Proshares Trust Ii Prospectus S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

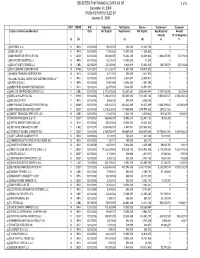

SELECTED FCM FINANCIAL DATA AS of December 31, 2008 FROM

SELECTED FCM FINANCIAL DATA AS OF 1 of 5 December 31, 2008 FROM REPORTS FILED BY January 31, 2009 B/D? DSRO A/O Adjusted Net Capital Excess Customers' Customer Futures Commission Merchant Date Net Capital Requirement Net Capital Seg Required Amount 4d(a)(2) Pt. 30 Required (a) (b) (c) (d) (e) (f) 1 3D FOREX, LLC N NFA 12/31/2008 18,931,722 500,000 18,431,722 0 0 2 ACM USA LLC N NFA 12/31/2008 11,575,482 10,000,000 1,575,482 0 0 3 ADM INVESTOR SERVICES INC N CBOT 12/31/2008 154,941,097 74,632,265 80,308,832 1,864,327,056 72,071,646 4 ADVANCED MARKETS LLC N NFA 12/31/2008 10,071,373 10,000,000 71,373 0 0 5 ADVANTAGE FUTURES LLC N CME 12/31/2008 25,081,866 6,446,918 18,634,948 188,738,579 32,311,026 6 AIG CLEARING CORPORATION N NYME 12/31/2008 321,823,187 11,903,795 309,919,392 0 0 7 ALARON TRADING CORPORATION N NFA 12/31/2008 3,711,574 500,000 3,211,574 0 0 8 ALLIANZ GLOBAL INVESTORS DISTRIBUTORS LLC * Y NFA 12/31/2008 27,457,078 6,847,647 20,609,431 0 0 9 ALPARI (US) LLC N NFA 12/31/2008 17,497,095 10,000,000 7,497,095 0 0 10 AMERIPRISE ADVISOR SERVICES INC Y NFA 12/31/2008 22,077,618 5,346,567 16,731,051 0 0 11 BANC OF AMERICA SECURITIES LLC Y CME 12/31/2008 3,171,801,285 166,357,841 3,005,443,444 1,007,978,026 16,837,469 12 BARCLAYS CAPITAL INC Y NYME 12/31/2008 7,878,067,153 500,000,000 7,378,067,153 5,993,650,575 2,976,258,742 13 BGC SECURITIES Y NFA 12/31/2008 8,855,236 500,000 8,355,236 0 0 14 BNP PARIBAS COMMODITY FUTURES INC N NYME 12/31/2008 322,615,874 242,242,565 80,373,309 2,668,759,643 445,566,495 15 BNP PARIBAS SECURITIES -

Page 01 Nov 25.Indd

ISO 9001:2008 CERTIFIED NEWSPAPER Sunday 25 November 2012 11 Muharram 1434 - Volume 17 Number 5529 Price: QR2 Al Sada opens Cook and CNG fuelling Pietersen station defy India Business | 21 Sport | 32 www.thepeninsulaqatar.com [email protected] | [email protected] Editorial: 4455 7741 | Advertising: 4455 7837 / 4455 7780 Khalfan trains guns on Aljazeera Kenyan arrested over Dubai police chief accuses channel of ignoring protests in Egypt murder of US woman DOHA: Known for Brotherhood- DOHA: The law-enforcement Al Sharq briefly reported yes- bashing, outspoken Dubai Police agencies here have arrested terday that an ‘African national’ Chief, Dahi Khalfan, has now a Kenyan security guard sus- suspected of killing an ‘expatri- aimed his guns at Aljazeera pected of killing an American ate’ last week had been taken TV Channel and criticised it woman who was teaching at a into custody and that he had severely for what he claimed school in Al Wakra, US-based confessed to the crime. was the Channel turning a blind newspaper, The Morning Call, Jennifer, according to The eye to Friday’s protests against reported yesterday. Morning Call, had been teach- President Mohammed Mursi in The newspaper identified ing pre-school children in her Egypt. the victim as Jennifer Brown, Al Wakra school since last Khalfan said he had lost trust a 40-year-old woman from Jim September. in Aljazeera and called on fellow Thorpe, a borough in Carbon “She was a good kid, a beauti- GCC nationals to boycott the County, Pennsylvania, and said ful girl,” her father was quoted popular Arabic Channel. -

Financial Technology Sector Summary

Financial Technology Sector Summary February 11, 2016 Financial Technology Sector Summary Financial Technology Sector Summary Table of Contents I. GCA Savvian Overview II. Market Summary III. Payments / Banking IV. Securities / Capital Markets / Data & Analytics V. Healthcare / Insurance 2 Financial Technology Sector Summary I. GCA Savvian Overview 3 Financial Technology Sector Summary GCA Savvian Overview Independent Investment Bank Focused on Growth Sectors of the Global Economy » Leading provider of mergers and acquisitions, 7+ AREAS OF INDUSTRY EXPERTISE private capital agency and capital markets advisory services, and private funds services Financial Technology Business & Tech Enabled Services » Headquarters in San Francisco and offices in Media & Digital Media Industrial Technology New York, London, Tokyo, Osaka, Singapore, Telecommunications Healthcare Mumbai, and Shanghai » Majority of U.S. senior bankers previously with Goldman Sachs, Morgan Stanley, Robertson Stephens, and JPMorgan 100+ CROSS - BORDER TRANSACTIONS » Senior level attention and focus, extensive transaction experience and deep domain insight 20+ REPRESENTATIVE COUNTRIES » Focused on providing strategic advice for our clients’ long-term success 580+ CLOSED TRANSACTIONS » 225+ investment banking professionals $145BN+ OF TRANSACTION VALUE 4 Financial Technology Sector Summary GCA Savvian Overview Financial Technology Landscape » GCA Savvian divides Financial Technology Financial Technology into three broad categories − Payments & Banking − Securities & Capital Markets -

A Non-Linear Analysis of Operational Risk and Operational Risk Management in Banking Industry

University of Wollongong Research Online University of Wollongong Thesis Collection 2017+ University of Wollongong Thesis Collections 2017 A non-linear analysis of operational risk and operational risk management in banking industry Yifei Li University of Wollongong Follow this and additional works at: https://ro.uow.edu.au/theses1 University of Wollongong Copyright Warning You may print or download ONE copy of this document for the purpose of your own research or study. The University does not authorise you to copy, communicate or otherwise make available electronically to any other person any copyright material contained on this site. You are reminded of the following: This work is copyright. Apart from any use permitted under the Copyright Act 1968, no part of this work may be reproduced by any process, nor may any other exclusive right be exercised, without the permission of the author. Copyright owners are entitled to take legal action against persons who infringe their copyright. A reproduction of material that is protected by copyright may be a copyright infringement. A court may impose penalties and award damages in relation to offences and infringements relating to copyright material. Higher penalties may apply, and higher damages may be awarded, for offences and infringements involving the conversion of material into digital or electronic form. Unless otherwise indicated, the views expressed in this thesis are those of the author and do not necessarily represent the views of the University of Wollongong. Recommended Citation Li, Yifei, A non-linear analysis of operational risk and operational risk management in banking industry, Doctor of Philosophy thesis, School of Accounting, Economics and Finance, University of Wollongong, 2017. -

Banking Litigation Law Review Banking Litigation Law Review

the Banking Litigation Law Review Law Litigation Banking Banking Litigation Law Review Fourth Edition Editor Deborah Finkler Fourth Edition Fourth lawreviews © 2020 Law Business Research Ltd Banking Litigation Law Review Fourth Edition Reproduced with permission from Law Business Research Ltd This article was first published in December 2020 For further information please contact [email protected] Editor Deborah Finkler lawreviews © 2020 Law Business Research Ltd PUBLISHER Tom Barnes SENIOR BUSINESS DEVELOPMENT MANAGER Nick Barette BUSINESS DEVELOPMENT MANAGER Joel Woods SENIOR ACCOUNT MANAGERS Pere Aspinall, Jack Bagnall ACCOUNT MANAGERS Olivia Budd, Katie Hodgetts, Reece Whelan PRODUCT MARKETING EXECUTIVE Rebecca Mogridge RESEARCH LEAD Kieran Hansen EDITORIAL COORDINATOR Tommy Lawson PRODUCTION AND OPERATIONS DIRECTOR Adam Myers PRODUCTION EDITOR Felicia Rosas SUBEDITOR Martin Roach CHIEF EXECUTIVE OFFICER Nick Brailey Published in the United Kingdom by Law Business Research Ltd, London Meridian House, 34–35 Farringdon Street, London, EC4A 4HL, UK © 2020 Law Business Research Ltd www.TheLawReviews.co.uk No photocopying: copyright licences do not apply. The information provided in this publication is general and may not apply in a specific situation, nor does it necessarily represent the views of authors’ firms or their clients. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts or omissions contained herein. Although -

Public Warnings - Securities Dealers

Public Warnings - Securities Dealers The Data as of September 7, 2018 Country No. forwarding Name Address warnings Reason Detailed information 1911DIRECT Sparkasse Ekonomisk Box 882, 114 79 Stockholm, Sverige, Klarabergsviadukten Sweden unauthorized subject www.fi.se/warning Forening 70/Kungsbron, 107 24 Stockoholm, Sverige, Finduras 1 Group/European Bransch, Carrer de Porto Pi 8/8, 070 15 Palma de Mallorca, Baleares/Espana 1st American Securities 632 Broadway, Suite 3002, Neww York NY 10012, USA Sweden unauthorized subject www.fi.se 7/D Tung Wai Commercial Building, 109-111 Glocester 2 Road, Wan Chai, Hong Kong www. 1stamericansecurities.com www.kerstdis.nl 2013 BEST INVEST 59 Thomas Street, Manchester M4 1NA, United Kingdom United unauthorized subject www.fsa.gov.uk 3 www.2013bestinvest.com Kingdom 4 247 Holdings Group Great Britain Italy unauthorized subject 5 4usignals.com http://4usignals.com Cyprus unauthorized subjec www.cysec.gov.cy 4XCELLENT Ltd with headquarters in Cyprus, Great Britain and Israel, Italy unauthorized subject http://www.consob.it/mainen/ 6 www.4xcellent.com. index.html 7 629 Plan France unauthorized subject Phone +33(0)1 5345 6031 8 7M MANAGEMENT SERVICES Ltd. Greece unauthorized subject tel.no. +30 210 33 77 100 A WALKER ASSOCIATES / ANDREW www.awalkerassociates.com United unauthorized subject www.fsa.gov.uk 9 WALKER ASSOCIATES / AW Kingdom ASSOCIATES A WARNER ASSOCIATES / ANDREW www.awarnerassociates.com United unauthorized subject www.fsa.gov.uk 10 WARNER ASSOCIATES / AW Kingdom ASSOCIATES 11 A.S. Konstantinidis Greece unauthorized subject www.hcmc.gr 12 AB Hutton Global Holdings www.abhglobal.com Cyprus unauthorized subject www.cysec.gov.cy Abacus Financial Management www.abacusfinancialmgmt.com United unauthorized subject www.fsa.gov.uk 13 Telephone: 0207 193 9451 Kingdom Clone of previously FSA authorised firm Public Warnings - Securities Dealers The Data as of September 7, 2018 Country No. -

Banking Litigation Law Review Banking Litigation Law Review

the Banking Litigation Law Review Law Litigation Banking Banking Litigation Law Review Third Edition Editor Deborah Finkler Third Edition Third lawreviews © 2019 Law Business Research Ltd Banking Litigation Law Review Third Edition Reproduced with permission from Law Business Research Ltd This article was first published in December 2019 For further information please contact [email protected] Editor Deborah Finkler lawreviews © 2019 Law Business Research Ltd PUBLISHER Tom Barnes SENIOR BUSINESS DEVELOPMENT MANAGER Nick Barette BUSINESS DEVELOPMENT MANAGER Joel Woods SENIOR ACCOUNT MANAGERS Pere Aspinall, Jack Bagnall ACCOUNT MANAGERS Olivia Budd, Katie Hodgetts, Reece Whelan PRODUCT MARKETING EXECUTIVE Rebecca Mogridge RESEARCH LEAD Kieran Hansen EDITORIAL COORDINATOR Gavin Jordan HEAD OF PRODUCTION Adam Myers PRODUCTION EDITOR Hilary Scott SUBEDITOR Caroline Herbert CHIEF EXECUTIVE OFFICER Nick Brailey Published in the United Kingdom by Law Business Research Ltd, London Meridian House, 34-35 Farringdon Street, London, EC4A 4HL, UK © 2019 Law Business Research Ltd www.TheLawReviews.co.uk No photocopying: copyright licences do not apply. The information provided in this publication is general and may not apply in a specific situation, nor does it necessarily represent the views of authors’ firms or their clients. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts or omissions contained herein. Although the information -

Testing for Arbitrage Opportunities Within the Foreign Exchange Market

TESTING FOR ARBITRAGE OPPORTUNITIES WITHIN THE FOREIGN EXCHANGE MARKET TESTIG FOR ARBITRAGE OPPORTUITIES WITHI THE FOREIG EXCHAGE MARKET Imran Hussain An Independent Study Presented to The Graduate School of Bangkok University In Partial Fulfillment Of the Requirement for the Degree Master of Business Administration 2009 © 2009 Imran Hussain All Right Reserved Hussain, Imran. Master of Business Administration, June 2009, Graduate School, Bangkok University Testing For Arbitrage Opportunities within the Foreign Exchange Market (51 pp.) Advisor of Independent Study: Andrew R. Criswell, Ph.D. ABSTRACT This study aims to determine whether or not arbitrage opportunities exist within the retail foreign exchange market and how the number of opportunities compares to those found within the interbank foreign exchange market. The concept of triangular arbitrage is used within this study to identify potential arbitrage opportunities. This study makes use of minute frequency data obtained from a retail foreign exchange broker involving the US dollar, Euro and Japanese Yen. This study covers a one week period from 4th to the 10th of April 2009, over which arbitrage opportunities are tested for using the triangular arbitrage trade strategy. This study also tested to see if triangular parity is a good predictor of future currency movement. This study finds that some arbitrage opportunities do exist within the retail foreign exchange market, however the returns of these opportunities suggests that the retail foreign exchange market falls in line with the efficient market hypothesis. This study finds that arbitrage opportunities in the form of triangular arbitrage are more common within the interbank market than the retail market. This study also finds that triangular parity is not a good predictor of currency movement. -

Metatrader 5’S Introduction, Brokers Still by Damian Chmiel Prefer Metatrader 4

Is MetaQuotes Its Own Worst Enemy? Nine Years after MetaTrader 5’s Introduction, Brokers Still By Damian Chmiel Prefer MetaTrader 4 Trading platforms designed by MetaQuotes Due to the unwavering popularity of Meta- which still looks more appealing to traders. On are definitely the most recognized and well- Trader 4, the supplier of the most popular top of that, big brokers that were so far avoiding known within the retail trading industry. If investment software on the market has been MT4 and promoting their own software finally we asked the average trader which platforms struggling with trying to increase the usage had to surrender and introduce their com- they use for trading, most of them would rates of MetaTrader 5 for years. As it turns out, petitor’s software to their clients. This unusual B2Broker of confirm at least occasional contact with one some brokers who already upgraded to MT5, turnaround led Finance Magnates to seek for CEO – of the MetaTrader versions. have decided to return to the “good ol’” solution, the answers to this surprising phenomenon. Azizov 52 Arthur MetaQuotes, originally from Russia and Main Differences between MetaTrader 4 and MetaTrader 5 today based in Cyprus, was established in 2000 with the launch of FX Charts, which Arthur Azizov, Fig. 23 CEO of B2Broker MetaTrader 4 MetaTrader 5 was renamed as MetaQuotes just a year later. Trading instruments FX and CFDs FX, CFDs, futures, and stocks The real breakthrough came however in the Timeframes 9 21 middle of the last decade when Metatrader Pending orders 4 types (buy stop, buy limit, sell limit, sell stop) 6 types (additionally buy stop-limit, sell-stop limit) 4 (MT4) was finally released. -

Project Finance in Practice: Case Studies

Project Finance in Practice Case Studies i Project Finance in Practice Case Studies Carmel de Nahlik and Chris Jackson E U R B O O M O O K N S E Y Published by Euromoney Institutional Investor PLC Nestor House, Playhouse Yard London EC4V 5EX United Kingdom Tel: +44 (0)20 7779 8999 or USA 11 800 437 9997 Fax: +44 (0)20 7779 8300 www.euromoneybooks.com E-mail: [email protected] Copyright © 2014 Euromoney Institutional Investor PLC ISBN 978 1 78137 263 0 This publication is not included in the CLA Licence and must not be copied without the permission of the publisher. All rights reserved. No part of this publication may be reproduced or used in any form (graphic, electronic or mechanical, including photocopying, recording, taping or information storage and retrieval systems) without permission by the publisher. This publication is designed to provide accurate and authoritative information with regard to the subject matter covered. In the preparation of this book, every effort has been made to offer the most current, correct and clearly expressed information possible. The materials presented in this publication are for informational purposes only. They reflect the subjective views of authors and contributors and do not necessarily represent current or past practices or beliefs of any organisation. In this publication, none of the contributors, their past or present employers, the editor or the publisher is engaged in rendering accounting, business, financial, investment, legal, tax or other professional advice or services whatsoever and is not liable for any losses, financial or otherwise, associated with adopting any ideas, approaches or frameworks contained in this book. -

Derivative (Finance)

Derivative (finance) In finance, a derivative is a contract that derives its value mented as inverse. Hence, specifically the market price from the performance of an underlying entity. This un- risk of the underlying asset can be controlled in almost derlying entity can be an asset, index, or interest rate, every situation.[6] [1][2] and is often simply called the "underlying". Deriva- There are two groups of derivative contracts: the pri- tives can be used for a number of purposes, including vately traded over-the-counter (OTC) derivatives such as insuring against price movements (hedging), increasing swaps that do not go through an exchange or other inter- exposure to price movements for speculation or getting [3] mediary, and exchange-traded derivatives (ETD) that are access to otherwise hard-to-trade assets or markets. traded through specialized derivatives exchanges or other Some of the more common derivatives include forwards, exchanges. futures, options, swaps, and variations of these such as synthetic collateralized debt obligations and credit default Derivatives are more common in the modern era, but their swaps. Most derivatives are traded over-the-counter (off- origins trace back several centuries. One of the oldest exchange) or on an exchange such as the Bombay Stock derivatives is rice futures, which have been traded on the Exchange, while most insurance contracts have devel- Dojima Rice Exchange since the eighteenth century.[7] oped into a separate industry. Derivatives are one of the Derivatives are broadly categorized by the relationship three main categories of financial instruments, the other between the underlying asset and the derivative (such two being stocks (i.e., equities or shares) and debt (i.e., as forward, option, swap); the type of underlying as- bonds and mortgages). -

1167 Capital Llp 1875 Finance (Luxembourg) Sa 1Oak Capital Limited 2 Pm Europe S.A

Entidades Autorizadas por la CNMV Fuente: estafastrading.com para prestar servicios de inversión cnmv.es 1167 CAPITAL LLP 1875 FINANCE (LUXEMBOURG) SA 1OAK CAPITAL LIMITED 2 PM EUROPE S.A. 20TWENTY INDEPENDENT LIMITED 2H WEALTHCARE LLP 2R CAPITAL LIMITED 36 SOUTH CAPITAL ADVISORS LLP 360 F-INSIGHT LIMITED 360 TREASURY SYSTEMS AG 3D GLOBAL FINANCIAL SERVICES LTD 3I EUROPE PLC 3I INVESTMENTS PLC 4 SHIRES ASSET MANAGEMENT LTD 4 THE RECORD COMPLIANCE LTD 415 LLP 42 FINANCIAL SERVICES A.S. 4BIO VENTURES MANAGEMENT LTD 7DAYSAHEAD 7Q FINANCIAL SERVICES LTD 9STREET CAPITAL MARKETS B.V. A J WEALTH MANAGEMENT LTD A ALLEN INVESTMENT SERVICES LIMITED A CAT-COIN FINANCES E INVERSIONS, S.L. A D M INVESTOR SERVICES INTERNATIONAL LIMITED A G EDWARDS SONS (UK) LIMITED A J ASSET MANAGEMENT LIMITED A K JENSEN LIMITED AM FINANCIAL SERVICES LTD A.A.M. WEALTH LTD A.J.K. WEALTH MANAGEMENT LIMITED A.N. ALLNEW INVESTMENTS LTD A.T.I. ASSOCIATES (CYPRUS) LTD A/S GLOBAL RISK MANAGEMENT LTD. FONDSMAEGLERSELSKAB AA ADVISERS LLP AA ADVISORS EUROPE LIMITED AAA TRADE LTD AARON TOWNY MORTGAGES LIMITED AB SVENSK EXPORTKREDIT ABACCO NEW CYCLE SL ABACO ASSET MANAGEMENT LLP ABACUS INVESTMENT SOLUTIONS LTD ABACUS WEALTH MANAGEMENT LIMITED ABANS GLOBAL LIMITED ABANTOS GESTIONA SL ABBEY CAPITAL LIMITED ABBEY NATIONAL TREASURY SERVICES PLC ABBEY STOCKBROKERS LIMITED ABBOTT CAPITAL (EUROPE) LIMITED ABC ASESORES PATRIMONIALES 2020 https://www.estafastrading.comS.L. Entidades Autorizadas por la CNMV Fuente: estafastrading.com para prestar servicios de inversión cnmv.es ABERDEEN