Definitive Information Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Continuing Professional Development (Cpd) Cpd Council for Sanitary Engineering List of Accredited Programs As of November 9, 2018

CONTINUING PROFESSIONAL DEVELOPMENT (CPD) CPD COUNCIL FOR SANITARY ENGINEERING LIST OF ACCREDITED PROGRAMS AS OF NOVEMBER 9, 2018 PROGRAM APPROVED NAME OF PROVIDER ACCR. NO. TITLE OF THE PROGRAM DATE OF CONDUCT PLACE CONDUCTED CREDIT UNIT FROM TO 2014 Philippine Society of Sanitary Engineers, Inc. 2014 Mid Year National Convention The Lake Hotel Tagaytay, 1 (PSSE) 2009-001-007 and General Assembly 8-May-14 10-May-14 Tagaytay City 7.75 2015 Philippine Society of PSSE 2012 National Convention Sanitary Engineers, Inc. Sanitary Engineers and the Green Great Eastern Hotel, Quezon 1 (PSSE) 2009-001-008 Growth Movement 15-Nov-12 17-Nov-12 Avenue, Quezon City 15 PSSE 2013 National Midyear Philippine Society of Convention Theme: "Sanitation: An Sanitary Engineers, Inc. Emerging Challenge in 2 (PSSE) 2009-001-009 Urbanization" 23-May-13 25-May-13 Citylight Hotel, Baguio City 15 Philippine Society of Sanitary Engineers, Inc. 3 (PSSE) 2009-001-010 2013 Annual National Convention 21-Nov-13 23-Nov-13 Hotel H2O, Luneta, Manila 15 Philippine Society of Sanitary Engineers, Inc. Crowne Plaza Hotel, Ortigas, 4 (PSSE) 2009-001-011 2014 Annual National Convention 20-Nov-14 22-Nov-14 Quezon, City 5 Philippine Society of Sanitary Engineers, Inc. Century Park Hotel, Malate, 5 (PSSE) 2009-001-012 2015 Midyear National Convention 23-Apr-15 25-Apr-15 Manila 15 2016 Philippine Society of Sanitary Engineers, Inc. 1 (PSSE) 2009-001-013 2015 Annual National Convention 3-Dec-15 5-Dec-15 Hotel H2O, Luneta, Manila 8 Philippine Society of Sanitary Engineers, Inc. 2 (PSSE) 2009-001-014 2016 Midyear National Convention 12-May-16 14-May-16 Citylight Hotel, Baguio City 9 Philippine Society of Sanitary Engineers, Inc. -

06 Power and Politics in the Philippine Banking Industry.Pdf

• Power and Politics in the Philippine Banking Industry An Analysis of State-Oligarchy Relations· Paul D. Hutchcroft·· Neither Lucio TannorVicente Tan, two Filipino-Chinese businessmen, were particularly noteworthy in 1965, the year that Ferdinand Marcos first • became President. Lucio was busy setting upa small cigarette factory inIlocos, the home region of Marcos, while Vicente (no relation to Lucio) was building updiversified operations in insurance andrealestate, andbadjust acquired 10% interest in a minor bank. By 1986, the yearthat Marcos was deposed, Lucio Tanwas a notorious crony who had built a large financial and manufacturing conglomerate, based around a bank said to be 60% owned by Marcos himself. Vicente Tan, on the otherhand, had beenforced during the martial law years to signover ownership of two banks to associates of Herminio Disini, a golfing partner and crony of President Marcos's, in orderto end three years of imprisonment without trial. In the late 1980s, his business empire was so diminished as to be based in a • small apartment fronting Manila Bay. I The stories of the fate of these two men, I will argue, shed light on thenature oftherelationship between thePhilippine state anddominant economic interests. For each Lucio Tan, one can think of scores of other oligarchs and cronies, both Filipino and Filipino-Chinese, who have plundered the state for particularistic advantage--not only during the time of Marcos, but also in the pre-martial law period (1946-72) and in the Aquino years, since 1986. Vicente Tan is perhaps a more unusual figure, in certain respects, but his decline highlights both theenormous limitations ofwealth accumulation inthePhilippines • forthose lacking access tothepolitical machinery, andtheharsh punitive powers that Philippine state officials are occasionally capable of exacting on their enemies. -

The Socio-Cultural and Political Dimensions of the Economic Success of the Chinese in the Philippines*

Perspectives on China and the Chinese Through the Years: Perspectives on China Aand Retrospective the Chinese Collection, Through 1992-2013 the Years: A Retrospective Collection, 1992-2013 Chinese Studies Journal, vol. 13 | October 2020 | ISSN: 0117-1933 THE SOCIO-CULTURAL AND POLITICAL DIMENSIONS OF THE ECONOMIC SUCCESS OF THE CHINESE IN THE PHILIPPINES* Teresita Ang See Introduction From the barren hills of Fujian and Guangdong to the corporate boardrooms of Makati; from crude sweatshops to huge commercial complexes; from the barefoot vendors in tattered clothing to owners of state-of-the-art megamalls; from illiterate peasants to prominent professionals – the Chinese in the Philippines have indeed come a long, long way. Behind these triumphs, however, were the silent years of hardships and struggles; of blood, sweat, and tears that brought them to where they or at least where their children are today. While some of the poignant stories of the early immigrants have been documented, they are focused mostly on the success stories. What few people realize is that for every success story, there are more untold stories of failures and heartbreaks. They have remained _________________________ *First published in Ellen Huang Palanca, ed. China, Taiwan, and the Ethnic Chinese in the Philippine Economy, Chinese Studies, vol. 5. Quezon City: Philippine Association for Chinese Studies, 1995, pp. 93-106. 142 © 2020 Philippine Association for Chinese Studies The Socio-Cultural and Political Dimensions of the Economic Success of the Chinese in the Philippines undocumented because the Chinese will be that last to remember or record incidents where they lose face. While we dissect the role of the Chinese in the Philippine economy in academic forums, it would also be worthwhile to recall the many untold stories behind each economic success that is presented. -

Arianas %Riety;~ Micronesia's Leading Newspaper Since 1972 · ~ ~ La Fiesta Reports Guam

~--·. arianas %riety;~ Micronesia's Leading Newspaper Since 1972 · ~ ~ La Fiesta reports Guam. legislature .1,· 30% revenue drop I Mall tenants come and go, says GM By Jojo Dass with tenants closing down rented in 'land:mark win' Variety News Staff space for new ones to occupy. LA FIESTA San Roque, seen as "It's not permanent," he said By Jojo Santo Tomas legislation. Saipan 's premier shopping mall, though. Variety News Staff Charfauros played a tape he is experiencing a 30-percent rev- Aria, nevertheless, dismissed HAGATNA - In a ruling that received anonymously during ses i enue decline due to decreasing the possibility of closing down effectively kills a current Supe sion last week, causing a stir that t tourist arrivals, Toshiro Aria, its the five-year old retail estab- rior Court case regarding tapes of led to a civil case, a temporary ' general manager, said yesterday. lishment, saying management is telephone conversations played restraining order, over a dozen i "We are suffering from that "doing every effort" to survive. inside the legislature last week, subpoenas, and emergency appeal 1 (low tourist arrivals). Sales are This, he said, include making the Supreme Court of Guam to the Supreme Court. '. getting low. Thirty percent of the mall more enticing with ten- : granted a stay on Civil Case No. The Supreme Court has can : the .revenues decreased in the ants doing more services to sur- i 2211-98. celled all depositions and lifted past nine months," said Aria, in vive. "This is a landmark victory, and the restraining order which had an interview. -

Philippine Airlines, Inc

PAL Holdings, Inc. Sustainability Report 2020 Contents 26 -- Governance 27 Compliance with laws and 32 Data security regulations 33 Customer privacy Introduction 28 Effective, accountable, and transparent governance 03 The Chairman’s message 04 Executive summary 06 About the Company 34 -- Social 14 Company highlights 35 Health and safety 44 Employee training and development 50 Customer management 19 -- About this report 53 Employee hiring and benefits 20 Purpose, Reporting Standards, Scope and Coverage 20 PHI’s Material Topics 54 -- Environment 55 Resource Management 58 Ecosystem and biodiversity 58 Environmental impact 21 -- Economic 22 Direct economic value generated and distributed 25 Outlook 62 – Our people and values 63 Employee welfare and communication 64 Corporate social responsibilities The Chairman's Message To our Dear Stakeholders, The mission of sustainability gained special force in 2020 when PAL We transformed our services to incorporate New Normal Holdings Inc. faced the greatest challenge in its history, no less than safety protocols that protect our employees and passengers: the survival of the PAL Group, which includes Philippine Airlines full Personal Protective Equipment (PPE) for our crew; modified (PAL) and PAL express (PALex), and their transformation into viable meals, amenities, facilities and digital assets to promote airline businesses for a vastly changed aviation market. healthy travel practices; stronger cleaning and disinfection measures; and new testing centers that helped authorities Impact of a Global Pandemic reopen borders and allow safe increases in travel volumes. The worldwide spread of COVID-19 shut down aviation markets and crippled the economies of most nations. PAL and PALex were forced Public Service and Public Accolades to cancel flights, affecting millions of passengers, wiping out more Our efforts as a responsible flag carrier contributed greatly to than USD 2 Billion in revenues and placing extreme pressure on the Philippine repatriation drive, with PAL flying majority of the liquidity. -

The Philippines Illustrated

The Philippines Illustrated A Visitors Guide & Fact Book By Graham Winter of www.philippineholiday.com Fig.1 & Fig 2. Apulit Island Beach, Palawan All photographs were taken by & are the property of the Author Images of Flower Island, Kubo Sa Dagat, Pandan Island & Fantasy Place supplied courtesy of the owners. CHAPTERS 1) History of The Philippines 2) Fast Facts: Politics & Political Parties Economy Trade & Business General Facts Tourist Information Social Statistics Population & People 3) Guide to the Regions 4) Cities Guide 5) Destinations Guide 6) Guide to The Best Tours 7) Hotels, accommodation & where to stay 8) Philippines Scuba Diving & Snorkelling. PADI Diving Courses 9) Art & Artists, Cultural Life & Museums 10) What to See, What to Do, Festival Calendar Shopping 11) Bars & Restaurants Guide. Filipino Cuisine Guide 12) Getting there & getting around 13) Guide to Girls 14) Scams, Cons & Rip-Offs 15) How to avoid petty crime 16) How to stay healthy. How to stay sane 17) Do’s & Don’ts 18) How to Get a Free Holiday 19) Essential items to bring with you. Advice to British Passport Holders 20) Volcanoes, Earthquakes, Disasters & The Dona Paz Incident 21) Residency, Retirement, Working & Doing Business, Property 22) Terrorism & Crime 23) Links 24) English-Tagalog, Language Guide. Native Languages & #s of speakers 25) Final Thoughts Appendices Listings: a) Govt.Departments. Who runs the country? b) 1630 hotels in the Philippines c) Universities d) Radio Stations e) Bus Companies f) Information on the Philippines Travel Tax g) Ferries information and schedules. Chapter 1) History of The Philippines The inhabitants are thought to have migrated to the Philippines from Borneo, Sumatra & Malaya 30,000 years ago. -

February 19, 2011 February 15, 2014

februarY 15, 2014 hawaii filiPino ChroniCle 1 ♦ FEBRUARY 15,19, 20142011 ♦ OPINION HAWAII-FILIPINO NEWS LEGAL NOTES Driverless Cars? ConGen torres, maYor hints of Possible Yes, almost Just CalDwell leaD traDe ComPromise on arounD the Corner mission to the PhiliPPines immiGration PRESORTED HAWAII FILIPINO CHRONICLE STANDARD 94-356 WAIPAHU DEPOT RD., 2ND FLR. U.S. POSTAGE WAIPAHU, HI 96797 PAID HONOLULU, HI PERMIT NO. 9661 2 hawaii filiPino ChroniCle februarY 15, 2014 EDITORIALS FROM THE PUBLISHER or hopeless romantics, February Publisher & Executive Editor The Mega Rich as 14th is one of the most antici- Charlie Y. Sonido, M.D. pated days of the year. It’s a day Publisher & Managing Editor Role Models that’s set aside to celebrate the Chona A. Montesines-Sonido ill Gates and Warren Buffet are household names in powerful human emotion called Associate Editors F love. When you think about it, Dennis Galolo the U.S. The multi-billionaires are rich, powerful and we should be showing our love Edwin Quinabo influential. But how many of us know of the late to those closest to us every day and not just Corliss Lamont, a Harvard graduate born of Wall Contributing Editor on special occasions like Valentine’s. On that note, Happy Belinda Aquino, Ph.D. Street wealth who championed the causes of poor B Valentine’s Day to all of you! Creative Designer people his entire life? Or Maud Younger (1870- Our cover story for this issue—“The 10 Wealthiest People Junggoi Peralta 1936), who despite coming from a wealthy family in San Francisco, in the Philippines” according to Forbes Magazine, was written worked for five years as a waitress to learn about working class Photography by our Philippine correspondent Gregory Garcia. -

Minutes of the Annual Stockhoders Meeting of Lt

MINUTES OF THE ANNUAL STOCKHODERS’ MEETING OF LT GROUP, INC. HELD ON MAY 7, 2019 AT THE KACHINA ROOM, CENTURY PARK HOTEL AT 10:00 A.M. STOCKHOLDERS: In Person 41,809 shares 0.000% By Proxy 8,365,125,489 shares 77.77% 8,365,167,298 shares 77.77% PRESENT: LUCIO C. TAN - CHAIRMAN CARMEN K. TAN - DIRECTOR HARRY C. TAN - DIRECTOR LUCIO K. TAN, JR. - DIRECTOR MICHAEL G. TAN - DIRECTOR/PRESIDENT VIVIENNE K. TAN - DIRECTOR JUANITA T. TAN LEE - DIRECTOR/TREASURER JOHNIP G. CUA - INDEPENDENT DIRECTOR WILFRIDO E. SANCHEZ - INDEPENDENT DIRECTOR FLORENCIA G. TARRIELA - INDEPENDENT DIRECTOR ABSENT: MARY G. NG - INDEPENDENT DIRECTOR I. CALL TO ORDER The Chairman, Dr. Lucio C. Tan, called the meeting to order and requested the President, Mr. Michael G. Tan to preside over the rest of the meeting. II. PROOF OF THE REQUIRED NOTICE OF THE MEETING Mr. Michael G. Tan inquired if the required notices of the meeting had been sent to the stockholders. The Corporate Secretary, Ms. Ma. Cecilia L. Pesayco, certified that proper notices of the meeting had been sent to all stockholders of record as early as April 2, 2019 or more than thirty-five (35) days, in full compliance with Rule 20 of the Securities Regulation Code that requires written notice of the meeting be sent to all stockholders of record at least twenty-eight (28) days prior to the date of the meeting. The Corporate Secretary therefore certify that notices for this meeting were duly sent. III. PROOF OF PRESENCE OF QUORUM The Corporate Secretary certified that there were present in person or by proxy, a total of 8,365,167,298 shares, or 77.77% of the Company’s 10,821,388,889 total issued and outstanding shares, thus a quorum existed for the valid transaction of business that may properly come before the body. -

Aliseo References You’Re As Good As the Company You Keep !

“At Your Service ...” Aliseo References You’re As Good As the Company You Keep ! Mit über 30 Jahre Erfahrung im internationalen Hotelgeschäft und mehr als 1 Million Installationen auf 6 Kontinenten haben ein einzigartiges Verständnis für neue Trends, kulturelle und geographische Unterschiede, Sicherheitsstandards und elektrische Voraussetzungen hervorgebracht. „Design-sensitive, klassische Produkte, technologisch ihrer Zeit voraus, erprobt im tagtäglichen Härtetest.“ Nachstehend nur einige unserer Referenzen von Hotels, die unsere Produkte einsetzen . With over thirty years of experience and more than 1 million installations on 6 continents, Aliseo has a unique understanding of hospitality needs - from design dictates and cultural sensitivities to electrical requirements and safety standards. By incorporating the latest technology with the needs of today’s travellers, Aliseo has developed a wide range of innovative products that bring value to the hotelier and convenience to their guest. A dedication to quality, design and innovation that is shared by many of the world’s top hoteliers. These are but a few . ALGERIA St. Antoner Hof St. Anton am Arlberg Sheraton Resort & Towers Club des Pins Biohotel Daberer St. Daniel Constantine Marriott Hotel Constantine Romantikhotel Weisses Rössl St. Wolfgang Le Meridien Oran Hotel Hochschober Turracher Höhe Sheraton Oran Hotel Oran Schlosshotel Velden am Royal Golden Tulip Skikda Wörthersee Renaissance - Tlemcen Hotel Tlemcen Seehotel Hubertushof Velden am Wörthersee Ana Grand Hotel Vienna ANDORRA -

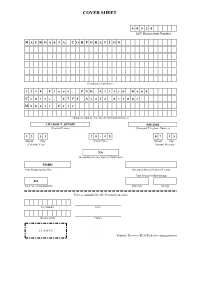

SEC Form 20-IS MAC 2015

COVER SHEET 4 0 5 2 4 SEC Registration Number M A C R O A S I A C O R P O R A T I O N (Company’s Full Name) 1 2 t h F l o o r , P N B A l l i e d B a n k C e n t e r , 6 7 5 4 A y a l a A v e n u e , M a k a t i C i t y (Business Address: No. Street City/Town/Province) AMADOR T. SENDIN 840-2001 (Contact Person) (Company Telephone Number) 1 2 3 1 2 0 - I S 0 7 1 5 Month Day (Form Type) Month Day (Calendar Year) (Annual Meeting) NA (Secondary License Type, If Applicable) MSRD Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 861 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. ANNUAL STOCKHOLDERS’ MEETING JULY 15, 2016 Kachina Room, Century Park Hotel, 599 P. Ocampo Sr. Street, Malate, Manila DEFINITIVE INFORMATION STATEMENT PROXY KNOW ALL MEN BY THESE PRESENTS: The undersigned, a stockholder of MACROASIA CORPORATION (“Corporation”), hereby constitutes and appoints _________________________ with power of substitution, to be his/her/its true and lawful Attorney, agent, and proxy to attend and represent the undersigned and to vote all shares registered his/her/its name in the books of the Corporation or owned by the undersigned, at the Annual Stockholders’ Meeting of the Corporation on Friday, 15 July 2016 at 3:00 P.M. -

Aliseo References You’Re As Good As the Company You Keep !

“At Your Service ...” Aliseo References You’re As Good As the Company You Keep ! Mit über 30 Jahre Erfahrung im internationalen Hotelgeschäft und mehr als 1 Million Installationen auf 6 Kontinenten haben ein einzigartiges Verständnis für neue Trends, kulturelle und geographische Unterschiede, Sicherheitsstandards und elektrische Voraussetzungen hervorgebracht. „Design-sensitive, klassische Produkte, technologisch ihrer Zeit voraus, erprobt im tagtäglichen Härtetest.“ Nachstehend nur einige unserer Referenzen von Hotels, die unsere Produkte einsetzen . With over thirty years of experience and more than 1 million installations on 6 continents, Aliseo has a unique understanding of hospitality needs - from design dictates and cultural sensitivities to electrical requirements and safety standards. By incorporating the latest technology with the needs of today’s travellers, Aliseo has developed a wide range of innovative products that bring value to the hotelier and convenience to their guest. A dedication to quality, design and innovation that is shared by many of the world’s top hoteliers. These are but a few . ALGERIA St. Antoner Hof St. Anton am Arlberg Sheraton Resort & Towers Club des Pins Biohotel Daberer St. Daniel Constantine Marriott Hotel Constantine Romantikhotel Weisses Rössl St. Wolfgang Le Meridien Oran Hotel Hochschober Turracher Höhe Sheraton Oran Hotel Oran Schlosshotel Velden am Royal Golden Tulip Skikda Wörthersee Renaissance - Tlemcen Hotel Tlemcen Seehotel Hubertushof Velden am Wörthersee Ana Grand Hotel Vienna ANDORRA -

(CAO) As of 05 February 2021

ACCOMMODATION ESTABLISHMENTS WITH CERTIFICATE OF AUTHORITY TO OPERATE (CAO) as of 05 February 2021 NAME OF ACCREDITATION CERTIFICATE OPERATIONAL QUARANTINE OPEN FOR ADDRESS CONTACT DETAILS CLASSIFICATION ESTABLISHMENT STATUS ISSUED STATUS FACILITY LEISURE CORDILLERA ADMINISTRATIVE REGION (CAR) BAGUIO CITY (074) 422-2075-76-80/ John Hay Special theforestlodge@campjohnhayhotel THE FOREST LODGE AT Economic Zone, Loakan s.ph/ Accredited 4 STAR HTL CAO OPEN No Yes CAMP JOHN HAY Road, Baguio City [email protected] h The Manor at Camp John THE MANOR AT CAMP (074) 424-0931 to 50/ Hay, Loakan Road, Accredited 4 STAR RES CAO OPEN No Yes JOHN HAY [email protected] Baguio City #1 J Felipe Street, (074) 619-0367/ HOTEL ELIZABETH Gibraltar Road, Baguio salesaccount2.baguio@hotelelizab Accredited 3 STAR HTL CAO OPEN No Yes BAGUIO City eth.com.ph #40 Bokawkan Rd., 09173981120/ (074) 442-3350/ Mabuhay PINE BREEZE COTTAGES Accredited CAO OPEN No Yes Baguio City [email protected] Accommodation #01 Apostol St., Corner (074) 442-1559/ 09176786874/ MINES VIEW PARK HOTEL Outlook Drive, Mines 09190660902/ Accredited Hotel CAO OPEN No Yes View, Baguio City [email protected] (074) 619-2050 (074) 442-7674/ Country Club Road, BAGUIO COUNTRY CLUB [email protected] Accredited 5 STAR Resort CAO OPEN No Yes Baguio City [email protected] [email protected] #37 Sepic St. Campo (074) 424-6092 (074) 620-3117/ NYC MANHATTAN HOTEL Accredited Hotel CAO OPEN No Yes Filipino, Baguio City [email protected]