Rostov Region

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

INVEST in RUSSIA the Right Place to Invest the Business Possibiliɵ Es in Russia Are Enormous

SPECIAL ISSUE SEPTEMBER 2013 INVEST IN RUSSIA The Right Place to Invest The business possibiliƟ es in Russia are enormous. There are almost no limits in view Content EXPERT. SPECIALEXPERT. ISSUE LEGION-MEDIA IN THE MOST-FAVORED REGIME 4consequently, the consumer segment, IT sector, and At the forthcoming economic forum in Sochi, the the mining and metals complexes have benefited Krasnodar Territory will present 1,800 different most from this situation. “Gazelles”, which were investment projects to investors able to ride the wave of this opportune economic phase, can be distinguished by a gradual increase IMPLEMENTING THE BRAZILIAN SYSTEM 10 in their workload Fifteen of the forty-three investment projects an- nounced or launched from February to April, 2013 TEN THOUSAND ROUNDS OF AMMUNITION 42 in Russia are part of the machine-building complex. When companies know how to manage their costs, Import substitution and elements of an active state business grows very fast. However, in order to run a industrial policy have contributed to increasing in- business, you need to constantly structure, modern- vestment activity in this sector ize, plan, motivate and take many different factors into account A TERRITORY WITH UNIQUE OPPORTUNITIES 18 DYNAMICALLY GROWING COMPANIES The Khanty-Mansi Autonomous District has virtually IN THE MIDDLE-SIZED BUSINESS SECTOR unlimited opportunities for investors. This is con- (“GAZELLES”), 2007-2011 46 nected not only with the fact that there is a lot of oil, money and progressive investment legislation in AN IMPORTANT -

BUSINESS PROPOSAL Location: Russia, Voronezh Oblast, Podgorenski District, Belogorie Village, Communications: Asphalted Road, G

BUSINESS PROPOSAL Location: Russia, Voronezh Oblast, Podgorenski district, Belogorie village, Communications: Asphalted road, gas, water, electricity and telephone landline; Land lot category: populated land; Allowed form of exploitation: individual habitat construction; Legal status: private property; Area: 80 000 m^2. General information: This lot is territory of a now defunct agricultural machinery repair company. It is situated in Belogorie village on the right bank of Don river 7 km away from M4 Highway (Moscow – Rostov – Krasnodar – Sochi) Access is via asphalted road. Westbound, there is the Kantemirovskaya highway which runs parallel to the Don highway and allows access to roads to Kursk, Belgorod and Ukraine Belogorie is a old village with rich history, it is situated in a scenic place on the south of Voronezh oblast. This land lot possess following useful geographical properties: 1. It is situated around the middle of M4 (Don) Highway between Moscow and Krasnodar. Land lot is accessible via the road that connects Don and Kantemirovskaya highways. Travel time from Moscow to Belogorie and from Belogorie to Krasnodar is approx. 6-8 hours, in Podgorenski city nearby there is access to railroad Moscow – Adler (Sochi): all of which can make it a strategic transport hub; 2. There is bridge across Don river nearby, that connects all automotive traffic from left bank to the right bank of Don river. This is an only bridge in the region; 3. Village has artesian waters, gas, electricity and phone landlines. Technical characteristics: 1. It is a perfect rectangle with dimensions of 220*380m. A quarter of land lot area was occupied by different buildings, most of them are being demolished at the moment; 2. -

1768-1830S a Dissertation Submitted to the Faculty of the Graduate

A PLAGUE ON BOTH HOUSES?: POPULATION MOVEMENTS AND THE SPREAD OF DISEASE ACROSS THE OTTOMAN-RUSSIAN BLACK SEA FRONTIER, 1768-1830S A Dissertation submitted to the Faculty of the Graduate School of Arts and Sciences of Georgetown University in partial fulfillment of the requirements for the Degree of Doctor of Philosophy in History By Andrew Robarts, M.S.F.S. Washington, DC December 17, 2010 Copyright 2010 by Andrew Robarts All Rights Reserved ii A PLAGUE ON BOTH HOUSES?: POPULATION MOVEMENTS AND THE SPREAD OF DISEASE ACROSS THE OTTOMAN-RUSSIAN BLACK SEA FRONTIER, 1768-1830S Andrew Robarts, M.S.F.S. Dissertation Advisor: Catherine Evtuhov, Ph. D. ABSTRACT Based upon a reading of Ottoman, Russian, and Bulgarian archival documents, this dissertation examines the response by the Ottoman and Russian states to the accelerated pace of migration and spread of disease in the Black Sea region from the outbreak of the Russo-Ottoman War of 1768-1774 to the signing of the Treaty of Hünkar Iskelesi in 1833. Building upon introductory chapters on the Russian-Ottoman Black Sea frontier and a case study of Bulgarian population movements between the Russian and Ottoman Empires, this dissertation analyzes Russian and Ottoman migration and settlement policies, the spread of epidemic diseases (plague and cholera) in the Black Sea region, the construction of quarantines and the implementation of travel document regimes. The role and position of the Danubian Principalities of Moldavia and Wallachia as the “middle ground” between the Ottoman and Russian Empires -

Safety of Technogenic and Natural Systems 2020

№3 Safety of Technogenic and Natural Systems 2020 UDC 614.849 https://doi.org/10.23947/2541-9129-2020-3-21-32 Territorial fire statistics and assessment of their causes and consequences on the example of the Rostov region V. G. Ustin1, Yu. I. Bulygin2, P. P. Tretyakov3, V. V. Maslenskiy4 1 MD of the MES of Russia for the Rostov region (Rostov-on-Don, Russian Federation) 2,3,4 Don State Technical University (Rostov-on-Don, Russian Federation) Introduction. A deep and comprehensive analysis of the parameters of the situation with fires in the territories of the Russian Federation and its relationship with socio-economic processes is more relevant than ever for Russia. The article presents, summarizes and analyzes statistical data on the situation with fires and their consequences on the territory of the Rostov region for 2018-2019. Problem Statement. The paper considers the problem of official statistical accounting of fires, the procedure for accounting for people killed and injured in a fire in the context of a changing regulatory framework in this area. The analysis of the situation, official and verified information on fires and their consequences will create a reliable socio- economic characteristic of the Rostov region. Theoretical Part. The paper deals with the peculiarities of accounting of fires and their consequences in Russia. The source materials are the official statistics of the MD of the MES of Russia for the Rostov region on the number of fires on the territory, months, the number of people injured and killed in fires and their distribution by gender, age and time of death, objects and causes of fires. -

Argus Nefte Transport

Argus Nefte Transport Oil transportation logistics in the former Soviet Union Volume XVI, 5, May 2017 Primorsk loads first 100,000t diesel cargo Russia’s main outlet for 10ppm diesel exports, the Baltic port of Primorsk, shipped a 100,000t cargo for the first time this month. The diesel was loaded on 4 May on the 113,300t Dong-A Thetis, owned by the South Korean shipping company Dong-A Tanker. The 100,000t cargo of Rosneft product was sold to trading company Vitol for delivery to the Amsterdam-Rotter- dam-Antwerp region, a market participant says. The Dong-A Thetis was loaded at Russian pipeline crude exports berth 3 or 4 — which can handle crude and diesel following a recent upgrade, and mn b/d can accommodate 90,000-150,000t vessels with 15.5m draught. 6.0 Transit crude Russian crude It remains unclear whether larger loadings at Primorsk will become a regular 5.0 occurrence. “Smaller 50,000-60,000t cargoes are more popular and the terminal 4.0 does not always have the opportunity to stockpile larger quantities of diesel for 3.0 export,” a source familiar with operations at the outlet says. But the loading is significant considering the planned 10mn t/yr capacity 2.0 addition to the 15mn t/yr Sever diesel pipeline by 2018. Expansion to 25mn t/yr 1.0 will enable Transneft to divert more diesel to its pipeline system from ports in 0.0 Apr Jul Oct Jan Apr the Baltic states, in particular from the pipeline to the Latvian port of Ventspils. -

MEGA Rostov-On-Don Rostov-On-Don, Russia a Way of 15 MLN Life for All VISITORS ANNUALLY

MEGA Rostov-on-Don Rostov-on-Don, Russia A way of 15 MLN life for all VISITORS ANNUALLY Conveniently located near the M4 federal highway, with Enjoying over 15 million visitors a year, MEGA Rostov-on-Don a competitive mix of anchor tenants, affordable family has the highest footfall in the region. Our concept allows every value, and an exceptional food and beverage offer, guest to find something which appeals to the whole family, be MEGA Rostov-on-Don has the highest brand awareness that leisure or shopping. Our wide range of stores, services and among our competitors. leisure opportunities significantly increases dwell time, providing Luhansk high sales and a fun day out for our guests. Kamensk-Shakhtinskiy Gukovo Donetsk Novoshakhtinsk ShakhtyShakaty Novocherkassk Volgodonsk ROSTOV-ON-DON City Centre Taganrog Bataysk Azov Catchment Areas People Distance ● Primary 40,720 11 km ● Secondary 1,450,920 11–18 km ● Tertiary 2,831,070 > 18–211 km 59% EyskTotal area: 4,322,710 9 33% CUSTOMERS COME BUS ROUTES LIFESTYLE BY CAR GUESTS Sal’sk Tikhoretsk A region with Loyal customers MEGA Rostov is located in the city of Rostov–on-Don and attracts shoppers from all over the strong potential city and surrounding area. MEGA is loved by families, lifestyle and experienced guests alike. Rostov region The city of Rostov-on-Don Rostov region is a part of the Southern Federal District. Considered as a southern capital of Russia, Rostov- GUESTS VISIT MEGA 125 MINS 756km away from Moscow it has major railway routes on-Don has a diverse economical profile, with major AVERAGE 34% 62% 2.7 TIMES PER MONTH DWELL TIME passing in many directions across Russia and abroad. -

NARRATING the NATIONAL FUTURE: the COSSACKS in UKRAINIAN and RUSSIAN ROMANTIC LITERATURE by ANNA KOVALCHUK a DISSERTATION Prese

NARRATING THE NATIONAL FUTURE: THE COSSACKS IN UKRAINIAN AND RUSSIAN ROMANTIC LITERATURE by ANNA KOVALCHUK A DISSERTATION Presented to the Department of Comparative Literature and the Graduate School of the University of Oregon in partial fulfillment of the requirements for the degree of Doctor of Philosophy June 2017 DISSERTATION APPROVAL PAGE Student: Anna Kovalchuk Title: Narrating the National Future: The Cossacks in Ukrainian and Russian Romantic Literature This dissertation has been accepted and approved in partial fulfillment of the requirements for the Doctor of Philosophy degree in the Department of Comparative Literature by: Katya Hokanson Chairperson Michael Allan Core Member Serhii Plokhii Core Member Jenifer Presto Core Member Julie Hessler Institutional Representative and Scott L. Pratt Dean of the Graduate School Original approval signatures are on file with the University of Oregon Graduate School. Degree awarded June 2017 ii © 2017 Anna Kovalchuk iii DISSERTATION ABSTRACT Anna Kovalchuk Doctor of Philosophy Department of Comparative Literature June 2017 Title: Narrating the National Future: The Cossacks in Ukrainian and Russian Romantic Literature This dissertation investigates nineteenth-century narrative representations of the Cossacks—multi-ethnic warrior communities from the historical borderlands of empire, known for military strength, pillage, and revelry—as contested historical figures in modern identity politics. Rather than projecting today’s political borders into the past and proceeding from the claim that the Cossacks are either Russian or Ukrainian, this comparative project analyzes the nineteenth-century narratives that transform pre- national Cossack history into national patrimony. Following the Romantic era debates about national identity in the Russian empire, during which the Cossacks become part of both Ukrainian and Russian national self-definition, this dissertation focuses on the role of historical narrative in these burgeoning political projects. -

Socio-Economic Conditions for Formation of an Ecological and Recreational Cluster in the Rostov Region and Its Development Potential

E3S Web of Conferences 273, 09018 (2021) https://doi.org/10.1051/e3sconf/202127309018 INTERAGROMASH 2021 Socio-economic conditions for formation of an ecological and recreational cluster in the Rostov region and its development potential Lyudmila Kazmina1*, Vadim Makarenko1, Valeria Provotorina1, and Elena Shevchenko1 1 Don State Technical University, Gagarina Sq., 1, Rostov-on-Don, 344000, Russia Abstract. The article is concerned with basic concepts related to development of an ecological-excursion cluster in the Rostov region. The socio-economic conditions of its formation are described. The research base on which the research related to the study of touristic clusters is found is reviewed. It also gives grounds for the possibility of functioning of the ecological and recreational cluster, defines its functions and importance for the development of inbound and domestic tourism, the economy and the social sphere of the region. The zoning of the territory of the Rostov region according to the prevailing types of ecological and recreational clusters is proposed and the specifics of their activities and the development of types of tourism are indicated. 1 Introduction An effective tool for development of socio-economic systems in the sphere of tourism is implementation of a cluster approach that provides harmonization of private and public interests, diversification of risks and improvement of regional potential use. The clustering process is coherent giving a number of management decisions related to the specifics of the industry, participants, location, capacity, and a number of other indicators. Therefore, it is necessary to develop an algorithm to cluster the regional territory and manage development of economic zones on the basis of a systematic approach and with consideration of all factors, which have an effect on this process. -

The Donbas As an Intentional Community

THIS IS A DRAFT PAPER From Exit to Take-Over: The Evolution of the Donbas as an Intentional Community VLAD MYKHNENKO* International Policy Fellow The Central European University & Open Society Institute E-mail: [email protected] Paper for Workshop No 20. The Politics of Utopia: Intentional Communities as Social Science Microcosms The European Consortium for Political Research Joint Sessions of Workshops 13-18 April 2004 Uppsala, Sweden ABSTRACT: The Donbas – a large old industrial region in the Ukrainian-Russian Cossack borderland – constitutes a particular intentional community. According to earlier positive accounts, it was a space, the open steppe, a frontier land, a fugitive’s paradise, where the notions of and desires for freedom and dignifying labour had been realised. According to its current negative associations, the Donbas is an allegedly realised utopia of an ‘anti-modern’ community, dominated by a ‘criminal-political nexus’ of terrorising mafia gangs and political clans. The purpose of this paper is to compare the Donbas community, the evolution of intentions of its founders and of the images produced in the process of its construction, in three very different points in time – under the Russian Empire, under the Bolshevik Rule and Stalin’s Great Terror, and during the post-communist transformation. * I would like to express my gratitude here to the International Policy Fellowships, affiliated with the Central European University and Open Society Institute – Budapest, for their generous help, which has allowed me, among many other things, to work on this paper. 2 In both a geographical and symbolic sense, the Donbas constitutes a particular community, just as a nation, city, or village does. -

As of June 30, 2018

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint-stock company) Issuer code: 0 1 4 8 1 – В as 3 0 0 6 2 0 1 8 of (indicate the date on which the list of affiliates of the joint-stock company was compiled) Address of the issuer: 19, Vavilova St., Moscow 117997 (address of the issuer – the joint-stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint-stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Deputy Chairperson of the Executive Board of Sberbank B. Zlatkis (position of the authorized individual of the joint-stock company) (signature) (initials, surname) L.S. “ 03 ” July 20 18 . Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 0 0 6 2 0 1 8 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint- the affiliate indicated only with the consent of became valid the joint-stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 Entity may manage more than The Central Bank of the Russian 12, Neglinnaya St., Moscow 20% of the total number of votes 1 21.03.1991 50.000000004 52.316214 Federation 107016 attached to voting shares of the Bank 1. -

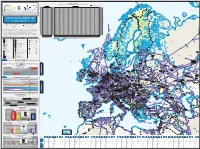

System Development Map 2019 / 2020 Presents Existing Infrastructure & Capacity from the Perspective of the Year 2020

7125/1-1 7124/3-1 SNØHVIT ASKELADD ALBATROSS 7122/6-1 7125/4-1 ALBATROSS S ASKELADD W GOLIAT 7128/4-1 Novaya Import & Transmission Capacity Zemlya 17 December 2020 (GWh/d) ALKE JAN MAYEN (Values submitted by TSO from Transparency Platform-the lowest value between the values submitted by cross border TSOs) Key DEg market area GASPOOL Den market area Net Connect Germany Barents Sea Import Capacities Cross-Border Capacities Hammerfest AZ DZ LNG LY NO RU TR AT BE BG CH CZ DEg DEn DK EE ES FI FR GR HR HU IE IT LT LU LV MD MK NL PL PT RO RS RU SE SI SK SM TR UA UK AT 0 AT 350 194 1.570 2.114 AT KILDIN N BE 477 488 965 BE 131 189 270 1.437 652 2.679 BE BG 577 577 BG 65 806 21 892 BG CH 0 CH 349 258 444 1.051 CH Pechora Sea CZ 0 CZ 2.306 400 2.706 CZ MURMAN DEg 511 2.973 3.484 DEg 129 335 34 330 932 1.760 DEg DEn 729 729 DEn 390 268 164 896 593 4 1.116 3.431 DEn MURMANSK DK 0 DK 101 23 124 DK GULYAYEV N PESCHANO-OZER EE 27 27 EE 10 168 10 EE PIRAZLOM Kolguyev POMOR ES 732 1.911 2.642 ES 165 80 245 ES Island Murmansk FI 220 220 FI 40 - FI FR 809 590 1.399 FR 850 100 609 224 1.783 FR GR 350 205 49 604 GR 118 118 GR BELUZEY HR 77 77 HR 77 54 131 HR Pomoriy SYSTEM DEVELOPMENT MAP HU 517 517 HU 153 49 50 129 517 381 HU Strait IE 0 IE 385 385 IE Kanin Peninsula IT 1.138 601 420 2.159 IT 1.150 640 291 22 2.103 IT TO TO LT 122 325 447 LT 65 65 LT 2019 / 2020 LU 0 LU 49 24 73 LU Kola Peninsula LV 63 63 LV 68 68 LV MD 0 MD 16 16 MD AASTA HANSTEEN Kandalaksha Avenue de Cortenbergh 100 Avenue de Cortenbergh 100 MK 0 MK 20 20 MK 1000 Brussels - BELGIUM 1000 Brussels - BELGIUM NL 418 963 1.381 NL 393 348 245 168 1.154 NL T +32 2 894 51 00 T +32 2 209 05 00 PL 158 1.336 1.494 PL 28 234 262 PL Twitter @ENTSOG Twitter @GIEBrussels PT 200 200 PT 144 144 PT [email protected] [email protected] RO 1.114 RO 148 77 RO www.entsog.eu www.gie.eu 1.114 225 RS 0 RS 174 142 316 RS The System Development Map 2019 / 2020 presents existing infrastructure & capacity from the perspective of the year 2020. -

Modernization of the Russian Education Under the Geopolitical Realities of Modernity: the Problem of Formation of the Russian Identity

Journal of History Culture and Art Research (ISSN: 2147-0626) Tarih Kültür ve Sanat Araştırmaları Dergisi Vol. 8, No. 3, September 2019 DOI: 10.7596/taksad.v8i3.2159 Citation: Lukash, S. N., Andrienko, N. K., Tersakova, A. A., & Pluzhnikova, E. A. (2019). Modernization of the Russian Education Under the Geopolitical Realities of Modernity: The Problem of Formation of the Russian Identity. Journal of History Culture and Art Research, 8(3), 179-188. doi:http://dx.doi.org/10.7596/taksad.v8i3.2159 Modernization of the Russian Education Under the Geopolitical Realities of Modernity: The Problem of Formation of the Russian Identity* Sergey N. Lukash1, Nadezhda K. Andrienko2, Angela A. Tersakova3, Elena A. Pluzhnikova4 Abstract The obvious contradiction between a modern geopolitical course of the country to multi-polarity, to the Eurasian vector of development and the strategy of modernization of Russian education according the Western (European) model derivative of the idea of uni-polarity, embedding the Russian education in a valuable semantic paradigm of the Western civilization is being implemented till present. The contradiction related to the strategic geopolitical vector of development of modern Russia and the strategy of its state institutes, education, in particular, leads to the fact that in the Russian society the complex unresolved humanitarian problems will turn into a serious crisis in future. One of such challenges in Russia aggravated due to the global opposition between Russia and the USA is the problem of national unity of Russian society, the formation of Russian national identity. Variants of the pedagogical solution of the given problem actualizing the idea of multi-polarity and the paradigm of the Russian Eurasian civilization corresponding to it, in particular, the Cossacks phenomenon are considered in the article.