The Legislative Reform (Further Renewal of Radio Licences) Order 2015 (“The Draft Order”) Which We Propose to Make Under Section 1 of That Act

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Media Nations 2019

Media nations: UK 2019 Published 7 August 2019 Overview This is Ofcom’s second annual Media Nations report. It reviews key trends in the television and online video sectors as well as the radio and other audio sectors. Accompanying this narrative report is an interactive report which includes an extensive range of data. There are also separate reports for Northern Ireland, Scotland and Wales. The Media Nations report is a reference publication for industry, policy makers, academics and consumers. This year’s publication is particularly important as it provides evidence to inform discussions around the future of public service broadcasting, supporting the nationwide forum which Ofcom launched in July 2019: Small Screen: Big Debate. We publish this report to support our regulatory goal to research markets and to remain at the forefront of technological understanding. It addresses the requirement to undertake and make public our consumer research (as set out in Sections 14 and 15 of the Communications Act 2003). It also meets the requirements on Ofcom under Section 358 of the Communications Act 2003 to publish an annual factual and statistical report on the TV and radio sector. This year we have structured the findings into four chapters. • The total video chapter looks at trends across all types of video including traditional broadcast TV, video-on-demand services and online video. • In the second chapter, we take a deeper look at public service broadcasting and some wider aspects of broadcast TV. • The third chapter is about online video. This is where we examine in greater depth subscription video on demand and YouTube. -

Special Issue

ISSUE 750 / 19 OCTOBER 2017 15 TOP 5 MUST-READ ARTICLES record of the week } Post Malone scored Leave A Light On Billboard Hot 100 No. 1 with “sneaky” Tom Walker YouTube scheme. Relentless Records (Fader) out now Tom Walker is enjoying a meteoric rise. His new single Leave } Spotify moves A Light On, released last Friday, is a brilliant emotional piano to formalise pitch led song which builds to a crescendo of skittering drums and process for slots in pitched-up synths. Co-written and produced by Steve Mac 1 as part of the Brit List. Streaming support is big too, with top CONTENTS its Browse section. (Ed Sheeran, Clean Bandit, P!nk, Rita Ora, Liam Payne), we placement on Spotify, Apple and others helping to generate (MusicAlly) love the deliberate sense of space and depth within the mix over 50 million plays across his repertoire so far. Active on which allows Tom’s powerful vocals to resonate with strength. the road, he is currently supporting The Script in the US and P2 Editorial: Paul Scaife, } Universal Music Support for the Glasgow-born, Manchester-raised singer has will embark on an eight date UK headline tour next month RotD at 15 years announces been building all year with TV performances at Glastonbury including a London show at The Garage on 29 November P8 Special feature: ‘accelerator Treehouse on BBC2 and on the Today Show in the US. before hotfooting across Europe with Hurts. With the quality Happy Birthday engagement network’. Recent press includes Sunday Times Culture “Breaking Act”, of this single, Tom’s on the edge of the big time and we’re Record of the Day! (PRNewswire) The Sun (Bizarre), Pigeons & Planes, Clash, Shortlist and certain to see him in the mix for Brits Critics’ Choice for 2018. -

Jeff Smith Head of Music, BBC Radio 2 and 6 Music Media Masters – August 16, 2018 Listen to the Podcast Online, Visit

Jeff Smith Head of Music, BBC Radio 2 and 6 Music Media Masters – August 16, 2018 Listen to the podcast online, visit www.mediamasters.fm Welcome to Media Masters, a series of one to one interviews with people at the top of the media game. Today, I’m here in the studios of BBC 6 Music and joined by Jeff Smith, the man who has chosen the tracks that we’ve been listening to on the radio for years. Now head of music for BBC Radio 2 and BBC Radio 6 Music, Jeff spent most of his career in music. Previously he was head of music for Radio 1 in the late 90s, and has since worked at Capital FM and Napster. In his current role, he is tasked with shaping music policy for two of the BBC’s most popular radio stations, as the technology of how we listen to music is transforming. Jeff, thank you for joining me. Pleasure. Jeff, Radio 2 has a phenomenal 15 million listeners. How do you ensure that the music selection appeals to such a vast audience? It’s a challenge, obviously, to keep that appeal across the board with those listeners, but it appears to be working. As you say, we’re attracting 15.4 million listeners every week, and I think it’s because I try to keep a balance of the best of the best new music, with classic tracks from a whole range of eras, way back to the 60s and 70s. So I think it’s that challenge of just making that mix work and making it work in terms of daytime, and not only just keeping a kind of core audience happy, but appealing to a new audience who would find that exciting and fun to listen to. -

Domain Stationid Station UDC Performance Date

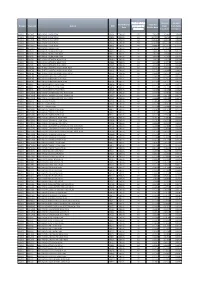

Number of days Amount Amount Performance Total Per Domain StationId Station UDC processed for from from Public Date Minute Rate distribution Broadcast Reception RADIO BR ONE BBC RADIO 1 NON PEAK BRA01 CENSUS 92 7.8347 4.2881 3.5466 RADIO BR ONE BBC RADIO 1 LOW PEAK BRB01 CENSUS 92 10.7078 7.1612 3.5466 RADIO BR ONE BBC RADIO 1 HIGH PEAK BRC01 CENSUS 92 13.5380 9.9913 3.5466 RADIO BR TWO BBC RADIO 2 NON PEAK BRA02 CENSUS 92 17.4596 11.2373 6.2223 RADIO BR TWO BBC RADIO 2 LOW PEAK BRB02 CENSUS 92 24.9887 18.7663 6.2223 RADIO BR TWO BBC RADIO 2 HIGH PEAK BRC02 CENSUS 92 32.4053 26.1830 6.2223 RADIO BR1EXT BBC RADIO 1XTRA NON PEAK BRA10 CENSUS 92 1.4814 1.4075 0.0739 RADIO BR1EXT BBC RADIO 1XTRA LOW PEAK BRB10 CENSUS 92 2.4245 2.3506 0.0739 RADIO BR1EXT BBC RADIO 1XTRA HIGH PEAK BRC10 CENSUS 92 3.3534 3.2795 0.0739 RADIO BRASIA BBC ASIAN NETWORK NON PEAK BRA65 CENSUS 92 1.4691 1.4593 0.0098 RADIO BRASIA BBC ASIAN NETWORK LOW PEAK BRB65 CENSUS 92 2.4468 2.4371 0.0098 RADIO BRASIA BBC ASIAN NETWORK HIGH PEAK BRC65 CENSUS 92 3.4100 3.4003 0.0098 RADIO BRBEDS BBC THREE COUNTIES RADIO NON PEAK BRA62 CENSUS 92 0.1516 0.1104 0.0411 RADIO BRBEDS BBC THREE COUNTIES RADIO LOW PEAK BRB62 CENSUS 92 0.2256 0.1844 0.0411 RADIO BRBEDS BBC THREE COUNTIES RADIO HIGH PEAK BRC62 CENSUS 92 0.2985 0.2573 0.0411 RADIO BRBERK BBC RADIO BERKSHIRE NON PEAK BRA64 CENSUS 92 0.0803 0.0569 0.0233 RADIO BRBERK BBC RADIO BERKSHIRE LOW PEAK BRB64 CENSUS 92 0.1184 0.0951 0.0233 RADIO BRBERK BBC RADIO BERKSHIRE HIGH PEAK BRC64 CENSUS 92 0.1560 0.1327 0.0233 RADIO BRBRIS BBC -

Radio Harrow

Community radio application form 1. Station Name Guidance Notes This is the name you expect to use to identify the station What is the proposed station name? on air. Radio Harrow 2. Community to be served Guidance Notes Define the community or communities you are It is a legislative requirement that a service is intended proposing to serve. Drawing from various sources of primarily to serve one or more communities (whether or data (e.g. from the Office of Population, Census and not it also serves other members of the public) and we Survey) and in relation to your proposed coverage need to understand who comprises that community or area, please determine the size of the population communities. The target community will also be concerned and the make-up of the population as a specified in the licence, if this application is successful. whole, along with any relevant socio-economic The legislation defines a ‘community’ as: people who live information that would support your application. or work or undergo education or training in a particular (Please tell us the sources of the information you area or locality, or people who have one or more provide.) interests or characteristics in common. Radio Harrow will serve a diverse and growing community living in the London Borough of Harrow, an outer London Borough in North West London and approximately 10 miles from central London. Covering 50 square kilometres, Harrow is the 12th largest borough in Greater London in terms of area, but 20th in terms of size of population (249,800) with an average population density of 49.5 persons per hectare. -

Public File Nation Radio Scotland Operated by Nation Radio Scotland Limited

Public File Nation Radio Scotland operated by Nation Radio Scotland Limited Nation Radio Scotland Limited is part of the Nation Broadcasting Group. Like each local commercial station in the UK has obligations with regard to its programmes, including its music and local content. These obligations are set out in the station Format which forms part of our Public File. The Public File is just one indicator of our output. Just ask us if you’d like a hard copy. If you have any comments on it, let us know or, if necessary, contact our regulator, Ofcom. Emergency measures - statement Since 1 April 2020, we have undertaken a number of measures to programming on our stations across the UK in the light of changing resourcing availability and income. Nation Radio Scotland is currently sharing programmes with Your Radio. In the case of Your Radio we felt that in order to provide a continued service of music, news and entertainment to listeners Dumbarton and Helensburgh it was a better use of our resources to relay Nation Radio Scotland on a temporary basis. We have also made some changes to the volume and location of presenters on the station during local hours in light of reduced resourcing and income. We’ve kept Ofcom fully informed of the steps we are taking and will review the situation regularly in light of the continuing UK emergency situation. We have also applied to Ofcom for the flexibility to adopt these changes within the station format and reduce local programming hours in line with the latest localness guidelines. -

Media Culture for a Modern Nation? Theatre, Cinema and Radio in Early Twentieth-Century Scotland

Media Culture for a Modern Nation? Theatre, Cinema and Radio in Early Twentieth-Century Scotland a study © Adrienne Clare Scullion Thesis submitted for the degree of PhD to the Department of Theatre, Film and Television Studies, Faculty of Arts, University of Glasgow. March 1992 ProQuest Number: 13818929 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 13818929 Published by ProQuest LLC(2018). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 Frontispiece The Clachan, Scottish Exhibition of National History, Art and Industry, 1911. (T R Annan and Sons Ltd., Glasgow) GLASGOW UNIVERSITY library Abstract This study investigates the cultural scene in Scotland in the period from the 1880s to 1939. The project focuses on the effects in Scotland of the development of the new media of film and wireless. It addresses question as to what changes, over the first decades of the twentieth century, these two revolutionary forms of public technology effect on the established entertainment system in Scotland and on the Scottish experience of culture. The study presents a broad view of the cultural scene in Scotland over the period: discusses contemporary politics; considers established and new theatrical activity; examines the development of a film culture; and investigates the expansion of broadcast wireless and its influence on indigenous theatre. -

Laissez-Faire Regulation, the Public Spending Squeeze and the Drive to Digital Guy Starkey*

Cultural Trends, 2015 http://dx.doi.org/10.1080/09548963.2014.1000591 COMMENTARY 5 Cultural policy in the coalition years: Laissez-faire regulation, the public spending squeeze and the drive to digital Guy Starkey* 10 Centre for Research in Media & Cultural Studies, University of Sunderland, Sunderland, UK Introduction Radio, so often described by academics as the “invisible” (Lewis & Booth, 1989), “Cinder- ” – “ ” 15 ella (Halesworth, 1971, pp. 189 191) or even forgotten medium (Pease & Dennis, 1994), has enjoyed a relatively settled period under the coalition government. There has been no crisis of confidence over ethical and legal issues, as exposed in the press by Leveson and the police operations, Elveden, Tuleta and Weeting. There have been few head- line-grabbing (if difficult-to-evaluate) initiatives like local television, as exemplified by London Live or Made in Tyne & Wear, and no government-rocking conflicts of interest as 20 spectacular as that over the ownership of BSkyB. Nor indeed has there been any game-chan- ging reorganisation of public funding, similar to the Arts Council’s lists of winners and losers. Yet, as is so often the case, radio remains a significant, but largely, ignored medium. In terms of government policy, it has suffered mixed fortunes under the five years of the coalition. Official listening figures continue to confirm recent trends in radio’s fortunes. If radio grabs 25 little of the media limelight, it remains a medium with an enviable ubiquity. It may have been slow to win audiences among younger people as large as when it broke new music and pro- vided the kind of escapism sought by youth in the 1960s and 1970s. -

Digital Switchover of Television and Radio in the United Kingdom

HOUSE OF LORDS Select Committee on Communications 2nd Report of Session 2009–10 Digital switchover of television and radio in the United Kingdom Report with Evidence Ordered to be printed 18 March 2010 and published 29 March 2010 Published by the Authority of the House of Lords London : The Stationery Office Limited £price HL Paper 100 The Select Committee on Communications The Select Committee on Communications was appointed by the House of Lords with the orders of reference “to consider communications”. Current Membership Baroness Bonham-Carter of Yarnbury Baroness Eccles of Moulton Lord Fowler (Chairman) Lord Gordon of Strathblane Baroness Howe of Idlicote Lord Inglewood Lord King of Bridgwater Lord Macdonald of Tradeston Baroness McIntosh of Hudnall Bishop of Manchester Lord Maxton Lord St John of Bletso Baroness Scott of Needham Market Publications The report and evidence of the Committee are published by The Stationery Office by Order of the House. All publications of the Committee are available on the intranet at: http://www.parliament.uk/parliamentary_committees/communications.cfm General Information General information about the House of Lords and its Committees, including guidance to witnesses, details of current inquiries and forthcoming meetings is on the internet at: http://www.parliament.uk/about_lords/about_lords.cfm Contact details All correspondence should be addressed to the Clerk of the Select Committee on Communications, Committee Office, House of Lords, London SW1A 0PW The telephone number for general enquiries is -

DATABANK INSIDE the CITY SABAH MEDDINGS the WEEK in the MARKETS the ECONOMY Consumer Prices Index Current Rate Prev

10 The Sunday Times November 11, 2018 BUSINESS Andrew Lynch LETTERS “The fee reflects the cleaning out the Royal Mail Send your letters, including food sales at M&S and the big concessions will be made for Delia’s fingers burnt by online ads outplacement amount boardroom. Don’t count on it SIGNALS full name and address, supermarkets — self-service small businesses operating charged by a major company happening soon. AND NOISE . to: The Sunday Times, tills. These are hated by most retail-type operations, but no Delia Smith’s website has administration last month for executives at this level,” 1 London Bridge Street, shoppers. Prices are lower at such concessions would been left with a sour taste owing hundreds of says Royal Mail, defending London SE1 9GF. Or email Lidl and other discounters, appear to be available for after the collapse of Switch thousands of pounds to its the Spanish practice. BBC friends [email protected] but also you can be served at businesses occupying small Concepts, a digital ad agency clients. Delia, 77 — no You can find such advice Letters may be edited a checkout quickly and with a industrial workshop or that styled itself as a tiny stranger to a competitive for senior directors on offer reunited smile. The big supermarkets warehouse units. challenger to Google. game thanks to her joint for just £10,000 if you try. Eyebrows were raised Labour didn’t work in the have forgotten they need Trevalyn Estates owns, Delia Online, a hub for ownership of Norwich FC — Quite why the former recently when it emerged 1970s, and it won’t again customers. -

Download Valuing Radio

Valuing Radio How commercial radio contributes to the UK A report by the All-Party Parliamentary Group on Commercial Radio The data within Valuing Radio is largely drawn from a 2018 survey of Radiocentre members. It is supplemented by additional research which is sourced individually. Contents 01 Introduction 03 Overview and recommendations 05 The public value of commercial radio • News and information • Economic value • Charity and community 21 Commercial radio people 27 Future of radio Introduction The APPG on Commercial Radio helps provide this important industry with a voice in parliament. With record audiences and more ways to listen than ever before, the impact of the industry should not be underestimated. While the challenges facing the sector have changed over the years, the steadfast commitment of stations to provide public value content every day remains. This new report, the first of its kind produced by the APPG, showcases the rich public value content that commercial radio provides to listeners for free. Valuing Radio explores the impact made by stations up and down the country, over and above the music and entertainment output that audiences expect. It looks particularly at radio’s role in providing news and information, the sector’s significant support for both charitable fundraising and education, in addition to work to improve diversity within the industry. Alongside this important public value content is a significant economic contribution to local economies across the UK. For the first time we have analysis on the impact of local advertising and the return on investment (ROI) that this generates for particular nations and regions of the UK. -

Pocketbook for You, in Any Print Style: Including Updated and Filtered Data, However You Want It

Hello Since 1994, Media UK - www.mediauk.com - has contained a full media directory. We now contain media news from over 50 sources, RAJAR and playlist information, the industry's widest selection of radio jobs, and much more - and it's all free. From our directory, we're proud to be able to produce a new edition of the Radio Pocket Book. We've based this on the Radio Authority version that was available when we launched 17 years ago. We hope you find it useful. Enjoy this return of an old favourite: and set mediauk.com on your browser favourites list. James Cridland Managing Director Media UK First published in Great Britain in September 2011 Copyright © 1994-2011 Not At All Bad Ltd. All Rights Reserved. mediauk.com/terms This edition produced October 18, 2011 Set in Book Antiqua Printed on dead trees Published by Not At All Bad Ltd (t/a Media UK) Registered in England, No 6312072 Registered Office (not for correspondence): 96a Curtain Road, London EC2A 3AA 020 7100 1811 [email protected] @mediauk www.mediauk.com Foreword In 1975, when I was 13, I wrote to the IBA to ask for a copy of their latest publication grandly titled Transmitting stations: a Pocket Guide. The year before I had listened with excitement to the launch of our local commercial station, Liverpool's Radio City, and wanted to find out what other stations I might be able to pick up. In those days the Guide covered TV as well as radio, which could only manage to fill two pages – but then there were only 19 “ILR” stations.