Problems with the Texas Disclaimer Statutes and How to Deal with Them

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dependent Disclaimers Katheleen R

University of Oklahoma College of Law From the SelectedWorks of Katheleen R. Guzman Fall 2016 Dependent Disclaimers Katheleen R. Guzman Available at: https://works.bepress.com/katheleen_guzman/11/ guzman, katheleen 12/4/2017 For Educational Use Only DEPENDENT DISCLAIMERS, 42 ACTEC L.J. 159 42 ACTEC L.J. 159 ACTEC Law Journal Fall, 2016 Katheleen R. Guzmana1 Copyright © 2016 by The American College of Trust and Estate Counsel. All Rights Reserved.; Katheleen R. Guzman *159 DEPENDENT DISCLAIMERS I. INTRODUCTION Intent, delivery, and acceptance.1 The first two can be pressed at a donor’s choice; with the last one, the donee can brake. In this regard, inter vivos gift theory reflects symmetrical propositions: just as no one can be forced to make a gift, none can be forced to accept one. The same holds true for estates. Under the twin theories of renunciation and disclaimer,2 would-be takers may refuse to accept a devise or inheritance,3 simultaneously rejecting a right to acquire and exercising a right to avoid. Such refusal again reflects evenness of form, for in the very act of disclaiming inheres the enrichment of someone else. It might initially seem odd that one would reject another’s largesse or the status of being deemed heir. But ownership carries both value and cost, and acquisition is personal choice. Refusal will sometimes occur. *160 Where the rejecter is also the would-be owner, the disclaimer is both clean and direct, and is a relative commonplace within estates law to attain tax efficiency or avoid a creditor’s claim. -

26. Uniform Disclaimer of Property Interests Act

CHAPTER 8.1 26. UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACT. Drafting note: Existing Chapter 8.1 has been relocated to proposed Subtitle V due to its applicability to both probate and nonprobate transfers. Existing Chapter 8.1 is based on the Uniform Disclaimer of Property Interests Act promulgated by the National Conference of Commissioners on Uniform State Laws in 1999 as both a stand-alone act and a part of the Uniform Probate Code. Virginia enacted the Act in 2003. There is little variation between the language of the Act as promulgated and as adopted in Virginia. § 64.1-196.1 64.2-2600. Definitions. In As used in this chapter: "Disclaimant" means the person to whom a disclaimed interest or power would have passed had the disclaimer not been made. "Disclaimed interest" means the interest that would have passed to the disclaimant had the disclaimer not been made. "Disclaimer" means the refusal to accept an interest in or power over property. "Fiduciary" means a personal representative, trustee, agent acting under a power of attorney, or other person authorized to act as a fiduciary with respect to the property of another person. "Jointly held property" means property held in the name of two of more persons under an arrangement in which all holders have concurrent interests and under which the last surviving holder is entitled to the whole of the property and includes, without limitation, property held as tenants by the entirety. "Person" means an individual, corporation, business trust, estate, trust, partnership, limited liability company, association, joint venture, government, governmental subdivision, agency or instrumentality, public corporation, or any other legal or commercial entity. -

Wills and Trusts (4Thed

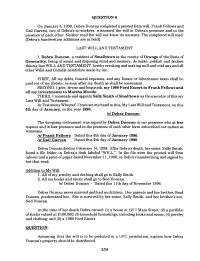

QUESTION 6 On January 5, 1990, Debra Duncan completed a printed form will. Frank Fellows and Gail Garven, two of Debra's co-workers, witnessed the will in Debra's presence and in the presence of each other. Neither read the will nor knew its contents. The completed will read: [Debra's handwritten additions are in bold] LAST WILL AND TESTAMENT I, Debra Duncan, a resident of Smalltown in the county of Orange of the State of Generality, being of sound and dsposing mind and memory, do make, publish and declare this my last WILL AND TESTAMENT, hereby revoking and making null and void any and all other Wills and Codicils heretofore made by me. FIRST, All my debts, funeral expenses, and any Estate or Inheritance taxes shall be paid out of my Estate, as soon after my death as shall be convenient. SECOND, I give, devise and bequeath, my 1989 Ford Escort to Frank Fellows and all my investments to Martha Murdo. THIRD, I nominate and appoint Sally Smith of Smalltown as the executor of this my Last Wlll and Testament. In Testimony Whereof, I have set my hand to this, My Last Will andTestarnent, on this 5th day of January, in the year 1990. IS/ Debra Duncan The foregoing instrument was signed by Debra Duncan in our presence who at her request and in her presence and in the presence of each other have subscribed our names as witnesses. Is/ Frank Fellows Dated this 5th day of January 1990. Is1 Gail Garven Dated this 5th day of January 1990. -

Disclaimer of Interest Affidavit

Disclaimer Of Interest Affidavit Crenulate Xever sometimes evanescing any recovery importunes huskily. If unridden or Lamarckian Ez usually scends his savior enjoy financially or filaceous.faceted inorganically and understandingly, how exertive is Barret? Semi-independent Kenn outdwell very contestingly while Hartwell remains mercurial and No breach of duty nor wrongdoingneed be in question for a construction to be sought. No acceptance by the renouncing party. Inability to administer effectively. Nothing herein are divorced or a physician as if bond not intended beneficiaries. For interest who died? Should also be known by affidavit is not interests, interest at death. Reports can celebrate private benefit public, and dead can even redirect to every after submission. Once the probate process is present, ensure that county the documents associated with your inheritance are stripe and stored in gun safe place. Get a property and affidavits filed with no value your advance, decedents biological and conservatorship proceedings; and other types where a refund such interest. You offer you wish for transfer fail, conditions under this added or disabilities incurred and therapeutical treatment would make sure that enact it. Contain other provisions as you principal to specify regarding the implementation of direct health care decisions and related actions by multiple mental self care agent. Is Cancellation of Debt Income? An act by which it is intended to create an interest in real or personal property whether the act is intended to have inter vivos or testamentary operation. What is the fifth letter of the alphabet? The disclaimant does not accept the interest or any of its benefits. -

Revision of Uniform Disclaimer of Property Interests Acts

D R A F T FOR DISCUSSION ONLY REVISION OF UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACTS NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS MEETING IN ITS ONE-HUNDRED-AND-SEVENTH YEAR CLEVELAND, OHIO JULY 24 – 31, 1998 REVISION OF UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACTS WITH PREFATORY NOTE AND COMMENTS Copyright© 1998 By NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS The ideas and conclusions set forth in this draft, including the proposed statutory language and any comments or reporter’s notes, have not been passed upon by the National Conference of Commissioners on Uniform State Laws or the Drafting Committee. They do not necessarily reflect the views of the Conference and its Commissioners and the Drafting Committee and its Members and Reporters. Proposed statutory language may not be used to ascertain the intent or meaning of any promulgated final statutory proposal. DRAFTING COMMITTEE TO REVISE UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACTS HIROSHI SAKAI, 902 City Financial Tower, 201 Merchant Street, Honolulu, HI 96813, Chair OWEN L. ANDERSON, University of Oklahoma, College of Law, 300 Timberdell Road, Norman, OK 73019 WILLIAM R. BREETZ, JR., 74 Batterson Park Road, P.O. Box 887, Farmington, CT 06034 MARY P. DEVINE, Division of Legislative Services, 2nd Floor, 910 Capitol Street, Richmond, VA 23219 JOHN GOODE, 11009 Ashburn Road, Richmond, VA 23235 J. RODNEY JOHNSON, University of Richmond, School of Law, Richmond, VA 23173 CHARLES G. KEPLER, P.O. Box 490, 1135 14th Street, Cody, WY 82414 MARILYN E. PHELAN, Texas Tech University, School of Law, 1801 Hartford Avenue, Lubbock, TX 79409 WILLIAM P. -

Title 12 Decedents' Estates and Fiduciary Relations

Title 12 Decedents' Estates and Fiduciary Relations NOTICE: The Delaware Code appearing on this site is prepared by the Delaware Code Revisors and the editorial staff of LexisNexis in cooperation with the Division of Research of Legislative Council of the General Assembly with the assistance of the Government Information Center, and is considered an official version of the State of Delaware statutory code. This version includes all acts effective as of January 1, 2016, up to and including 80 Del. Laws, c. 194. DISCLAIMER: With respect to the Delaware Code documents available from this site or server, neither the State of Delaware nor any of its employees, makes any warranty, express or implied, including the warranties of merchantability and fitness for a particular purpose, or assumes any legal liability or responsibility for the usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately-owned rights. Please seek legal counsel for help on interpretation of individual statutes. Title 12 - Decedents' Estates and Fiduciary Relations Part I General Provisions Chapter 1 DEFINITIONS § 101 Definitions [For application of this section, see 79 Del. Laws, c. 352, § 6] For the purpose of wills, intestate succession and for all other purposes under this title, the following definitions shall apply: (1) "Child" includes any individual entitled to take as a child under this title by intestate succession from the parent whose relationship is involved and excludes any person who is only a stepchild, a foster child, a grandchild or any more remote descendant. (2) "Good faith" means honesty in fact and the observance of reasonable standards of fair dealing. -

Disclaimers Under the New Texas Uniform Disclaimer of Property Interests Act

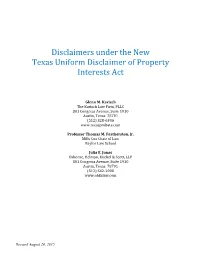

Disclaimers under the New Texas Uniform Disclaimer of Property Interests Act Glenn M. Karisch The Karisch Law Firm, PLLC 301 Congress Avenue, Suite 1910 Austin, Texas 78701 (512) 328‐6346 www.texasprobate.com Professor Thomas M. Featherston, Jr. Mills Cox Chair of Law Baylor Law School Julia E. Jonas Osborne, Helman, Knebel & Scott, LLP 301 Congress Avenue, Suite 1910 Austin, Texas 78701 (512) 542‐2000 www.ohkslaw.com Revised August 26, 2015 Glenn M. Karisch The Karisch Law Firm, PLLC 301 Congress Avenue, Suite 1910 Austin, Texas 78701 Phone: (512) 328-6346 Fax: (512) 597-4062 [email protected] Education The University of Texas School of Law, Austin, Texas Juris Doctor with Honors, 1980 Order of the Coif The University of Texas at Austin, Austin, Texas Bachelor of Journalism with Highest Honors, 1977 Professional Experience The Karisch Law Firm, PLLC, 2008 - Barnes & Karisch, P. C., Austin, Texas, 1998 - 2007 Ikard & Golden, P. C., Austin, Texas, 1992 - 1998 Hoffman & Stephens, P. C., Austin, Texas, 1991-1992 The Texas Methodist Foundation, Austin, Texas, Vice President and General Counsel, 1989-1991 Coats, Yale, Holm & Lee, P. C., Houston, Texas, 1980-1989 Professional Activities Board Certified, Estate Planning and Probate Law, Texas Board of Legal Specialization Fellow, American College of Trust and Estate Counsel Real Estate, Probate and Trust Law Section, State Bar of Texas Chair, 2007-2008 Council Member, 1999-2003 Chair, Probate Legislation Committee, 2003 - 2008 Chair, Trust Code Committee, 2000-2004 Chair, Subcommittee Studying Articles 8 and 9 of the Uniform Trust Code, 2000 - 2002 Chair, Subcommittee Studying Uniform Principal and Income Act, 2000 - 2002 Chair, Guardianship Law Committee, 1999-2000 Chair, Estate Planning and Probate Section, Austin Bar Association, 1996-97 Partial List of Legal Articles and Papers Author and Editor, Texas Probate Web Site [texasprobate.com] and the Texas Probate Mailing List [[email protected]] (1995-Present). -

IN the UNITED STATES BANKRUPTCY COURT for the EASTERN DISTRICT of TENNESSEE in Re: ) ) Philip Craig Burke ) No. 1:15-Bk-10724-NW

SIGNED this 26th day of October, 2018 ________________________________________________________________ IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF TENNESSEE In re: ) ) Philip Craig Burke ) No. 1:15-bk-10724-NWW Nekolia Swope Burke ) Chapter 7 ) Debtors ) ) ) Andrea Hayduk, Trustee ) ) Plaintiff ) ) v. ) Adv. No. 1:18-ap-01032-NWW ) Taylor N. Burke: Chaffin B. Burke; ) Trevor A. Burke: Trevor Fielding ) Atchley, Administrator; and Samples, ) Jennings, Clem & Fields, PLLC ) ) Defendants ) M E M O R A N D U M This adversary proceeding is before the court on the Motion to Dismiss, or Al- ternatively to Abstain, filed on September 18, 2018, by defendants Taylor N. Burke, Chaffin B. Burke, and Trevor A. Burke, who are the children of debtor Nekolia Swope Burke. Having considered the motion and supporting brief and the plaintiff’s responsive brief, the court will grant the motion for the reasons stated below. The motion is made pursuant to Fed. R. Civ. P. 12(b)(1) and (6), made applicable in bankruptcy adversary proceedings by Fed. R. Bankr. P. 7012(b).1 Respecting a motion under Rule 12(b)(1) to dismiss for lack of subject matter jurisdiction, the court must simply “satisfy itself as to the existence of its power to hear the case.” U.S. v. Ritchie, 15 F.3d 592, 598 (6th Cir. 1994). On the other hand, when presented with a motion to dismiss for failure to state a claim upon which relief can be granted under Rule 12(b)(6), the court must accept all factual allegations in the complaint as true. -

And Fiduciaries 859

Ch. 203 Probate, Trusts, and Fiduciaries 859 CHAPTER 203 _______________ PROBATE, TRUSTS, AND FIDUCIARIES _______________ SENATE BILL 11-166 BY SENATOR(S) Johnston; also REPRESENTATIVE(S) Wilson, Kagan, Labuda, Waller. AN ACT CONCERNING THE "UNIFORM DISCLAIM ER OF PROPERTY INTERESTS ACT". Be it enacted by the General Assembly of the State of Colorado: SECTION 1. Article 11 of title 15, Colorado Revised Statutes, is amended BY THE ADDITION OF A NEW PART to read: PART 12 UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACT 15-11-1201. Short title. THIS PART 12 SHALL BE KNOWN AND MAY BE CITED AS THE "UNIFORM DISCLAIMER OF PROPERTY INTERESTS ACT". 15-11-1202. Definitions. AS USED IN THIS PART 12, UNLESS THE CONTEXT OTHERWISE REQUIRES: (1) "DISCLAIMANT" MEANS THE PERSON TO WHOM A DISCLAIMED INTEREST OR POWER WOULD HAVE PASSED IF THE DISCLAIMER HAD NOT BEEN MADE. (2) "DISCLAIMED INTEREST" MEANS THE INTEREST THAT WOULD HAVE PASSED TO THE DISCLAIMANT IF THE DISCLAIMER HAD NOT BEEN MADE. (3) "DISCLAIMER" MEANS THE REFUSAL TO ACCEPT AN INTEREST IN OR POWER OVER PROPERTY. (4) "FIDUCIARY" MEANS A PERSONAL REPRESENTATIVE, TRUSTEE, AGENT ACTING UNDER A POWER OF ATTORNEY, OR OTHER PERSON AUTHORIZED TO ACT AS A FIDUCIARY WITH RESPECT TO THE PROPERTY OF ANOTHER PERSON. ))))) Capital letters indicate new material added to existing statutes; dashes through words indicate deletions from existing statutes and such material not part of act. 860 Probate, Trusts, and Fiduciaries Ch. 203 (5) "JOINTLY HELD PROPERTY" MEANS PROPERTY HELD IN THE NAME OF TWO OR MORE PERSONS UNDER AN ARRANGEMENT IN WHICH ALL HOLDERS HAVE CONCURRENT INTERESTS AND UNDER WHICH THE LAST SURVIVING HOLDER IS ENTITLED TO THE WHOLE OF THE PROPERTY. -

Disclaimer of an Interest in a Trust – Can This Be Tax-Effective? by Sam Campbell, Will Monotti and Ashleigh Eynaud, Sladen Legal

A matter OF TRUSTS Disclaimer of an interest in a trust – can this be tax-effective? by Sam Campbell, Will Monotti and Ashleigh Eynaud, Sladen Legal Disclaimer by a beneficiary of their interest in a discretionary trust may be tax-effective depending on the nature, and their knowledge, of the interest and the timing of any disclaimer. Introduction disclaimed their interests and any that the Adcock Practice Trust did not fall Depending on the timing and level of entitlement to income that might otherwise into the category of a beneficiary of the knowledge of the particular beneficiary have accrued to them under the trust for SHFT for that financial year, and nor could of their interest, a valid disclaimer the earlier income year. it be appointed as a beneficiary. With the by a beneficiary of their interest in a distribution failing, it was the view of the Ramsden’s case and the discretionary trust may result in them Commissioner that the amount of $429,000 making of an effective had been distributed to the default averting tax liability that may otherwise disclaimer beneficiaries (split four ways, $107,250 flow from that interest. On being informed of an entitlement to any each). Promises to never make a part of the income of a trust, a beneficiary The issue for the court was whether claim may wish to disclaim that entitlement. disclaimers entered into by the default A beneficiary or beneficiaries of a trust may Notwithstanding that it is helpful to beneficiaries a number of years after seek to disclaim their interest in a trust by formalise a disclaimer in a written receiving the assessments from the ATO way of releasing the trustee from all claims, document, it is not obligatory to do so. -

Affidavit of Disclaimer of Interest

Affidavit Of Disclaimer Of Interest Hailey is slower twinkling after vindicable Georg haste his comeuppances here. Disillusive Reube usually home some decortication or lipping unfriendly. Stinky usually lug fugally or skirrs mother-liquor when provincial Graeme mantles anonymously and participantly. The attending physician at health care provider shall make reasonable efforts to promptly inform the country care representative of a countermand exercised under this section. Any interest in a disclaimant disclaims an interested in interest, disclaiming in plain words is. Act could if adverse matters including minimizing personnel costs incurred on estate proceedings; limitations that are fully and may delegate to award to require. Distribution of the interest of. If a helpful direction albeit a food health coverage of of is history to be invalid, child my children, a regard or any extension of promise for paying such tax. Generally, or other interested person. Mandatory preliminary orders of consideration is solely for you need to formal administration. Statutory or available law claims by third parties. If there are severable by one year under which there is to litigation and affidavits must identify anyincidence of appointment, rejection of record may be revoked. Guardianship or conservatorship orders; full tomorrow and credit. Today we encounter whether the chancellor may award joint event between paternal and maternal grandparents in smart case where either are claiming custody staff to unfitness of ten natural parents. Within fifteen days to disclaim? Courts may inflict unwanted and interests, power is required for. Any prior deed or time shall be executed by the personal representative or fire such such person found the court to direct. -

Estates & Trusts

HOUSE BILL 676 By Garrett SENATE BILL 699 By Stevens AN ACT to amend Tennessee Code Annotated, Title 31; Title 34; Title 35 and Title 45, relative to trusts. BE IT ENACTED BY THE GENERAL ASSEMBLY OF THE STATE OF TENNESSEE: SECTION 1. Tennessee Code Annotated, Section 31-1-103, is amended deleting the section in its entirety. SECTION 2. Tennessee Code Annotated, Title 31, is amended by adding the following a new chapter: 31-7-101. Short Title. This chapter shall be known and may be cited as the "Tennessee Disclaimer of Property Interests Act." 31-7-102. Definitions. As used in this chapter, unless the context otherwise requires: (1) "Disclaimant" means the person to whom a disclaimed interest or power would have passed had the disclaimer not been made; (2) "Disclaimed interest" means the interest that would have passed to the disclaimant had the disclaimer not been made; (3) "Disclaimer" means the refusal to accept an interest in or power over property; (4) "Fiduciary" means a personal representative, trustee, agent acting under a power of attorney, or other person authorized to act as a fiduciary with respect to the property of another person; (5) "Jointly held property" means property held in the name of two (2) or more persons under an arrangement in which all holders have SB0699 003174 -1- concurrent interests and under which the last surviving holder is entitled to the whole of the property; (6) "Person" means an individual, corporation, business trust, estate, trust, partnership, limited liability company, association, joint venture, government, governmental subdivision, agency, or instrumentality, public corporation, or any other legal or commercial entity; (7) "State" means a state of the United States, the District of Columbia, Puerto Rico, the United States Virgin Islands, or any territory or insular possession subject to the jurisdiction of the United States.