The Mineral Industry of Mauritania in 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

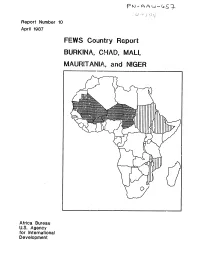

FEWS Country Report BURKINA, CHAD, MALI, MAURITANIA, and NIGER

Report Number 10 April 1987 FEWS Country Report BURKINA, CHAD, MALI, MAURITANIA, and NIGER Africa Bureau U.S. Agency for International Development Summary Map __ Chad lMurltanl fL People displaced by fighting High percentage of population have bothL.J in B.E.T. un~tfood needsa nd no source of income - High crop oss cobied with WESTERN Definite increases in retes of malnutrition at CRS centers :rom scarce mrket and low SAHARA .ct 1985 through Nov 196 ,cash income Areas with high percentage MA RTAI of vulnerable LIBYA MAU~lAN~A/populations / ,,NIGER SENEGAL %.t'"S-"X UIDA Areas at-risk I/TGI IEI BurkinaCAMEROON Areas where grasshoppers r Less than 50z of food needs met combined / CENTRAL AFRICAN would have worst impact Fi with absence of government stocks REPLTL IC if expected irdestat ions occur W Less than r59 of food needs met combined ith absence of government stocks FEYIS/PWA. April 1987 Famine Early Warning System Country Report BURKINA CHAD MALI MAURITANIA NIGER Populations Under Duress Prepared for the Africa Bureau of the U.S. Agency for International Development Prepared by Price, Williams & Associates, Inc. April 1987 Contents Page i Introduction 1 Summary 2 Burkina 6 Chad 9 Mali 12 Mauritania 18 Niger 2f FiAures 3 Map 2 Burkina, Grain Supply and OFNACER Stocks 4 Table I Burkina, Production and OFNACER Stocks 6 Figure I Chad, Prices of Staple Grains in N'Djamcna 7 Map 3 Chad, Populations At-Risk 10 Table 2 Mali, Free Food Distribution Plan for 1987 II Map 4 Mali, Population to Receive Food Aid 12 Figure 2 Mauritania, Decreasing -

Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

Phase 2 Environmental Impact Assessment On-Site Mine Process

Tasiast Mauritanie Limited SA Tasiast Gold Mine Expansion Project Phase 2: On-Site Mine, Process and Infrastructure Environmental Impact Assessment Final 30 March 2012 Prepared for Prepared for Tasiast Mauritanie Limited SA Tasiast Gold Mine Expansion Project Revision Schedule Phase 2 Environmental Impact Assessment 30 March 2012 Final Rev Date Details Prepared by Reviewed by Approved by 01 21/12/2011 Draft for review Reine Loader Julie Raynor Russell Foxwell Environmental Consultant Associate Associate Fraser Paterson Associate 02 01/03/2012 Draft for Reine Loader Julie Raynor Russell Foxwell translation Environmental Consultant Associate Associate Fraser Paterson Associate 03 30/03/2012 FINAL Reine Loader Fraser Paterson Russell Foxwell Environmental Consultant Associate Associate URS Infrastructure & Environment UK Limited 6-8 Greencoat Place London SW1P 1PL United Kingdom Tel +44 (0) 20 7798 5000 Fax +44 (0) 20 7798 5001 www.ursglobal.com Tasiast Mauritanie Limited SA Tasiast Gold Mine Expansion Project Limitations URS Infrastructure & Environment UK Limited (“URS”) (formerly URS Scott Wilson Ltd) has prepared this Report for the use of Tasiast Mauritanie Limited SA (“Client”) in accordance with the Agreement under which our services were performed. No other warranty, expressed or implied, is made as to the professional advice included in this Report or any other services provided by URS. Notwithstanding anything to the contrary, URS acknowledge that the Report may be disclosed by the Client to any third party, including members of the public for the specific purposes which have been advised to URS. URS shall not have any liability to any third parties for the unauthorised copying and any subsequent reliance on this Report. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Preparing for Growth: Capitalizing on a Period of Progress and Stability

Preparing for growth: Capitalizing on a period of progress and stability www.pwc.com/ca/canadianmine A year of stability Contents 2 A year of stability 3 Highlights and analysis 7 Agnico Eagle: Perfecting a successful 60 year-old strategy 9 Osisko Gold Royalties: Disrupting the cycle An interview with John Matheson, Partner, PwC Canada 11 Savvy investments in stable times Call it breathing room. Over the last year, into Eastern and Central Europe with its Canada’s major mining companies have Belt and Road Initiative (formerly One Belt entered a period of relative stability after and One Road) is increasing demand for weathering a frenzied period of boom, industrial products. bust and recovery. Globally, the geopolitical situation will About this report The sector has been paying down debt, likely remain volatile through 2018 and Preparing for growth is one of improving balance sheets and judiciously beyond. While bullion largely shrugged four publications in our annual investing in capital projects, on trend with off 2017’s world events, international Canadian mine series looking at the wider global mining industry in 2017. uncertainties could yet become an the realities and priorities of public Maintaining flexibility and increasing upward force on gold prices. The success mining companies headquartered efficiency are key goals for many executive of stock markets around the globe last in Canada. It offers a summary of financial analysis of the top 25 teams as they try to position themselves to year dampened general investor interest listings by market capitalization on capitalize on the next stages of the cycle. in gold equities, with the precious metal the TSX and complements our Junior Some companies have sought to enhance traditionally serving as a hedge against mine 2017 report, which analyzes the operations through acquisitions, but on market downturns, said David Smith, top 100 listings on the TSX Venture the whole, 2017 saw few eye-popping Senior Vice President of Finance and Chief Exchange (TSX-V). -

IEA: the Role of Critical Minerals in Clean Energy Transitions

The Role of Critical Minerals in Clean Energy Transitions World Energy Outlook Special Report INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of IEA member countries: Spain energy issues including oil, gas and Australia Sweden coal supply and demand, renewable Austria Switzerland energy technologies, electricity Belgium Turkey markets, energy efficiency, access to Canada United Kingdom energy, demand side management Czech Republic United States and much more. Through its work, the Denmark IEA advocates policies that will Estonia IEA association countries: enhance the reliability, affordability Finland Brazil and sustainability of energy in its 30 France China member countries, 8 association Germany India countries and beyond. Greece Indonesia Hungary Morocco Please note that this publication is Ireland Singapore subject to specific restrictions that Italy South Africa limit its use and distribution. The Japan Thailand terms and conditions are available Korea online at www.iea.org/t&c/ Luxembourg Mexico This publication and any map included herein are Netherlands without prejudice to the status of or sovereignty New Zealand over any territory, to the delimitation of international frontiers and boundaries and to the Norway name of any territory, city or area. Poland Portugal Slovak Republic Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org The Role of Critical Minerals in Clean Energy Transitions Foreword Foreword Ever since the International Energy Agency (IEA) was founded in world to anticipate and navigate possible disruptions and avoid 1974 in the wake of severe disruptions to global oil markets that damaging outcomes for our economies and our planet. shook the world economy, its core mission has been to foster secure This special report is the most comprehensive global study of this and affordable energy supplies. -

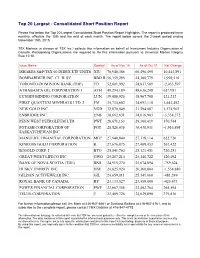

Top 20 Largest - Consolidated Short Position Report

Top 20 Largest - Consolidated Short Position Report Please find below the Top 20 Largest Consolidated Short Position Report Highlights. The report is produced twice monthly, effective the 15th and the end of each month. The report below covers the 2-week period ending November 15th, 2015. TSX Markets (a division of TSX Inc.) collects this information on behalf of Investment Industry Organization of Canada. Participating Organizations are required to file this information pursuant to Universal Market Integrity Rule 10.10. Issue Name Symbol As of Nov 15 As of Oct 31 Net Change ISHARES S&P/TSX 60 INDEX ETF UNITS XIU 70,940,386 60,496,495 10,443,891 BOMBARDIER INC. CL 'B' SV BBD.B 56,359,295 54,360,779 1,998,516 TORONTO-DOMINION BANK (THE) TD 52,801,992 54,837,589 -2,035,597 ATHABASCA OIL CORPORATION J ATH 49,294,189 48,636,208 657,981 LUNDIN MINING CORPORATION LUN 39,088,920 38,967,708 121,212 FIRST QUANTUM MINERALS LTD. J FM 35,734,602 34,091,110 1,643,492 NEW GOLD INC. NGD 32,870,049 31,294,087 1,575,962 ENBRIDGE INC. ENB 30,662,631 34,016,903 -3,354,272 PENN WEST PETROLEUM LTD. PWT 28,671,163 28,300,419 370,744 POTASH CORPORATION OF POT 28,520,036 30,436,931 -1,916,895 SASKATCHEWAN INC. MANULIFE FINANCIAL CORPORATION MFC 27,940,840 27,318,114 622,726 KINROSS GOLD CORPORATION K 27,676,875 27,409,453 267,422 B2GOLD CORP. -

PIF) Entry – Full Sized Project – GEF - 7 Development of an Integrated System to Promote the Natural Capital in the Drylands of Mauritania

5/5/2020 WbgGefportal Project Identification Form (PIF) entry – Full Sized Project – GEF - 7 Development of an integrated system to promote the natural capital in the drylands of Mauritania Part I: Project Information GEF ID 10444 Project Type FSP Type of Trust Fund GET CBIT/NGI CBIT NGI Project Title Development of an integrated system to promote the natural capital in the drylands of Mauritania Countries Mauritania Agency(ies) IUCN Other Executing Partner(s) Executing Partner Type CNEOZA, Ministère de l'Environnement et du Développement Durable Government https://gefportal2.worldbank.org 1/51 5/5/2020 WbgGefportal GEF Focal Area Land Degradation Taxonomy Climate Change Adaptation, Climate Change, Focal Areas, Climate resilience, Livelihoods, Disaster risk management, Land Degradation, Sustainable Land Management, Drought Mitigation, Integrated and Cross-sectoral approach, Improved Soil and Water Management Techniques, Sustainable Livelihoods, Sustainable Pasture Management, Ecosystem Approach, Restoration and Rehabilitation of Degraded Lands, Community-Based Natural Resource Management, Sustainable Agriculture, Income Generating Activities, Food Security, Land Degradation Neutrality, Land Productivity, Influencing models, Transform policy and regulatory environments, Strengthen institutional capacity and decision-making, Convene multi-stakeholder alliances, Private Sector, Stakeholders, Individuals/Entrepreneurs, Large corporations, SMEs, Beneficiaries, Non-Governmental Organization, Civil Society, Community Based Organization, Participation, -

Poverty and the Struggle to Survive in the Fuuta Tooro Region Of

What Development? Poverty and the Struggle to Survive in the Fuuta Tooro Region of Southern Mauritania Dissertation Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Christopher Hemmig, M.A. Graduate Program in Near Eastern Languages and Cultures. The Ohio State University 2015 Dissertation Committee: Sabra Webber, Advisor Morgan Liu Katey Borland Copyright by Christopher T. Hemmig 2015 Abstract Like much of Subsaharan Africa, development has been an ever-present aspect to postcolonial life for the Halpulaar populations of the Fuuta Tooro region of southern Mauritania. With the collapse of locally historical modes of production by which the population formerly sustained itself, Fuuta communities recognize the need for change and adaptation to the different political, economic, social, and ecological circumstances in which they find themselves. Development has taken on a particular urgency as people look for effective strategies to adjust to new realities while maintaining their sense of cultural identity. Unfortunately, the initiatives, projects, and partnerships that have come to fruition through development have not been enough to bring improvements to the quality of life in the region. Fuuta communities find their capacity to develop hindered by three macro challenges: climate change, their marginalized status within the Mauritanian national community, and the region's unfavorable integration into the global economy by which the local markets act as backwaters that accumulate the detritus of global trade. Any headway that communities can make against any of these challenges tends to be swallowed up by the forces associated with the other challenges. -

Notice to Participating Organizations 2005-028

Notice to Participating Organizations --------------------------------------------------------------------------------------------------------------------- August 12, 2005 2005-028 Addition of Market On Close (MOC) Eligible Securities Toronto Stock Exchange will roll out MOC eligibility to the symbols of the S&P/TSX Composite Index in preparation for the quarter end index rebalancing on September 16, 2005. TSX will enable MOC eligibility in two phases: I. S&P/TSX Mid Cap Index will become MOC eligible effective September 6, 2005. II. S&P/TSX Small Cap Index will become MOC eligible effective September 12, 2005. A list of securities for each of these indices follows this notice. To ensure you are viewing the most current list of securities, please visit the Standard and Poor's website at www.standardandpoors.com prior to the above rollout dates. “S&P” is a trade-mark owned by The McGraw-Hill, Companies Inc. and “TSX” is a trade- mark owned by TSX Inc. MOC Eligible effective MOC Eligible effective September 6, 2005 September 12, 2005 S&P TSX Mid Cap S&P TSX Small Cap SYMBOL COMPANY SYMBOL COMPANY ABZ Aber Diamond Corporation AAC.NV.B Alliance Atlantis Communications Inc. ACM.NV.A Astral Media Inc. AAH Aastra Technologies Ltd. ACO.NV.X Atco Ltd. ACE.RV ACE Aviation Holdings Inc. AGE Agnico-Eagle Mines AEZ Aeterna Zentaris Inc. AGF.NV AGF Management Ltd. AGA Algoma Steel Inc. AIT Aliant Inc. ANP Angiotech Pharmaceuticals Inc. ATA ATS Automation Tooling Systems Inc. ATD.SV.B Alimentation Couche-Tard Inc. AXP Axcan Pharma Inc. AU.LV Agricore United BLD Ballard Power Systems Inc. AUR Aur Resources Inc. -

Appraisal Manual for Centrally Valued Natural Resource Property

Appraisal Manual For Centrally Valued Natural Resource Property Valuation Guidelines for Natural Resource Property Preface Preface The Department of Revenue’s Local Jurisdictions District is responsible for ensuring fair, accurate, and uniform property valuations as prescribed by Arizona statutes. The Local Jurisdictions District contains the Centrally Valued Property Unit which is responsible for producing this manual. The Centrally Valued Property Unit is responsible for determining the full cash value of certain utilities, railroads, airlines, private rail cars, mines, and other complex or geographically diverse property. With the exception of airline and private rail car valuations, the values are then transmitted for entry on the individual county tax rolls for levy and collection of property taxes. The manual is produced each year to serve as a guide in the appraisal of mines and other natural resource property. The techniques, procedures, and factors described in the manual are reviewed annually and revised in accordance with standard appraisal methods and techniques along with changes in statutes, rules, and regulations. Revisions are also made based on case law decisions. The procedures described in the manual are designed to assist the appraiser in the application of the income, cost, and market approach methods of valuation to these properties for the current tax year. This manual is intended for use in ad valorem appraisal of specific centrally valued property including producing mines, certain non-producing mines, qualifying environmental technology property and oil, gas, and geothermal interests in Arizona. The guidelines in this manual are used to establish full cash values for these properties as of January 1 of the valuation year. -

Linde Equity Research TSX Performance Review 2011 Q2: TSX Composite Gives Back Q1 Gains Most Important Sectors All Register Losses in Q2 Q2 Sector Returns

Linde Equity Research TSX Performance Review 2011 Q2: TSX Composite gives back Q1 gains Most important sectors all register losses in Q2 Q2 Sector Returns Telecommunications Services 7.54% Health Care 3.31% Consumer Staples 1.62% Industrials 1.42% Consumer Discretionary 0.11% -0.54% Utilities -3.64% Financials -5.78% S&P/TSX Composite -8.60% Materials -9.11% Energy -31.44% Consumer Discretionary Information Technology -35% -30% -25% -20% -15% -10% -5% 0% 5% 10% • The S&P/TSX Composite lost 5.8% in Q2. 2011 Index Returns Q2 YTD • Of the 265 stocks that were in the TSX S&P/TSX Composite -5.78% -1.06% Composite at some point during Q2, 177 (67%) lost ground in the quarter. S&P/TSX 60 (Large Cap) -5.59% -0.62% • The TSX 60 (large cap) outperformed mid-cap S&P/TSX Completion (Mid) -6.32% -2.38% and small-cap stocks for the second straight S&P/TSX Small Cap -8.75% -5.37% quarter, consistent with late-bull market periods. • In Q2, the Canadian market lagged the US Q2 Biggest Contributors Q2 Biggest Detractors market in home currency terms (US returned -0.4%) and in Canadian dollar terms (US BCE Inc Research in Motion returned -0.9% in C$ terms). TransCanada Corporation Suncor Energy • Information Technology was the worst performing sector due to weakness from Research in Motion. Equinox Minerals Cdn Natural Resources • Energy (Canada’s 2nd biggest sector) was the Rogers Communications Barrick Gold second worst performing sector on weakening oil Canadian National Railways Royal Bank of Canada and gas prices (worst sector worldwide).