Colour Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

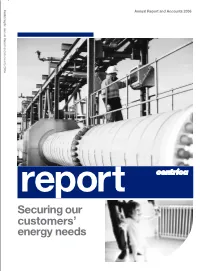

Annual Report and Accounts 2006 Annual Report and Accounts 2006

Centrica plc Annual Report and Accounts 2006 Annual Report and Accounts 2006 report Securing our customers’ energy needs Our vision is to become a leading integrated energy company in selected markets in order to maximise value to shareholders. In 2006 we focused on securing energy to meet our customers’ future needs. Our strategy Our strategy is to create a distinctive business model that delivers sustained profitability through the commodity cycle. We will achieve this by focusing on the following clear priorities: Transform British Gas Sharpen up the organisation and reduce costs Reduce risk by adding new sources of gas and power Build on our multiple growth platforms Our main activities Our upstream business Our downstream business We source energy internationally We supply energy to homes We find and produce gas predominantly in the UK We are Britain’s largest gas and electricity retailer, and have acquired licence blocks in Norway and supplying 49% of the residential gas market and 22% north and west Africa. We trade energy in the UK, of residential electricity. We are a growing North America and Europe and secure contracts force in North America, serving customers in five to bring gas to the UK. Canadian provinces and 15 US states. We generate energy We supply energy to businesses We generate electricity through our gas-fired power In Britain, we are a major supplier of gas and stations in the UK and US and through a growing electricity to the commercial sector. We also have portfolio of wind assets and purchasing agreements. customers in Belgium, the Netherlands and Spain. -

01 STA Cover 2007

15-28 STA Listings 2007 21/2/07 2:37 PM Page 15 THE SOURCE TESTING ASSOCIATION THE STA MEMBERSHIP 3M UK Aerosol Industrial Station Road, Coleshill ALcontrol On-Site Services Ian Clarkson Research Group Birmingham B46 1JY Trevor Worrall 3M Centre, Cain Road, Bracknell Cristina Gutiérrez-Cañas T: 0800 917 1313 Templeborough House, Mill Close Berkshire RG12 8HT Maria Diaz de Haro 68 F: 01675 467022 Rotherham, South Yorkshire T: 01344 857801 Bajo Pab 3-4-5, Portugalete [email protected] S60 1BZ [email protected] Bizakaia 48920, Spain www.uk.airliquide.com T: 01709 841028 www.mmm.com T: (+34) 944 723597 F: 01709 841079 F: (+34) 944 723604 Air Monitors [email protected] A-Plus Consulting [email protected] James Mills www.alcontrol.co.uk Graham Clarke www.aerosolirg.com Unit 2, The Hawthorns 35 Holmesdale Road, Dronfield Pillows Green Road, Staunton Derbyshire S18 2FA AES Gloucestershire GL19 3NY T: 01246 410256 Mark Elliott T: 01452 849111 [email protected] Northumberland Dock Road F: 01452 849112 Wallsend, Tyne & Wear NE28 0QD [email protected] T: 0191 2968500 www.airmonitors.co.uk Anchem Laboratories F: 0191 2968560 Gethyn Jones [email protected] Air Products Unit 5a, Darcy Business Park www.aes-labs.co.uk Dr Gary Yates Darcy Way, Llandarcy, Neath 2 Millennium Gate, Westmere Drive SA10 6EJ ABB AES Kilroot Power Crewe, Cheshire CW1 6AP T: 01792 323223 John Kelly Stephen Fleming T: 01270 614227 F: 01792 323236 Hortonwood 37, Telford, Shropshire Larne Road, Carrickfergus F: 01932 258622 [email protected] -

Agecroft in Steam

( ?I ~- - - ~"~ _., -- ........... / -- . , ·--....., __ t) \ ,-- The 1960's saw a dramatic change m the use of The 'A' station system was abandoned early m steam locomotion in the North West of 1947 as construction of 'B' station cooling to Cl!Jton Junc1:c'n ) England. Within the short space of 8 years the towers severed the line. Between then and its QI✓ . familiar sight of a steam-hauled train closure the 'A' station received coal by road. {not all 1he rm,ways shown exi~ad al the some time vanished completely from British Rail. For a A Stallon .,:· :·, ,: ' _::' .·. ·-~ ·.. while steam continued to be used at some ·'..,·.'. _. 1, · ,_ c · ·n... c····. ~:·y···,--·· Reception Sidings industrial sites in Lancashire but now only II AG hopper Agecroft Power Station, near Manchester, .if •i•>,c': fp , ' . ,. Ill ·• continues the tradition. Three power stations (A, B and C ) have been A completely ne w coal handling system using developed on the Agecroft site smce 1925 and steam locomotives, was built on a separate each has used a rrnl system in its coal site· to se rve···•· both 'B ' and 'C' stations. A senes of handling. lines, approximately I mile lung, was coalslockmg construc ted running from the original gmundwilh ,:···. ~ ~ -c·,.' .-:B.ft. .,. ....:;: y ·:·:· conveyor to Agecroft Junc tion. The line passed crone lrack (standard gmrgel -.. ~~:: .. ·~&--... 2 loco sheds and fanned into wagon sidings ,,,. .-n:v ...' ... which converged lo pass through the tippler. .. .. A new conveyor was built to take the coal over . .. ... the British Rail line and the canal to the power The original 'A' statio,n used a 2' 6" gauge station. -

Digest of United Kingdom Energy Statistics 2017

DIGEST OF UNITED KINGDOM ENERGY STATISTICS 2017 July 2017 This document is available in large print, audio and braille on request. Please email [email protected] with the version you require. Digest of United Kingdom Energy Statistics Enquiries about statistics in this publication should be made to the contact named at the end of the relevant chapter. Brief extracts from this publication may be reproduced provided that the source is fully acknowledged. General enquiries about the publication, and proposals for reproduction of larger extracts, should be addressed to BEIS, at the address given in paragraph XXVIII of the Introduction. The Department for Business, Energy and Industrial Strategy (BEIS) reserves the right to revise or discontinue the text or any table contained in this Digest without prior notice This is a National Statistics publication The United Kingdom Statistics Authority has designated these statistics as National Statistics, in accordance with the Statistics and Registration Service Act 2007 and signifying compliance with the UK Statistics Authority: Code of Practice for Official Statistics. Designation can be broadly interpreted to mean that the statistics: ñ meet identified user needs ONCEñ are well explained and STATISTICSreadily accessible HAVE ñ are produced according to sound methods, and BEENñ are managed impartially DESIGNATEDand objectively in the public interest AS Once statistics have been designated as National Statistics it is a statutory NATIONALrequirement that the Code of Practice S TATISTICSshall continue to be observed IT IS © A Crown copyright 2017 STATUTORY You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. -

News Release

` 11 January 2010 News Release Siemens’ Newcastle operation celebrates double success with record orders totalling £110 million Siemens Energy is celebrating double success after securing record orders at its Energy Service Fossil facility in Newcastle. The first for the Ministry of Electricity in Iraq, involves the supply of steam turbine spares for the Al Mussaib Power Station in Iraq. The contract was secured after three years of negotiation in a very challenging market. The steam turbine replacement component work will be completed at the Siemens Shields Road facility in Newcastle. Carl Ennis, Managing Director of Siemens Energy Service Fossil comments: “This contract will pave the way for future business to assist the Ministry of Electricity in its efforts to improve the reliability and maintenance of the electricity supply for the people of Iraq.” The second order for parts, shop repairs and field service for the Siemens designed gas turbines, generators and steam turbines at Seabank Power Station in the Bristol area has given the order book a massive boost. All field service and on shore project management activities will be coordinated from Siemens in the UK. Owned and operated by Seabank Power Limited, the combined cycle gas turbine power station has two modules with an overall capacity of 1,155MW. Siemens will supply parts, repair and service the plant’s equipment on both modules with the contract expected to run until 2018. Carl Ennis adds that: “Siemens Energy Service Fossil has made significant strides in the past two years. -

DRAFT FINAL REPORT Cambridge Economic Policy Associates

SCOPING TOWARDS POTENTIAL HARMONISATION OF ELECTRICITY TRANSMISSION TARIFF STRUCTURES AGENCY FOR COOPERATION OF ENERGY REGULATORS (ACER) JUNE 2015 DRAFT FINAL REPORT Prepared by: Cambridge Economic Policy Associates Ltd CONTENTS 1. Introduction .............................................................................................................. 1 1.1. The European electricity market ............................................................................... 1 1.2. Tariff structure harmonisation .................................................................................. 2 1.3. Scope of study ............................................................................................................ 2 1.4. Study methodology .................................................................................................... 3 1.5. Report structure ......................................................................................................... 4 2. Context of study ....................................................................................................... 6 2.1. The Internal Electricity Market .................................................................................. 6 2.2. Objectives for transmission tariffs ........................................................................... 10 3. Transmission tariff structures in Europe today ......................................................... 12 3.1. What are transmission tariffs? ............................................................................... -

Annual Review and Summary Financial Statements 2010 Shareholder Information Continued

Centrica plc Registered office: Millstream, Maidenhead Road, Windsor, Berkshire SL4 5GD Company registered in England and Wales No. 3033654 www.centrica.com Annual Review and Summary Financial Statements 2010 Shareholder Information continued SHAREHOLDER SERVICES Centrica shareholder helpline To register for this service, please call the shareholder helpline on 0871 384 2985* to request Centrica’s shareholder register is maintained by Equiniti, a direct dividend payment form or download it from which is responsible for making dividend payments and www.centrica.com/shareholders. 01 10 updating the register. OVERVIEW SUMMARY OF OUR BUSINESS The Centrica FlexiShare service PERFORMANCE If you have any query relating to your Centrica shareholding, 01 Chairman’s Statement please contact our Registrar, Equiniti: FlexiShare is a ‘corporate nominee’, sponsored by Centrica and administered by Equiniti Financial Services Limited. It is 02 Our Performance 10 Operating Review Telephone: 0871 384 2985* a convenient way to manage your Centrica shares without 04 Chief Executive’s Review 22 Corporate Responsibility Review Textphone: 0871 384 2255* the need for a share certificate. Your share account details Write to: Equiniti, Aspect House, Spencer Road, Lancing, will be held on a separate register and you will receive an West Sussex BN99 6DA, United Kingdom annual confirmation statement. Email: [email protected] By transferring your shares into FlexiShare you will benefit from: A range of frequently asked shareholder questions is also available at www.centrica.com/shareholders. • low-cost share-dealing facilities provided by a panel of independent share dealing providers; Direct dividend payments • quicker settlement periods; Make your life easier by having your dividends paid directly into your designated bank or building society account on • no share certificates to lose; and the dividend payment date. -

2008 Corporate Responsibility Report Centrica Plc Corporate Responsibility Report 2008

2008 Corporate responsibility report Centrica plc Corporate responsibility report 2008 www.centrica.com/cr08 Contents 3 Chief Executive’s introduction 4 Assurance and scope 5 Excerpt from Corporate Citizenship’s Assurance Statement 6 2008 Highlights 7 Business overview 8 Our approach 14 CR Committee and Governance 17 Business principles 22 Key Performance Indicators 25 Key impact areas 26 Climate change and the environment 44 Customer service 56 Securing future energy supplies 64 Health and safety 72 Employees 83 Supply chain 87 Local impact 92 Our stakeholders 94 Customers 97 Investors 99 Employees 101 Suppliers and business partners 103 Governments and regulators 105 Communities 107 NGOs and consumer organisations 109 Media 110 Trade unions 111 Appendix – Memberships 2 Centrica plc Corporate responsibility report 2008 www.centrica.com/cr08 Chief Executive’s introduction Introduction from Sam Laidlaw 2008 was my first full year as a member of the Corporate Responsibility Committee. Throughout the year, the Committee challenged our current performance and debated areas of future activity across a range of critical business issues. Through this continual process of improvement, I have confidence that we are making good progress in developing the necessary structures and processes, allied to a management commitment that will build a sustainable and environmentally aware business for the future. In this report, you can read about our initiatives and performance over the year, as well as our forward- looking plans for 2009 and beyond. As our CR programmes mature, there is an increasing amount of available information to present to our internal and external audiences. As in previous years, we have chosen to use the online environment to report. -

Proposed Response to the North West Coast Connections Route Corridor Consultation – Appendix 1

PROPOSED RESPONSE TO THE NORTH WEST COAST CONNECTIONS ROUTE CORRIDOR CONSULTATION – APPENDIX 1 PURPOSE OF APPENDIX The purpose of this Appendix is to set out the proposed response of SLDC to the National Grid North West Coast Connections Route Corridor Consultation 1 General comments 1.1 SLDC broadly supports the preferred option – Onshore South with Tunnel. 1.2 The preferred option includes a tunnel under Morecambe Bay from close to Heysham to the Rampside area and then broadly follows the existing 132kV Electricity North West power line northwards through the Furness peninsula to Broughton in Furness and then up the West Coast of Cumbria, much of which will be removed and replaced by a smaller number of larger 400kV pylons. 1.3 The preferred option, in the main, avoids the significant impacts to South Lakeland communities that would be incurred if other alternative options, such as Onshore South, were implemented. 1.4 However, SLDC’s support for the preferred option is subject to consideration of the remaining concerns and needs for mitigation detailed below. 2 Section H1 (South eastern Furness) 2.1 The preferred tunnel route is proposed to surface slightly inland in the area between Roosebeck and Rampside. SLDC considers that locating the convertor stations at the points where the cable surfaces as close to the existing energy infrastructure at Roosecote Power Station as possible (as indicated by the larger blue hatched polygon in the consultation material) would indeed be preferable. It would have the least impact on social, environmental and economic factors, including landscape, impacts on local communities and tourism. -

Planning Supporting Statement

Branston Locks Employment Land Statement November 2012 Employment Land Statement Nurton Developments (Quintus) Limited Branston Locks, Burton upon Trent November 2012 Branston Locks – Employment Land Statement Contents 1 Introduction ............................................................................................................................................................ 2 2 Communications and Site Characteristics .......................................................................................................... 3 3 Relevant Planning Policy and Supporting Evidence Base................................................................................. 4 4 Market Overview for Burton ................................................................................................................................ 10 5 Assessment of Demand ...................................................................................................................................... 16 6 Conclusions ......................................................................................................................................................... 18 Appendix 1 – Schedule of Occupiers and Map of Centrum ........................................................................................ 19 Appendix 2 – Schedule of Available Industrial Floor Space in Burton Upon Trent .................................................. 20 Appendix 3 – Schedule of Available Office Floor Space in Burton Upon Trent ....................................................... -

G59 Generator Protection Settings - Progress on Changes to New Values (Information Received As at End of 2010 - Date of Latest Updates Shown for Each Network.)

G59 Generator Protection Settings - Progress on Changes to new Values (Information received as at End of 2010 - Date of latest updates shown for each network.) DNO [Western Power Distribution - South West Area] total responses as at 05/01/11 User Data Entry Under Frequency Over Frequency Generator Generator Generator Changes Generator Stage 1 Stage 2 Stage 1 Stage 2 Agreed to capacity capacity capacity changes Site name Genset implemented capacity unable Frequency Frequency Frequency Frequency Comments changes (Y/N) installed agreed to implemented (Y/N) to change (MW) (Hz) (Hz) (Hz) (Hz) (MW) change (MW) (MW) Scottish and Southern Energy, Cantelo Nurseries, Bradon Farm, Isle Abbots, Taunton, Somerset Gas Y Y 9.7 9.7 9.7 0.0 47.00 50.50 Following Settings have been applied: 47.5Hz 20s, 47Hz 0.5s, 52Hz 0.5s Bears Down Wind Farm Ltd, Bears Down Wind Farm, St Mawgan, Newquay, Cornwall Wind_onshore Y N 9.6 9.6 0.0 0.0 47.00 50.50 Contact made. Awaiting info. Generator has agreed to apply the new single stage settings (i.e. 47.5Hz 0.5s and 51.5Hz 0.5s) - British Gas Transco, Severn Road, Avonmouth, Bristol Gas Y Y 5.5 5.5 5.5 0.0 47.00 50.50 complete 23/11/10 Cold Northcott Wind Farm Ltd, Cold Northcott, Launceston, Cornwall Wind_onshore Y Y 6.8 6.8 6.8 0.0 47.00 50.50 Changes completed. Generator has agreed to apply the new single stage settings (i.e. 47.5Hz 0.5s and 51.5Hz Connon Bridge Energy Ltd, Landfill Site, East Taphouse, Liskeard, Cornwall 0.5s).Abdul Sattar confirmed complete by email 19/11/10. -

International Passenger Survey, 2008

UK Data Archive Study Number 5993 - International Passenger Survey, 2008 Airline code Airline name Code 2L 2L Helvetic Airways 26099 2M 2M Moldavian Airlines (Dump 31999 2R 2R Star Airlines (Dump) 07099 2T 2T Canada 3000 Airln (Dump) 80099 3D 3D Denim Air (Dump) 11099 3M 3M Gulf Stream Interntnal (Dump) 81099 3W 3W Euro Manx 01699 4L 4L Air Astana 31599 4P 4P Polonia 30699 4R 4R Hamburg International 08099 4U 4U German Wings 08011 5A 5A Air Atlanta 01099 5D 5D Vbird 11099 5E 5E Base Airlines (Dump) 11099 5G 5G Skyservice Airlines 80099 5P 5P SkyEurope Airlines Hungary 30599 5Q 5Q EuroCeltic Airways 01099 5R 5R Karthago Airlines 35499 5W 5W Astraeus 01062 6B 6B Britannia Airways 20099 6H 6H Israir (Airlines and Tourism ltd) 57099 6N 6N Trans Travel Airlines (Dump) 11099 6Q 6Q Slovak Airlines 30499 6U 6U Air Ukraine 32201 7B 7B Kras Air (Dump) 30999 7G 7G MK Airlines (Dump) 01099 7L 7L Sun d'Or International 57099 7W 7W Air Sask 80099 7Y 7Y EAE European Air Express 08099 8A 8A Atlas Blue 35299 8F 8F Fischer Air 30399 8L 8L Newair (Dump) 12099 8Q 8Q Onur Air (Dump) 16099 8U 8U Afriqiyah Airways 35199 9C 9C Gill Aviation (Dump) 01099 9G 9G Galaxy Airways (Dump) 22099 9L 9L Colgan Air (Dump) 81099 9P 9P Pelangi Air (Dump) 60599 9R 9R Phuket Airlines 66499 9S 9S Blue Panorama Airlines 10099 9U 9U Air Moldova (Dump) 31999 9W 9W Jet Airways (Dump) 61099 9Y 9Y Air Kazakstan (Dump) 31599 A3 A3 Aegean Airlines 22099 A7 A7 Air Plus Comet 25099 AA AA American Airlines 81028 AAA1 AAA Ansett Air Australia (Dump) 50099 AAA2 AAA Ansett New Zealand (Dump)