9.0International Gateways

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Patrick Port Botany Terminal, December 2017

Community Feedback Report Port Botany Terminal Patrick HSE Management System Operation Environmental Management Plan Courtesy of Bob Wood - Patrick Port Botany Terminal, December 2017 Report No. PBT_HSE_PLN_11_01_v02 Date Issued: 5 July 2019 CommunityPort Feedback Botany Report Terminal Operation Environmental Management Plan (OEMP) Community Feedback Report DOCUMENT CONTROL Document control shall be in accordance with Patrick’s corporate PAT_HSE_PRO_14_014 Document Management Procedure, ensuring: • The Operation Environmental Management Plan (OEMP or Operation EMP) is maintained and up to date; • The current version of the OEMP is readily available to managers, employees and key stakeholders; and • A copy of the OEMP is retained for a minimum of seven years. Listed below are the four most recent issues for this document. Document History Version Page Issue Date Description of Amendment(s) Prepared By Approved By No. No. 0.7 All 3-Mar-15 Additional edits following DPE comment. A Robinson S Jones 0.8 All 29-Mar-19 Update to new template. Formal Review Marie Gibbs Bruce Guy (draft) conducted as per Condition of Consent 6.5 and includes changes to procedures and practices since the previous review. Issued to NSW Ports for review. 1 All 7-Jun-19 Final revision reissued to DPE. Marie Gibbs Bruce Guy 2 Section 5-Jul-19 Updated with further details related to Marie Gibbs Bruce Guy 6.12 unpacking (opening) a container. A person using Patrick’s documents or data accepts the risk of: • Using the documents or data in electronic form without requesting and checking them for accuracy against the original hard copy version; and • Using the documents or data for any purpose not agreed to in writing by Patrick. -

Sydney Gateway

Sydney Gateway State Significant Infrastructure Scoping Report BLANK PAGE Sydney Gateway road project State Significant Infrastructure Scoping Report Roads and Maritime Services | November 2018 Prepared by the Gateway to Sydney Joint Venture (WSP Australia Pty Limited and GHD Pty Ltd) and Roads and Maritime Services Copyright: The concepts and information contained in this document are the property of NSW Roads and Maritime Services. Use or copying of this document in whole or in part without the written permission of NSW Roads and Maritime Services constitutes an infringement of copyright. Document controls Approval and authorisation Title Sydney Gateway road project State Significant Infrastructure Scoping Report Accepted on behalf of NSW Fraser Leishman, Roads and Maritime Services Project Director, Sydney Gateway by: Signed: Dated: 16-11-18 Executive summary Overview Sydney Gateway is part of a NSW and Australian Government initiative to improve road and freight rail transport through the important economic gateways of Sydney Airport and Port Botany. Sydney Gateway is comprised of two projects: · Sydney Gateway road project (the project) · Port Botany Rail Duplication – to duplicate a three kilometre section of the Port Botany freight rail line. NSW Roads and Maritime Services (Roads and Maritime) and Sydney Airport Corporation Limited propose to build the Sydney Gateway road project, to provide new direct high capacity road connections linking the Sydney motorway network with Sydney Kingsford Smith Airport (Sydney Airport). The location of Sydney Gateway, including the project, is shown on Figure 1.1. Roads and Maritime has formed the view that the project is likely to significantly affect the environment. On this basis, the project is declared to be State significant infrastructure under Division 5.2 of the NSW Environmental Planning & Assessment Act 1979 (EP&A Act), and needs approval from the NSW Minister for Planning. -

NSW Freight and Ports Plan 2018-2023

NSW Freight and Ports Plan 2018-2023 September 2018 Contents Message from the Ministers 4 Executive Summary – A Plan For Action 2018-2023 6 What the Plan will achieve over the next five years 6 Objective 1: Economic growth 7 Objective 2: Efficiency, connectivity and access 8 Objective 3: Capacity 9 Objective 4: Safety 10 Objective 5: Sustainability 11 Part 1 – Introduction 13 About this Plan 13 Part 2 – Context: The State Of Freight 17 About this chapter 17 The NSW freight and ports sector at glance 17 Greater Sydney production and freight movements 26 The Greater Sydney freight network 28 Regional NSW production and freight movements 36 The regional freight network 39 Part 3 – How We Will Respond To Challenges And Opportunities 45 About this chapter 45 The five objectives 45 Objective 1: Economic growth 47 Objective 2: Efficiency, connectivity and access 51 Objective 3: Capacity 62 Objective 4: Safety 70 Objective 5: Sustainability 73 Part 4 - Implementation Plan 77 Appendix 78 Message from the Ministers The freight industry is the lifeblood of the • Deliver more than $5 billion in committed NSW economy – worth $66 billion to our key infrastructure projects for freight in State economy. From big businesses to NSW. These include $543 million towards farmers, retailers to consumers, we all rely Fixing Country Roads, $400 million on our goods getting to us in a safe and towards Fixing Country Rail, $15 million efficient manner. towards the Fixing Country Rail pilot, $21.5 million towards the Main West rail line, The NSW Freight and Ports Strategy $500 million towards the Sydney Airport released in 2013 was the first long-term Road upgrade, $400 million towards Port freight vision to be produced for NSW, Botany Rail Line duplication, $1171 million which drove targeted investment in both towards the Coffs Harbour Bypass and metropolitan and regional transport $2.2-$2.6 billion towards Sydney Gateway. -

Port Botany Expansion June 2003 Prepared for Sydney Ports Corporation

Port Botany Expansion June 2003 Prepared for Sydney Ports Corporation Visual Impact Assessment Architectus Sydney Pty Ltd ABN 11 098 489 448 41 McLaren Street North Sydney NSW 2060 Australia T 61 2 9929 0522 F 61 2 9959 5765 [email protected] www.architectus.com.au Cover image: Aerial view of the existing Patrick Terminal and P&O Ports Terminal looking south east. Contents 1 Introduction 5 2 Methodology 5 3 Assessment criteria 6 3.1 Visibility 6 3.2 Visual absorption capacity 7 3.3 Visual Impact Rating 8 4 Location 9 5 Existing visual environment 10 5.1 Land form 10 5.2 Land use 10 5.3 Significant open space 11 5.4 Botany Bay 12 5.5 Viewing zones 13 6 Description of the Proposal 28 6.1 New terminal 28 6.2 Public Recreation & Ecological Plan 32 7 Visual impact assessment 33 7.1 Visual impact on views in the immediate vicinity 33 7.2 Visual impact on local views 44 7.3 Visual impact on regional views 49 7.4 Visual impact aerial views 59 7.5 Visual impact on views from the water 65 7.6 Visual impact during construction 74 8 Mitigation measures 75 9 Conclusion 78 Quality Assurance Reviewed by …………………………. Michael Harrison Director Urban Design and Planning Architectus Sydney Pty Ltd …………………………. Date This document is for discussion purposes only unless signed. 7300\08\12\DGS30314\Draft.22 Port Botany Expansion EIS Visual Impact Assessment Figures Figure 1. Location of Port Botany 9 Figure 2. Residential areas surrounding Port Botany 10 Figure 3. -

Existing Port Facilities CHAPTER 3

Existing Port Facilities CHAPTER 3 Summary of key outcomes: Sydney’s ports provide a vital economic gateway for the Australian and NSW economies. In 2001/02, Sydney’s ports handled approximately $42 billion worth of international trade which represents 17% of Australia’s total international trade and 56% of NSW’s international air and sea cargo trade by value. Due to its proximity to the Sydney market, Port Botany is and will remain the primary port for the import and export of containerised cargo in NSW. Currently, over 90% of container trade passing through Sydney’s ports is handled at Port Botany. Port Botany Expansion Environmental Impact Statement – Volume 1 Existing Port Facilities CHAPTER 3 3 Existing Port Facilities 3.1 Role and Significance of Sydney’s Ports The port facilities of Sydney are located at Port Botany and within Sydney Harbour. These ports, along with the airport, are the economic gateways to NSW. This is reflected by the fact that in 2001/02 Sydney’s ports handled approximately $42 billion worth of international trade. This represents: $10,000 for each person in the greater Sydney region, which has a population of close to 4 million; 56% of NSW’s total international air and sea cargo trade by value; and 17% of Australia’s total international trade. Cargo throughput through Sydney’s ports (Sydney Ports Corporation owned and private berths) during 2001/02 was 24.3 million mass tonnes, with containerised cargo accounting for 43.9%. This trade comprised more than 1 million TEUs, 183,000 motor vehicles and about 13.6 million mass tonnes of bulk and general cargo. -

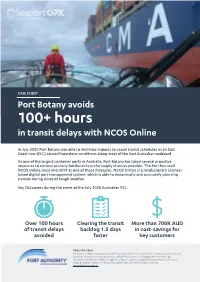

Port Botany Avoids 100+ Hours in Transit Delays with NCOS Online

CASE STUDY Port Botany avoids 100+ hours in transit delays with NCOS Online In July 2020 Port Botany was able to minimize impacts to vessel transit schedules as an East Coast Low (ECL) caused hazardous conditions along most of the East Australian seaboard. As one of the largest container ports in Australia, Port Botany has taken several proactive measures to remove as many bottlenecks in the supply chain as possible. The Port has used NCOS Online since mid-2019 as one of these measures. NCOS Online is a revolutionary science- based digital port management system, which is able to dynamically and accurately plan ship transits during times of rough weather. Key Outcomes during the event of the July 2020 Australian ECL: Over 100 hours Clearing the transit More than 700K AUD of transit delays backlog 1.5 days in cost-savings for avoided faster key customers About the Client Port Botany is a deep-water seaport located in Botany Bay, Sydney. It is one of Australia’s largest container ports and specialises in trade in manufactured products and bulk liquid imports including petroleum and natural gas. Port Authority of New South Wales manages the navigation, security and operational safety needs of commercial shipping in Sydney Harbour, Port Botany, Newcastle Harbour, Port Kembla, Eden and Yamba. portauthoritynsw.com.au East Coast Lows Common during winter months, east coast lows (ECL) are one of the most dangerous weather systems to affect Australia’s east coast. These low- pressure systems have relatively long lifecycles, typically about a week, and can produce gale to storm-force winds, heavy widespread rainfall, and very rough seas and prolonged heavy swells. -

Draft Greater Sydney Region Plan

OUR GREATER SYDNEY 2056 A metropolis of three cities – connecting people DRAFT Greater Sydney Region Plan October 2017 How to be involved The draftGreater Sydney Region Plan sets out a vision, Before making a submission, please read the Privacy objectives, strategies and actions for a metropolis of three Statement at www.greater.sydney/privacy. If you provide cities across Greater Sydney. It is on formal public exhibition a submission in relation to this document using any of the until 15 December 2017. above addresses, you will be taken to have accepted the Privacy Statement. You can read the entire draft Plan atwww.greater.sydney Please note that all submissions and comments will be You can make a submission: treated as public and will be published in a variety of by visiting www.greater.sydney/submissions mediums. If you would like to make a submission without by emailing [email protected] it being made public or if you have any questions about the application of the Commission’s privacy policy, please by post to: contact the Commission directly on 1800 617 681 or Greater Sydney Commission [email protected] Draft Greater Sydney Region Plan PO BOX 257 Parramatta NSW 2124 Greater Sydney Commission | Draft Greater Sydney Region Plan 2017 3 A metropolis of three cities will transform land use and transport patterns and boost Greater Sydney’s liveability, productivity and sustainability by spreading the benefits of growth to all its residents. Chief Commissioner Lucy Hughes Turnbull AO I am delighted to present the Greater take the pressure off housing affordability Sydney Commission’s first draft regional and maintain and enhance our plan to the people of Greater Sydney and natural resources. -

Northern Sydney Freight Corridor

Northern Sydney Freight Corridor Scoping Phase Completion Report Document information Scoping Phase Completion Report - final for publishing 13 Feb Document No. 2012.doc Revisions Revision 1 Draft 30/01/2012 Revision 2 Final 09/02/2012 Northern Sydney Freight Corridor Program Scoping Phase Completion Report Contents Background ............................................................................................................................................. 1 1 Introduction ............................................................................................................................. 2 1.1 Northern Sydney Freight Corridor ............................................................................. 2 1.2 Need for the NSFC Program ..................................................................................... 5 1.3 NSFC Program scoping phase .................................................................................. 6 1.3.1 Functional scope definition ......................................................................... 7 1.3.2 Options development ................................................................................. 8 1.3.3 Options assessment ................................................................................... 9 1.4 Preferred projects ....................................................................................................10 1.4.1 Future options & alternatives ...................................................................11 2 Options overview and assessment -

BOTANY RAIL DUPLICATION OCTOBER 2019 Contents

GUIDE TO THE ENVIRONMENTAL IMPACT STATEMENT BOTANY RAIL DUPLICATION OCTOBER 2019 Contents About the Botany Rail Duplication Project About this document and ARTC 3 About Botany Rail Duplication 4 Strategic context – Planning for the future NSW Freight and Ports Plan 2018 – 2023 6 Navigating the Future, NSW Ports’ 30 year Master Plan Planning and consultation What is an Environmental Impact Statement? 7 Consultation inputs to the EIS 8 Construction of the project Design and construction methodology 9 Indicative construction program 10 Construction compounds 11 Our environment Traffic, transport and access 12 Noise and vibration 13 Heritage 15 Summary of other key environmental 16 assessments Next steps Make a submission 19 Submissions to the NSW Department of Planning, Industry and Environment should be made on the Environmental Impact Statement (EIS) and not this document, which provides a guide to the EIS only. 2 | October 2019 | Guide to the Environmental Impact Statement | ARTC In May 2018 the Australian Government announced a funding commitment to duplicate the remaining section of single line track between Mascot and Botany, known as the Botany Rail Duplication project. Efficient access to and from Port Botany is critical to the economic growth and prosperity of Sydney. About this document How were the impacts assessed? Following consultation with the community, businesses and stakeholders and detailed environmental investigations an The EIS was prepared through initial community Environmental Impact Statement (EIS) for the project has and stakeholder consultation and detailed specialist been prepared. The Department of Planning, Industry and assessment of key environmental issues, including Environment (DPIE) has placed the Botany Rail Duplication field surveys, data analysis and predictive modelling Project EIS on public exhibition and is inviting submissions. -

Western Sydney Freight Line Corridor – Draft

TRANSPORT FOR NSW FEBRUARY 2018 SENSITIVE: NSW GOVERNMENT DRAFT WESTERN SYDNEY FREIGHT LINE CORRIDOR DRAFT STRATEGIC ENVIRONMENTAL ASSESSMENT Draft Western Sydney Freight Line Corridor Draft Strategic Environmental Assessment Transport for NSW WSP Level 27, 680 George Street Sydney NSW 2000 GPO Box 5394 Sydney NSW 2001 Tel: +61 2 9272 5100 Fax: +61 2 9272 5101 wsp.com REV DATE DETAILS A 16/02/2018 Final draft for consultation NAME DATE SIGNATURE Morgan Cardiff; Prepared by: 16/02/2018 Ron dela Pena Reviewed by: Emma Dean 16/02/2018 Approved by: Paul Greenhalgh 16/02/2018 This document may contain confidential and legally privileged information, neither of which are intended to be waived, and must be used only for its intended purpose. Any unauthorised copying, dissemination or use in any form or by any means other than by the addressee, is strictly prohibited. If you have received this document in error or by any means other than as authorised addressee, please notify us immediately and we will arrange for its return to us. 2270947A-ENV-REP-002 RevA Sensitive: NSW Government February 2018 TABLE OF GLOSSARY, ABBREVIATIONS AND KEY TERMS .................. IX CONTENTS EXECUTIVE SUMMARY ................................................................ XI 1 INTRODUCTION ................................................................... 1 1.1 BACKGROUND .......................................................................... 1 1.2 KEY TRANSPORT CORRIDORS OF WESTERN SYDNEY ..................................................................................... -

Urban Freight Intermodal Transport: an Analogue Theory Using Electrical Circuits

Urban Freight Intermodal Transport: An Analogue Theory Using Electrical Circuits Paul Charles Beavis A thesis submitted in fulfillment of the requirement for the degree of Doctor of Philosophy School of Civil and Environmental Engineering University of New South Wales Sydney, Australia Urban Freight Intermodal Transport: An Analogue Theory Using Electrical Circuits Abstract Container Seaports co-located with populations in Australian cities generate and attract inexorable, increasing discrete- diffuse flows which lead to landside access constraints and conflicts. Network models in freight transport are deficient in addressing demand management initiatives to ecologically re-structure the landside container freight task. Conventional freight planning stages road building and port expansion to facilitate mobility and container storage, and a vicious, inefficient cycle ensues. The miss-specification of modelling and planning frameworks is due to a conceptualisation of node impedance as a constraint phenomenon rather than as a necessary measure of precision. This thesis pioneers an activity-based approach to theoretically support investigations towards the adoption of urban freight intermodalism. A necessary signature of true transhipment- consolidation network formulations is the capture of service generation and inter-temporal storage mechanisms. Intermodal terminals offer a means to retrofit existing road-rail networks so that modes interface and deliver consolidation and accessibility outcomes. The essences captured are the changing value proposition and precision relations necessary to harmonise terminal complex activity with rail operating forms. Analytical relations are proposed using electrical circuit and process control theories to represent impedance relations based on new flux variables and sparse system parameters. This transhipment calculus allows for precision specifications to be measured according to novel “Figures of Merit” which assess storage-handling and throughput trade-offs. -

NSW Implementation of the National Freight and Supply Chain Strategy and National Action Plan

NSW Implementation of the National Freight and Supply Chain Strategy and National Action Plan November 2019 1 National Critical Area 1: Smarter and targeted infrastructure investment National Action 1.1: Ensure that domestic and international supply chains are serviced by resilient and efficient key freight corridors, precincts and assets Committed/ Initiative Freight and Ports Plan Goal Freight and Ports Plan Initiatives for Timeframe type investigation Port Botany Rail Line Duplication. Through Australian Government funding, duplicate the final three Deliver new infrastructure to kilometres of Port Botany Rail Line, which will allow Immediate increase rail freight capacity freight to be more reliably transported by rail to Infrastructure Committed 0-2 years Initiative ID 31063 metropolitan intermodal terminals from regional intermodal terminals to port (subject to Final Business Case, 3-5 years) Amplification of the Southern Sydney Freight Line. Deliver new infrastructure to Construction of a passing loop at Cabramatta to Immediate increase rail freight capacity Infrastructure Committed support operations at Moorebank Intermodal Terminal 0-2 years Initiative ID 31064 (Subject to Final Business Case, 3-5 years) Outer Sydney Orbital. Freight rail line and motorway Deliver new infrastructure to linking the North West and South West Growth Areas, Medium term increase rail freight capacity connecting with the Western Sydney Airport Growth Infrastructure Committed 5-10 years Initiative ID 31066 Area and future employment lands (10+ years, corridor identified). Western Sydney Freight Line. Freight rail connections to serve the Western Sydney Airport Growth Area; Deliver new infrastructure to connect Port Botany to Western Sydney and Western For Medium term increase rail freight capacity NSW via the Southern Sydney Freight Line; and Infrastructure investigation 5-10 years Initiative ID 31068 support the movement of container and bulk freight by rail across Greater Sydney (10+ years, corridor protection progressing now).