Profitability of Britannia Industries Limited”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sun Life Excel India Fund

SUN LIFE EXCEL INDIA FUND Summary of Investment Portfolio* as at September 30, 2020 Top 25 Investments³ Sector Allocation³ Percentage of Net Asset Percentage of Net Asset Holding Name Value of the Fund (%) Value of the Fund % 1 Reliance Industries Limited 8.6 Financials 23.9 2 Infosys Limited 8.5 Information Technology 12.3 3 iShares MSCI India ETF 8.1 Energy 9.3 4 ICICI Bank Limited 7.3 Exchange-Traded Funds - International 5 HDFC Bank Limited 3.9 Equities 8.1 6 HCL Technologies Limited 3.7 Consumer Staples 7.6 7 Bharti Airtel Limited 3.7 Consumer Discretionary 7.1 8 Housing Development Finance Corporation Limited 3.5 Health Care 7.0 9 Hindustan Unilever Limited 3.1 Other Assets less Liabilities 5.7 10 Axis Bank Limited 2.3 Materials 4.7 11 Kotak Mahindra Bank Limited 2.0 Communication Services 4.6 12 Maruti Suzuki India Limited 2.0 Industrials 4.5 13 Mahindra & Mahindra Limited 2.0 Cash and Cash Equivalents 3.1 14 Bajaj Finance Limited 1.9 Real Estate 2.1 15 Dalmia Bharat Limited 1.6 100.0 16 Strides Pharma Science Limited 1.5 17 Dabur India Limited 1.4 Asset Allocation³ 18 Polycab India Limited 1.4 19 Aster DM Healthcare Limited 1.3 Percentage of Net Asset Value of the Fund % 20 Trent Limited 1.3 21 Britannia Industries Limited 1.3 International Equities 91.2 22 Sun Pharmaceutical Industries Limited 1.3 Other Assets less Liabilities 5.7 23 Motherson Sumi Systems Limited 1.3 Cash and Cash Equivalents 3.1 24 Clearing Corporation of India Limited 1.2 100.0 25 UltraTech Cement Limited 1.2 ³ 75.4 Geographic Allocation Total Net Asset Value (©000©s) $ 203,711 Percentage of Net Asset Value of the Fund % India 91.2 Other Assets less Liabilities 5.7 Cash and Cash Equivalents 3.1 100.0 (*) All information is as at September 30, 2020. -

Equity-Thematic

EQUITY-THEMATIC NET ASSET VALUE Option NAV (` ) Reg-Plan-Dividend 9.5442 Reg-Plan-Growth 9.5441 Dir-Plan-Dividend 9.5809 Dir-Plan-Growth 9.5808 Investment Objective The investment objective of the scheme is to provide long term capital appreciation by investing in a diversified basket of companies in Nifty 50 Index while aiming for minimizing the portfolio volatility. However, there is no PORTFOLIO guarantee or assurance that the investment objective of the scheme will be achieved. Stock Name (%) Of Total AUM % of AUM Derivatives Stock Name (%) Of Total AUM % of AUM Derivatives Fund Details Equity Shares HDFC Ltd. 0.95 - • Type of Scheme Dr. Reddy's Laboratories Ltd. 8.70 - Zee Entertainment An Open Ended Equity Scheme following HCL Technologies Ltd. 7.83 - Enterprises Ltd. 0.94 - minimum variance theme Britannia Industries Ltd. 7.78 - UPL Ltd. 0.94 - • Date of Allotment: 02/03/2019 Tech Mahindra Ltd. 7.61 - Bharat Petroleum Wipro Ltd. 7.56 - Corporation Ltd. 0.94 - • Report As On: 28/02/2020 Infosys Ltd. 7.48 - Reliance Industries Ltd. 0.93 - • AAUM for theMonth of February 2020 Tata Consultancy Services Ltd. 5.35 - Maruti Suzuki India Ltd. 0.93 - ` 50.14 Crores Nestle India Ltd. 3.81 - JSW Steel Ltd. 0.93 - • AUM as on February 28, 2020 Cipla Ltd. 2.50 - Bharti Infratel Ltd. 0.93 - ` 46.59 Crores Power Grid Corporation Mahindra & Mahindra Ltd. 0.92 - • Fund Manager: Mr. Raviprakash Sharma Of India Ltd. 2.11 - Hero Motocorp Ltd. 0.90 - Managing Since: March-2019 Kotak Mahindra Bank Ltd. 1.33 - ITC Ltd. -

Britannia Industries Ltd. | Aarti Industries Ltd

Market Overview Mutual Fund Overview Economy Review Technical View Prominent Headlines Stock Picks Startup Corner Commodity Monthly Round up Testimonials Monthly Insight Performance Sector Outlook: Chemical Book Review Q&A with CIO Management Meet Note Q3FY20 Result Analysis World Economic Event Calendar INSIGHT March 2020 Q&A WITH CIO Mr. Saurabh Mukherjea, Founder and Chief Investment Officer - Marcellus Investment Managers Viral Markets BRITANNIA INDUSTRIES LTD. | AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD. INSIDE THIS ISSUE Market Economy 1 overview 34 Review Prominent Startup headlines corner PROMINENT February 2020 4 39 Testimo- Sector - 6 nials Testimonial 40 Chemical Q&A with CIO Q3FY20 - Mr. Saurabh Result Analysis Mukherjea, Founder and Chief Investment Officer - Marcellus 7 Investment Managers 46 Mutual Technical 11 fund overview 64 view Stock picks Commodity monthly round up • Britannia Industries Ltd. • Aarti Industries Ltd. • Metropolis Healthcare Ltd. 15 68 Monthly Book insight review Recommendation Value Investing performance and Behavioral 24 69 Finance by Parag Parekh Management World meet note economic • Phillips Carbon Black calendar Ltd. 30 72 March 2020 INSIGHT 2 MarketOVERVIEW The coronavirus code named as COVID-19 has turned out to be a new scare for the world markets and have beaten previous records of notorious SARS though the positive thing is the mortality rate which is around 2% in comparison to earlier epidemic outbreaks. 1 INSIGHT March 2020 s the number of death 2018 alone, 30% of growth in world have estimated that even after ease toll has already crossed GDP is contributed by China. These of lockdown in March, Chinese 2,762 worldwide while the data thus signify that a massive economy could experience largest total number of infected impact on China’s GDP will not spare quarterly drop due to simultaneous Apeople at more than 80,000. -

Investing in Partnerships

INVESTING IN PARTNERSHIPS SYNGENE INTERNATIONAL LIMITED Biocon SEZ, Biocon Park, Plot No. 2 & 3, Bommasandra Industrial Area, IV Phase, Jigani Link Road, Bengaluru - 560 099, Karnataka, India. ANNUAL REPORT 2018-19 CONTENTS Business Review About us 02 Inspiring us on our path 07 Financial Highlights 08 The Syngene Journey 10 Managing Director’s Message 12 CEO’s Operational Review 14 CFO’s Financial Review 18 The cover image depicts The Marketplace 21 embryological development, which epitomises the Our Business Model 22 continuous process of growth. Dedicated R&D Centres 24 At Syngene, the aim behind Discovery Services 26 investing in our partnerships Leveraging Bioinformatics in is inspired from this infinitely Drug Discovery & Development 30 small cell. We believe that when we connect and collaborate Development & Manufacturing Services 32 with our stakeholders, we will, Every Client Matters 34 just like the cell embryo, set Investing in Quality 36 up a continuous process of Investing in Information Technology 37 development, benefitting all who are directly or indirectly Investing in Supply Chain 38 connected with the Company. Investing in People 40 Investing for Long-Term Value Creation 42 Investing in Sustainable Operations 44 Investing in a Larger Purpose 46 Board of Directors 48 Executive Committee 50 Business Unit Heads 51 Corporate Information 52 Statutory Reports Board’s Report 53 Corporate Governance Report 89 Business Responsibility Report 110 Management Discussion and Analysis 123 Financial Statements Standalone Financial Statements 135 Consolidated Financial Statements 190 AGM Notice 246 Glossary 265 To download or view this report online, please log on to www.syngeneintl.com/investor-relations INVESTING IN PARTNERSHIPS Syngene International Limited has always believed in the power of partnerships to unlock long-term value for its stakeholders. -

Aegon Life Indepth May 2021.Pdf

MAY 2021 IN-DEPTH INVESTMENT BULLETIN OF AEGON LIFE INSURANCE COMPANY LTD AEGON, toh tension gone. INDEX Description Page No. Enhanced Equity Fund 6 Accelerator Fund 7 Pension Enhanced Equity Fund 8 Pension Index Fund 9 Group Equity Fund 10 Blue Chip Equity Fund 11 Opportunity Fund 12 Debt Fund 14 Pension Debt Fund 15 Secure Fund 16 Pension Secure Fund 17 Conservative Fund 18 Balanced Fund 20 Pension Balanced Fund 22 Stable Fund 24 NAVPF Fund 26 Indepth | May 2021 | 2 Commentary on the Indian Securities Market for April 2021 Nifty (down 0.4%) was largely flat in April post a flattish march. The covid situation has worsened in the month of April in India leading to different levels of lockdowns in various states. The vaccination program for the age group of 18-44 years has been allowed from 1 st May. However, vaccination availability is a concern in the short term and may lead to some delays. The dollar index corrected after three months of up move. It was down 2.09% and closed at 91.28 level. Despite the fall in Dollar index, the rupee was weak and depreciated by 97 paise to close at 74.08 level. Brent Crude gained almost 6% after one month of correction and ended at 67.25 level. Gold was up by 3.6% after three months of correction. Foreign institutional investors (FIIs) investment turned negative after six month of positive inflows. They sold about $1.3 bn worth of equity in April. Domestic institutional investors (DIIs) investment continued to be positive for a second month in a row. -

Inner 32 Arbitrage Fund Low

Tata Arbitrage Fund (An open ended scheme investing in arbitrage opportunities.) As on 30th June 2020 PORTFOLIO % to % to NAV % to % to NAV Company name Company name INVESTMENT STYLE NAV Derivative NAV Derivative The scheme invests in equity and equity related instruments that tries Hedge Positions 65.55 -65.33 Punjab National Bank 0.34 -0.34 to take advantage of the difference in prices of a security in the cash Reliance Industries Ltd. 2.34 -2.33 Sun Tv Network Ltd. 0.32 -0.32 segment and derivatives segment by turning market volatility to its ICICI Bank Ltd. 2.14 -2.13 Hindalco Industries Ltd. 0.29 -0.29 advantage. Housing Development Finance Corporation Ltd. 2.12 -2.10 ICICI Prudential Life Insurance Company Ltd. 0.24 -0.24 ITC Ltd. 1.94 -1.94 Axis Bank Ltd. 0.22 -0.22 INVESTMENT OBJECTIVE Tata Consumer Products Ltd. 1.54 -1.54 Larsen & Toubro Ltd. 0.22 -0.22 The investment objective of the Scheme is to seek to generate Sbi Life Insurance Company Ltd. 1.53 -1.53 Gmr Infrastucture Ltd. 0.20 -0.20 HCL Technologies Ltd. 1.52 -1.51 Mindtree Ltd. 0.17 -0.17 reasonable returns by investing predominantly in arbitrage Colgate-Palmolive India Ltd. 1.46 -1.46 Coal India Ltd. 0.16 -0.15 opportunities in the cash and derivatives segments of the equity Titan Company Ltd. 1.44 -1.44 Mahanagar Gas Ltd. 0.15 -0.15 markets and by investing balance in debt and money market Hindustan Unilever Ltd. 1.42 -1.42 Century Textiles & Industries Ltd. -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines. -

Loan Against Securities – Approved Single Scrip

Loan against securities – Approved single scrip Security ISIN Code Scrip Name Type Margin INE769A01020 AARTI INDUSTRIES Single Scrip 50 INE012A01025 ACC LIMITED Single Scrip 50 INE079A01024 AMBUJA CEMENTS LTD Single Scrip 50 INE437A01024 APOLLO HOSPITALS ENTERPRISE LTD Single Scrip 50 INE208A01029 ASHOK LEYLAND LTD Single Scrip 50 INE021A01026 ASIAN PAINTS LTD Single Scrip 50 INE406A01037 AUROBINDO PHARMA LTD Single Scrip 50 INE192R01011 AVENUE SUPERMARTS Single Scrip 50 INE917I01010 BAJAJ AUTO LTD Single Scrip 50 INE296A01024 BAJAJ FINANCE LTD Single Scrip 50 INE028A01039 BANK OF BARODA Single Scrip 50 INE084A01016 BANK OF INDIA Single Scrip 50 INE463A01038 BERGER PAINTS INDIA LTD Single Scrip 50 INE029A01011 BHARAT PETROLEUM CORPORATION LTD Single Scrip 50 INE323A01026 BOSCH LTD Single Scrip 50 INE216A01030 BRITANNIA INDUSTRIES LIMITED Single Scrip 50 INE010B01027 CADILA HEALTHCARE LTD Single Scrip 50 INE476A01014 CANARA BANK Single Scrip 50 INE172A01027 CASTROL INDIA LTD Single Scrip 50 INE059A01026 CIPLA LTD Single Scrip 50 INE522F01014 COAL INDIA LTD Single Scrip 50 INE259A01022 COLGATE-PALMOLIVE (INDIA) LTD Single Scrip 50 INE016A01026 DABUR INDIA LTD Single Scrip 50 INE361B01024 DIVIS LABORATORIES LTD Single Scrip 50 INE089A01023 DRREDDYS LABORATORIES LTD Single Scrip 50 INE066A01021 EICHER MOTORS LIMITED Single Scrip 50 INE302A01020 EXIDE INDUSTRIES LTD Single Scrip 50 INE129A01019 GAIL (INDIA) LTD Single Scrip 50 INE176B01034 HAVELLS INDIA LTD Single Scrip 50 INE860A01027 HCL TECHNOLOGIES LTD Single Scrip 50 INE040A01034 HDFC -

Aegon Life Indepth Mar 2021

MARCH 2021 IN-DEPTH INVESTMENT BULLETIN OF AEGON LIFE INSURANCE COMPANY LTD AEGON, toh tension gone. INDEX Description Page No. Enhanced Equity Fund 6 Accelerator Fund 7 Pension Enhanced Equity Fund 8 Pension Index Fund 9 Group Equity Fund 10 Blue Chip Equity Fund 11 Opportunity Fund 12 Debt Fund 14 Pension Debt Fund 15 Secure Fund 16 Pension Secure Fund 17 Conservative Fund 18 Balanced Fund 20 Pension Balanced Fund 22 Stable Fund 24 NAVPF Fund 26 Indepth | Mar 2021 | 2 Commentary on the Indian Securities Market for February 2021 Nifty (up 6.5%) was up for the month after a correction in January as the markets were enthused by a pro-growth Budget. In the budget, the government signalled its inten- tion to support growth without any meaningful change in tax regime. The active covid cases has seen a slight uptick in the month of February. The vaccination program has entered the second phase in the country with senior citizens and comorbid patients also eligible to receive vaccination from 1st March. The dollar index was up for second month in a row. It was up 0.3% and closed at 90.88 level. The rupee depreciated after three months of appreciation. It depreciated by 51 paise to end at 73.46 level. Brent crude continued its upmove and was up another 18% to close above $65 mark. It has moved up by 78% in the last four months. Gold corrected by 6% to close at $1734. Foreign institutional investors (FIIs) investment continued to be strong in February with inflow of $3.5 bn. -

Indepth Feb 2021.Pdf

FEBRUARY 2021 IN-DEPTH INVESTMENT BULLETIN OF AEGON LIFE INSURANCE COMPANY LTD AEGON, toh tension gone. INDEX Description Page No. Enhanced Equity Fund 6 Accelerator Fund 7 Pension Enhanced Equity Fund 8 Pension Index Fund 9 Group Equity Fund 10 Blue Chip Equity Fund 11 Opportunity Fund 12 Debt Fund 14 Pension Debt Fund 15 Secure Fund 16 Pension Secure Fund 17 Conservative Fund 18 Balanced Fund 20 Pension Balanced Fund 22 Stable Fund 24 NAVPF Fund 26 Indepth | Feb 2021 | 2 Commentary on the Indian Securities Market for January 2021 Nifty (down 2.5%) was marginally negative after giving positive return in the last three months. The covid cases continued to decline across the country with only two states having more than 10000 active cases now. The vaccination program has also started in the country with healthcare workers receiving the vaccination first. The dollar index took a breather after 2 consecutive months of depreciation. It was up 0.7% and closed at 90.58 level. The rupee continued to appreciate for the 3 rd month in a row and appreciated marginally by 11 paise to close at 72.95 level. Brent crude continued its upmove and was up another 8% to close above $55 mark. It has moved up by 49% in the last three months. Gold corrected by 2.67% to close at $1847. Foreign institutional investors (FIIs) investment continued to be strong in January albeit lower than last two months with inflow of $2.7 bn. Domestic institutional investors (DIIs) continued to be net sellers as outflows in Equity mutual funds continued for the sixth month in a row. -

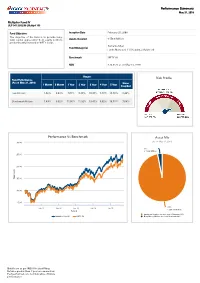

Risk Profile Performance Vs Benchmark Asset Mix Performance

Performance Summary May 31, 2019 Multiplier Fund IV ULIF 047 25/02/08 LMultip4 105 Fund Objective: Inception Date February 25, 2008 The objective of the fund is to provide long- ₹ term capital appreciation from equity portfolio Assets Invested 556.6 Million predominantly invested in NIFTY scrips. Sumanta Khan Fund Manager(s) Funds Managed: 11 (9 Equity, 2 Balanced) Benchmark NIFTY 50 NAV ₹ 24.9122 as on May 31, 2019 Return Risk Profile Fund Performance (As on May 31, 2019 ) Since 1 Month 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year Inception Fund Return 1.82% 8.43% 7.01% 8.39% 10.97% 7.78% 10.78% 8.44% Benchmark Return 1.49% 9.62% 11.05% 11.32% 13.47% 9.02% 10.51% 7.64% Performance Vs Benchmark Asset Mix (As on May 31, 2019) 30.00 3% ₹ 17.68 Million 25.00 20.00 ) ₹ V in ( NA 15.00 10.00 5.00 Jan 10 Jan 12 Jan 14 Jan 16 Jan 18 97% ₹ 538.91 Million Period Equity and Equity related securities Minimum 80% Multiplier Fund IV NIFTY 50 Debt, Money Market and Cash Maximum 20% Details are as per IRDAI Product Filing. Returns greater than 1 year are annualized. Past performance is not indicative of future performance. Performance Summary May 31, 2019 % of Invested Top 10 Sectors * Assets Financial and insurance activities 24.43% Computer programming consultancy and related activities 13.69% Manufacture of coke and refined petroleum products 10.45% Infrastructure 9.03% Manufacture of chemicals and chemical products 6.81% Manufacture of tobacco products 5.72% Manufacture of Basic Metals 1.92% Manufacture of pharmaceuticalsmedicinal chemical and botanical 1.79% products Manufacture of motor vehicles trailers and semi-trailers 1.78% Manufacture of other non-metallic mineral products 1.57% OTHERS 22.81% *As per IRDAI NIC industry classification Details are as per IRDAI Product Filing. -

Indepth Aug 2020 1

September 2020 IN-DEPTH INVESTMENT BULLETIN OF AEGON LIFE INSURANCE COMPANY LTD AEGON, toh tension gone. INDEX Description Page No. Enhanced Equity Fund 6 Accelerator Fund 7 Pension Enhanced Equity Fund 8 Pension Index Fund 9 Group Equity Fund 10 Blue Chip Equity Fund 11 Opportunity Fund 12 Debt Fund 14 Pension Debt Fund 15 Secure Fund 16 Pension Secure Fund 17 Conservative Fund 18 Balanced Fund 20 Pension Balanced Fund 22 Stable Fund 24 NAVPF Fund 26 Indepth | Aug 2020 | 2 Indian Securities Market Commentary for the month of August 2020 Indian Equities moved higher (Nifty +2.8%) in August, in line with the region and S&P which touched new highs during the month. Indian Bonds witnessed price decline as yields spiked to 6.20% for 10-year G-Sec during August before recovering to 6.12% at the end of August following announcement of Open Market Operations by RBI. Jump in inflation and a wait & watch mode adopted by the MPC could be cited as major reasons for the spike from a level of 5.76% where we ended July. Bond yields further cooled down in early September as RBI announced further OMOs and other regu- latory measures. Indian rupee appreciated by 1.6% to end the month at Rs.73.62 to a US Dollar. The price of Brent Crude has been in a range and closed the month at Dollar 45 to a barrel. Gold was steady at Dollar 1,968 for an ounce of gold. Dollar weakness, gradual re-opening of the economy and hopes of a vaccine supported sentiments for equities.