Ost of Capital Study Air Transport

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

JANUARY European Parliament Vote on Airport Charges (15 January)

REVIEW www.airtransportnews.aero JANUARY European Parliament vote on airport charges (15 January) he European Parliament concluded its first reading on a proposed Directive on airport charges, initially the Directive will only incentivise conflicts between airlines and airports, resulting in uncertainty over infra - adopted by the European Commission a year ago. ACI EUROPE is appreciative of the European Parlia - structure investments and potentially delaying much needed capacity development. Olivier Jankovec added: T ment’s work to improve the proposal of the European Commission, but considers that serious concerns "That the Directive is silent on the need for airports to be incentivised to invest in time for the new facilities regarding fundamental issues remain. These include risking costly and damaging over-regulation as well as com - to match demand, is puzzling. It shows that the Directive not only remains imbalanced in favour of airlines but promising the ability of European airports to finance much needed infrastructure and capacity development. also fails to reflect that the interests of the airlines and that of the travelling public are not the same." Whilst the European Commission proposed to apply the Directive to all airports with more than 1 million pas - Responding to the vote of the European Parliament on Airport Charges, IACA is extremely disappointed that an sengers per year, the European Parliament increased this figure to 5 million, leaving States still free to apply opportunity to address the unbalanced relationship between the fully deregulated airline sector and their mo - the Directive to airports below this threshold. As most European airports now operate in a highly competitive nopolistic service provider (airports) has been missed. -

ABX Holdings, Inc. 145 Hunter Drive, Wilmington, Ohio 45177

ABX Holdings, Inc. 145 Hunter Drive, Wilmington, Ohio 45177 NOTICE OF ANNUAL MEETING OF STOCKHOLDERS TO BE HELD MAY 13, 2008 Notice is hereby given that the 2008 annual meeting of the stockholders of ABX Holdings, Inc., a Delaware corporation (the “Company”), has been called and will be held on May 13, 2008, at 11:00 a.m., local time, at the Roberts Convention Centre, 188 Roberts Road, Wilmington, Ohio, for the following purposes: 1. To elect two directors to the Board of Directors each for a term of three years. 2. To consider and vote on a proposal to amend the Company’s Certificate of Incorporation to change the name of the Company from ABX Holdings, Inc. to “Air Transport Services Group, Inc.” 3. To ratify the appointment of Deloitte & Touche LLP as the independent registered public accounting firm of the Company for fiscal year 2008. 4. To consider and vote on a stockholder proposal. 5. To attend to such other business as may properly come before the meeting and any adjournments thereof. The foregoing matters are described in more detail in the Proxy Statement that is attached to this notice. At the meeting, we will also report on the Company’s 2007 business results and other matters of interest to stockholders. Only holders of record, as of the close of business on March 17, 2008, of shares of common stock of the Company will be entitled to notice of and to vote at the meeting and any adjournments thereof. By Order of the Board of Directors Wilmington, Ohio W. -

APR 2009 Stats Rpts

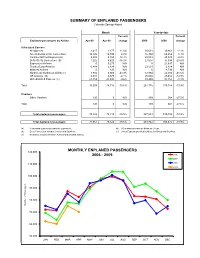

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

MAR 2009 Stats Rpts

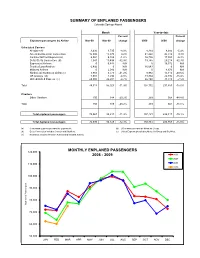

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Mar-09 Mar-08 change 2009 2008 change Scheduled Carriers Allegiant Air 3,436 3,735 -8.0% 8,214 8,684 -5.4% American/American Connection 15,900 15,873 0.2% 41,268 45,510 -9.3% Continental/Cont Express (a) 6,084 6,159 -1.2% 16,736 17,884 -6.4% Delta /Delta Connection (b) 7,041 10,498 -32.9% 19,785 29,218 -32.3% ExpressJet Airlines 0 6,444 N/A 0 16,372 N/A Frontier/Lynx Aviation 6,492 0 N/A 16,643 0 N/A Midwest Airlines 0 2,046 N/A 0 4,673 N/A Northwest/ Northwest Airlink (c) 3,983 6,773 -41.2% 8,982 15,110 -40.6% US Airways (d) 7,001 7,294 -4.0% 19,364 22,892 -15.4% United/United Express (e) 24,980 26,201 -4.7% 66,140 71,510 -7.5% Total 74,917 85,023 -11.9% 197,132 231,853 -15.0% Charters Other Charters 150 188 -20.2% 289 564 -48.8% Total 150 188 -20.2% 289 564 -48.8% Total enplaned passengers 75,067 85,211 -11.9% 197,421 232,417 -15.1% Total deplaned passengers 72,030 82,129 -12.3% 192,861 226,953 -15.0% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

Prof. Paul Stephen Dempsey

AIRLINE ALLIANCES by Paul Stephen Dempsey Director, Institute of Air & Space Law McGill University Copyright © 2008 by Paul Stephen Dempsey Before Alliances, there was Pan American World Airways . and Trans World Airlines. Before the mega- Alliances, there was interlining, facilitated by IATA Like dogs marking territory, airlines around the world are sniffing each other's tail fins looking for partners." Daniel Riordan “The hardest thing in working on an alliance is to coordinate the activities of people who have different instincts and a different language, and maybe worship slightly different travel gods, to get them to work together in a culture that allows them to respect each other’s habits and convictions, and yet work productively together in an environment in which you can’t specify everything in advance.” Michael E. Levine “Beware a pact with the devil.” Martin Shugrue Airline Motivations For Alliances • the desire to achieve greater economies of scale, scope, and density; • the desire to reduce costs by consolidating redundant operations; • the need to improve revenue by reducing the level of competition wherever possible as markets are liberalized; and • the desire to skirt around the nationality rules which prohibit multinational ownership and cabotage. Intercarrier Agreements · Ticketing-and-Baggage Agreements · Joint-Fare Agreements · Reciprocal Airport Agreements · Blocked Space Relationships · Computer Reservations Systems Joint Ventures · Joint Sales Offices and Telephone Centers · E-Commerce Joint Ventures · Frequent Flyer Program Alliances · Pooling Traffic & Revenue · Code-Sharing Code Sharing The term "code" refers to the identifier used in flight schedule, generally the 2-character IATA carrier designator code and flight number. Thus, XX123, flight 123 operated by the airline XX, might also be sold by airline YY as YY456 and by ZZ as ZZ9876. -

List of Section 13F Securities

List of Section 13F Securities 1st Quarter FY 2004 Copyright (c) 2004 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2004, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2004. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by Section 13(f)(1) and Rule 13f-1 thereunder. -

REPUBLIC AIRWAYS HOLDINGS INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 ___________________________________ FORM 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011 OR o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM ______________ TO _____________ COMMISSION FILE NUMBER: 000-49697 REPUBLIC AIRWAYS HOLDINGS INC. (Exact name of registrant as specified in its charter) DELAWARE 06-1449146 (State or other jurisdiction of (I.R.S. Employer Identification Number) incorporation or organization) 8909 Purdue Road, Suite 300, Indianapolis, Indiana 46268 (Address of principal executive offices) (Zip Code) (317) 484-6000 (Registrant’s telephone number, including area code) _____________________________ Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $.001 per share Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Insper Instituto De Ensino E Pesquisa Leonardo Francisco Sant'ana

Insper Instituto de Ensino e Pesquisa Faculdade de Economia e Administração Leonardo Francisco Sant’Ana Júnior FUSÕES E AQUISIÇÕES NO SETOR AÉREO São Paulo 2011 1 Leonardo Francisco Sant’Ana Júnior Fusões e aquisições no setor aéreo Monografia apresentada ao curso de Ciências Econômicas, como requisito para a obtenção do Grau de Bacharel I do Insper Instituto de Ensino e Pesquisa. Orientadora: Prof.ª Maria Cristina N. Gramani – Insper São Paulo 2011 2 Sant’ Ana, Leonardo Francisco Jr. Fusões e aquisições no setor aéreo / Leonardo Francisco Sant’ Ana Júnior. – São Paulo: Insper, 2011. 37 f. Monografia: Faculdade de Economia e Administração. Insper Instituto de Ensino e Pesquisa. Orientadora: Prof.ª Maria Cristina N. Gramani 1.Fusões e aquisições 2. Análise Envoltória de dados 3. Setor aéreo 3 Leonardo Francisco Sant’ Ana Júnior Fusões e aquisições no setor aéreo Monografia apresentada à Faculdade de Economia do Insper, como parte dos requisitos para conclusão do curso de graduação em Economia. EXAMINADORES ___________________________________________________________________ ________ Prof.ª Maria Cristina N. Gramani Orientadora ___________________________________________________________________ ________ Prof. Eduardo de Carvalho Andrade Examinador ________ Prof. Henrique Machado Barros Examinador 4 Agradecimentos Aos professores, à minha orientadora, aos amigos e colegas de faculdade e do trabalho e ao pessoal da biblioteca. 5 Dedicatória Dedico este trabalho a Deus, aos meus pais que sem a ajuda deles nada conseguiria, à minha namorada que me dá a força e o carinho necessário no meu dia-a-dia e aos meus amigos que sempre estão por perto pra compartilhar os momentos da minha vida. 6 Resumo Sant’ Ana, Leonardo Francisco Júnior. -

November 2017 Newsletter

PilotsPROUDLY For C ELEBRATINGKids Organization 34 YEARS! Pilots For KidsSM ORGANIZATION Helping Hospitalized Children Since 1983 Want to join in this year’s holiday visits? Newsletter November 2017 See pages 8-9 to contact the coordinator in your area! PFK volunteers have been visiting youngsters at Texas Children’s Hospital for 23 years. Thirteen volunteers representing United, Delta and Jet Blue joined together and had another very successful visit on June 13th. Sign up for holiday visits in your area by contacting your coordinator! “100% of our donations go to the kids” visit us at: pilotsforkids.org (2) Pilots For Kids Organization CITY: LAX/Los Angeles, CA President’s Corner... COORDINATOR: Vasco Rodriques PARTICIPANTS: Alaska Airlines Dear Members, The volunteers from the LAX Alaska Airlines Pilots Progress is a word everyone likes. The definition for Kids Chapter visited with 400 kids at the Miller of progress can be described as growth, develop- Children’s Hospital in Long Beach. This was during ment, or some form of improvement. their 2-day “Beach Carnival Day”. During the last year we experienced continual growth in membership and also added more loca- The crews made and flew paper airplanes with the tions where our visits take place. Another sign kids. When the kids landed their creations on “Run- of our growth has been our need to add a second way 25L”, they got rewarded with some cool wings! “Captain Baldy” mascot due to his popularity. Along with growth comes workload. To solve this challenge we have continually looked for ways to reduce our workload and cost through increased automation. -

Here Aspiring Pilots Are Well Prepared to Make the Critical Early Career and Lifestyle Choices Unique to the Aviation Industry

August 2021 Aero Crew News Your Source for Pilot Hiring and More.. START PREPARING FOR YOUR APPROACH INTO RETIREMENT Designed to help you understand some of the decisions you will need to make as you get ready for your approach into retirement, our free workbook includes 5 key steps to begin preparing for life after flying. You’ll discover more about: • How you will fund your retirement “paycheck” • What your new routine might look like • If your investment risk needs to be reassessed • And much more Dowload your free Retirement Workbook » 800.321.9123 | RAA.COM Aero Crew News 2021 PHOTO CONTEST Begins Now! This year’s theme is Aviation Weather! Submit your photos at https://rebrand.ly/ACN_RAA_Photo_Contest Official rules can be found at https://rebrand.ly/ACN-RAA-Rules. Jump to each section Below contents by clicking on the title or photo. August 2021 37 50 41 56 44 Also Featuring: Letter from the Publisher 8 Aviator Bulletins 11 Mortgage - The Mortgage Process Part 2 52 Careers - Routines and Repetition 54 4 | Aero Crew News BACK TO CONTENTS the grid US Cargo US Charter US Major Airlines US Regional Airlines ABX Air Airshare Alaska Airlines Air Choice One Alaska Seaplanes GMJ Air Shuttle Allegiant Air Air Wisconsin Ameriflight Key Lime Air American Airlines Cape Air Atlas Air/Southern Air Omni Air International Delta Air Lines CommutAir FedEx Express Ravn Air Group Frontier Airlines Elite Airways iAero Airways XOJET Aviation Hawaiian Airlines Endeavor Air Kalitta Air JetBlue Airways Envoy Key Lime Air US Fractional Southwest Airlines ExpressJet Airlines UPS FlexJet Spirit Airlines GoJet Airlines NetJets Sun Country Airlines Grant Aviation US Cargo Regional PlaneSense United Airlines Horizon Air Empire Airlines Key Lime Air Mesa Airlines ‘Ohana by Hawaiian Piedmont Airlines PSA Airlines Republic Airways The Grid has moved online. -

Public Utility and Flight Equipment Ad Valorem Tax Digest 2015

Georgia Department of Revenue Prepared October 2015 Local Government Services Division Public Utility and Airline Flight Equipment Valuation for 2015 Public Utility Section Changes From Previous Year Type of Company Electric EMC Flight Gas Gas Pipeline Railroads Telephones Total Equipment Municipal Private PY Number of Companies 7 49 32 23 4 9 28 72 224 CY Number of Companies 7 49 31 23 3 9 27 68 217 PY Unit Value 48,950,000,000 12,811,187,809 64,120,130,852 24,553,680 1,602,800,000 10,368,000,000 32,150,986,260 30,148,631,901 200,176,290,501 CY Unit Value 51,850,000,000 13,379,434,393 68,905,426,563 24,855,950 1,652,800,000 10,738,000,000 35,260,086,260 31,066,573,609 212,877,176,776 % Change 5.92% 4.44% 7.46% 1.23% 3.12% 3.57% 9.67% 3.04% 6.34% PY Georgia FMV Operating 14,697,025,514 9,678,333,634 1,648,054,153 25,059,840 1,447,611,744 1,429,453,118 2,325,974,002 4,353,532,609 35,605,044,614 CY Georgia FMV Operating 15,478,375,119 10,008,123,101 1,261,013,097 24,852,641 1,508,383,612 1,447,570,758 2,591,045,933 4,181,996,069 36,501,360,330 % Change 5.32% 3.41% -23.48% -0.83% 4.20% 1.27% 11.40% -3.94% 2.52% PY Georgia FMV Non-OP 1,378,063,438 27,260,749 0 39,304 692,489 7,712,106 45,825,487 4,660,870 1,464,254,443 CY Georgia FMV Non-OP 1,377,784,780 27,789,278 0 39,304 692,489 7,745,763 45,779,699 3,456,906 1,463,288,219 % Change -0.02% 1.94% 0.00% 0.00% 0.00% 0.44% -0.10% -25.83% -0.07% PY Georgia FMV Total 16,075,088,952 9,705,594,383 1,648,054,153 25,060,740 1,448,304,233 1,437,165,224 2,371,799,489 4,358,193,479 37,069,260,653 CY -

Capitalization Rate Study 2008

CAPITALIZATION RATE STUDY For CENTRALLY ASSESSED PROPERTIES As of January 1, 2008 UTAH STATE TAX COMMISSION PROPERTY TAX DIVISION CAPITALIZATION RATE STUDY SUMMARIES UTAH STATE TAX COMMISSION PROPERTY TAX DIVISION Utah State Tax Commission 2008 Capitalization Rate Study Equity Percent Yield Common Rate Equity Airlines - Major 19.70% 75% 25% 38.50% Airlines - Secondary 13.85% 55% 45% 39.46% .Airlines................................... ...-.... ...Secondary................ with Southwest 13.61% 50.0% 50% 39.00% Airlines - Frei 11 .28% 5% 95% 36.35% .............................................................. ............................................................... ............................................................... ............................................................... Electric Utilities 11 .11% 40% 60% 33.83% Natural Gas Utilities 11 .08% 30% 70% 35 .05% ...................................................................................................... ...................................................................................................... ...................................................................................................... ...................................................................................................... Natural Gas Pipelines 10.99% 25% 75% 32.58% ..................................................... ...................................................................................................... ........................................................................................................