegeleiders TU/e Eerste begeleider Prof dr. -

Aegon Fixed Income

Executing our strategy April 2014 Fixed income presentation aegon.com Key messages . Focus on executing our strategy is delivering clear results ► Strategic transformation to become a truly customer-centric company is well underway ► Solid business growth is driving increase in profitability ► Risk profile significantly improved . Executing on balanced capital deployment strategy, supporting a sustainable dividend . Making progress towards 2015 targets . Intention to remain on track to be within leverage target ranges by the end of 2014 2 Over 150 Life insurance, pensions years of & asset management history AA- financial Present in more than 25 strength rating markets throughout the Americas, Europe and Asia Underlying earnings before tax Revenue-generating investments Paid out in claims and benefits in 2013 in 2013 Over EUR 1.9 EUR 20 26,500 billion billion EMPLOYEES1 EUR 475 billion1 Aegon at a glance 1) As per December 31, 2013 3 Building on leading market positions United States United Kingdom The Netherlands China of America # 7 Individual pensions # 1 Group pensions # 11 of foreign-owned life # 5 Individual life # 3 Group pensions # 6 Individual life insurers in China # 8 Variable Annuities # 10 Individual protection # 6 Accident & health # 12 Pensions # 10 Annuities # 10 Property & casualty Japan Canada Central & Spain # 1 Variable annuities # 5 Universal life Eastern Europe Historic positions do not reflect # 6 Term life # 1 Household in Hungary current business India # 6 Life in Hungary Start up # 3 Pensions Romania1 Brazil # -

Controversial Arms Trade

Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Anniek Herder Alex van der Meulen Michel Riemersma Barbara Kuepper 18 June 2015, embargoed until 18 June 2015, 00:00 CET Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Summary ..................................................................................................................... i Samenvatting .......................................................................................................... viii Introduction ................................................................................................................ 1 Chapter 1 Background ...................................................................................... 2 1.1 What is at stake? ....................................................................................... 2 1.2 Trends in international arms trade .......................................................... 3 1.3 International standards............................................................................. 4 1.3.1 Arms embargoes ......................................................................................... 4 1.3.2 EU arms export policy ................................................................................. 4 1.3.3 Arms Trade Treaty .....................................................................................