A Non-Linear Analysis of Operational Risk and Operational Risk Management in Banking Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amcham Body 69V4.Qxd

issue 69 may 2006 Bulgaria, United States Sign on Joint Training Facilities ■ IMF Performance Review Completed With Three Waivers ■ AmCham and Symix Host an Award Ceremony ■ Maritsa Forum Mulls Infrastructure, Industrial Zones and Support of SMEs ■ Member News ■ New Members NATO IN SOFIA: An April Walk Through a Global Agenda American Chamber of Commerce in Bulgaria Business Park Sofia, Mladost 4 Area, Building 2, Floor 6, 1715 Sofia Tel.: (359 2) 9769 565 Fax: (359 2) 9769 569 homepage: www.amcham.bg e-mail: [email protected] editorial Dear Readers: Each of us has a personal interpretation of the beneficial corollaries for Bulgaria from the just-concluded NATO meeting in Sofia (please read in-depth analyses by Boyko Vassilev and Panayot Angarev on pp. 4-14). Most of you, too, have a position on whether Bulgaria and Romania's EU entry will be delayed by a year. Neither I, nor any other journalist can answer this question definitively at this time (for details, see Yuliana Boncheva's article on p. 22.) NATO and the European Union have been subjects of numerous articles in our publica- tion, among others. So I would rather switch your attention toward another topic now. Namely, it is the story by Chris Warde-Jones in the New York Times on Sofia as a tourist destination, which was published in the newspaper of record in early May. (We present it for you on p. 44.) This travel feature offers a refreshing view of the Bulgarian capital, written by someone who was impressed by images of the city that are, generally speaking, flattering. -

JOHN THOMAS FINANCIAL, INC., And

-~;i;e:l: UNITED STATES OF AMERICA Before the I SECURITIES AND EXCHANGE COMMISSlON. y " . MA c:.8 2014 ~FFlCE otrH{SECRETARt In the Matter of JOHN THOMAS CAPITAL MANAGMENT GROUP LLC d/b/a PATRIOT28 LLC, File No. 3-15255 GEORGE R. JARKESY, JR., JOHN THOMAS FINANCIAL, INC., and ANASTASIOS "TOMMY" BELESIS, Respondents. RESPONDENTS' POST-HEARING MEMORANDUM OF LAW Karen Cook, Esq. S. Michael McColloch, Esq. Karen Cook, PLLC S. Michael McColloch, PLLC E-mail: [email protected] E-mail: [email protected] Phone: 214.593.6429 Phone: 214.593.6415 1717 McKinney A venue, Suite 700 171 7 McKinney A venue, Suite 700 Dallas, Texas 75202 Dallas, Texas 75202 Fax: 214.593.6410 Fax: 214.593.6410 Counsel for: John Thomas Capital Management Group d/b/a Patriot28 LLC and George Jarkesy, Jr. TABLE OF CONTENTS Preliminary Statement....................................................................................................... l The AP is Void Because the Commission Prejudged the Case Against Respondents ............................................................................................................ 2 The AP Should Be Dismissed Due to Improper Ex Parte Communications with the Division of Enforcement Prior to the Hearing ..................................... 8 The AP is Void Because the Commission Failed to Follow its Own Rules of Practice.................................................................................................................. ll Respondents' Constitutional Rights Were {and continue to be) Violated ................. -

Disciplinary and Other FINRA Actions

Disciplinary and Other FINRA Actions Firms Fined, Individuals Sanctioned Reported for Delaney Equity Group, LLC (CRD® #142285, Palm Beach Gardens, Florida) October 2013 and David Cameron Delaney (CRD #2447186, Registered Principal, West Palm Beach, Florida) submitted an Offer of Settlement in which the firm was censured and fined $215,000. The firm was prohibited from directly or FINRA has taken disciplinary actions indirectly receiving, in any manner, any penny stock in any form, and prohibited against the following firms and from selling, for the benefit of any customer or firm proprietary account, any individuals for violations of FINRA penny stock deposited with the firm (including through the firm’s clearing rules; federal securities laws, rules firm) by Automated Customer Account Transfer (ACAT) unless the stock has and regulations; and the rules of been held in the account for at least 180 days or has been beneficially owned the Municipal Securities Rulemaking by the accountholder, including the accountholders predecessors, if any, for Board (MSRB). the requisite statutory period not to be less than 180 days, and in amounts not to exceed the volume limitations prescribed by the applicable federal securities laws; or the stock is subject to an effective registration statement. The firm shall retain, within 60 days of the date of the Order Accepting Offer of Settlement, an independent consultant, to conduct a comprehensive review of the adequacy of the firm’s policies, systems and procedures (written and otherwise) and training relating to the compliance with Section 5 of the Securities Act of 1933, applicable rules and regulations with respect to the distribution of unregistered non-exempt securities, compliance with the requirements of the Bank Secrecy Act, and the regulations promulgated thereunder. -

The Complete Idiot's Guide to Starting an Ebay Business, Second Edition

Starting an eBay Business Second Edition by Barbara Weltman and Malcolm Katt A member of Penguin Group (USA) Inc. Starting an eBay Business Second Edition by Barbara Weltman and Malcolm Katt A member of Penguin Group (USA) Inc. This book is dedicated to all the eBay sellers, present and future, who prove that the entrepreneurial spirit is indomitable. ALPHA BOOKS Published by the Penguin Group Penguin Group (USA) Inc., 375 Hudson Street, New York, New York 10014, USA Penguin Group (Canada), 90 Eglinton Avenue East, Suite 700, Toronto, Ontario M4P 2Y3, Canada (a division of Pearson Penguin Canada Inc.) Penguin Books Ltd, 80 Strand, London WC2R 0RL, England Penguin Ireland, 25 St. Stephen’s Green, Dublin 2, Ireland (a division of Penguin Books Ltd.) Penguin Group (Australia), 250 Camberwell Road, Camberwell, Victoria 3124, Australia (a division of Pearson Australia Group Pty. Ltd.) Penguin Books India Pvt. Ltd., 11 Community Centre, Panchsheel Park, New Delhi—110 017, India Penguin Group (NZ), 67 Apollo Drive, Rosedale, North Shore, Auckland 1311, New Zealand (a division of Pearson New Zealand Ltd.) Penguin Books (South Africa) (Pty.) Ltd, 24 Sturdee Avenue, Rosebank, Johannesburg 2196, South Africa Penguin Books Ltd., Registered Offices: 80 Strand, London WC2R 0RL, England Copyright © 2008 by Barbara Weltman and Malcolm Katt All rights reserved. No part of this book shall be reproduced, stored in a retrieval system, or transmitted by any means, electronic, mechanical, photocopying, recording, or otherwise, without written permission from the pub- lisher. No patent liability is assumed with respect to the use of the information contained herein. Although every precaution has been taken in the preparation of this book, the publisher and authors assume no responsibility for errors or omissions. -

Financial Sectors in EU Accession Countries

Financial Sectors in EU Accession Countries EUROPEAN CENTRAL BANK EUROPEAN Financial Sectors in EU Accession Countries Financial Sectors in EU Financial Sectors in EU Accession Countries Editor: Christian Thimann Published by: © European Central Bank, July 2002 Address Kaiserstrasse 29 60311 Frankfurt am Main Germany Postal address Postfach 16 03 19 60066 Frankfurt am Main Germany Telephone +49 69 1344 0 Internet http://www.ecb.int Fax +49 69 1344 6000 Telex 411 144 ecb d Copies of the individual articles can also be downloaded from the ECB’s website. The views expressed in this publication are those of the authors and not necessarily those of the ECB. No responsibility for them should be attributed to the ECB or to any of the other institutions with which the authors are affiliated. All rights reserved by the authors. Editor: Christian Thimann Typeset and printed by: Kern & Birner GmbH + Co. ISBN 92-9181-292-7 Table of Contents Foreword “The importance of financial sector developments in EU accession countries” T. Padoa-Schioppa (European Central Bank) .....................................................................005 Summary “Financial sectors in EU accession countries: Issues for the workshop and summary of the discussion” C. Thimann (European Central Bank) ................................................................................007 “Key features of the financial sectors in EU accession countries” G. Caviglia, G. Krause and C. Thimann (European Central Bank) ...................................015 “The financial sector in Bulgaria: structure, functioning and trends” V. Yotzov (Bulgarian National Bank) .................................................................................031 “The financial sector in Cyprus: structure, performance and main developments” L. Georgiadou (Central Bank of Cyprus) ...........................................................................051 “The financial sector in the Czech Republic: an assessment of its current state of development and functioning” P. -

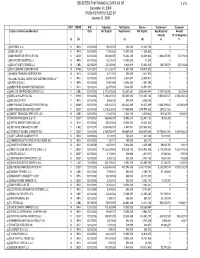

SELECTED FCM FINANCIAL DATA AS of December 31, 2008 FROM

SELECTED FCM FINANCIAL DATA AS OF 1 of 5 December 31, 2008 FROM REPORTS FILED BY January 31, 2009 B/D? DSRO A/O Adjusted Net Capital Excess Customers' Customer Futures Commission Merchant Date Net Capital Requirement Net Capital Seg Required Amount 4d(a)(2) Pt. 30 Required (a) (b) (c) (d) (e) (f) 1 3D FOREX, LLC N NFA 12/31/2008 18,931,722 500,000 18,431,722 0 0 2 ACM USA LLC N NFA 12/31/2008 11,575,482 10,000,000 1,575,482 0 0 3 ADM INVESTOR SERVICES INC N CBOT 12/31/2008 154,941,097 74,632,265 80,308,832 1,864,327,056 72,071,646 4 ADVANCED MARKETS LLC N NFA 12/31/2008 10,071,373 10,000,000 71,373 0 0 5 ADVANTAGE FUTURES LLC N CME 12/31/2008 25,081,866 6,446,918 18,634,948 188,738,579 32,311,026 6 AIG CLEARING CORPORATION N NYME 12/31/2008 321,823,187 11,903,795 309,919,392 0 0 7 ALARON TRADING CORPORATION N NFA 12/31/2008 3,711,574 500,000 3,211,574 0 0 8 ALLIANZ GLOBAL INVESTORS DISTRIBUTORS LLC * Y NFA 12/31/2008 27,457,078 6,847,647 20,609,431 0 0 9 ALPARI (US) LLC N NFA 12/31/2008 17,497,095 10,000,000 7,497,095 0 0 10 AMERIPRISE ADVISOR SERVICES INC Y NFA 12/31/2008 22,077,618 5,346,567 16,731,051 0 0 11 BANC OF AMERICA SECURITIES LLC Y CME 12/31/2008 3,171,801,285 166,357,841 3,005,443,444 1,007,978,026 16,837,469 12 BARCLAYS CAPITAL INC Y NYME 12/31/2008 7,878,067,153 500,000,000 7,378,067,153 5,993,650,575 2,976,258,742 13 BGC SECURITIES Y NFA 12/31/2008 8,855,236 500,000 8,355,236 0 0 14 BNP PARIBAS COMMODITY FUTURES INC N NYME 12/31/2008 322,615,874 242,242,565 80,373,309 2,668,759,643 445,566,495 15 BNP PARIBAS SECURITIES -

Vol. 83 Wednesday, No. 60 March 28, 2018 Pages 13183–13374

Vol. 83 Wednesday, No. 60 March 28, 2018 Pages 13183–13374 OFFICE OF THE FEDERAL REGISTER VerDate Sep 11 2014 22:04 Mar 27, 2018 Jkt 244001 PO 00000 Frm 00001 Fmt 4710 Sfmt 4710 E:\FR\FM\28MRWS.LOC 28MRWS amozie on DSK30RV082PROD with FRONT MATTER WS II Federal Register / Vol. 83, No. 60 / Wednesday, March 28, 2018 The FEDERAL REGISTER (ISSN 0097–6326) is published daily, SUBSCRIPTIONS AND COPIES Monday through Friday, except official holidays, by the Office PUBLIC of the Federal Register, National Archives and Records Administration, Washington, DC 20408, under the Federal Register Subscriptions: Act (44 U.S.C. Ch. 15) and the regulations of the Administrative Paper or fiche 202–512–1800 Committee of the Federal Register (1 CFR Ch. I). The Assistance with public subscriptions 202–512–1806 Superintendent of Documents, U.S. Government Publishing Office, Washington, DC 20402 is the exclusive distributor of the official General online information 202–512–1530; 1–888–293–6498 edition. Periodicals postage is paid at Washington, DC. Single copies/back copies: The FEDERAL REGISTER provides a uniform system for making Paper or fiche 202–512–1800 available to the public regulations and legal notices issued by Assistance with public single copies 1–866–512–1800 Federal agencies. These include Presidential proclamations and (Toll-Free) Executive Orders, Federal agency documents having general FEDERAL AGENCIES applicability and legal effect, documents required to be published Subscriptions: by act of Congress, and other Federal agency documents of public interest. Assistance with Federal agency subscriptions: Documents are on file for public inspection in the Office of the Email [email protected] Federal Register the day before they are published, unless the Phone 202–741–6000 issuing agency requests earlier filing. -

Justin Bio Handout 2020-01-21

Justin S. Weddle Founder 212-997-5518 [email protected] Justin Weddle is a skilled trial lawyer, litigation strategist, counselor, and Education appellate advocate. When the stakes are high, clients rely on his tenacity Columbia University School of Law, J.D. 1995 Managing Editor, Columbia Law Review and incisive analysis for tailor-made strategies and solutions in both Kent Scholar, Stone Scholar domestic and cross-border criminal, civil, and regulatory matters. As a Haverford College, B.A. 1992 result, Justin Weddle is a regular participant in the highest-profile Bar Admissions investigations, trials, and appeals, such as: New York Massachusetts LIBOR criminal cases U.S. District Courts: Southern District of New York, Eastern District of New York, and The FIFA corruption case District of Massachusetts U.S. Courts of Appeals: First, Second, Third, Circuit Court cases on SEC disgorgement and ALJ appointment issues Tenth, Eleventh, and D.C. Circuits U.S. Supreme Court U.S. investigation and litigation relating to Brazil’s Lava Jato Recognitions investigation Recognized by Super Lawyers as a Top Rated The Supreme Court Lucia decision rejecting the SEC’s ALJs as White Collar Crimes Attorney in New York, NY, since 2017 unconstitutional Listed in Who’s Who Legal, Business Crime Defense for both Corporates and The KPMG-PCAOB leaks criminal jury trial in the Southern District of Individuals New York Professional Activities Justin prosecuted white collar crime for more than 12 years as an Assistant Chair of the Appeals Subcommittee NYC Bar Association Federal Courts United States Attorney in the Southern District of New York, building and Committee trying complex fraud cases. -

Jonathan C. Rugg, CFA, President Cyrus M

Item 1. Cover Page PART 2B of FORM ADV Jonathan C. Rugg, CFA, President Cyrus M. Amini, Esq., CFA, CIO & CCO Shawn Hsieh, MBA, CFA, CFP Aaron Dejuan Morris, AIF Jamie N. Rugg, CFP David Fitzgerald, CIMA Thomas Murphy K. David Yoshioka Hugh A. Meyer, MBA David D. Hu, CLU, CFP Charlesworth & Rugg, Inc. 20750 Ventura Boulevard, Suite 420 Los Angeles, California 91364 Phone: (818) 340-0157 Facsimile: (818) 702-8851 Email: [email protected] March 31, 2019 This brochure supplement provides information about the qualifications of Charlesworth & Rugg, Inc. (C&R) supervised persons. If you have any questions about the contents of this brochure supplement, please contact us at (818) 340-0157. The information in this brochure supplement has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. C&R is a registered investment adviser. However, being a registered investment adviser does not imply a certain level of skill or training and does not guarantee investment performance. Additional information about C&R is also available on the SEC’s website at www.adviserinfo.sec.gov. 1 Jonathan C. Rugg, CFA Item 2. Educational Background and Business Experience NAME: Jonathan Christopher Rugg YEAR OF BIRTH: 1983 FORMAL EDUCATION: B.S. with concentrations in Finance, Real Estate and Marketing at The University of Pennsylvania, Wharton School of Business, 2006 Chartered Financial Analyst (CFA) Charterholder, 2010 BUSINESS BACKGROUND: Firm Position Responsibilities Period C&R President Investment selection, asset 8/16 - Present allocation and business development Chief Develops, maintains, monitors, 8/16 – 3/19 Compliance and revises, compliance related Officer policies and procedures Vice Investment selection, asset 8/10 – 7/16 President allocation and business development Urdang Capital Associate, Analyzing investments, 7/06 - 6/10 Management Acquisitions underwriting, due diligence Item 3. -

7Th Annual Risk Americas Convention - 2018

7th Annual Risk Americas Convention - 2018 Fraud, Cybercrime and Reputation Risk – What Organizations Can Do About It Dalit Stern, CPA, CFE Senior Director Enterprise Fraud Risk Management, TIAA New York - May 17, 2018 Agenda The intertwined landscape of fraud and cyber A vibrant marketplace changes the face of fraud Sophistication of social engineering techniques Customers Corporations The impact of cyber risk on fraud and reputation risks what to do about it Q&A 2 Disclaimer The views expressed in this presentation and in today’s discussion are the views of the speaker and do not necessarily reflect the views or policies of TIAA. Examples, charts and metrics are purely for illustrational purposes, and may have been modified or simplified in order to clarify a point. Neither the speaker, nor TIAA, accept responsibility for any consequence of the use of any part of the framework presented herein. 3 The Intertwined Landscape of Fraud and Cyber Assessing the risk of fraud in financial institutions: • Financial institutions continue to be subject to fraud: • In person • Remote fraud (online, interactive voice response (IVR) , paper ) • Consistent trends of money out and account maintenance fraud enabled by cyber incidents • Cyberattacks are becoming a more prominent fraud threat - designed to target: • Customer assets • Financial institution assets • Certain subsectors are more prone to cyber fraud but most see increased activity (e.g., banking, brokerage, retirement 4 insurance, investments) The Intertwined Landscape of Fraud and -

03-YU-Contemporary-I

Page 1 IN THE REGULAR DIVISION OF THE OREGON TAX COURT (Property Tax) ) YU CONTEMPORARY, INC. ) ) Plaintiff, ) ) vs. ) ) DEPARTMENT OF REVENUE, STATE OF ) OREGON, ) ) Defendants, ) CASE NO. TC 5245 ) and ) ) MULTNOMAH COUNTY ASSESSOR, ) ) Intervenor. ) _________________________________________________________________ VERBATIM REPORT OF PROCEEDINGS _________________________________________________________________ April 5, 2016 Before the HONORABLE HENRY C. BREITHAUPT TRANSCRIBED BY: Kaedra Ray Wakenshaw, CCR, RPR, CRR CCR No. 1900 Page 2 1 A P P E A R A N C E S 2 FOR THE PLAINTIFF: 3 Jeffrey G. Bradford 4 Tonkon Torp L.L.P. 1600 Pioneer Tower 5 888 SW Fifth Avenue Portland, Oregon 97204 6 Michael J. Millender 7 Tonkon Torp L.L.P. 1600 Pioneer Tower 8 888 SW Fifth Avenue Portland, Oregon 97204 9 10 FOR THE DEFENDANT: 11 Daniel Paul Assistant Attorney General 12 Department of Justice 1162 Court Street NE 13 Salem, Oregon 97301 14 FOR THE INTERVENOR: 15 Carlos Rasch 16 Assistant County Counsel Multnomah County Attorney's Office 17 501 SE Hawthorne Boulevard Suite 500 18 Portland, Oregon 97214 19 20 21 22 23 24 25 Page 3 1 T A B L E O F C O N T E N T S 2 3 PROCEEDINGS PAGE 4 Opening Statement (Plaintiff)........................ 10 Opening Statement (Defense).......................... 20 5 6 TESTIMONY PAGE 7 JENNIFER L. MARTIN 8 Direct Examination..............................32 Cross-Examination...............................106 9 Redirect Examination............................152 Recross-Examination.............................160 10 AARON F. JAMISON 11 Direct Examination..............................162 Cross-Examination...............................203 12 Redirect Examination............................217 13 BELINDA M. DEGLOW Direct Examination..............................221 14 Cross-Examination...............................249 15 KARLA HARTENBERGER Direct Examination..............................263 16 JENNIFER L. -

Miguel Ortiz January 4, 2017 New York, NY

BEFORE THE NATIONAL ADJUDICATORY COUNCIL FINANCIAL INDUSTRY REGULATORY AUTHORITY In the Matter of Department of Enforcement, DECISION Complainant, Complaint No. 2014041319201 vs. Miguel Ortiz January 4, 2017 New York, NY, Respondent. Respondent willfully made material misrepresentations to conceal losses in an account. Respondent also willfully failed to disclose on his Form U4 an unsatisfied judgment. Held, findings and sanctions affirmed. Appearances For the Complainant: Leo F. Orenstein, Esq., Jeffrey D. Pariser, Esq., Department of Enforcement, Financial Industry Regulatory Authority For the Respondent: Pro se Decision Miguel Ortiz appeals a November 6, 2015 Hearing Panel decision. The Hearing Panel found that Ortiz made materially false statements and omitted material facts concerning the composition, value, and performance of an investment account and concealed the losses incurred in that account. It further found that Ortiz willfully failed to disclose on his Uniform Application for Securities Industry Registration and Transfer (“Form U4”) an unsatisfied judgment against him. The Hearing Panel barred Ortiz for his material misrepresentations and omissions and did not impose additional sanctions for Ortiz’s remaining misconduct. On appeal, Ortiz concedes that he made material misrepresentations and omitted to disclose material facts, but argues that his motivation was not greed or his own monetary gain. Rather, Ortiz argues that he misrepresented the composition, value, and performance of the account in a misguided attempt to shield the account’s owners, his longtime friend and her partner, from the “unpleasant reality” of large losses while he purportedly tried to recover the losses. Ortiz urges us to reduce the bar imposed upon him for this misconduct.