Gemologist Q1 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

White Collar Defense & Investigations Arrest of Executive of Leading

White Collar Defense & Investigations DECEMBER 2018 • NO. 3 Arrest of Executive of Leading Chinese Telecom Firm in Canada Evidences DOJ’s Far-Reaching Tools to Effectuate Recently Announced Initiative The recent arrest of a top executive of a Chinese company follows the U.S. Department of Justice’s (“DOJ”) newly announced “China Initiative.” The initiative consists of a task force aimed at identifying suspected Chinese trade theft cases for investigation and enforcement. The arrest is a bold move by the U.S. government and one that reinforces DOJ’s commitment to enforcing U.S. law against Chinese companies and executives. On December 1, 2018, Meng Wanzhou, the CFO of Chinese Act (“FCPA”) against Chinese companies that compete telecommunications company Huawei Technologies Co., against U.S. companies as a goal. Ltd., was arrested for extradition to the U.S. while switching planes in Canada. Ms. Meng is the eldest daughter of Ms. Meng’s arrest follows reports that Huawei has been Huawei’s founder, Ren Zhengfei. Huawei confirmed that Ms. under investigation by multiple U.S. government agencies. Meng faces prosecution in the Eastern District of New York. In 2012, a congressional report raised red flags about The charges against Ms. Meng were “unspecified” at the security risks posed by Huawei equipment. In 2016, the time of her arrest. U.S. Department of Commerce issued subpoenas to Huawei related to potential export law violations and later that The arrest comes a month after the DOJ announced the year, the U.S. Treasury Department’s Office of Foreign new “China Initiative” targeting Chinese companies and Assets Control (“OFAC”) issued a subpoena about a related individuals for unfair Chinese practices related to technology sanctions investigation. -

Canadian Views on China from Ambivalence to Distrust Canadian Views on China: from Ambivalence to Distrust

Research Paper Roland Paris US and the Americas Programme | July 2020 Canadian Views on China From Ambivalence to Distrust Canadian Views on China: From Ambivalence to Distrust Summary • Public opinion surveys in Canada indicate that attitudes towards China have hardened dramatically since the two countries became locked in a diplomatic dispute in late 2018. Whereas public views of China had long been ambivalent, they are now strongly negative. • Hardened Canadian attitudes are likely to persist, even if the current dispute ends. The two countries appear to have entered a new, warier phase in their relationship. A return to the status quo ante in bilateral relations is unlikely. • China’s detention of two Canadian citizens and its trade actions against Canada have startled the country. So has the Trump administration’s mercurial treatment of Canada and other US allies. These developments have highlighted risks that Canada faces in a world of intensified geopolitical rivalry, where Canada may be subject to direct forms of great-power coercion. • Although managing the current dispute with China is important, Canadian leaders understand that maintaining productive relations with the US and reliable access to its market is a vital national interest. Canada is not ‘neutral’ in the growing rivalry between the US and China. It will align with the US, but it will also seek to prevent tensions with China from escalating. 1 | Chatham House Canadian Views on China: From Ambivalence to Distrust Introduction China’s handling of the COVID-19 crisis, including its apparent suppression of information about the initial outbreak in Wuhan, has produced a backlash against Beijing in several countries.1 For many Canadians, however, these developments have reinforced existing misgivings. -

Huawei Founder Says Company Would Not Share User Secrets (Update) 15 January 2019, by Joe Mcdonald

Huawei founder says company would not share user secrets (Update) 15 January 2019, by Joe Mcdonald Huawei is China's first global tech brand. The United States, Australia, Japan and some other governments have imposed curbs on use of its technology over such concerns. "We would definitely say no to such a request," said Ren when asked how the company would respond to a government demand for confidential information about a foreign buyer of its telecom technology. Ren said neither he nor the company have ever received a government request for "improper information" about anyone. Ren Zhengfei, founder and CEO of Huawei, gestures Asked whether Huawei would challenge such an during a round table meeting with the media in order in court, Ren chuckled and said it would be Shenzhen city, south China's Guangdong province, up to Chinese authorities to "file litigation." Tuesday, Jan. 15, 2019. The founder of network gear and smart phone supplier Huawei Technologies said the Huawei is facing heightened scrutiny as phone tech giant would reject requests from the Chinese carriers prepare to roll out fifth-generation government to disclose confidential information about its technology in which Huawei is a leading competitor. customers. (AP Photo/Vincent Yu) 5G is designed to support a vast expansion of networks to serve medical devices, self-driving cars and other technology. That increases the cost of potential security failures and has prompted The founder of China's Huawei, the world's biggest governments increasingly to treat telecoms supplier of network gear to phone and internet communications networks as strategic assets. -

Huawei Board of Directors

Huawei Board of Directors DIRECTOR CRISIS MANAGER MODERATOR Priscilla Layarda Brayden Ning Sharon Lee CRISIS ANALYSTS Sahreesh Nawar Victoria Wang Huiyang (Harry) Chen UTMUN 2020 Huawei Board of Directors Contents Content Disclaimer 3 UTMUN Policies 4 Equity Concerns and Accessibility Needs 4 A Letter from Your Director 5 Historical Context 7 Global Technological Landscape 8 Reasons for the Ban 8 Effects of the Ban 8 Huawei Business Model 12 Core Business 12 Value Proposition 12 Customer Segments and Customer Relationships 13 Key Partners 13 Key Resources 14 Governance Structure 15 Finances 17 Sanctions and Privacy Concerns 18 US-China Trade Tensions 18 Supply-Chain Concerns 18 Potential Loss of Market for Current Products 19 Legal Challenges 20 Privacy and Security Concerns 20 Long-Term Strategic Plan 21 Pace of Innovation 21 Brand Image in the US 21 1 UTMUN 2020 Huawei Board of Directors Mergers and Acquisitions 21 Growth Markets 22 New Products 22 Questions to Consider 24 Further Research 25 Bibliography 26 2 UTMUN 2020 Huawei Board of Directors Content Disclaimer At its core, Model United Nations (MUN) is a simulatory exercise of diplomatically embodying, presenting, hearing, dissecting, and negotiating various perspectives in debate. Such an exercise offers opportunities for delegates to meaningfully explore possibilities for conflict resolution on various issues and their complex, even controversial dimensions – which, we recognize, may be emotionally and intellectually challenging to engage with. As UTMUN seeks to provide an enriching educational experience that facilitates understanding of the real-world implications of issues, our committees’ contents may necessarily involve sensitive or controversial subject matter strictly for academic purposes. -

HUAWEI ARREST: Canada Caught in a Political Tug of War

TABLE OF CONTENTS Video Summary & Related Content 3 Video Review 4 Before Viewing 5 While Viewing 7 Talk Prompts 9 After Viewing 13 The Story 15 Activity #1: Building Canada’s 5G Network 20 Activity #2: Imagine the Worst 23 Sources 25 CREDITS News in Review is produced by Visit www.curio.ca/newsinreview for an archive CBC NEWS and curio.ca of all previous News In Review seasons. As a companion resource, go to www.cbc.ca/news GUIDE for additional articles. Writer/editor: Sean Dolan Additional editing: Michaël Elbaz CBC authorizes reproduction of material VIDEO contained in this guide for educational Host: Michael Serapio purposes. Please identify source. Senior Producer: Jordanna Lake News In Review is distributed by: Packaging Producer: Marie-Hélène Savard curio.ca | CBC Media Solutions Associate Producer: Francine Laprotte Supervising Manager: Laraine Bone © 2019 Canadian Broadcasting Corporation HUAWEI ARREST: Canada Caught in a Political Tug of War Video duration – 18:02 The arrest of a top executive from Chinese company Huawei has placed Canada in the middle of a political tug of war. In December 2018, Canadian authorities detained Meng Wanzhou at the Vancouver Airport at the request of U.S. law officials. Meng is the daughter of the founder of Huawei, the largest technical communications company in the world. She remains in Canada while awaiting possible extradition to the U.S. on charges of fraud and violating international sanctions. Her arrest has heightened diplomatic tensions between China and Canada. And the case has far reaching implication raising security concerns about giving Huawei access to Canada's 5G network. -

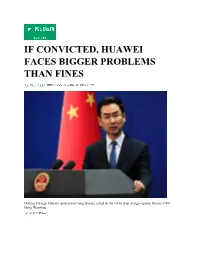

If Convicted, Huawei Faces Bigger Problems Than Fines

IF CONVICTED, HUAWEI FACES BIGGER PROBLEMS THAN FINES Chinese Foreign Ministry spokesman Geng Shuang called on the US to drop charges against Huawei CFO Meng Wanzhou. CHINESE TELECOM GIANT Huawei could face millions in fines if convicted of all charges in two indictments unsealed by the US Department of Justice Monday. But the money is likely the least of Huawei’s worries. The first indictment accuses Huawei and its executives, including CFO Meng Wanzhou, of crimes including bank fraud, wire fraud, money laundering, and obstruction of justice related to alleged violations of sanctions forbidding the sale of US-made equipment to Iran. The potential blow to the company is particularly severe because Meng is the daughter of Huawei founder Ren Zhengfei; she was arrested in Canada last month and is awaiting extradition to the US. The other indictment accuses the company of stealing intellectual property from T- Mobile, as part of an effort that included offering bonuses to employees who stole confidential information from competitors. According to the indictment, a company policy promised employees they wouldn’t be disciplined for such actions, and encouraged them to use an encrypted email address for particularly sensitive information. "The company denies that it or its subsidiary or affiliate have committed any of the asserted violations of U.S. law set forth in each of the indictments, is not aware of any wrongdoings by Ms. Meng, and believes the U.S. courts will ultimately reach the same conclusion," Huawei said in a statement published on Twitter. Huawei has already faced civil suits in the US over alleged intellectual property theft, but the new indictments raise the stakes for the company, and especially Meng. -

Case 1:18-Cr-00457-AMD Document 126 Filed 02/13/20 Page 1 of 56 Pageid #: 1349

Case 1:18-cr-00457-AMD Document 126 Filed 02/13/20 Page 1 of 56 PageID #: 1349 UNITED STATES DISTRICT COURT EASTERN DISTRICT OF NEW YORK - - - - - - - - - - - - - - - - - - - - - - - - - - - - X UNITED STATES OF AMERICA SUPERSEDING INDICTMENT - against - Cr. No. 18-457 (S-3) (AMD) HUAWEI TECHNOLOGIES CO., LTD., (T. 18, U.S.C., §§ 371, 981(a)(1)(C), HUAWEI DEVICE CO., LTD., 982(a)(1), 982(a)(2), 982(b)(1), 1343, HUAWEI DEVICE USA INC., 1344, 1349, 1512(k), 1832(a)(5), FUTUREWEI TECHNOLOGIES, INC., 1832(b), 1956(h), 1962(d), 1963(a), SKYCOM TECH CO., LTD., 1963(m), 2323(b)(1), 2323(b)(2), 2 and WANZHOU MENG, 3551 et seq.; T. 21, U.S.C., § 853(p); also known as “Cathy Meng” and T. 28, U.S.C., § 2461(c); T. 50, U.S.C., “Sabrina Meng,” §§ 1702, 1705(a) and 1705(c)) Defendants. - - - - - - - - - - - - - - - - - - - - - - - - - - - - X THE GRAND JURY CHARGES: INTRODUCTION At all times relevant to this Superseding Indictment, unless otherwise indicated: I. The Defendants 1. The defendant HUAWEI TECHNOLOGIES CO., LTD. (“HUAWEI”) was a global networking, telecommunications and services company headquartered in Shenzhen, Guangdong, in the People’s Republic of China (“PRC”). As of the date of the filing of this Superseding Indictment, HUAWEI was the largest telecommunications Case 1:18-cr-00457-AMD Document 126 Filed 02/13/20 Page 2 of 56 PageID #: 1350 2 equipment manufacturer in the world. HUAWEI was owned by its parent company, Huawei Investment & Holdings Co., Ltd. (“Huawei Holdings”), which was registered in Shenzhen, Guangdong, PRC, and predecessor entities of that company. -

Huawei in Europe: a Way to High-End Brand

International Journal of Business and Management Invention (IJBMI) ISSN (Online): 2319-8028, ISSN (Print):2319-801X www.ijbmi.org || Volume 10 Issue 6 Ser. II || June 2021 || PP 01-17 Huawei In Europe: A Way to High-End Brand Ivzhenko Yuliia Corresponding Author: Ivzhenko Yuliia Shanghai University, School of Management ABSTRACT: It was March 26, 2019, when Richard Yu, CEO of the Consumer Business Group (CBG) in Huawei Investment & Holding Co., Ltd. (Huawei), was giving a speech on the stage, representing the new flagship smartphone P30 in Paris. 42 The P30 Pro, Huawei's P30 premium version, with its four rear cameras, promised to “Rewrite the Rules of Photography” and aimed to take on Samsung's Galaxy S10 and Apple's iPhone X. The unveiling of Huawei's flagship in Paris coincided with the visit of Chinese President Xi Jinping to the French capital on March 23-24, where President Emmanuel Macron held a meeting along with German Chancellor Angela Merkel and European Commission President Jean-Claude Juncker to discuss political issues and trade. 43More recently, Huawei has been under much international scrutiny following US allegations that the company’s telecoms network equipment could be used for spying. Huawei has strongly rejected the allegations and, on March 6, 2019, sued the US government over the issue. Speaking about the legal action, Huawei Deputy Chairman Guo Ping stated that the US Congress did not present evidences for its ban on company’s products and equipment, hence it was unconstitutional. 44 Meanwhile, the race to roll out 5G technologies was going on. -

Proven Honour Capital Limited Huawei Investment

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement is for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for securities or an invitation to enter into any agreement to do any such things, nor is it calculated to invite any offer to acquire, purchase or subscribe for any securities. The material contained in this announcement is not for distribution or circulation, directly or indirectly, in or into the United States. This announcement is solely for the purpose of reference and does not constitute an offer to sell or the solicitation of an offer to buy, any securities in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The securities referred to herein have not been and will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and may not be offered or sold in the United States, except in certain transactions exempt from, or not subject to, the registration requirements of the Securities Act. No public offer of securities is to be made in the United States, Hong Kong or in any other jurisdiction where such an offering is restricted or prohibited. -

Caso Huawei - USA: Cosa Cambia Davvero Per Aziende E Utenti Dall’Entity List, Alla Richiesta Di Incostituzionalità Dell’NDAA Da Parte Di Huawei, Ad ARK OS

n.201 / 19 3 GIUGNO 2019 MAGAZINE edition Sky senza esclusive Whirlpool chiude Gli incredibili schermi Allestire un sistema Come cambia a Napoli. I sindacati OLED trasparenti di videosorveglianza lo scenario pay TV 09 insorgono 11 di LG in Italia 27 con un NAS 33 Caso Huawei - USA: cosa cambia davvero per aziende e utenti Dall’Entity List, alla richiesta di incostituzionalità dell’NDAA da parte di Huawei, ad ARK OS. Analisi e approfondimenti su un caso in continuo evolversi 02 DAZN, il primo anno in Italia 43 Intervista a Veronica Diquattro DAZN ha diffuso i numeri e le curiosità sulla prima stagione sportiva in Italia. La CEO Veronica Panasonic Lumix S1 Diquattro racconta strategia e ruolo della società Prima puntata: 17 Unboxing e hands-on Xbox Game Pass arriva su PC 1053 Microsoft alleata e rivale di Steam Con Game Pass su PC la posizione di Microsoft nel settore game PC sarà curiosa. Da una parte editore FCATerre - rare,Renault preziose con i propri giochi, dall’altra andrà di traverso a Propostama pericolose. ufficiale La 30 Steam con un’offerta parallela e alternativa disoluzione matrimonio è il riciclo IN PROVA IN QUESTO NUMERO 39 45 47 50 TV 8K Sony ZG9 iPad Mini 2019 OnePlus 7 Pro Oppo Reno Un “mondo di luce” Oltre le apparenze Velocità prima di tutto Pronto a stupire n.201 / 19 3 GIUGNO 2019 MAGAZINE edition MERCATO Vediamo come si è arrivati alla decisione di Google e perché Google ha dovuto prenderla Huawei - Usa, concessi 3 mesi Huawei e aziende USA: non solo Android di licenza. -

US Unveils Criminal Charges Against Huawei | Financial Times

2/8/2019 US unveils criminal charges against Huawei | Financial Times US-China trade dispute US unveils criminal charges against Huawei China slams case as ‘unfair’ as prosecutors also charge telecom group’s CFO Meng Wanzhou Huawei has been accused of stealing American technology and breaking US sanctions against Iran © Getty Kiran Stacey in Washington and Tom Mitchell in Beijing JANUARY 29, 2019 The US has accused China’s Huawei of stealing American technology and breaking US sanctions against Iran, in a criminal indictment that sharply escalates the two countries’ technological rivalry. The move will overshadow trade talks this week aimed at averting an all-out trade war between the world’s two largest economies. Matthew Whitaker, acting attorney-general, announced the action against the world’s biggest telecoms equipment maker on Monday as China’s trade negotiators, led by Vice-Premier Liu He, arrived in Washington for talks scheduled to open on Wednesday. Depending on the penalties sought by the justice department, the Trump administration’s salvo could disrupt the global operations of a Chinese corporate champion and land its chief financial officer, Meng Wanzhou, in prison. Ms Meng is the daughter of Huawei’s founder, Ren Zhengfei, and is currently in Vancouver as she fights a US extradition request in Canadian courts. Canada’s justice department late Monday said it had received a formal extradition request from the US, the Canadian Broadcasting Corporation reported. https://www.ft.com/content/ff000e70-233c-11e9-b329-c7e6ceb5ffdf 1/6 2/8/2019 US unveils criminal charges against Huawei | Financial Times Mr Whitaker told a press conference: “These are very serious actions by a company that appears to be using corporate espionage and sanctions violations not only to enhance their bottom line, but also to compete in the world economy. -

Corporate Governance Report

Huawei Turkey employees rafting on Melen River, Düzce, Turkey 101 Shareholders Corporate 102 The Shareholders' Meeting and the Representatives' Commission Governance 102 Board of Directors and Committees 107 Supervisory Board Report 107 Rotating CEOs 108 Members of the Board of Directors, the Supervisory Board, and the BOD Committees 114 Independent Auditor 114 Business Structure 115 Improving the Management System 117 Improving the Internal Control System By staying customer-centric and inspiring dedication, we have sustained long-term growth by continuously improving our corporate governance structure, organizations, processes, and appraisal systems. Shareholders’ Meeting Board of Directors Independent Auditor Supervisory Board Executive Committee Human Resources Strategy & Finance Committee Development Audit Committee Committee Committee CEO/Rotating CEOs Group Functions Corporate Strategy Cyber Security & Human Resources Finance Quality, BP & IT Development Marketing User Privacy Protection Joint Committee Engineering Ethics & PR & GR Legal Affairs Internal Audit of Regions Inspection Compliance 2012 Laboratories Chief Supply Chain Officer (Supply Chain, Purchase, Products & Carrier Enterprise Consumer Manufacturing) Solutions BG BG BG Huawei University Huawei Internal Service Regional Organizations (Regions and Representative Offices) Shareholders Huawei Investment & Holding Co., Ltd. (the "Company" or "Huawei") is a private company wholly owned by its employees. Huawei's shareholders are the Union of Huawei Investment & Holding Co., Ltd. (the "Union") and Mr. Ren Zhengfei. Through the Union, the company implements an Employee Shareholding Scheme (the "Scheme"), which involved 79,563 employees as of December 31, 2015. The Scheme effectively aligns employee contributions with the company's long-term development, fostering Huawei's continued success. Mr. Ren Zhengfei is the individual shareholder of the Company and also participates in the Scheme.