Enterprise Productivity Measurement Framework for ERP in Indian Refineries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India: Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil-Fuels

INDIA: INVENTORY OF ESTIMATED BUDGETARY SUPPORT AND TAX EXPENDITURES FOR FOSSIL-FUELS Energy resources and market structure India is one of the fastest growing energy markets in the world. The country is the world’s third largest coal producer owing to its large deposits. Coal is the leading primary fuel in India’s energy mix, accounting for 44% of the country’s total primary energy supply (TPES), with thermal power plants making up the majority of coal consumption. Biomass accounts for 25% of total energy use, followed by oil and natural gas, which account respectively for 22% and 7% of the country’s energy needs. Remaining energy sources, such as nuclear power and hydro-electricity, account for about 1% each. The country’s proven reserves of oil were 5.5 billion barrels as of December 2012; nonetheless, domestic production falls far short of domestic demand and the country depends heavily on imported crude oil. The state-owned coal company, Coal India Limited (CIL), retains a near monopoly of coal extraction, with over 90% of domestic coal extraction attributed to government-controlled mines. Most coal mining occurs in the states of Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Orissa, and West Bengal. Market reforms are being implemented to bring competition and transparency to the coal sector. The government has been grappling to get an effective regulatory framework in place, which includes the loosening of regulations for the coal industry, with the objective of moving some grades of coal closer to international market prices, and allocating additional coal blocks through a transparent open bidding process. -

Government of India Ministry of Micro, Small and Medium Enterprises

GOVERNMENT OF INDIA MINISTRY OF MICRO, SMALL AND MEDIUM ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 4232 TO BE ANSWERED ON 07.01.2019 PUBLIC PROCUREMENT POLICY 4232. SHRI ADHALRAO PATIL SHIVAJIRAO: SHRI SHRIRANG APPA BARNE: SHRI KUNWAR PUSHPENDRA SINGH CHANDEL: DR. SHRIKANT EKNATH SHINDE: SHRI ANANDRAO ADSUL: SHRI VINAYAK BHAURAO RAUT: Will the Minister of MICRO, SMALL AND MEDIUM ENTERPRISES be pleased to state: (a) the details of the total annual procurement of goods and services by each Public Sector Enterprise (PSE) in the year 2014-15, 2015-16, 2016-17 and 2017-18; (b) the quantity of calculated value of goods and services procured under Public Procurement Policy Order, 2012 during the said period in each PSE; (c) the status of procurement under this policy from MSMEs owned by SC/ST and non-SC/STs during the said period by each PSE; (d) whether the public procurement policy is not being complied with by many Government departments/PSEs; and (e) if so, the details thereof and the reasons therefor along with corrective steps taken/being taken by the Government in this regard? ANSWER MINISTER OF STATE (INDEPENDENT CHARGE) FOR MICRO, SMALL AND MEDIUM ENTERPRISES (SHRI GIRIRAJ SINGH) (a) to (e): The details of annual procurement of goods & services by the Central Public Sector Enterprise (CPSE) as per information provided by Department of Public Enterprises (DPE) are as under: Year No. of Total Procurement Procurement from MSEs CPSEs Procurement From MSEs owned by SC/ST (Rs. in Crore) (Rs. in Crore) Entrepreneur (Rs. in Crore) 2014-15 133 131766.86 15300.57 59.37 2015-16 132 279167.15 12566.15 50.11 2016-17 142 245785.31 25329.44 400.87 2017-18 169 280785.49 24226.51 442.52 Ministry of MSME has taken several measures for effective implementation of the Public Procurement Policy. -

India CCS Scoping Study: Final Report

January 2013 Project Code 2011BE02 India CCS Scoping Study: Final Report Prepared for The Global CCS Institute © The Energy and Resources Institute 2013 Suggested format for citation T E R I. 2013 India CCS Scoping Study:Final Report New Delhi: The Energy and Resources Institute. 42pp. [Project Report No. 2011BE02] For more information Project Monitoring Cell T E R I Tel. 2468 2100 or 2468 2111 Darbari Seth Block E-mail [email protected] IHC Complex, Lodhi Road Fax 2468 2144 or 2468 2145 New Delhi – 110 003 Web www.teriin.org India India +91 • Delhi (0)11 ii Table of Contents 1. INTRODUCTION ..................................................................................................................... 1 2. COUNTRY BACKGROUND ...................................................................................................... 1 3. CO2 SOURCES ......................................................................................................................... 7 4. CURRENT CCS ACTIVITY IN INDIA ..................................................................................... 15 5. ECONOMIC ANALYSIS .......................................................................................................... 19 6. POLICY & LEGISLATION REVIEW ......................................................................................... 26 7. CAPACITY ASSESSMENT ...................................................................................................... 27 8. BARRIERS TO CCS IMPLEMENTATION IN INDIA ............................................................... -

PRSI National Awards-2020 Winners

PRSI NATIONAL AWARDS- 2020 Results Public Relations Society of India www. prsi.org.in PRSI NATIONAL AWARDS - 2020 No of S No Category Name of Organization entries 1 First Prize HP Samachar Hindustan Petroleum Corporation Ltd – Mumbai House Journal (Hindi) Second Petroleum Swar Prize Bharat Petroleum Corporation Ltd – Mumbai Third Prize Prayas Numaligarh Refinery Limited – Guwahati 2 First Prize Sail News House Journal (English) Steel Authority of India - New Delhi First Prize Varta Garden Reach Shipbuilders & Engineers Ltd. Second HP News Prize Hindustan Petroleum Corporation Ltd – Mumbai Second Kribhco News Prize Kribhco, Noida Third Prize IndianOil News Indian Oil Corporation - Marketing Division HO,Mumbai 3 Newsletter (English) First Prize Heritage Institute of Technology / Kalyan Bharti Trust, kolkata Second Ordnance Factory Board (OFB), Prize Kolkata Third Prize Aditya Birla Fashion & Retail Limited - Bengaluru, Karnataka / Mumbai 4 Third Prize Indian Oil Corporation Ltd - Barauni Newsletter (Hindi) Refinery ,Barauni 5 First Prize NTPC Ltd - New Delhi Special/Prestige Publication Second Steel Authority of India - New Delhi Prize Third Prize Indian Oil Corporation - Marketing Division (HO), Mumbai 6 Coffee Table Book First Prize Indian Oil Corporation - Marketing Division (HO) Second Garden Reach Shipbuilders & Prize Engineers Ltd. Kolkata Third Prize AIRADS Ltd. Third Prize Ordnance Factory Board (OFB) Kolkata 7 Sustainable Development Report First Prize ITC Ltd – Kolkata Second Indian Oil Corporation Ltd - Prize Corporate Office, New -

C:\Docume~1\Mahesh~1.Bud

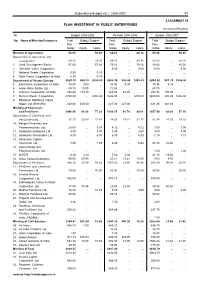

Expenditure Budget Vol. I, 2006-2007 39 STATEMENT 14 PLAN INVESTMENT IN PUBLIC ENTERPRISES (In crores of Rupees) Sl. Budget 2005-2006 Revised 2005-2006 Budget 2006-2007 No. Name of Ministry/Enterprise Total Budget Support Total Budget Support Total Budget Support Plan Plan Plan Outlay Equity Loans Outlay Equity Loans Outlay Equity Loans Ministry of Agriculture 58.00 ... 58.00 84.16 ... 84.16 50.00 ... 50.00 Department of Agriculture and Cooperation 58.00 ... 58.00 84.16 ... 84.16 50.00 ... 50.00 1. Land Development Banks 57.00 ... 57.00 79.16 ... 79.16 45.00 ... 45.00 2. Damodar Valley Corporation ... ... ... 5.00 ... 5.00 5.00 ... 5.00 3. National Seeds Corporation 0.30 ... 0.30 ... ... ... ... ... ... 4. State Farms Corporation of India 0.70 ... 0.70 ... ... ... ... ... ... Department of Atomic Energy 5529.70 568.10 2004.00 4205.38 300.05 1280.03 4294.34 991.19 1606.00 5. Electronics Corporation of India 34.00 9.00 ... 34.00 9.00 ... 39.34 9.34 ... 6. Indian Rare Earths Ltd. 85.10 10.00 ... 72.80 ... ... 80.79 ... ... 7. Uranium Corporation of India 280.60 119.10 ... 225.55 64.05 ... 292.36 100.00 ... 8. Nuclear Power Corporation 4700.00 ... 2004.00 3646.03 ... 1280.03 3400.00 400.00 1606.00 9. Bharatiya Nabhikiya Vidyut Nigam Ltd (BHAVINI) 430.00 430.00 ... 227.00 227.00 ... 481.85 481.85 ... Ministry of Chemicals and Fertilisers 1096.96 91.09 77.29 1109.35 41.70 80.61 1057.54 88.39 57.15 Department of Chemicals and Petrochemicals 97.70 53.60 21.00 49.33 18.21 31.12 91.46 47.53 18.15 10. -

Bharat Petroleum Corporation Ltd

Bharat Petroleum Corporation Ltd. Investor Presentation February 2016 Disclaimer No information contained herein has been verified for truthfulness completeness, accuracy, reliability or otherwise whatsoever by anyone. While the Company will use reasonable efforts to provide reliable information through this presentation, no representation or warranty (express or implied) of any nature is made nor is any responsibility or liability of any kind accepted by the Company or its directors or employees, with respect to the truthfulness, completeness, accuracy or reliability or otherwise whatsoever of any information, projection, representation or warranty (expressed or implied) or omissions in this presentation. Neither the Company nor anyone else accepts any liability whatsoever for any loss, howsoever, arising from use or reliance on this presentation or its contents or otherwise arising in connection therewith. This presentation may not be used, reproduced, copied, published, distributed, shared, transmitted or disseminated in any manner. This presentation is for information purposes only and does not constitute an offer, invitation, solicitation or advertisement in any jurisdiction with respect to the purchase or sale of any security of BPCL and no part or all of it shall form the basis of or be relied upon in connection with any contract, investment decision or commitment whatsoever. The information in this presentation is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the Company. We do not have any obligation to, and do not intend to, update or otherwise revise any statements reflecting circumstances arising after the date of this presentation or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition. -

Global Notice Inviting Expression of Interest (Eoi)

HINDUSTAN PETROLEUM BHARAT PETROLEUM CORPORATION LIMITED CORPORATION LIMITED (A Govt of India Undertaking) (A Govt of India Undertaking) Mumbai, India Mumbai, India GLOBAL NOTICE INVITING EXPRESSION OF INTEREST (EOI) FOR SUPPLY OF HYDROGEN GAS TO REFINERIES OF HPCL AND BPCL AT MAHUL, MUMBAI BY INSTALLATION OF HYDROGEN GENERATION UNIT (HGU) ON BUILD–OWN–OPERATE (B-O-O) BASIS NEAR THEIR REFINERIES PREPARED AND ISSUED BY MECON LIMITED (A Govt. of India Undertaking) Mumbai, India 1. PURPOSE OF NOTICE Hindustan Petroleum Corporation (HPCL) is currently enhancing its capability to produce environment friendly fuel products to the more stringent Euro III and IV specifications and to meet this objective, Mumbai Refinery of HPCL requires 20,000 TPA of additional Hydrogen to supplement their internal generating capacity at Mahul, Mumbai. HPCL proposes to outsource this additional Hydrogen requirement and HPCL may also decide to phase out its existing Hydrogen Generation Units In future leading to increase in the requirement of outsourced Hydrogen. Bharat Petroleum Corporation (BPCL) is also setting up process units within their refinery at Mahul, Mumbai to produce products compliant to Euro III and IV fuel specifications. BPCL proposes to phase out a part of their internal hydrogen generation facility, by outsourcing of Hydrogen to the tune of 40,000 TPA.. Hydrogen Generation Unit (HGU) Hydrogen requirement for HPCL and BPCL is as follows: Sl. Description Requirement TOTAL No. HPCL BPCL 1 Average Hourly Flow 24,500 49,000 73,500 (Nm3/hr) 2. Annual Requirement 20,000 40,000 60,000 (Tonnes/year) Steam generated as a by-product in the process of production of Hydrogen may not be consumed either by HPCL or BPCL. -

(Eoi) for Pre- Qualification of Bidders to Provide Technolo

OIL INDIA LIMITED (A GOVERNMENT OF INDIA ENTERPRISE) And NUMALIGARH REFINERY LIMITED (A GOVERNMENT OF INDIA ENTERPRISE) EXPRESSION OF INTEREST (EOI) FOR PRE- QUALIFICATION OF BIDDERS TO PROVIDE TECHNOLOGY AND INSTALL A PLANT FOR CONVERSION OF WASTE PLASTIC TO HYDROCARBON FUELS ON BUILD, OPERATE &MAINTAIN MODEL (EOI Document No. : COMM/C22/2370) OIL INDIA LIMITED NUMALIGARH REFINERY LIMITED P.O. Duliajan, Dist. Dibrugarh Numaligarh, Dist. Golaghat Assam‐786 602 Assam‐785699 Page 1 of 11 Press Advertisement Expression of Interest Name of the Job : Provide Technology and Install a 10 TPD plant for conversion of Waste Plastic to Hydrocarbon Fuels, at Guwahati (Assam), on Build, Operate & Maintain (BOM) Model. The project shall be executed jointly by Oil India Ltd. (OIL) and Numaligarh Refinery Limited (NRL), as a CSR initiative. For details of complete EOI (no. COMM/C22/2370), interested parties may refer to respective websites of OIL and NRL (www.oil‐ india.com; www.nrl.co.in) Due date and time for submission of EOI: 19/06/2015, 15:00 Hrs Page 2 of 11 INVITATION FOR EXPRESSION OF INTEREST 1 INTRODUCTION Oil India limited (OIL), a Navratna Company under the Ministry of Petroleum andNatural gas, Government of India, is a premier National Oil Company engaged inthe business of Exploration, Production and Transportation of Crude Oil andNatural Gas. Numaligarh Refinery Limited (NRL) is a group company of Bharat Petroleum Corporation Limited operating a 3.0 MMTPA capacity petroleum refinery located at Numaligarh in Golaghat district of Assam. NRL is a Category‐I Miniratna Company and is certified under ISO 9001, ISO 14001, OHSAS 18001 and ISO 27001. -

Petr Oleum (Refiner Y and Marketing)

PETROLEUM (REFINERY AND MARKETING) (REFINERY Public Enterprises Survey 2015-2016 : Vol-II 97 6. Petroleum (Refinery & Marketing) (` in Crore) As on 31.03.2016, there were 8 Central Public Sector Net Profit/ Loss S. No. Enterprise Enterprises in the Petroleum (Refinery and Marketing) 2015-16 2014-15 group. The names of these enterprises along with their 1 BHARAT PETROLEUM CORPN. LTD. 7431.88 5084.51 year of incorporation in chronological order are given 2 CHENNAI PETROLEUM CORPORATION 770.68 -38.99 below: - LTD. 3 GAIL (INDIA) LTD. 2298.9 3039.17 Year of S. No. Enterprise 4 GAIL GAS LTD. 38.96 16.84 Incorporation 5 HINDUSTAN PETROLEUM CORPN. LTD. 3862.74 2733.26 1 INDIAN OIL CORPORATION LTD. 1964 6 INDIAN OIL CORPORATION LTD. 10399.03 5273.03 2 CHENNAI PETROLEUM CORPORATION LTD. 1965 7 MANGALORE REFINERY & 1148.16 -1712.23 3 BHARAT PETROLEUM CORPN. LTD. 1976 PETROCHEMICALS LTD. 4 HINDUSTAN PETROLEUM CORPN. LTD. 1952 8 NUMALIGARH REFINERY LTD. 1222.34 718.31 5 GAIL (INDIA) LTD. 1984 SUB TOTAL : 27172.69 15113.9 MANGALORE REFINERY & PETROCHEMICALS 6 1988 LTD. 6. Dividend: The details of dividend declared by the 7 NUMALIGARH REFINERY LTD. 1993 individual enterprises are given below: (` in Crore) 8 GAIL GAS LTD. 2008 Dividend S. No. Enterprise 2. The enterprises falling in this group are mainly 2015-16 2014-15 engaged in producing and selling of petroleum and 1 BHARAT PETROLEUM CORPN. LTD. 2241.56 1626.94 petroleum products such as diesel, kerosene, naphtha, 2 CHENNAI PETROLEUM CORPORATION 94.08 0 gas lubes, greases, chemical additives, lubricants, etc. -

ANSWERED ON:26.08.2004 FARMERS` LAND ACQUIRED by IOC/GAIL/ONGC Thummar Shri Virjibhai;Varma Shri Ratilal Kalidas

GOVERNMENT OF INDIA PETROLEUM AND NATURAL GAS LOK SABHA STARRED QUESTION NO:446 ANSWERED ON:26.08.2004 FARMERS` LAND ACQUIRED BY IOC/GAIL/ONGC Thummar Shri Virjibhai;Varma Shri Ratilal Kalidas Will the Minister of PETROLEUM AND NATURAL GAS be pleased to state: (a) the total number of refineries in the country run by the IOC/GAIL/ONGC and other PSUs under Ministry of Petroleum and how much land of the farmers has been acquired by them; (b) whether all such landless farmers have been provided any employment or rehabilitated: (c) if so, the details thereof State-wise; (d) if not, the reasons therefor; and (e) the steps taken to rehabilitate remaining farmers? Answer MINISTER OF PETROLEUM & NATURAL GAS AND PANCHAYATI RAJ (SHRI MANI SHANKAR AIYAR) (a) to (e): A statement is laid on the Table of the House. STATEMENT REFERED TO IN REPLY TO PARTS (a) TO (e) OF THE LOK SABHA STARRED QUESTION NO.446 BY SHRI V.K. THUMMAR AND SHRI RATILAL KALIDAS VARMA TO BE ANSWERED ON 26TH AUGUST, 2004 REGARDING FARMERS' LAND ACQUIRED BY IOC/GAIL/ONGC. (a)to(e): There are 17 Public Sector refineries operating in the country. Approximately 16097 acres of land have been acquired for setting up these refineries, as per details given in the Annex. All land owners, including farmers, were provided compensation as per the Land Acquisition Act,1894. In addition, as a rehabilitation measure, rehabilitation grants, training, self-employment, employment in the project etc. were also considered by the Public Sector Refineries for different projects. ANNEX REFERED TO IN REPLY TO PARTS (a) TO (e) OF THE LOK SABHA STARRED QUESTION NO.446 BY SHRI V.K. -

Petroleum (Refinery and Marketing)

PETROLEUM (REFINERY AND MARKETING) Public Enterprises Survey 2013-2014 : Vol-II 97 3HWUROHXP 5H¿QHU\ 0DUNHWLQJ (` in crore) As on 31.03.2014, there were 8 Central Public Sector S. Enterprise 1HW 3UR¿W /RVV (QWHUSULVHV LQ WKH 3HWUROHXP 5H¿QHU\ DQG 0DUNHWLQJ No. 2013-14 2012-13 group. The names of these enterprises along with their 1 BHARAT PETROLEUM 4060.88 2642.9 year of incorporation in chronological order are given CORPN. LTD. below: - 2 CHENNAI PETROLEUM -303.85 -1766.84 CORPORATION LTD. S. Enterprise Year of 3 GAIL (INDIA) LTD. 4375.27 4022.2 No. Incorporation 4 GAIL GAS LTD. 11.44 26.94 1 INDIAN OIL CORPORATION LTD. 1964 5 HINDUSTAN PETROLEUM 1733.77 904.71 2 CHENNAI PETROLEUM 1965 CORPN. LTD. CORPORATION LTD. 6 INDIAN OIL CORPORATION 7019.09 5005.17 3 BHARAT PETROLEUM CORPN. LTD. 1976 LTD. 4 HINDUSTAN PETROLEUM CORPN. 1976 7 MANGALORE REFINERY & 601.18 -756.91 LTD. PETROCHEMICALS LTD. 5 GAIL (INDIA) LTD. 1984 8 NUMALIGARH REFINERY 371.09 144.26 6 MANGALORE REFINERY & 1988 LTD. PETROCHEMICALS LTD. TOTAL : 17868.87 10222.43 7 NUMALIGARH REFINERY LTD. 1993 8 GAIL GAS LTD. 2008 6. Dividend: The details of dividend declared by the individual enterprises are given below: 2. The enterprises falling in this group are mainly engaged (` in crore) in producing and selling of petroleum and petroleum S. Enterprise Dividend SURGXFWV VXFK DV GLHVHO NHURVHQH QDSKWKD JDV OXEHV No. 2013-14 2012-13 greases, chemical additives, lubricants. Etc. 1 BHARAT PETROLEUM CORPN. 1229.24 795.39 7KH FRQVROLGDWHG ¿QDQFLDO SRVLWLRQ WKH ZRUNLQJ UHVXOWV LTD. -

Bharat Petroleum Corporation Ltd

Bharat Petroleum Corporation Ltd. Investor Presentation June 2015 Disclaimer No information contained herein has been verified for truthfulness completeness, accuracy, reliability or otherwise whatsoever by anyone. While the Company will use reasonable efforts to provide reliable information through this presentation, no representation or warranty (express or implied) of any nature is made nor is any responsibility or liability of any kind accepted by the Company or its directors or employees, with respect to the truthfulness, completeness, accuracy or reliability or otherwise whatsoever of any information, projection, representation or warranty (expressed or implied) or omissions in this presentation. Neither the Company nor anyone else accepts any liability whatsoever for any loss, howsoever, arising from use or reliance on this presentation or its contents or otherwise arising in connection therewith. This presentation may not be used, reproduced, copied, published, distributed, shared, transmitted or disseminated in any manner. This presentation is for information purposes only and does not constitute an offer, invitation, solicitation or advertisement in any jurisdiction with respect to the purchase or sale of any security of BPCL and no part or all of it shall form the basis of or be relied upon in connection with any contract, investment decision or commitment whatsoever. The information in this presentation is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the Company. We do not have any obligation to, and do not intend to, update or otherwise revise any statements reflecting circumstances arising after the date of this presentation or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition.