Alkem Laboratories Ltd. BUY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inner 20 Ethical Fund Low

Tata Ethical Fund (An open ended equity scheme following Shariah principles) As on 30th June 2020 PORTFOLIO No. of Market Value % of No. of Market Value % of INVESTMENT STYLE Company name Company name An equity scheme which invests primarily in equities of Shares Rs. Lakhs Assets Shares Rs. Lakhs Assets Shariah compliant companies and other instrument if Equity & Equity Related Total 49401.57 90.21 Oil allowed under Shariah principles. Auto Oil & Natural Gas Co. 925000 752.49 1.37 INVESTMENT OBJECTIVE Hero Motocorp Ltd. 31300 797.20 1.46 Pesticides To provide medium to long- term capital gains by investing Auto Ancillaries Rallis India Ltd. 502000 1366.95 2.50 in Shariah compliant equity and equity related instruments Wabco India Ltd. 15800 1087.06 1.99 Petroleum Products of well-researched value and growth - oriented companies. Sundram Fasteners Ltd. 267000 999.38 1.83 Bharat Petroleum Corporation Ltd. 435000 1626.90 2.97 Tata Ethical Fund aims to generate medium to long term Amara Raja Batteries Ltd. 116849 759.99 1.39 Castrol India Ltd. 505000 634.79 1.16 capital growth by investing in equity and equity related Cement Pharmaceuticals instruments of shariah compliant companies. Shree Cement Ltd. 3800 875.94 1.60 Alkem Laboratories Ltd. 83000 1965.69 3.59 DATE OF ALLOTMENT Commercial Services Ipca Laboratories Ltd. 93750 1569.75 2.87 May 24,1996 3M India Ltd. 4500 845.79 1.54 Lupin Ltd. 145000 1322.11 2.41 Consumer Durables Software FUND MANAGER Titan Company Ltd. 113000 1073.33 1.96 Tata Consultancy Services Ltd. -

Availability and Regulatory Status of Major Antiretroviral Drugs (September 2009)

Availability and regulatory status of major antiretroviral drugs (September 2009) Medium price per patient per year (in U$) Suppliers International Preferred 2008 Dosage Nonproprietary Strengths form Lower Upper Name (INN) (adults) Low income Middle Middle Originator Generics income income Aurobindo Pharma Ltd.; Cipla Ltd.; Eastern Surgical Company; Emcure; Hetero Drugs 317 a 370 Ltd.; Laboratorio Elea S.A.C.I.F.y A; Abacavir tablets 300 mg 350 a GlaxoSmithKline (286-370) (353-401) Laborotorios Filaxis Argentina; Laborotorios (313-374) Richmond S.A.C.I.F; Matrix Laboratories Ltd.; Ranbaxy Ltd; Strides Arcolab Ltd. 238 a Matrix, Ranbaxy, Hetero; Cipla; Aurobindo; Tenofovir tablets 300 mg 166 a 207 a Gilead Sciences (238-420) Emcure; Aspen; Strides Arcolab Ltd. (151-207) (177-256) Apotex Mexico (Protein, S.A. de C.V.); Aspen Pharmacare Ltd.; Aurobindo Pharma Ltd.; Cipla Ltd.; Cristalia, productos quimicos 212 a 462 Bristol-Myers farmaceuticos Ltda.; Emcure; Hetero Drugs 100 mg 251 a (187-235) (242-1100) Squibb Ltd.; Laboratorio Dosa S.A; Laborotorios (187-310) Filaxis Argentina; Laborotorios Richmond buffered S.A.C.I.F; Ranbaxy Ltd.; Zhejiang Huahai tablets Pharmaceutical Co., Ltd. 208 b Bristol-Myers Aspen Pharmacare Ltd.; Aurobindo Pharma 150 mg Didanosine (172-244) Squibb Ltd.; Cipla Ltd. Aurobindo Pharma Ltd; Barr Laboratories, Inc; 242 a 238 a 220 Bristol-Myers 200 mg Cipla Ltd.; Laborotorios Richmond S.A.C.I.F; (197-310) (233-794) (217-235) Squibb Macleods Pharmaceuticals Ltd.; Ranbaxy Ltd.; 242 a 238 a 220 Bristol-Myers 200 mg Aurobindo Pharma Ltd; Barr Laboratories, Inc; (197-310) (233-794) (217-235) Squibb EC 223 799 997 Bristol-Myers Aurobindo Pharma Ltd.; Barr Laboratories, 250 mg capsules (214-223) (675-874) (613-997) Squibb Inc; Cipla Ltd.; Ranbaxy Ltd.; 288 1267 a 1269 Bristol-Myers Aurobindo Pharma Ltd.; Barr Laboratories; 400 mg (279-288) (507-1302) (1129-1386) Squibb Hetero Drugs Ltd.; Cipla Ltd.; Ranbaxy Ltd. -

Partial List Ex Conference 20

Artemis Health Institute Bharat Serums & Vaccines Carrier CP Milk & Food Products Discovery FCDO GlaxoSmithkline Henkel India Shelter Finance Corporation Kadtech Infraprojects LSEG MIND NIIT Paytm Money PT Bank BTPN RTI Shyam Spectra Stryker ThoughtWorks ValueMined Technologies Y-Axis Solutions Arth Group Bharti Axa Life Insurance Cars24 CP Plus Dksh FE fundinfo Glenmark Pharmaceuticals Herbalife Nutition IndiaMART Kaivalya Educatiion Foundation LTI MindTickle Nineleaps technology solutions PayU PT. Media Indra Buana Ruby Seven Studios Shyam Spectra STT Global Data Centres Thryve Digital Valuex Technologies Yamaha Motor Arvind Fashions Bhel Caterpillar CP Wholesale DLF Fedex GlobalEdge Here Technologies Indigo Kalpataru Luminous Power Technologies Mindtree Nippon Koei PCCPL PTC Network Rustomjee Sidel Successive Technologies Tierra Agrotech Varroc Engineering Yanbal Asahi India Glass BIC CDK Global CPI DMD ADVOCATES Ferns n Petals GlobalLogic Herman Miller Indmoney Kama Ayurveda Luthra Group MiQ Digital NISA Global PCS Publicis Media S P Setia Siemens Sulzer Pumps Tifc Varuna Group Yanmar TAKE A LOOK AT LIST OF Ashirvad Pipes Bidgely Technologies CEAT Creditas Solutions DP World Ferrero GMR Hero Indofil industries Kanishk Hospital Luxury Personified Mizuho Bank Nissan Peak Infrastructure Management PUMA Group S&P Global Sigma AVIT Infra Services Summit Digitel Infrastructure TIL Vastu Housing Finance Corpora- Yara COMPANIES WHO WILL JOIN Asian paints Bigtree Entertainment Celio Cremica Dr Reddy's Ferring Pharmaceuticals Godrej & Boyce -

Creating a Global Enterprise

Creating a Global Enterprise ANNUAL REPORT 2005–06 DR. REDDY’S LABORATORIES LIMITED CREATING A GLOBAL ENTERPRISE In the world of matter, a drop of liquid diffuses slowly in another and forms a pattern that it is distinctive, reflective of its nature. Through more than a decade of steady effort and guided by an unswerving original vision, Dr. Reddy’s Laboratories has been growing into a business that has earned the right to be called global. When a business evolves, rather than changes suddenly, its growth is likely to endure. This year’s cover images, as a whole, tell the story of this transformation. The front shows how an enterprise, like a drop of reagent, can take a global shape in its own distinctive way, guided by its inherent nature. The back cover reflects our focus on three continental geographies and in the inside covers are images of diffusion, reflective of our creative energy. CONTENTS DR. REDDY'S LABORATORIES LIMITED chairman’s key creating a global inspired people, letter highlights enterprise — breakthrough Dr. Reddy’s performance transformational journey 004 008 010 020 safety, health & social board of management corporate environment responsibility — directors discussion & governance Dr. Reddy’s analysis Foundation 023 025 028 030 045 additional five years intangible ratio directors’ shareholders‘ at a glance accounting analysis report information 062 073 074 075 076 IGAAP IGAAP U.S.GAAP information on statement standalone consolidated consolidated the financials of pursuant to financials financials financials subsidiary Section 212 companies 087 125 163 202 203 notice of glossary annual general meeting 204 209 chairman’s letter 2005-06 has been a momentous what has happened in 2005-06 — and has transformational year in the history of occurred across various businesses of your your Company. -

Impact of Financial Planning on Financial Performance-A Study of Select Undertakings

Quest Journals Journal of Research in Business and Management Volume 9 ~ Issue 5 (2021) pp: 88-95 ISSN(Online):2347-3002 www.questjournals.org Research Paper Impact of Financial planning on Financial performance-A study of select undertakings Dr. PasunuriAmaraveni Associate Professor, University College of Commerce & Business Management, Kakatiya University, Warangal, Telangana, (India) MulukalapallySusruth Research scholar, Kakatiya University, Warangal, Telangana (India) ABSTRACT Financial planning is an integral part of financial management which deals with the management of a firm’s funds with a view to maximizing profit and the wealth of shareholders. The main aim of this study is to examine the impact of financial planning on financial performance. The sample used in this study are 5 companies of pharmaceutical industry which listed in National stock exchange and secondary data collected for period 2011- 2020.Regression analysis were employed to analyze the relationship between the dependent variable and independent variables. Findings show that there is a significant relationship between Financial planning and the financial performance with the R2 of 43%,30%,45%,36% and38%. Overall, the financial performance of Alkem laboratories Ltd. is highest with comparison of other companies and lowest is cadila Healthcare Ltd. The study findings indicated that Financial planning had positive impact on the financial performance. The study recommended the pharma companies should invest optimum amount infunding decisions, investment decisions and implementing financial policies with maintaining minimum level of profit as it had positive impact on the financial performance, the least variation to the expected results and that leads to highest contribution to operating profit.The study therefore concludes that sound financial planning by the pharma companies lead to a better financial performance as accountability was enhanced through all levels of decision making. -

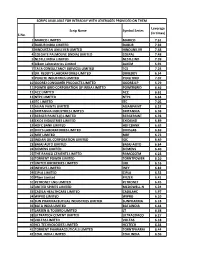

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

IN the UNITED STATES DISTRICT COURT for the DISTRICT of DELAWARE ) NOVARTIS PHARMACEUTICALS ) CORPORATION ) ) Plaintiff, ) ) V

Case 1:18-cv-01043-LPS Document 3 Filed 07/16/18 Page 1 of 4 PageID #: 132 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE ) NOVARTIS PHARMACEUTICALS ) CORPORATION ) ) Plaintiff, ) ) v. ) C.A. No. _____ ) ACCORD HEALTHCARE INC., INTAS ) PHARMACEUTICALS LIMITED, ) ALKEM LABORATORIES, LTD., S&B ) PHARMA, INC., AUROBINDO ) PHARMA LIMITED, AUROBINDO ) PHARMA USA, INC., BIOCON ) LIMITED, BIOCON PHARMA, INC.. ) BIONPHARMA INC., BRECKENRIDGE ) PHARMACEUTICAL, INC., ) STANDARD CHEMICAL & ) PHARMACEUTICAL CO., LTD., DR. ) REDDY’S LABORATORIES, INC., DR. ) REDDY’S LABORATORIES, LTD., ) EMCURE PHARMACEUTICALS, ) HERITAGE PHARMACEUTICALS INC., ) EZRA VENTURES, LLC, FIRST TIME ) US GENERICS LLC, GLENMARK ) PHARMACEUTICALS INC., USA, ) GLENMARK PHARMACEUTICALS ) LIMITED, HEC PHARM CO., LTD., HEC ) PHARM GROUP, HEC PHARM USA ) INC., HETERO USA INC, HETERO ) LABS LIMITED UNIT-V, HETERO ) LABS LIMITED, MYLAN ) PHARMACEUTICALS, INC., ) NOSTRUM LABORATORIES INC., ) NOSTRUM PHARMACEUTICALS, ) LLC, MSN LABORATORIES PRIVATE ) LIMITED, MSN PHARMACEUTICALS ) INC., PAR PHARMACEUTICAL INC., ) PRINSTON PHARMACEUTICAL INC., ) STRIDES GLOBAL PHARMA PRIVATE ) LIMITED, STRIDES PHARMA, INC., ) TORRENT PHARMA INC., TORRENT ) PHARMACEUTICALS LTD., ZYDUS ) PHARMACEUTICALS (USA) INC., and ) CADILA HEALTHCARE LIMITED ) ) Defendants. ME1 27645531v.1 Case 1:18-cv-01043-LPS Document 3 Filed 07/16/18 Page 2 of 4 PageID #: 133 SUPPLEMENTAL INFORMATION FOR PATENT CASES INVOLVING AN ABBREVIATED NEW DRUG APPLICATION (ANDA) Plaintiffs hereby provide the information below with respect to the deadlines set forth in 21 U.S.C. § 355(j): Date Patentee(s) Received Notice: See attached chart Date of Expiration of Patent: 9,187,405 (June 25, 2027) Thirty Month Stay Deadline: N/A Dated: July 16, 2018 McCARTER & ENGLISH, LLP By: /s/ Daniel M. Silver Michael P. -

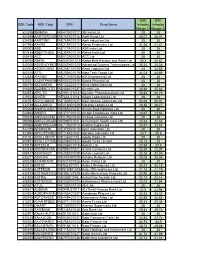

NSE Symbol NSE 6 Month Avg Total Market

Average Market Cap of 200 listed companies on BSE & NSE for the six months ended 30 June 2021 BSE 6 month Avg NSE 6 month Avg Average of BSE and NSE 6 Total Market Cap Total Market Cap month Avg Total Market Cap S.No. Company Name ISIN BSE SYMBOL (Rs. In Crs.) NSE Symbol (Rs. In Crs.) (Rs. in Crs.) 1 Reliance Industries Ltd INE002A01018 RELIANCE 1338017.01 RELIANCE 1355067.509 1346542.26 Tata Consultancy Services 2 Ltd. INE467B01029 TCS 1169783.56 TCS 1173068.166 1171425.86 3 HDFC Bank Ltd. INE040A01034 HDFCBANK 819037.95 HDFCBANK 818713.671 818875.81 4 Infosys Ltd INE009A01021 INFY 579784.19 INFY 579697.3885 579740.79 5 Hindustan Unilever Ltd., INE030A01027 HINDUNILVR 549336.78 HINDUNILVR 549358.908 549347.84 Housing Development 6 Finance Corp.Lt INE001A01036 HDFC 462288.58 HDFC 461373.1089 461830.84 7 ICICI Bank Ltd. INE090A01021 ICICIBANK 416645.51 ICICIBANK 416389.0234 416517.27 8 Kotak Mahindra Bank Ltd. INE237A01028 KOTAKBANK 361640.52 KOTAKBANK 361438.6361 361539.58 9 State Bank Of India, INE062A01020 SBIN 329767.32 SBIN 329789.268 329778.29 10 Bajaj Finance Limited INE296A01024 BAJFINANCE 324996.53 BAJFINANCE 324843.5005 324920.02 11 Bharti Airtel Ltd. INE397D01024 BHARTIARTL 299981.36 BHARTIARTL 299955.7729 299968.57 12 HCL Technologies Ltd INE860A01027 HCLTECH 261400.46 HCLTECH 261392.0109 261396.24 13 Wipro Ltd., INE075A01022 WIPRO 258617.45 WIPRO 261102.3994 259859.92 14 ITC Ltd INE154A01025 ITC 259423.16 ITC 259396.0648 259409.61 15 Asian Paints Ltd. INE021A01026 ASIANPAINT 253487.28 ASIANPAINT 253454.4536 253470.87 16 AXIS Bank Ltd. -

Strong Expanding to Newer Ones

2015-16 ANNUAL REPORT Strong in Our Core Market Expanding to Newer Ones Contents Corporate Overview Financial Statements 02 Alkem at a Glance Standalone 04 Global Presence 94 Independent Auditor’s Report 06 Key Therapeutic Areas and Brands in Domestic Market 100 Balance Sheet 08 Chairman’s Message 101 Statement of Profit and Loss 09 Executive Chairman’s Message 102 Cash Flow Statement 10 CEO’s Message 104 Notes 12 Key Financial Highlights 14 Strong Brand Building Capabilities Consolidated 16 Strong Manufacturing and R&D Capabilities 140 Independent Auditor’s Report 18 Extensive Sales Network and Distribution Infrastructure 144 Balance Sheet 20 Growing International Business 145 Statement of Profit and Loss 22 The People Edge 146 Cash Flow Statement 24 Board of Directors 148 Notes 26 Awards and Accolades 197 Notice Statutory Reports Proxy Form 28 Management Discussion and Analysis 48 Directors’ Report 79 Corporate Governance Report Earnings per Net Revenue EBITDA PAT share ` 49,915 ` 8,482 ` 6,731 ` 56.3 million million million Strong in Our Core Market. Expanding to Newer Ones. Growth and consolidation are business imperatives that are achieved as a result of conscious and persistent strategy. More often than not, companies that are able to step out of their comfort zone while retaining their hold over captive markets are the ones that succeed in the long-term. We believe that the path to value-creation is twofold. On the one hand, we continue to focus on consolidating our presence in India and introducing newer products consistently, while improving the breadth and depth of our reach. -

Alkem Laboratories Ltd

Name of the issue: Alkem Laboratories Ltd 1 Type of issue (IPO/ FPO) IPO 2 Issue size (Rs crore) 1347.7* * Source: Basis of Allotment - pursuant to spill over of undersubscription in Employee category to Net Offer 3 Grade of issue alongwith name of the rating agency Not applicable 4 Subscription level (number of times). If the issue was undersubscribed, please clarify how the funds were 30.8708* Figure is before technical rejections and after adjusting for cheque return cases arranged. *Source: Basis of Allotment 5 QIB holding (as a % of total outstanding capital) as disclosed to stock exchanges (See Clause 35 of the listing agreement) (i) allotment in the issue 5.3 Source: Minutes for basis of allotment dated 19 Dec 2015 (ii) at the end of the 1st Quarter immediately after the listing Source: BSE Filings of the issue (December 31, 2015) 6.04 (iii) at the end of 1st FY (March 31, 2016) 6.81 Source: BSE Filings (iv) at the end of 2nd FY (March 31, 2017) 6.75 Source: BSE Filings (v) at the end of 3rd FY (March 31, 2018) 6.92 Source: BSE Filings 6 Financials of the issuer (as per the annual financial results submitted to stock exchanges under Clause 41 of the listing agreement) As per the annual Consolidated financial results submitted to stock exchanges (Rs. in crores) 1st FY 2nd FY 3rd FY Parameters (March 31, 2016) (March 31, 2017) (March 31, 2018) 1 Income from operations 4,992 5,853 6,431 2 Net Profit for the period 673.12 869.12 611.87 Paid-up equity share capital 23.91 23.91 23.91 Reserves excluding revaluation reserves 3,478.74 4,443.73 4,839.86 Source: Alkem BSE Filings. -

FTSE India 30/18 Capped

2 FTSE Russell Publications 19 August 2021 FTSE India 30/18 Capped Indicative Index Weight Data as at Closing on 30 June 2021 Constituent Index weight (%) Country Constituent Index weight (%) Country Constituent Index weight (%) Country 3M India 0.1 INDIA Glenmark Pharmaceuticals 0.14 INDIA Oil India Ltd 0.07 INDIA ABB India 0.13 INDIA GMR Infrastructure 0.1 INDIA Oracle Financial Services Software 0.12 INDIA ACC 0.24 INDIA Godrej Consumer Products 0.45 INDIA Page Industries 0.24 INDIA Adani Enterprises 0.57 INDIA Godrej Industries 0.07 INDIA Petronet LNG 0.24 INDIA Adani Gas 0.4 INDIA Godrej Properties 0.18 INDIA PI Industries 0.3 INDIA Adani Green Energy 0.63 INDIA Grasim Industries 0.82 INDIA Pidilite Industries 0.47 INDIA Adani Ports and Special Economic Zone 0.77 INDIA Gujarat Gas 0.19 INDIA Piramal Enterprises 0.41 INDIA Adani Power 0.15 INDIA Havells India 0.34 INDIA Power Finance 0.21 INDIA Aditya Birla Capital 0.08 INDIA HCL Technologies 1.52 INDIA Power Grid Corp of India 0.78 INDIA Alkem Laboratories 0.11 INDIA HDFC Asset Management 0.27 INDIA Punjab National Bank 0.06 INDIA Ambuja Cements 0.33 INDIA HDFC Life Insurance Company 0.63 INDIA Rajesh Exports 0.11 INDIA Apollo Hospitals Enterprise 0.51 INDIA Hero MotoCorp 0.54 INDIA RBL Bank 0.13 INDIA Ashok Leyland 0.25 INDIA Hindalco 0.75 INDIA REC 0.2 INDIA Asian Paints 1.92 INDIA Hindustan Aeronautics 0.05 INDIA Reliance Industries 9.35 INDIA Astral 0.25 INDIA Hindustan Petroleum 0.3 INDIA Reliance Industries - Partly Paid 0.36 INDIA AU Small Finance Bank 0.23 INDIA Hindustan -

BSE Code NSE Code ISIN Scrip Name NSE Intraday Margin % BSE

NSE BSE BSE Code NSE Code ISIN Scrip Name Intraday Intraday Margin % Margin % 523395 3MINDIA INE470A01017 3M India Ltd 20 20 524348 AARTIDRUGS INE767A01016 Aarti Drugs Ltd 26.01 26.01 524208 AARTIIND INE769A01020 Aarti Industries Ltd 20 20 541988 AAVAS INE216P01012 Aavas Financiers Ltd 21.46 21.41 500002 ABB INE117A01022 ABB India Ltd 20 20 500488 ABBOTINDIA INE358A01014 Abbott India Ltd 20 20 500410 ACC INE012A01025 ACC Ltd 20 20 535755 ABFRL INE647O01011 Aditya Birla Fashion and Retail Ltd 20.4 20.62 540025 ADVENZYMES INE837H01020 Advanced Enzyme Technologies Ltd 25.33 25.28 500003 AEGISCHEM INE208C01025 Aegis Logistics Ltd 23 22.95 500215 ATFL INE209A01019 Agro Tech Foods Ltd 21.02 20.99 532683 AIAENG INE212H01026 AIA Engineering Ltd 20 20 532331 AJANTPHARM INE031B01049 Ajanta Pharma Ltd 20 20 500710 AKZOINDIA INE133A01011 Akzo Nobel India Ltd 20 20 506235 ALEMBICLTD INE426A01027 Alembic Ltd 25.66 25.62 533573 APLLTD INE901L01018 Alembic Pharmaceuticals Ltd 20.82 20.79 539523 ALKEM INE540L01014 Alkem Laboratories Ltd 20 20 506767 ALKYLAMINE INE150B01021 Alkyl Amines Chemicals Ltd 26.94 26.91 532749 ALLCARGO INE418H01029 Allcargo Logistics Ltd 20.35 20.27 500008 AMARAJABAT INE885A01032 Amara Raja Batteries Ltd 20 20 540902 AMBER INE371P01015 Amber Enterprises India Ltd 23.67 23.64 500425 AMBUJACEM INE079A01024 Ambuja Cements Ltd 20 20 590006 AMRUTANJAN INE098F01031 Amrutanjan Health Care Ltd 22.63 22.63 590062 ANDHRSUGARINE715B01013 Andhra Sugars Ltd 23.47 23.47 532259 APARINDS INE372A01015 Apar Industries Ltd 20 20 523694 APCOTEXIND