Indepth Aug 2020 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sun Life Excel India Fund

SUN LIFE EXCEL INDIA FUND Summary of Investment Portfolio* as at September 30, 2020 Top 25 Investments³ Sector Allocation³ Percentage of Net Asset Percentage of Net Asset Holding Name Value of the Fund (%) Value of the Fund % 1 Reliance Industries Limited 8.6 Financials 23.9 2 Infosys Limited 8.5 Information Technology 12.3 3 iShares MSCI India ETF 8.1 Energy 9.3 4 ICICI Bank Limited 7.3 Exchange-Traded Funds - International 5 HDFC Bank Limited 3.9 Equities 8.1 6 HCL Technologies Limited 3.7 Consumer Staples 7.6 7 Bharti Airtel Limited 3.7 Consumer Discretionary 7.1 8 Housing Development Finance Corporation Limited 3.5 Health Care 7.0 9 Hindustan Unilever Limited 3.1 Other Assets less Liabilities 5.7 10 Axis Bank Limited 2.3 Materials 4.7 11 Kotak Mahindra Bank Limited 2.0 Communication Services 4.6 12 Maruti Suzuki India Limited 2.0 Industrials 4.5 13 Mahindra & Mahindra Limited 2.0 Cash and Cash Equivalents 3.1 14 Bajaj Finance Limited 1.9 Real Estate 2.1 15 Dalmia Bharat Limited 1.6 100.0 16 Strides Pharma Science Limited 1.5 17 Dabur India Limited 1.4 Asset Allocation³ 18 Polycab India Limited 1.4 19 Aster DM Healthcare Limited 1.3 Percentage of Net Asset Value of the Fund % 20 Trent Limited 1.3 21 Britannia Industries Limited 1.3 International Equities 91.2 22 Sun Pharmaceutical Industries Limited 1.3 Other Assets less Liabilities 5.7 23 Motherson Sumi Systems Limited 1.3 Cash and Cash Equivalents 3.1 24 Clearing Corporation of India Limited 1.2 100.0 25 UltraTech Cement Limited 1.2 ³ 75.4 Geographic Allocation Total Net Asset Value (©000©s) $ 203,711 Percentage of Net Asset Value of the Fund % India 91.2 Other Assets less Liabilities 5.7 Cash and Cash Equivalents 3.1 100.0 (*) All information is as at September 30, 2020. -

Profitability of Britannia Industries Limited”

FINAL YEAR BBA(H) STUDY PAPER ON “PROFITABILITY OF BRITANNIA INDUSTRIES LIMITED” SUBMITTED BY: GROUP MEMBERS SUBHAJIT BHATTACHARYA (Roll: 15405015050) SUSHMITA SAHA (Roll: 15405015061) PRITAM DASGUPTA (Roll: 15405015023) RADHIKA DUTTAGUPTA (Roll: 15405015025) STREAM- BBA (H) YEAR- 3rd (THIRD) SEMESTER – 6th (SIXTH) SESSION- 2015-2018 COLLEGE- DINABANDHU ANDREWS INSTITUTE OF TECHNOLOGY AND MANAGEMENT UNIVERSITY- MAULANA ABUL KALAM AZAD UNIVERSITY OF TECHNOLOGY, WEST BENGAL INDEX TOPICS PAGE NUMBER INTRODUCTION 03 OBJECTIVES 04 SIGNIFICANCE OF 04 OBJECTIVES COMPANY PROFILE 04 BOARD OF DIRECTORS 07 PRODUCT LINE 08 THEORITICAL 20 FRAMEWORK RESEARCH METHODOLOGY 35 FINDINGS 36 SUGGESTION 44 CONCLUSION 45 BIBLIOGRAPHY 45 ANNEXURE 46 INTRODUCTION This project is all about analysis of profitability of Britannia Industries Ltd. for last five years (2013-2017) through ratio analysis, where we have analysed company’s profitability & its impact to the business. Here, we have estimated the profitability of the company through changes in gross profit ratio, net profit ratio, operating profit ratio, net worth ratio & return on long term fund ratio. OBJECTIVES The objectives for this project are as follows: i) To enumerate the profitability of Britannia Industries ltd. through profitability ratio analysis. ii) To formulate some specific suggestion from the ratio analysis for the growth of Britannia Industries ltd. SIGNIFICANCE OF OBJECTIVES • Measuring the profitability: Profitability is the profit earning capacity of the business. This can be measured by Gross Profit, Net Profit, Expenses and Other Ratios. If these ratios fall we can take corrective measures. • Facilitating comparative analysis: Present performance can be compared with past performance to discover the plus and minus points. Comparison with the performance of other competitive firms can also be made. -

In Every Relationship Titan Company Limited

IN EVERY RELATIONSHIP TITAN COMPANY LIMITED ANNUAL REPORT 2017-18 Announcement We are taking our first steps to move ANNUAL REPORT to Integrated Reporting in line with our continuous commitment to 2017-18 voluntarily disclose more information to our stakeholders on all aspects of our business. Accordingly, we have introduced key content elements of Integrated Reporting <IR> aligned to the Integrated Reporting Council Framework (IIRC) and as per SEBI’s circular dated 6 February 2017. We will add more IR content elements over the years as we move towards a complete <IR>. It is possible that some IR related data Contents are management estimates. Reporting Principle Financial Statements About TItaN The financial and statutory data presented in this Report is in line with 02 Financial Highlights Standalone Financial the requirements of the 03 Operating Context Statements Companies Act, 2013 (including 04 The Titan Journey 116 Independent the Rules made thereunder), Indian 06 Titan Today Auditor’s Report Accounting Standards, the Securities 08 Business Review 112 Balance Sheet and Exchange Board of India 18 Journey towards 113 Profit & Loss Account (Listing Obligations and Disclosure Integrated Reporting 115 Cash Flow Statement Requirements) Regulations, 2015 and 26 Engaging with 117 Significant accounting the Secretarial Standards. our Stakeholders policies 28 Outlook and Opportunities 130 Notes to Financial The non-financial section of the Report 30 People and Culture Statements is guided by the framework of the 31 Leadership Development International Integrated Reporting 32 Purity of Intent Consolidated Financial Council (IIRC), Securities and Exchange Statements 34 Board Of Directors Board of India and Principles of 130 AOC-1 36 Awards National Voluntary Guidelines on 169 Independent Auditor’s social, environmental and economic Report responsibilities of business. -

Equity-Thematic

EQUITY-THEMATIC NET ASSET VALUE Option NAV (` ) Reg-Plan-Dividend 9.5442 Reg-Plan-Growth 9.5441 Dir-Plan-Dividend 9.5809 Dir-Plan-Growth 9.5808 Investment Objective The investment objective of the scheme is to provide long term capital appreciation by investing in a diversified basket of companies in Nifty 50 Index while aiming for minimizing the portfolio volatility. However, there is no PORTFOLIO guarantee or assurance that the investment objective of the scheme will be achieved. Stock Name (%) Of Total AUM % of AUM Derivatives Stock Name (%) Of Total AUM % of AUM Derivatives Fund Details Equity Shares HDFC Ltd. 0.95 - • Type of Scheme Dr. Reddy's Laboratories Ltd. 8.70 - Zee Entertainment An Open Ended Equity Scheme following HCL Technologies Ltd. 7.83 - Enterprises Ltd. 0.94 - minimum variance theme Britannia Industries Ltd. 7.78 - UPL Ltd. 0.94 - • Date of Allotment: 02/03/2019 Tech Mahindra Ltd. 7.61 - Bharat Petroleum Wipro Ltd. 7.56 - Corporation Ltd. 0.94 - • Report As On: 28/02/2020 Infosys Ltd. 7.48 - Reliance Industries Ltd. 0.93 - • AAUM for theMonth of February 2020 Tata Consultancy Services Ltd. 5.35 - Maruti Suzuki India Ltd. 0.93 - ` 50.14 Crores Nestle India Ltd. 3.81 - JSW Steel Ltd. 0.93 - • AUM as on February 28, 2020 Cipla Ltd. 2.50 - Bharti Infratel Ltd. 0.93 - ` 46.59 Crores Power Grid Corporation Mahindra & Mahindra Ltd. 0.92 - • Fund Manager: Mr. Raviprakash Sharma Of India Ltd. 2.11 - Hero Motocorp Ltd. 0.90 - Managing Since: March-2019 Kotak Mahindra Bank Ltd. 1.33 - ITC Ltd. -

Bajaj Finserv (BAFINS)

Bajaj Finserv (BAFINS) CMP: | 11000 Target: | 11500 (5%) Target Period: 12 months HOLD April 30, 2021 Gradual revival in finance; insurance picks pace Bajaj Finserv reported a mixed performance with a gradual pick-up in lending business and robust growth in life insurance while general insurance momentum was slower. Consolidated topline grew 15.7% YoY to | 15387 crore, led by improved traction in insurance business, partially offset by moderation in lending business. Consolidated earnings increased 4x YoY to | 980 crore with improvement in all segments. Particulars Consolidated AUM witnessed QoQ growth of 4% YoY to | 152947 crore, led Particular Amount by mortgages. NII remained broadly flat YoY at | 4,659 crore. Lower Market Update Result | 176612 crore provision at | 1230 crore led to higher earnings at | 1346 crore, up 42% YoY Capitalization and 18% QoQ. Asset quality has synced with proforma GNPA, NNPA by Q4 Net worth | 35830 crore reaching at 1.79%, 0.75% (post ~| 2000 crore i.e. 1.3% write-off in Q4) from 52 week H/L (|) 11299 /3986 proforma GNPA, NNPA of 2.86%, 1.22%, respectively, in Q3FY21. Face value | 5 Gross written premium (GWP) in general insurance increased 5% YoY to DII Holding (%) 6.1 | 2787 crore. Excluding crop insurance, GWP increased 10% YoY to | 2663 FII Holding (%) 9.1 crore. The 2-W, 4-W saw healthy growth at 21.4%, 27.9%, respectively, but CV business (especially passenger CV) remains muted with de-growth of Key Highlights 2%. Growth in retail health business moderates. Stance on group health insurance still continues to remain cautious. -

John Hancock Emerging Markets Fund

John Hancock Emerging Markets Fund Quarterly portfolio holdings 5/31/2021 Fund’s investments As of 5-31-21 (unaudited) Shares Value Common stocks 98.2% $200,999,813 (Cost $136,665,998) Australia 0.0% 68,087 MMG, Ltd. (A) 112,000 68,087 Belgium 0.0% 39,744 Titan Cement International SA (A) 1,861 39,744 Brazil 4.2% 8,517,702 AES Brasil Energia SA 14,898 40,592 Aliansce Sonae Shopping Centers SA 3,800 21,896 Alliar Medicos A Frente SA (A) 3,900 8,553 Alupar Investimento SA 7,050 36,713 Ambev SA, ADR 62,009 214,551 Arezzo Industria e Comercio SA 1,094 18,688 Atacadao SA 7,500 31,530 B2W Cia Digital (A) 1,700 19,535 B3 SA - Brasil Bolsa Balcao 90,234 302,644 Banco Bradesco SA 18,310 80,311 Banco BTG Pactual SA 3,588 84,638 Banco do Brasil SA 15,837 101,919 Banco Inter SA 3,300 14,088 Banco Santander Brasil SA 3,800 29,748 BB Seguridade Participacoes SA 8,229 36,932 BR Malls Participacoes SA (A) 28,804 62,453 BR Properties SA 8,524 15,489 BrasilAgro - Company Brasileira de Propriedades Agricolas 2,247 13,581 Braskem SA, ADR (A) 4,563 90,667 BRF SA (A) 18,790 92,838 Camil Alimentos SA 11,340 21,541 CCR SA 34,669 92,199 Centrais Eletricas Brasileiras SA 5,600 46,343 Cia Brasileira de Distribuicao 8,517 63,718 Cia de Locacao das Americas 18,348 93,294 Cia de Saneamento Basico do Estado de Sao Paulo 8,299 63,631 Cia de Saneamento de Minas Gerais-COPASA 4,505 14,816 Cia de Saneamento do Parana 3,000 2,337 Cia de Saneamento do Parana, Unit 8,545 33,283 Cia Energetica de Minas Gerais 8,594 27,209 Cia Hering 4,235 27,141 Cia Paranaense de Energia 3,200 -

Model Portfolio Update

Model Portfolio update January 21, 2016 LatestDeal Team Model – PortfolioAt Your Service Large cap Midcap Name of the company Weightage(%) Name of the company Weightage(%) Auto 14 Aviation 6 Tata Motor DVR 4 Interglobe Aviation 6 Bosch 3 Auto 6 Maruti 4 Bharat Forge 6 EICHER Motors 3 BFSI 6 BFSI 23 BjjFiBajaj Finserve 6 HDFC Bank 8 Capital Goods 6 Axis Bank 3 HDFC 8 Bharat Electronics 6 Bajaj Finance 4 Cement 6 Capital Goods 5 Ramco Cement 6 L & T 5 Consumer 24 Cement 3 Symphony 6 UltraTech Cement 3 Supreme Ind 6 FMCG/Consumer 14 Kansai Nerolac 6 ITC 7 Pidilite 6 United Spirits 2 FMCG 8 Asian Paints 5 Nestle 8 IT 21 Infrastructure 8 Infosys 10 NBCC 8 TCS 8 Oil & Gas 6 Wipro 3 Meida 2 CtlCastrol 6 Zee Entertainment 2 Logistics 6 Metal 2 Container Corporation of India 6 Tata Steel 2 Pharma 12 Oil & Gas 4 Natco Pharma 6 Reliance Industries 4 Torrent Pharma 6 Pharma 12 Textile 6 Lupin 5 Arvind 6 Dr Reddys 4 Total 100 Aurobindo Pharma 3 Total 100 • Exclusion - Eicher Motors, Bajaj Finance (transferred to large cap), PVR, • Exclusion- State Bank of India, Bharti Airtel and ONGC CARE, Cummins & Shree Cement • Inclusion – Eicher Motors, Bajaj Finance (transferred from midcap), Wipro, • Inclusion – Ramco Cement, Bajaj Finserv, Supreme Industries, Indigo, Reliance Industries & Aurobindo Pharma Pidilite, Bharat Electronics and Bharat Forge Source: Bloomberg, ICICIdirect.com Research *Diversified portfolio - Combination of 70% large cap and 30% midcap portfolio OutperformanceDeal Team – At continues Your Service across all portfolios… • Our indicative large cap equity model portfolio (“Quality -20”) has • In the large cap space we continue to remain positive on pharma & IT. -

Bajaj Finserv (BAFINS)

Bajaj Finserv (BAFINS) CMP: | 5983 Target: | 7000 (17%) Target Period: 12 months BUY October 22, 2020 Steady revival & holdco discount remains favourable Bajaj Finserv reported steady traction in its lending business. With slower premium accretion for Bajaj Finserv, consolidated topline was up 5.8% YoY to | 15052 crore, lower compared to earlier run rate, due to moderation in the lending business. While the insurance business witnessed an improvement in earnings, contingent provisioning of | 1370 crore impacted consolidated earnings reported at | 986 crore, down 18% YoY. Particulars Amid lockdown & risk aversion, AUM remained flat at | 137300 crore. Particu lar Am o u n t Subsequently, NII growth came in at 4% YoY to | 4158 crore. Contingent Market C apitalization | 93801 crore Result Update Result provision of | 1370 crore was partially offset by tight cost control, leading to Net worth | 32243 crore 14% YoY growth in operating profit to | 3005 crore. PAT came in at | 965 52 week H/L (|) 10297/3986 crore, down 36% YoY and flat QoQ. Asset quality improved amid standstill E quity capital | 80 C rore classification with GNPA at 1.03% vs 1.4% in Q1FY21. F ace value | 5 DII Holding (% ) 6.8 The pick-up seen in premium accretion in general insurance was at | 4156 FII Holding (% ) 7.7 crore, down 3% YoY. Crop insurance premium broadly stayed flat YoY at | 1759 crore. Non crop premium declined ~6% YoY to | 2397 crore, led by Key Highlights de-growth in CV & two-wheeler due to base effect. Cautious approach led 10% de-growth in group health business though retail health insurance Healthy revival witnessed in insurance increased 28.5% in H1FY21. -

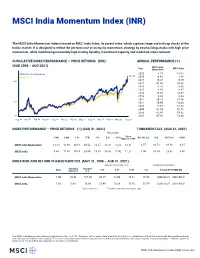

MSCI India Momentum Index (INR) (PRICE)

MSCI India Momentum Index (INR) The MSCI India Momentum Index is based on MSCI India Index, its parent index, which captures large and mid cap stocks of the Indian market. It is designed to reflect the performance of an equity momentum strategy by emphasizing stocks with high price momentum, while maintaining reasonably high trading liquidity, investment capacity and moderate index turnover. CUMULATIVE INDEX PERFORMANCE — PRICE RETURNS (INR) ANNUAL PERFORMANCE (%) (AUG 2006 – AUG 2021) MSCI India Year Momentum MSCI India MSCI India Momentum 2020 4.74 16.84 453.82 MSCI India 2019 14.91 8.46 423.96 2018 -10.28 -0.19 400 2017 47.32 28.68 2016 -1.26 -0.30 2015 -2.59 -2.97 2014 19.60 24.37 2013 9.89 6.93 2012 30.23 27.86 200 2011 -20.90 -26.33 2010 21.67 14.74 2009 68.04 91.51 2008 -62.86 -56.82 50 2007 95.83 52.49 Aug 06 Nov 07 Feb 09 May 10 Aug 11 Nov 12 Feb 14 May 15 Aug 16 Nov 17 Feb 19 May 20 Aug 21 INDEX PERFORMANCE — PRICE RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr May 31, 1996 Div Yld (%) P/E P/E Fwd P/BV MSCI India Momentum 12.03 13.69 44.58 29.22 12.27 12.31 12.22 12.31 0.57 36.78 19.56 4.15 MSCI India 8.80 11.41 50.55 24.89 13.10 13.38 11.92 11.25 1.00 31.04 23.31 3.86 INDEX RISK AND RETURN CHARACTERISTICS (MAY 31, 1996 – AUG 31, 2021) ANNUALIZED STD DEV (%) 2 MAXIMUM DRAWDOWN Tracking Turnover Beta Error (%) (%) 1 3 Yr 5 Yr 10 Yr (%) Period YYYY-MM-DD MSCI India Momentum 1.00 10.48 127.60 20.17 18.90 16.61 76.66 2000-02-21—2001-09-21 MSCI India 1.00 0.00 16.96 21.44 18.28 16.70 65.74 2000-02-21—2001-09-21 1 Last 12 months 2 Based on monthly price returns data The MSCI India Momentum Index was launched on Dec 11, 2013. -

Britannia Industries Ltd. | Aarti Industries Ltd

Market Overview Mutual Fund Overview Economy Review Technical View Prominent Headlines Stock Picks Startup Corner Commodity Monthly Round up Testimonials Monthly Insight Performance Sector Outlook: Chemical Book Review Q&A with CIO Management Meet Note Q3FY20 Result Analysis World Economic Event Calendar INSIGHT March 2020 Q&A WITH CIO Mr. Saurabh Mukherjea, Founder and Chief Investment Officer - Marcellus Investment Managers Viral Markets BRITANNIA INDUSTRIES LTD. | AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD. INSIDE THIS ISSUE Market Economy 1 overview 34 Review Prominent Startup headlines corner PROMINENT February 2020 4 39 Testimo- Sector - 6 nials Testimonial 40 Chemical Q&A with CIO Q3FY20 - Mr. Saurabh Result Analysis Mukherjea, Founder and Chief Investment Officer - Marcellus 7 Investment Managers 46 Mutual Technical 11 fund overview 64 view Stock picks Commodity monthly round up • Britannia Industries Ltd. • Aarti Industries Ltd. • Metropolis Healthcare Ltd. 15 68 Monthly Book insight review Recommendation Value Investing performance and Behavioral 24 69 Finance by Parag Parekh Management World meet note economic • Phillips Carbon Black calendar Ltd. 30 72 March 2020 INSIGHT 2 MarketOVERVIEW The coronavirus code named as COVID-19 has turned out to be a new scare for the world markets and have beaten previous records of notorious SARS though the positive thing is the mortality rate which is around 2% in comparison to earlier epidemic outbreaks. 1 INSIGHT March 2020 s the number of death 2018 alone, 30% of growth in world have estimated that even after ease toll has already crossed GDP is contributed by China. These of lockdown in March, Chinese 2,762 worldwide while the data thus signify that a massive economy could experience largest total number of infected impact on China’s GDP will not spare quarterly drop due to simultaneous Apeople at more than 80,000. -

Corporate Governance Scores S&P BSE 100 Companies

Corporate Governance Scores S&P BSE 100 companies Technical Partner Supported by the Government of Japan January 2018 TABLE OF CONTENTS Foreword 2 1 Introduction 4 2 SENSEX Trends 6 3 S&P BSE 100 Findings 8 4 Conclusion 12 5 Annexures 13 6 1 1. FOREWORD Vladislava Ryabota Regional Lead for Corporate Governance in South Asia, IFC Welcome to this second report on the Indian Corporate Governance Scorecard, developed jointly by the BSE, IFC and Institutional Investor Advisory Services (IiAS), with the financial support of the Government of Japan. The goal of a scorecard is to provide a fair assessment of corporate governance practices at the corporate level. This, in return, gives investors, regulators and stakeholders key information to help them in their decisions with regards to such companies. Since we started this journey in India, with our first scorecard issued in December 2016, a lot of dynamic changes have been set in motion. For instance, the scorecard of 2016 scored 30 companies, and now we have a 100 in this year’s edition. We were also happy to notice that several best practice requirements, covered by the scoring methodology, have been recommended by the Kotak Committee, formed in 2017 at the initiative of the Securities and Exchange Board of India. Changes have also taken place at the regulatory level to incite investors to take a more active role at Annual General Assemblies and vote in order to bring positive changes in the practices of their investee companies. All these changes form part of an overall dynamic aimed at helping the private sector raise its visibility in India and throughout the world and IFC is proud to be a solid partner and actor to this initiative. -

Directors Ceased

Bajaj Finserv Limited Note on cessation of Directors due to death or resignation 1. Cessation of directorship of Late Shri S H Khan on account of sad demise Shri S H Khan, an Independent Director of the Company since 2008 passed away on 12 January 2016. He was 77 years old. Shri Khan served on various committees including Audit Committee and the Nomination and Remuneration Committee (Chairman) of the Company. He was also on the boards of other Bajaj Group companies, including the two insurance companies. The Board of Directors of the Company at its meeting held on 3 February 2016 recorded its whole- hearted appreciation of the valuable contribution made by Shri S H Khan during his long tenure as a member of the Board and noted his sad demise. 2. Cessation of directorship of Late Shri Naresh Chandra on account of sad demise Shri Naresh Chandra, an Independent Director of the Company since 11 September 2008, passed away in Goa on 9 July 2017. He was 82 years old. He was a member of the Audit Committee and Chairman of the Nomination and Remuneration Committee. The Board of Directors of the Company at its meeting held on 19 July 2017 recorded its whole- hearted appreciation of the valuable contribution made by Shri Naresh Chandra during his long tenure as a member of the Board and noted his sad demise. 3. Resignation of Shri Rahul Bajaj as a Non-Executive Chairman of the Company Shri Rahul Bajaj, Non-Executive Chairman of the Company, having been at the helm of the Company since its inception in 2007 and the Group for around five decades, as part of succession planning, has expressed his intention to step down as the Non-Executive Chairman of the Company with effect from the conclusion of Board meeting of the Company scheduled on 16 May 2019.