Go-Ahead Rail and a Our Devol to Deliver

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Employment and Working Conditions in the Air Transport Sector Over the Period 1997/2010

Study on the effects of the implementation of the EU aviation common market on employment and working conditions in the Air Transport Sector over the period 1997/2010 Final Report Report July 2012 Prepared for: Prepared by: European Commission Steer Davies Gleave DG MOVE 28-32 Upper Ground Unit E1 London SE1 9PD DM 24-5/106 B-1049 Brussels Belgium +44 (0)20 7910 5000 www.steerdaviesgleave.com Final Report CONTENTS EXECUTIVE SUMMARY ...................................................................................... I Background ............................................................................................ i Scope of this study ................................................................................... i Conclusions ........................................................................................... ii Recommendations .................................................................................. xi 1 INTRODUCTION ..................................................................................... 1 Background ............................................................................................ 1 Key findings of the 2010 Working Document .................................................... 1 The need for this study ............................................................................. 1 Structure of this report ............................................................................. 2 2 RESEARCH METHODOLOGY ....................................................................... 3 Objectives -

The Go-Ahead Group Plc Annual Report and Accounts 2019 1 Stable Cash Generative

Annual Report and Accounts for the year ended 29 June 2019 Taking care of every journey Taking care of every journey Regional bus Regional bus market share (%) We run fully owned commercial bus businesses through our eight bus operations in the UK. Our 8,550 people and 3,055 buses provide Stagecoach: 26% excellent services for our customers in towns and cities on the south FirstGroup: 21% coast of England, in north east England, East Yorkshire and East Anglia Arriva: 14% as well as in vibrant cities like Brighton, Oxford and Manchester. Go-Ahead’s bus customers are the most satisfied in the UK; recently Go-Ahead: 11% achieving our highest customer satisfaction score of 92%. One of our National Express: 7% key strengths in this market is our devolved operating model through Others: 21% which our experienced management teams deliver customer focused strategies in their local areas. We are proud of the role we play in improving the health and wellbeing of our communities through reducing carbon 2621+14+11+7+21L emissions with cleaner buses and taking cars off the road. London & International bus London bus market share (%) In London, we operate tendered bus contracts for Transport for London (TfL), running around 157 routes out of 16 depots. TfL specify the routes Go-Ahead: 23% and service frequency with the Mayor of London setting fares. Contracts Metroline: 18% are tendered for five years with a possible two year extension, based on Arriva: 18% performance against punctuality targets. In addition to earning revenue Stagecoach: 13% for the mileage we operate, we have the opportunity to earn Quality Incentive Contract bonuses if we meet these targets. -

S/C/W/270 18 July 2006 ORGANIZATION (06-3471) Council for Trade in Services

WORLD TRADE RESTRICTED S/C/W/270 18 July 2006 ORGANIZATION (06-3471) Council for Trade in Services SECOND REVIEW OF THE AIR TRANSPORT ANNEX DEVELOPMENTS IN THE AIR TRANSPORT SECTOR (PART ONE) Note by the Secretariat1 TABLE OF CONTENTS LIST OF TABLES, CHARTS, FIGURES AND APPENDIXES......................................................vi LIST OF ACRONYMS ........................................................................................................................ix INTRODUCTION..................................................................................................................................1 I. AIRCRAFT REPAIR AND MAINTENANCE (MRO).........................................................4 A. ECONOMIC DEVELOPMENTS .......................................................................................................4 B. REGULATORY DEVELOPMENTS.................................................................................................13 1. Developments concerning the regulation of Maintenance Repair and Overhaul .........13 (a) General evolution ..............................................................................................................13 (b) Maintenance Steering Group (MSG) rules........................................................................13 (c) WTO developments...........................................................................................................13 (d) European Communities .....................................................................................................14 -

Aviance UK Limited

Completed acquisition by Servisair UK Limited of the regional ground handling business of Aviance UK Limited ME/4429/10 The OFT’s decision on reference under section 22(1) given on 27 May 2010. Full text of decision published 15 June 2010. PARTIES 1. Servisair UK Limited ('Servisair') provides ground handling services at 21 UK airports. Its ultimate parent is Derichebourg SA, a leading global provider of aviation ground handling operations delivering a range of ground handling services across 148 airports worldwide. 2. Aviance UK Limited ('Aviance') is a subsidiary of the Go-Ahead Group, a leading UK public transport operator, and founder member of the worldwide Aviance alliance of airport service providers. Prior to this transaction, Aviance operated at a number of UK airports including Edinburgh, Heathrow, Manchester and Stansted. TRANSACTION 3. The transaction concerns the transfer to Servisair of Aviance's ground handling business at 11 regional airports in the UK, namely Aberdeen, Belfast Harbour, Belfast International, Birmingham International, Cardiff, Edinburgh, Glasgow, Luton, Manchester, Southampton and Stansted. In addition to ground handling services, Servisair also acquired Aviance’s passenger lounge at Gatwick and its cargo operations at Stansted. 4. By way of background, Aviance, having decided to exit the provision of ground handling services at regional airports, invited a number of parties operating in the air transport industry to express their interest in acquiring its regional airport ground handling business. Servisair declined to make a bid for Aviance’s ground handling business as a whole. 1 5. Aviance retained its contracts at London Heathrow Terminal 1 as a continuing activity and sold the ground handling business at Heathrow Terminals 3 and 4 to Dnata, a company owned by the Investment Corporation of Dubai. -

Railnews 2009 Directory

Railnews 2009 Directory 1.Train Operators Full listing of all UK passenger & freight operating companies in the UK 2. Recruitment & Training Companies & government-run organisations focused on training and recruitment within the UK rail industry 3. Industry Stakeholders Government & independent organisations including Network Rail and the BTP 4. Industry Suppliers UK and International companies supplying, manufacturing and serving the UK industry 5. Industry Representatives Rail and transport unions Railnews Ltd, 180-186 Kings Cross Road, Kings Cross Business Centre, London, WC1X 9DE | 020 7689 1610 | www.railnews.co.uk | [email protected] Train Operators Train Operators ARRIVA PLC Fax: 01603 214 517 Managing Director UK Trains: Bob Holland Email: [email protected] EAST MIDLAND TRAINS (Stagecoach Group) Telephone: 0191 520 4000 Website: www.c2c-online.co.uk Managing Director: Tim Shoveller Email: [email protected] Postal Address: c2c Rail Ltd, 207 Old Street, London, EC1V 9NR Telephone: 08457 125 678 Website: www.arriva.co.uk Email: [email protected] Postal Address: Admiral Way, Doxford International Business Park, CHILTERN RAILWAYS (DB Regio/Laing Rail) Website: www.eastmidlandstrains.co.uk Sunderland, SR3 3XP Chairman: Adrian Shooter Postal Address: East Midlands Trains, 1 Prospect Place, Millennium Franchises: Arrive Trains Wales; CrossCountry. Telephone: 08456 005 165 Way, Pride Park, Derby, DE24 8HG Fax: 01296 332126 ARRIVA TRAINS WALES/TRENAU ARRIVA CYMRU Website: www.chilternrailways.co.uk EUROSTAR Managing Director: Tim Bell Postal Address: The Chiltern Railway Company Ltd, 2nd floor, Eurostar (UK) Ltd is part of Eurostar Group. the UK company is owned Telephone: 0845 6061660 Western House, 14 Rickfords Hill, Aylesbury, Buckinghamshire, HP20 by London and Continental Railways and managed by Inter Capital Fax: 02920 645349 2RX and Regional Rail Ltd, a consortium of National Express Group, Email: [email protected] Belgian Railways, French Railways and British Airways. -

Volume 3 Appendix C 1 APPENDIX C 1 COUNTRY/CURRENCY CODES

PPSysB 19.00x PageLayout: HMRC2R [SO] Page: 1 Processed: 01-10-2015 11:17:34 Job: TARIFC Unit: PG09 . Volume 3 Appendix C 1 APPENDIX C 1 COUNTRY/CURRENCY CODES Enter in boxes 15a, 17a, 18, 21, 34a and 55 the appropriate code for the country in question, as directed. Enter in Box 22, 63, 65a, 66, 67 and 68 the appropriate code for the currency in question as directed. Country Code Currency Code Country Code Currency Code A Bulgaria BG Lev BGN Abu Dhabi (1) AE UAE Dirham AED Burkina Faso (formerly Upper BF West African Franc XOF Afghanistan AF Afghani AFN Volta) Ajman (1) AE UAE Dirham AED Burundi BI Burundese Franc BIF A˚ land Islands (2) FI Euro EUR C Alaska (3) US US Dollar USD Cambodia (Kampuchea) KH Khmer Rial KHR Albania AL Lek ALL Cameroon CM CFA Franc XAF Algeria DZ Algerian Dinar DZD Canada CA Canadian Dollar CAD American Polynesia UM US Dollar USD and Oceania (4) Canary Islands IC Euro EUR American Samoa AS US Dollar USD Cape Verde CV Cape Verde Escudo CVE Andorra AD Euro EUR Caroline Islands (4) UM US Dollar USD Angola (including Cabinda) AO Kwanza AOA Cayman Islands KY Cayman Island Dollar KYD Anguilla AI East Caribbean Dollar XCD Central African Republic CF CFA Franc XAF Antarctica (Territory south of AQ Norwegian Krone NOK Ceuta XC Euro EUR 60) south latitude; not Chad TD CFA Franc XAF including the French Chile CL Chilean Peso CLP Southern Territories (TF), China CN Yuan (Ren Min Bi) CNY Bouvet Islands (BV), South Georgia and South Christmas Island (Indian Ocean) CX Australian Dollar AUD Sandwich Islands (GS)) Cocos Islands -

Delivering a Better Railway for a Better Britain

Network Rail Limited Annual report and accounts 2014 Delivering a better railway for a better Britain Network Rail Limited Annual report and accounts 2014 About us We are the not for dividend owner and operator of Britain’s railway infrastructure, which includes the tracks, signals, tunnels, bridges, viaducts, level crossings and stations – the largest of which we also manage. We aim to provide a safe, reliable and efficient rail infrastructure for freight and passenger trains. Our highlights during the year Our railway is more popular than ever, with We exceed our level crossing Extreme flooding in Dawlish passenger numbers increasing at a faster closure target Severe storms, torrential rainfall rate than expected. This alone has put a We closed 804 level crossings, exceeding and strong winds in early 2014 disrupted strain on our assets, and combined with the our target of closing 750, 10 per cent our network, including 100 metres of sea wettest winter for almost 250 years, has of Britain’s crossings, by April 2014. wall destroyed in Devon. Our 300-strong required increasing our efforts to deliver, The closure of level crossings has been ‘orange army’ battled for over two months particularly with regards to operational supported by a programme of other works to restore services so people could reach performance. Whilst we have failed to including Rail Life – a national schools their destinations in Devon and Cornwall meet some of the targets set for CP4, campaign and investment in technology. in time for Easter. our people have delivered some tangible results during the year – which we are proud to share. -

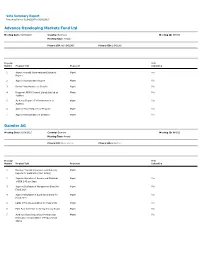

Quarterly Voting Disclosure Q2

Vote Summary Report Reporting Period: 01/04/2015 to 30/06/2015 Advance Developing Markets Fund Ltd Meeting Date: 01/04/2015 Country: Guernsey Meeting ID: 939199 Meeting Type: Annual Primary ISIN: GG00B45L2K95 Primary SEDOL: B45L2K9 Proposal Vote Number Proposal Text Proponent Instruction 1 Accept Financial Statements and Statutory Mgmt For Reports 2 Approve Remuneration Report Mgmt For 3 Reelect John Hawkins as Director Mgmt For 4 Reappoint KPMG Channel Islands Limited as Mgmt For Auditors 5 Authorise Board to Fix Remuneration of Mgmt For Auditors 6 Approve Share Repurchase Program Mgmt For 7 Approve Remuneration of Directors Mgmt For Daimler AG Meeting Date: 01/04/2015 Country: Germany Meeting ID: 940823 Meeting Type: Annual Primary ISIN: DE0007100000 Primary SEDOL: 5529027 Proposal Vote Number Proposal Text Proponent Instruction 1 Receive Financial Statements and Statutory Mgmt Reports for Fiscal 2014 (Non-Voting) 2 Approve Allocation of Income and Dividends Mgmt For of EUR 2.45 per Share 3 Approve Discharge of Management Board for Mgmt For Fiscal 2014 4 Approve Discharge of Supervisory Board for Mgmt For Fiscal 2014 5 Ratify KPMG AG as Auditors for Fiscal 2015 Mgmt For 6 Elect Paul Achleitner to the Supervisory Board Mgmt For 7 Authorize Share Repurchase Program and Mgmt For Reissuance or Cancellation of Repurchased Shares Vote Summary Report Reporting Period: 01/04/2015 to 30/06/2015 Daimler AG Proposal Vote Number Proposal Text Proponent Instruction 8 Authorize Use of Financial Derivatives when Mgmt For Repurchasing Shares 9 Approve -

Completed Acquisition by Menzies Aviation (UK) Limited of Part of the Business of Airline Services Limited

Completed acquisition by Menzies Aviation (UK) Limited of part of the business of Airline Services Limited Decision on relevant merger situation and substantial lessening of competition ME/6746/18 The CMA’s decision on reference under section 22(1) of the Enterprise Act 2002 given on 7 August 2018. Full text of the decision published on 21 August 2018. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. SUMMARY 1. On 4 April 2018, Menzies Aviation (UK) Limited (Menzies) acquired part of the business of Airline Services Limited (Airline Services) (the Merger). Menzies and Airline Services are together referred to as the Parties. 2. The Competition and Markets Authority (CMA) believes that it is or may be the case that each of Menzies and Airline Services is an enterprise, that these enterprises have ceased to be distinct as a result of the Merger, and that the share of supply test is met. The four-month period for a decision, as extended, has not yet expired. The CMA therefore believes that it is or may be the case that a relevant merger situation has been created. 3. The Parties overlap in the supply of: (a) De-icing services at Edinburgh airport (EDI); (b) De-icing services at Glasgow airport (GLA); (c) De-icing services at London Heathrow airport (LHR); 1 (d) Ground handling services1 at London Gatwick airport (LGW); (e) Ground handling services at Manchester airport (MAN); and (f) Internal presentation services at MAN. -

The Go-Ahead Group Plc Environmental & Social Report 2007

THE GO-AHEAD GROUP PLC ENVIRONMENTAL & SOCIAL REPORT 2007 www.go-ahead.com/corporateresponsibility Group 100% magenta Group 100% magenta Group 100% magenta GrouGroup p300u 100% magenta Group 300uGroup 300u Group 300u Group 100% magenta Group 300u CONTENTS 02 06 14 22 28 GROUP OVERVIEW BUS OPERATIONS RAIL OPERATIONS AVIATION SUPPORT PERFORMANCE AND PARKING DATA - About The Go-Ahead Carrying almost We operate the We offer ground - CR performance data Group 550 million people, our Southern and handling and parking for each of our - Our role in society buses play a vital role Southeastern rail services at 17 airports in operating companies - Why corporate in reducing local franchises connecting the UK and Ireland. Our - Independent responsibility congestion and helping London and the South parking management Assurance Statement matters to us tackle social exclusion. Coast. Responsibility is company also provides - Benchmarking our Here we report on at the heart of our specialist security performance our responsibilities successful transformation services.We report on as a bus operator: of Southern and our our responsibilities: 04 future plans for INTRODUCTION Southeastern.We explain here our priorities - Our responsibilities and plans: - Consulting stakeholders 06 MARKETPLACE 14 MARKETPLACE 22 MARKETPLACE 08 WORKPLACE 16 WORKPLACE 24 WORKPLACE 10 ENVIRONMENT 18 ENVIRONMENT 26 ENVIRONMENT 12 COMMUNITY 20 COMMUNITY 27 COMMUNITY Go-Ahead Environmental & Social Report 2007 1 CHIEF EXECUTIVE’S STATEMENT CLIMATE CHANGE IS THE MOST PRESSING ISSUE FACING THIS GENERATION.THE WEIGHT OF SCIENTIFIC EVIDENCE IS SUCH THAT GOVERNMENTS AND OTHERS ARE LOOKING URGENTLY TO ADDRESS THE CHALLENGES WE FACE. Surface transport is part of the climate change Our rail, aviation and parking companies share I have focused on the environment for this ‘mix’, accounting for around a quarter of UK this commitment to environmental excellence. -

Annual Report for 2016/17

London Transport Museum is an educational and heritage preservation charity. Our purpose is to conserve and explain the history of London’s transport, to offer people an understanding of the Capital’s past development and to engage them in the debate about its future. London Transport Museum Annual STRATEGIC REPORT 03 Message from the Chair of Trustees and Managing Director Report 2016/17 incorporating the 05 Designology Strategic Report, Annual Report of 13 The year in summary the Trustees and financial 20 Access and museum operations statements for the year ended 23 Education and engagement 31 March 2017 28 Heritage and collections 32 Plans for the future 34 Interchange 36 Income and support 41 Corporate Members 43 Supporters and Sponsors 45 Patrons Circle 48 Public programme 57 Financial review ANNUAL REPORT OF THE TRUSTEES 64 History of the Museum 66 Structure, governance and management 72 Trustees’ statement 74 Trustees and advisers 76 Independent auditor’s report 79 Financial statements We are proud to present the London Transport Museum (LTM) A highlight of our integrated education strategy is the ‘Enjoyment Annual Report for 2016/17. It was another busy and exciting to Employment’ programme which builds on young visitors’ year with nearly 370,000 visitors to the Museum and Depot, enjoyment of our galleries and points them towards a career in making it our second-best result ever. We also increased our transport and engineering. Industry partners, encouraged by our reach well beyond the Museum’s walls with successful ability to work with young people to develop their confidence and education programmes, popular tours, heritage vehicle trips employability, have engaged with us to promote careers in the and much more. -

Downloaded in Microsoft Excel Spreadsheet Format and Includes All Times on Different Parts of the Airport (Runway Or Taxiways), Speeds, and Ground Holding Times

EUROPEAN ORGANISATION FOR THE SAFETY OF AIR NAVIGATION EUROCONTROL EUROCONTROL EXPERIMENTAL CENTRE LONDON Heathrow CDM WP1 EEC Note No. 03/05 Project London Heathrow CDM Issued: February 2005 The information contained in this document is the property of the EUROCONTROL Agency and no part should be reproduced in any form without the Agency’s permission. The views expressed herein do not necessarily reflect the official views or policy of the Agency. REPORT DOCUMENTATION PAGE Reference: Security Classification: EEC Note No. 03/05 Unclassified Originator: Originator (Corporate Author) Name/Location: EEC - APT EUROCONTROL Experimental Centre Centre de Bois des Bordes (Airport Throughput Business Area) B.P.15 F – 91222 Brétigny-sur-Orge Cedex FRANCE Telephone: +33 (0)1 69 88 75 00 Sponsor: Sponsor (Contract Authority) Name/Location: EUROCONTROL EUROCONTROL Agency 96, Rue de la Fusée B-1130 Brussels BELGIUM Telephone: +32 2 729 90 11 TITLE: LONDON Heathrow CDM WP1 Authors Date Pages Figures Tables Annexes References R. Lane 02/2005 xvi + 115 39 11 3 - D. Hogg Project Task No. Sponsor Period CDM London - 2004 Heathrow Airport Distribution Statement: (a) Controlled by: Peter ERIKSEN - EUROCONTROL BUSINESS AREA MANAGER Roger LANE - EUROCONTROL CDM PROJECT MANAGER (b) Special Limitations: None (c) Copy to NTIS: YES / NO Descriptors (keywords): Collaborative Decision Making – Target Off Block Time – Common Situational Awareness – Flight Update Message – Departure Planning Information – Start-up Approval Time – Variable Taxi Time Abstract: This project is a collaboration between the EUROCONTROL Experimental Centre (EEC), EUROCONTROL Airport Operations Unit (APR) and London Heathrow Airport represented by the BAA, UK National Air Traffic Services (NATS), British Airways (BA), bmi and other partners.