Southern Africa June 2018 Highlights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2021 Indices Des Prix De Détail Relatif Aux Dépenses De La Vie Courante Des Fonctionnaires De L'onu New York = 100, Date D'indice = Juin 2021

Price indices Indices des prix Retail price indices relating to living expenditures of United Nations Officials New York City = 100, Index date = June 2021 Indices des prix de détail relatif aux dépenses de la vie courante des fonctionnaires de l'ONU New York = 100, Date d'indice = Juin 2021 National currency per US $ Index - Indice Monnaie nationale du $ E.U. Excluding Country or Area Duty Station housing 2 Pays ou Zone Villes-postes Per US$ 1 Currency Total Non compris 1 Cours du $E-U Monnaie l'habitation 2 Afghanistan Kabul 78.070 Afghani 86 93 Albania - Albanie Tirana 98.480 Lek 78 82 Algeria - Algérie Algiers 132.977 Algerian dinar 80 85 Angola Luanda 643.121 Kwanza 84 93 Argentina - Argentine Buenos Aires 94.517 Argentine peso 81 84 Armenia - Arménie Yerevan 518.300 Dram 75 80 Australia - Australie Sydney 1.291 Australian dollar 82 88 Austria - Autriche Vienna 0.820 Euro 91 100 Azerbaijan - Azerbaïdjan Baku 1.695 Azerbaijan manat 81 87 Bahamas Nassau 1.000 Bahamian dollar 100 96 Bahrain - Bahreïn Manama 0.377 Bahraini dinar 83 86 Bangladesh Dhaka 84.735 Taka 81 89 Barbados - Barbade Bridgetown 2.000 Barbados dollar 90 95 Belarus - Bélarus Minsk 2.524 New Belarusian ruble 85 91 Belgium - Belgique Brussels 0.820 Euro 84 92 Belize Belmopan 2.000 Belize dollar 76 80 Benin - Bénin Cotonou 537.714 CFA franc 83 92 Bhutan - Bhoutan Thimpu 72.580 Ngultrum 77 83 Bolivia (Plurinational State of) - Bolivie (État plurinational de) La Paz 6.848 Boliviano 73 80 Bosnia and Herzegovina - Bosnie-Herzégovine Sarajevo 1.603 Convertible mark 73 79 Botswana Gaborone 10.582 Pula 75 83 Brazil - Brésil Brasilia 5.295 Real 71 82 British Virgin Islands - Îles Vierges britanniques Road Town 1.000 US dollar 87 93 Bulgaria - Bulgarie Sofia 1.603 Lev 70 85 Burkina Faso Ouagadougou 537.714 CFA franc 80 87 Burundi Bujumbura 1,953.863 Burundi franc 82 90 Cabo Verde - Cap-Vert Praia 90.389 CV escudo 79 87 Cambodia - Cambodge Phnom Penh 4,098.000 Riel 82 88 Cameroon - Cameroun Yaounde 537.714 CFA franc 83 91 Canada Montreal 1.208 Canadian dollar 91 96 Central African Rep. -

Crown Agents Bank's Currency Capabilities

Crown Agents Bank’s Currency Capabilities September 2020 Country Currency Code Foreign Exchange RTGS ACH Mobile Payments E/M/F Majors Australia Australian Dollar AUD ✓ ✓ - - M Canada Canadian Dollar CAD ✓ ✓ - - M Denmark Danish Krone DKK ✓ ✓ - - M Europe European Euro EUR ✓ ✓ - - M Japan Japanese Yen JPY ✓ ✓ - - M New Zealand New Zealand Dollar NZD ✓ ✓ - - M Norway Norwegian Krone NOK ✓ ✓ - - M Singapore Singapore Dollar SGD ✓ ✓ - - E Sweden Swedish Krona SEK ✓ ✓ - - M Switzerland Swiss Franc CHF ✓ ✓ - - M United Kingdom British Pound GBP ✓ ✓ - - M United States United States Dollar USD ✓ ✓ - - M Africa Angola Angolan Kwanza AOA ✓* - - - F Benin West African Franc XOF ✓ ✓ ✓ - F Botswana Botswana Pula BWP ✓ ✓ ✓ - F Burkina Faso West African Franc XOF ✓ ✓ ✓ - F Cameroon Central African Franc XAF ✓ ✓ ✓ - F C.A.R. Central African Franc XAF ✓ ✓ ✓ - F Chad Central African Franc XAF ✓ ✓ ✓ - F Cote D’Ivoire West African Franc XOF ✓ ✓ ✓ ✓ F DR Congo Congolese Franc CDF ✓ - - ✓ F Congo (Republic) Central African Franc XAF ✓ ✓ ✓ - F Egypt Egyptian Pound EGP ✓ ✓ - - F Equatorial Guinea Central African Franc XAF ✓ ✓ ✓ - F Eswatini Swazi Lilangeni SZL ✓ ✓ - - F Ethiopia Ethiopian Birr ETB ✓ ✓ N/A - F 1 Country Currency Code Foreign Exchange RTGS ACH Mobile Payments E/M/F Africa Gabon Central African Franc XAF ✓ ✓ ✓ - F Gambia Gambian Dalasi GMD ✓ - - - F Ghana Ghanaian Cedi GHS ✓ ✓ - ✓ F Guinea Guinean Franc GNF ✓ - ✓ - F Guinea-Bissau West African Franc XOF ✓ ✓ - - F Kenya Kenyan Shilling KES ✓ ✓ ✓ ✓ F Lesotho Lesotho Loti LSL ✓ ✓ - - E Liberia Liberian -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

WM/Refinitiv Closing Spot Rates

The WM/Refinitiv Closing Spot Rates The WM/Refinitiv Closing Exchange Rates are available on Eikon via monitor pages or RICs. To access the index page, type WMRSPOT01 and <Return> For access to the RICs, please use the following generic codes :- USDxxxFIXz=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR, GBP or CHF xxx can be any of the following currencies :- Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy -

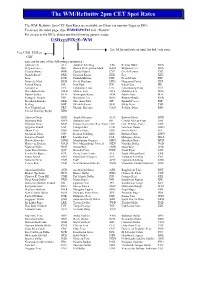

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

World Bank Document

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized CONTENTS Acronyms iii Foreword iv Acknowledgements v Part One: Recent Economic Developments 1 A The Real Sector 2 B External Sector 6 C Monetary Policy 12 D Fiscal Sector 14 Part Two: Economic Outlook 17 Part Three: Managing Fuel Pricing in Madagascar 19 A Introduction 20 B Why the government has engaged in the reform of fuel prices 20 C Key considerations in pricing fuel 24 D Policy options available for fuel pricing 25 E Conclusion 30 References 31 FIGURES Figure 1 The services sector continues to be a strong driver of growth 2 Figure 2 Madagascar’s per capita growth rate compares favorably with other regions but still lags other high performing economies in Africa 2 Figure 3 International visitor numbers in 2018 have fallen 3 Figure 4 Prices of vanilla continue to trend upward 4 Figure 5 Since 2016, prices of nickel and cobalt have started to rebound (latest official data available) 4 Figure 6 Paddy production levels in 2018 are estimated to be on par with earlier years 4 Figure 7 Export receipts continue to perform well, particularly for vanilla, nickel and cobalt 6 Figure 8 Import receipts have increased largely due to a higher price of petroleum 6 Figure 9 The current account balance realized a moderate surplus in 2018 7 Figure 10 JIRAMA’s quasi-fiscal deficit is on an upward trend 8 i Figure 11 The operating costs of power generation in Madagascar are amongst the highest in Africa 9 Figure 12 Less than half of produced electricity is actually paid for 10 Figure 13 If JIRAMA’s reform momentum continues, financial equilibrium should be reached by 2022 11 Figure 14 Inflation in 2018 fell compared with the previous year 12 Figure 15 Inflation still remains relatively high in Madagascar compared with other countries 12 Figure 16 The ariary has been on a depreciating trend in nominal terms 13 Figure 17 The real effective exchange rate has been relatively constant in 2018 (2017 = 100) 13 Figure 18 Lending to the private sector has picked up.. -

Retail Price Indices Relating to Living Expenditures of United Nations

Price indices Indices des prix Retail price indices relating to living expenditures of United Nations Officials New York City = 100, Index date = August 2019 Indices des prix de détail relatif aux dépenses de la vie courante des fonctionnaires de l'ONU New York = 100, Date d'indice = Août 2019 National currency per US $ Index - Indice Monnaie nationale du $ E.U. Excluding Country or Area Duty Station housing 2 Pays ou Zone Villes-postes Per US$ 1 Currency Total Non compris 1 Monnaie 2 Cours du $E-U l'habitation Afghanistan Kabul 79.450 Afghani 87 94 Albania - Albanie Tirana 107.800 Lek 74 81 Algeria - Algérie Algiers 119.675 Algerian dinar 84 89 Angola Luanda 345.910 Kwanza 93 97 Argentina - Argentine Buenos Aires 56.500 Argentine peso 81 82 Armenia - Arménie Yerevan 476.000 Dram 77 81 Australia - Australie Sydney 1.471 Australian dollar 77 87 Austria - Autriche Vienna 0.894 Euro 84 93 Azerbaijan - Azerbaïdjan Baku 1.698 Azerbaijan manat 80 87 Bahamas Nassau 1.000 Bahamian dollar 101 96 Bahrain - Bahreïn Manama 0.377 Bahraini dinar 84 88 Bangladesh Dhaka 84.525 Taka 85 91 Barbados - Barbade Bridgetown 2.000 Barbados dollar 93 101 Belarus - Bélarus Minsk 2.031 New Belarusian ruble 86 94 Belgium - Belgique Brussels 0.894 Euro 81 89 Belize Belmopan 2.000 Belize dollar 76 81 Benin - Bénin Cotonou 586.252 CFA franc 76 86 Bhutan - Bhoutan Thimpu 68.860 Ngultrum 80 88 Bolivia (Plurinational State of) - Bolivie (État plurinational de) La Paz 6.910 Boliviano 73 81 Bosnia and Herzegovina - Bosnie-Herzégovine Sarajevo 1.748 Convertible mark 71 78 Botswana Gaborone 10.695 Pula 74 81 Brazil - Brésil Brasilia 3.793 Real 84 87 British Virgin Islands - Îles Vierges britanniques Road Town 1.000 US dollar 87 93 Bulgaria - Bulgarie Sofia 1.748 Lev 68 83 Burkina Faso Ouagadougou 586.252 CFA franc 80 87 Burundi Bujumbura 1,834.883 Burundi franc 80 87 Cabo Verde - Cap-Vert Praia 98.548 CV escudo 77 85 Cambodia - Cambodge Phnom Penh 4,033.000 Riel 83 89 Cameroon - Cameroun Yaounde 586.252 CFA franc 80 89 Canada Montreal 1.324 Canadian dollar 85 91 Central African Rep. -

ACE CATAIR Appendix B

CBP and Trade Automated Interface Requirements Appendix B – Valid Codes July 28, 2021 DRAFT 1 Pub # 0875-0419 The reader should be advised that this technical document is considered final. However, the document retains the DRAFT designation in the footer until such time that an official OPA (Office of Public Affairs) publication number has been assigned to the new “ACE ABI CATAIR” publication. For your information, subsequent revisions to this document will be controlled through the official CBP document amendment process. DRAFT 2 Table of Contents General Appendix Information ....................................................................................................... 6 Country and Currency Codes ...................................................................................................... 7 EU Country Codes .................................................................................................................... 18 Location Identifiers ................................................................................................................... 19 Units of Measure ....................................................................................................................... 23 Entry Type Codes ...................................................................................................................... 27 Mode of Transportation Codes .................................................................................................. 28 Equipment Description Codes .................................................................................................. -

Retail Price Indices Relating to Living Expenditures of United Nations

Price indices Indices des prix Retail price indices relating to living expenditures of United Nations Officials New York City = 100, Index date = June 2017 Indices des prix de détail relatif aux dépenses de la vie courante des fonctionnaires de l'ONU New York = 100, Date d'indice = Juin 2017 National currency per US $ Index - Indice Monnaie nationale du $ E.U. Excluding Country or Area Duty Station housing 2 Pays ou Zone Villes-postes Per US$ 1 Currency Total Non compris 1 Monnaie 2 Cours du $E-U l'habitation Afghanistan Kabul 67.570 Afghani 88 94 Albania - Albanie Tirana 118.700 Lek 75 82 Algeria - Algérie Algiers 108.549 Algerian dinar 86 90 Angola Luanda 165.090 Kwanza 131 120 Argentina - Argentine Buenos Aires 16.040 Argentine peso 88 95 Armenia - Arménie Yerevan 482.000 Dram 78 80 Australia - Australie Sydney 1.341 Australian dollar 81 91 Austria - Autriche Vienna 0.893 Euro 86 95 Azerbaijan - Azerbaïdjan Baku 1.690 Azerbaijan manat 75 80 Bahamas Nassau 1.000 Bahamanian dollar 102 96 Bahrain - Bahreïn Manama 0.377 Bahraini dinar 85 92 Bangladesh Dhaka 80.770 Taka 84 90 Barbados - Barbade Bridgetown 2.000 Barbadian dollar 95 106 Belarus - Bélarus Minsk 1.865 New Belarusian ruble 83 87 Belgium - Belgique Brussels 0.893 Euro 87 95 Belize Belmopan 1.999 Belize dollar 80 85 Benin - Bénin Cotonou 586.095 CFA franc 76 88 Bhutan - Bhoutan Thimpu 64.670 Ngultrum 81 88 Bolivia (Plurinational State of) - Bolivie (État plurinational de) La Paz 6.910 Boliviano 81 88 Bosnia and Herzegovina - Bosnie-Herzégovine Sarajevo 1.748 Convertible mark 73 79 Botswana Gaborone 10.309 Pula 73 81 Brazil - Brésil Brasilia 3.269 Real 87 90 Bulgaria - Bulgarie Sofia 1.748 Lev 74 82 Burkina Faso Ouagadougou 586.095 CFA franc 82 90 Burundi Bujumbura 1,705.645 Burundi franc 90 99 Cabo Verde - Cap-Vert Praia 98.521 CV escudo 80 88 Cambodia - Cambodge Phnom Penh 4,040.000 Riel 79 86 Cameroon - Cameroun Yaounde 586.095 CFA franc 81 88 Canada Montreal 1.348 Canadian dollar 82 88 Central African Rep. -

7 Exchange Rates Taux De Change Tipos De Cambio (National Currency Per US Dollar) (Valeur Du Dollar E.U. En Monnaie Nationale) (

7 Exchange rates Taux de change Tipos de cambio (National currency per US Dollar) (Valeur du dollar E.U. en monnaie nationale) (Valor del dólar EE.UU. en moneda nacionale) XXA IB XXC 2010I 2011I 2012I 2013I XXA IB XXC 2010I 2011I 2012I 2013I Albania ALL Lek 103.79 100.83 108.15 105.63 Latvia EUR EURO 0.75 0.72 0.78 0.75 Antigua Barb XCD East Caribbean Dollar - 2.70 2.70 2.70 Madagascar MGA Malagasy Ariary 2087.63 2022.86 - 2206.72 Aruba AWG Aruban Guilder - 1.79 - - Malawi MWK Kwacha 150.48 - - - Australia AUD Australian Dollar 1.09 0.97 0.97 1.03 Malaysia MYR Malaysian Ringgit 3.22 3.06 - - Bahamas BSD Bahamian Dollar - - - 1.00 Maldives MVR Rufiyaa 12.80 14.51 15.36 15.37 Bahrain BHD Bahraini Dinar 0.38 0.38 - - Mali XOF CFA Franc - - 510.24 - Barbados BBD Barbados Dollar 2.00 2.00 2.00 - Mauritania MRO Ouguiya 275.56 281.02 - 300.66 Belize BZD Belize Dollar - - - 2.00 Mauritius MUR Mauritius Rupee 30.76 28.69 - 30.70 Benin XOF CFA Franc 494.36 - 510.24 493.89 Montenegro EUR EURO 0.75 0.72 0.78 0.75 Bhutan BTN Ngultrum 45.71 - 53.35 - Montserrat XCD East Caribbean Dollar 2.70 - - 2.70 Bosnia Herzg EUR EURO 0.75 - - - Morocco MAD Moroccan Dirham 8.41 8.08 8.63 - Botswana BWP Pula 6.79 6.82 - 8.39 Nepal NPR Nepalese Rupee 73.24 - 85.06 92.60 Brunei Darsm BND Brunei Dollar - - 1.25 1.25 NewCaledonia XPF CFP Franc 89.93 85.76 92.82 89.85 Burkina Faso XOF CFA Franc 494.36 471.43 510.24 493.89 New Zealand NZD New Zealand Dollar 1.39 1.26 1.23 1.22 Burundi BIF Burundi Franc 1230.75 - 1440.97 - Niger XOF CFA Franc 494.36 471.43 510.24 493.89 -

International Poverty Line

Poverty & Equity Brief Sub-Saharan Africa Madagascar April 2019 Madagascar made little progress in improving the welfare of the poor during the past decade. The period has been marked by political, economic, and climatic shocks, which resulted in slow economic growth and limited progress with poverty reduction. Poverty increased between 2001 and 2005 and then started declining slightly, but remained exceedingly high. The national poverty rate was estimated at 70.7 percent in 2012, nearly the same rate as in 2001. When using the international poverty line of $1.90 per capita per day (in 2011 PPP), poverty is estimated at 77.6 percent in 2012 which places Madagascar among the poorest countries in the world. Despite stagnating poverty, inequality has declined, with the Gini index dropping from 46.9 in 2001 to 42.6 in 2012. This trend was accompanied by consumption gains among households in the poorest groups and a reduction in poverty depth by around 4 percentage points (from 36 percent in 2001 to 32 percent in 2012). The persistence of poverty is the result of the poor performance of agriculture and high unemployment in urban areas. The agriculture sector is highly vulnerable to frequent climatic shocks, price fluctuations, and market integration. In addition, national policies to insulate the economy from rising world rice prices, coupled with deteriorating transport conditions and costs, negatively affected the returns to agriculture. Many poor households shifted into low-productivity off-farm secondary activities as coping mechanisms. While this diversification increased earnings, it has not been enough to lift households out of poverty. -

20 000,00 $ Can Sample Table of the Maximum Contribution In

SAMPLE TABLE OF THE MAXIMUM CONTRIBUTION IN LOCAL CURRENCY Date: July 8, 2016 20 000,00 $ CAN COUNTRY CURRENCY CAN$1 = AMOUNT IN LOCAL CURRENCY South Africa ZAR - South African Rand 11,8511 237 022 ZAR Bangladesh BDT - Bangladeshi Taka 61,1799 1 223 598 BDT Benin XOF - West African CFA Franc 452,5570 9 051 140 XOF Bolivia BOB - Bolivian Boliviano 5,3629 107 257 BOB Brazil BRL - Brazilian Real 2,6810 53 620 BRL Burkina Faso XOF - West African CFA Franc 452,5570 9 051 140 XOF Burundi BIF - Burundian Franc 1 291,2600 25 825 200 BIF Cameroon XAF - Central African CFA Franc 452,5570 9 051 140 XAF Chile CLP - Chilean Peso 529,3806 10 587 612 CLP Colombia COP - Columbian Peso 2 314,8148 46 296 296 COP Ivory Coast XOF - West African CFA Franc 452,5570 9 051 140 XOF Cuba CUC - Cuban Convertible Peso 0,7789 15 577 CUC El Salvador SVC - Salvadoran Colon 0,7668 15 336 USD Ecuador USD - United States Dollar 0,7668 15 336 USD United States USD - United States Dollar 0,7668 15 336 USD Europe EUR - Euro 0,6873 13 746 EUR Ghana GHS - Ghanaian Cedi 3,0093 60 186 GHS Guatemala GTQ - Guatemalan Quetzal 6,0024 120 048 GTQ Guinea GNF - Guinean Franc 5 726,8900 114 537 800 GNF Haiti HTG - Haitian Gourde 48,7618 975 236 HTG Honduras HNL - Honduran Lempira 17,4216 348 432 HNL India INR - Indian Rupee 51,7063 1 034 126 INR Indonesia IDR - Indonesian Rupiah 10 204,0816 204 081 632 IDR Kenya KES - Kenyan Shilling 78,8467 1 576 934 KES Lesotho LSL - Lesotho Loti 11,8168 236 336 LSL Madagascar MGA - Malagasy Ariary 2 539,0700 50 781 400 MGA Malawi MWK - Malawian Kwacha