The French Automotive Industry Analysis and Statistics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jsc Avtovaz Avtovaz Group* Operating Highlights for 2003

ANNUAL REPORT | 2003 | JSC AVTOVAZ AVTOVAZ GROUP* OPERATING HIGHLIGHTS FOR 2003 Vehicle unit sales, JSC AVTOVAZ 2003 2002 Change 000’s units 000’s units % Domestic market 626 577 8.49 Export market 92 98 (6.12) Total 718 675 6.3 Automotive assembly kits sales 98 101 (2.97) RR mln RR mln % Net sales 130,772 119,432 9.49 Operating income 5,941 5,591 6.26 Consolidated Statement 2003 2002 Change of Income** RR mln RR mln % For the year ended 31 December Net sales 130,772 119,432 9.49 Cost of sales (110,003) (99,331) 10.74 Gross profit 20,769 20,101 3.32 Interest expense (3,416) (3,077) (11.02) Other expense, net (14,402) (15,896) (9.4) Net income for the year 2,951 1,128 161.61 Consolidated Balance Sheet** 2003 2002 Change At 31 December RR mln RR mln % Cash and cash equivalents 6,767 2,751 145.98 Other current assets 37,069 33,393 11.01 Non-current assets 108,228 102,836 5.24 Total liabilities 72,562 62,166 16.72 Minority interest 1,290 1,587 (18.71) Total shareholders’ equity 78,212 75,227 3.97 Share price and dividend 2003 2002 Change development, JSC AVTOVAZ*** Share price RR RR % For the year ended 31 December Ordinary share Closing 774.7 679.72 +13.97 Annual high 906.42 1201.31 -24.55 Annual low 582.06 558.64 +4.19 Preference share Closing 471.88 371.17 +27.13 Annual high 525.68 667.54 -21.25 Annual low 339.77 319.10 +6.48 Dividends Per ordinary share 6.00 5.00 +20.0 Per preference share 95.00 17.00 +458.82 * The AVTOVAZ Group mentioned hereinafter is the parent company (JSC AVTOVAZ or the “Company”) and all of its subsidiaries and associated companies. -

Impact of Political Course Shift in Ukraine on Stock Returns

IMPACT OF POLITICAL COURSE SHIFT IN UKRAINE ON STOCK RETURNS by Oleksii Marchenko A thesis submitted in partial fulfillment of the requirements for the degree of MA in Economic Analysis Kyiv School of Economics 2014 Thesis Supervisor: Professor Tom Coupé Approved by ___________________________________________________ Head of the KSE Defense Committee, Professor Irwin Collier __________________________________________________ __________________________________________________ __________________________________________________ Date ___________________________________ Kyiv School of Economics Abstract IMPACT OF POLITICAL COURSE SHIFT IN UKRAINE ON STOCK RETURNS by Oleksii Marchenko Thesis Supervisor: Professor Tom Coupé Since achieving its independence from the Soviet Union, Ukraine has faced the problem which regional block to integrate in. In this paper an event study is used to investigate investors` expectations about winners and losers from two possible integration options: the Free Trade Agreement as a part of the Association Agreement with the European Union and the Custom Union of Russia, Belarus and Kazakhstan. The impact of these two sudden shifts in the political course on stock returns is analyzed to determine the companies which benefit from each integration decisions. No statistically significant impact on stock returns could be detected. However, our findings suggest a large positive reaction of companies` stock prices to the dismissal of Yanukovych regime regardless of company`s trade orientation and political affiliation. -

Worldwide Equipment Guide

WORLDWIDE EQUIPMENT GUIDE TRADOC DCSINT Threat Support Directorate DISTRIBUTION RESTRICTION: Approved for public release; distribution unlimited. Worldwide Equipment Guide Sep 2001 TABLE OF CONTENTS Page Page Memorandum, 24 Sep 2001 ...................................... *i V-150................................................................. 2-12 Introduction ............................................................ *vii VTT-323 ......................................................... 2-12.1 Table: Units of Measure........................................... ix WZ 551........................................................... 2-12.2 Errata Notes................................................................ x YW 531A/531C/Type 63 Vehicle Series........... 2-13 Supplement Page Changes.................................... *xiii YW 531H/Type 85 Vehicle Series ................... 2-14 1. INFANTRY WEAPONS ................................... 1-1 Infantry Fighting Vehicles AMX-10P IFV................................................... 2-15 Small Arms BMD-1 Airborne Fighting Vehicle.................... 2-17 AK-74 5.45-mm Assault Rifle ............................. 1-3 BMD-3 Airborne Fighting Vehicle.................... 2-19 RPK-74 5.45-mm Light Machinegun................... 1-4 BMP-1 IFV..................................................... 2-20.1 AK-47 7.62-mm Assault Rifle .......................... 1-4.1 BMP-1P IFV...................................................... 2-21 Sniper Rifles..................................................... -

WTO Documents Online

WORLD TRADE RESTRICTED WT/ACC/SPEC/UKR/5/Rev.3 24 August 2005 ORGANIZATION (05-3737) Working Party on the Accession of Ukraine DRAFT REPORT OF THE WORKING PARTY ON THE ACCESSION OF UKRAINE TO THE WORLD TRADE ORGANIZATION Revision WT/ACC/SPEC/UKR/5/Rev.3 Page i TABLE OF CONTENTS I. INTRODUCTION ....................................................................................................................1 DOCUMENTATION PROVIDED ......................................................................................................1 INTRODUCTORY STATEMENTS....................................................................................................2 II. ECONOMIC POLICIES..........................................................................................................3 - Monetary and Fiscal Policy......................................................................................................3 - Foreign Exchange and Payments ............................................................................................5 - Investment Regime....................................................................................................................8 - State Ownership and Privatization .......................................................................................10 - Pricing Policies ........................................................................................................................14 - Competition Policy..................................................................................................................21 -

2 General Description of the Russian-Made Vehicle Fleet

;-.. ; : s -- 0--21297 .4 { Public Disclosure Authorized VehicleFle'et Public Disclosure Authorized Characterizationin CentralAsia and, the Caucasus Public Disclosure Authorized Reportfor the RegionalStudy on: CleanerTransportation FuelIs for UrbanAir QualityImprovement Public Disclosure Authorized inCentralAsia -and the Caucasus Vehicle Fleet Characterization in Central Asia and the Caucasus Report for the Regional Study on: Cleaner Transportation Fuels for Urban Air Quality Improvement in Central Asia and the Caucasus Canadian International Development Agency Joint UNDPlWorld Bank Energy Sector ManagementAssistance Programme (ESMAP) Contents Acknowledgments ............................................... vii Abbreviations and Acronyms ............................................... ix Executive Summary ............................................... xi Vehicle Technology in Central Asia and the Caucasus........................................ xii Fleet Octane Requirements ........................................ xiii Inspection and Maintenance Programs ........................................ xiv Uzbekistan's Natural Gas Conversion Program ........................................ xvi Conclusions and Recommendations ....................................... xvii 1 Introduction ................................................ 1 1.1 Objectives .1 1.2 Background .2 Impact of Fuel on Vehicle Emissions .2 Long Range Effects of Emissions .2 Climate Change and Greenhouse Gases .2 Impact of Fuel on Vehicle Technology. 3 1.3 Study Methodology.3 -

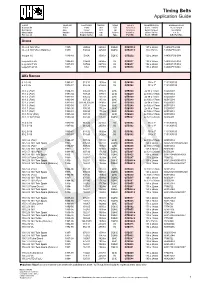

Timing Belts Application Guide

Timing Belts Application Guide merkki vuosimalli moott.sarja tilavuus tyyppi osa n:o hampaita/leveys Ensiasennusosa descripción fecha motor cm3 tipo referencia diente / ancho no. de origen description date moteur cm3 typ référence dents / largeur no.original fahrzeugtyp baujahr motor-kennung ccm formen bestell nr. zähne / breite o.e. nr. For use on Date Engine Series CC Type Part No. Teeth / Width O.E. Part No. Acura CL 2.3i 16V VTec 1997- H23A2 2259cc DOHC QTB335! 127 x 24mm 14400-P14-004 CL 2.3i 16V VTec (Balance) 1997- H23A2 2259cc DOHC QTB291! 70 x 15mm 13405-PT0-004 Integra 1.6 1986-89 D16A 1590cc DOHC QTB252 129 x 24mm 14400-PG6-004 Legend 2.5 V6 1986-88 C25A2 2494cc V6 QTB237 192 x 28mm 14400-PH7-014 Legend 2.7 V6 1987-91 C27A2 2675cc V6 QTB237 192 x 28mm 14400-PH7-014 Legend 3.2i V6 1991- C32 3179cc V6 QTB534 196 x 28mm 14400-PY3-004 Alfa Romeo 6 2.0i V6 1985-87 019.32 1995cc V6 QTB162 134 x 1" 1191303105 6 2.5i V6 1979-87 016.46 2492cc V6 QTB162 134 x 1" 1191303105 33 1.2 (Pair) 1984-89 305.00 1186cc OHC QTB100 2x 98 x 17mm 102500/01 33 1.2 (Pair) 1990-94 307.43 1186cc OHC QTB249 2x 100 x 17mm 60515034 33 1.3 (Pair) 1983-89 305.02 1351cc OHC QTB100 2x 98 x 17mm 102500/01 33 1.3 (Pair) 1990-94 307.32 1351cc OHC QTB249 2x 100 x 17mm 60515034 33 1.5 (Pair) 1983-89 301.46,305.04 1490cc OHC QTB100 2x 98 x 17mm 102500/01 33 1.5 (Pair) 1990-94 307.34 1490cc OHC QTB249 2x 100 x 17mm 60515034 33 1.7 (Pair) 1983-90 305.50 1712cc OHC QTB100 2x 98 x 17mm 102500/01 33 1.7 (Pair) 1990-91 305.50 1712cc OHC QTB249 2x 100 x 17mm 60515034 33 1.7i -

Army Field Manual Volume 2: Generic Enemy (Basic Forces)

D/HQDT/18/34/47 Ar my Code No 71583 (Pt 3) THE ARMY FIELD MANUAL VOLUME II GENERIC ENEMY (BASIC FORCES) PA RT 3 ORBATS AND TABLES OF ORGANISATIONS & EQUIPMENT 1995 Prepared under the direction of the Chief of the General Staff CONDITIONS OF RELEASE (Applicable to copies supplied with Ministry of Defence approval to Common wealth and Foreign Governments). 1. This information is released by the United Kingdom Government to the recipient Government for Defence purposes only. 2. This information must be accorded the same degree of security protection as that accorded thereto by the United Kingdom Government. 3. This information may be disclosed only within the Defence Department of the recipient Government, except as otherwise authorized by the Ministry of Defence (Army). AMENDMENTS Amendment Number By whom amended Date amended AL1 Cover & Facing Page DISTRIBUTION (see Catalogue of Army publications, Part II) Regular Army (other than those mentioned below) ..................................... Scale C TA ............................................................................................................... Scale C Joint Services Defence College ................................................................. 100 Staff College ............................................................................................... 350 JDSC .......................................................................................................... 100 RMCS ........................................................................................................ -

For Potential Foreign Investors & Business Partners

925<'1/'-;/*+ For Potential Foreign Investors & Business Partners 2009 ISBN 978-80-970068-6-0 Sponsored by The American Chamber of Commerce in the Slovak Republic © 2009, Published by ECENTER The American Chamber of Commerce in the Slovak Republic Founded in 1993, the American Chamber of Commerce (AmCham) in Bratislava is an indepen- dent and self-supported organization, relying entirely on contributions from its member compa- nies. Fifteen years after, this membership has grown to more than 300 international and Slovak companies, including a majority of the largest and most important ¿ rms in Slovakia. IMPORTANT ECONOMIC FIGURES 15 Years in Slovakia 20 Percentage of Slovakia´s GDP represented by AmCham members 320 Number of AmCham members* 130,000 Number of employees in AmCham membership 13,000,000,000 Total annual turnover in EUR represented by AmCham members * From the total of AmCham members, approximately 1/3 are subsidiaries of US companies, 1/3 are Slovak com- panies and 1/3 are multinational companies The American Chamber of Commerce in Slovakia Come join us! Crowne Plaza, Hodžovo nám. 2, 811 06 Bratislava Tel: (421-2) 5464 0534, Fax: (421-2) 5464 0535 We´re making E-mail: of¿ [email protected], Web: www.amcham.sk KOŠICE OFFICE: Hlavná 6, 040 01 Košice things happen! Tel./Fax: (421-55) 720 5218, E-mail: [email protected] amchamA52008.indd 1 26.9.2008 10:47:30 We provide help with research, consulting, coaching, management, implementation, and operations. ECENTER – helps its clients to excel Think, Work & Excel with us! ECENTER HELPS your business enter the Slovak market. -

Guide to Assembly Plants in Europe

AN_071112_16_17.qxd 3/13/08 4:11 PM Page 16 PAGE 16 · www.autonew seurope.com November 12, 2007 Guide to assembly plants in Europe BMW GROUP A San Benedetto Val di Sangro, Italy (Sevel Sud: Fiat 50%, (2008). Note: GM has temporary plant on site until 4 Flins, France – Renault Clio III, Clio II (See also 3 , 25 ) PSA 50%) – Citroen Jumper/Relay; Fiat Ducato; permanent plant opens in 2008. 5 Maubeuge, France – Passenger cars: Kangoo, new 1 Dingolfing, Germany – BMW 5-series sedan, station Peugeot Boxer 11 Asaka, Uzbekistan (UzDaewoo: joint venture of GM, Kangoo; LCV: new Kangoo Express, new Kangoo Express wagon, 6-series coupe, convertible, 7-series sedan, B Lieu Saint-Amand, France (Sevel Nord: Fiat 50%, PSA GM Daewoo and Uzautosanoat) – Daewoo Tico, Matiz, Compact; Nissan Kubistar M5 sedan, station wagon, M6 coupe, convertible 50%) – Citroen Atlante/C8, Dispatch/Jumpy; Fiat Scudo, Damas, Nexia, Lacetti; (from kits** starting in 2008) 6 Sandouville, France – Renault Laguna III Sport Tourer and 2 Leipzig, Germany – BMW 1-series 3 door, coupe, Scudo Panorama, Ulysse; Lancia Phedra; Peugeot 807, Chevrolet Epica, Tacuma, Captiva hatchback, Espace IV, Vel Satis convertible, 3-series sedan Expert, TePee A Togliatti, Russia (joint venture of GM and AvtoVAZ) – 7 Palencia, Spain – Renault Megane II hatchback, sport 3 Munich, Germany – BMW 3-series sedan, station wagon Chevrolet Niva, Viva; Opel car (2008) hatch, sport station wagon 4 Regensburg, Germany – BMW 1-series 5 door, 3-series FORD B Warsaw, Poland (FSO: UkrAvto 60%, GM Daewoo 40%) – 8 Valladolid, -

UA Automotive Industry Overview

18.09.2013 Brussels Ukrainian car industry overview Summary 1 Ukraine car industry – core data Indicator Ukraine Population 2013 45,5 Mio Population growth rate 0,56 % Share of employed in automotive <0,1% sector from total employed RU GDP growth 2012 0,2 % GDP per capita 2012 5.770 € Share of automotive sector in GDP 0,9 % DE Inflation (official) 0,1 % CZ UA Unemployment 7,8 % Car density (per 1000 people) 158 Average car age 18,7 Trade deficit formed by automotive -3,9 bln $ import 2012 1 USD = 8,1 UAH; 1 EUR = Exchange Rate (4.09.2013) 10,6 UAH 2 Market review 2 Car producers in Ukraine: capacity underloading Enterprise Model Model Bohdan PrJSC Zaporozhe Automobile ZAZ Lanos, ZAZ Sense, ZAZ Vida, CKD Building Plant ZAZ Chance, ZAZ Forza (ZAZ) 2 Cherkassy PJSC LuAZ Bogdan (VAZ 2110), Hyundai Uzhgorod (Bogdan CKD Tucson 4 Motors) PrJSC Eurocar Illichevsk Skoda (Octavia, Rapid, Fabia, Zaporozhe SKD 1 Superb, Roomster, Yeti) Eurocar 1 Kremenchuk car Geely (MK-1, MK Cross, Emgrand), UkrAvto assembly plant SKD SsangYong (Rexton, Kyron, UkrAvto Ltd. (KrASZ) Korando) Current average plant Car production by year 05 06 07 08 09 10 11 12 capacity loading is only In k units per year 196,7 267,2 380,1 400,8 65,6 75,3 97,6 69,7 17,4%. Existing total plant capacity in 2012 amounted to 400 k units per year Source: Ukrautoprom 3 New passenger cars market 4 Passenger cars sales dynamics of locally produced and imported cars – sales of locally produced cars X – passenger cars market in k units Х% – share of internally produced cars From May10%. -

Army Field Manual Volume 2: Generic Enemy (Mobile Forces)

D/HQDT/18/34/48 Army Code No 71584 (Pt 2) THE ARMY FIELD MANUAL VOLUME II GENERIC ENEMY (MOBILE FORCES) PART 2 TABLES OF ORGANISATIONS & EQUIPMENT PRESS HERE TO RETURN TO MAIN CONTENTS PAGE 1996 Prepared under the direction of the Chief of the General Staff AL1 Copyright This work is Crown copyright and the intellectual property rights for this publication belong exclusively to the Ministry of Defence (MOD). No material or information contained in this publication should be repro- duced, stored in a retrieval system or transmitted in any form outside MOD establishments except as authorised by both the sponsor and the MOD where appropriate. Authority This publication is issued under the overall direction of the CGS . It is an MOD Approved Code of Practice (ACOP). Status The contents provide clear military information concerning the most up to date experience and best practice available for commanders and troops to use in their operations and training. Amendment Amendment No Date Amendment No Date 1 - (INCORPORATED) SEP 97 Distribution As directed by ___________LW1 DGD&D who is the sponsor and to whom comments and queries concerning this publication should be addressed. PREFACE GENFORCE MOBILE FORCES GENFORCE 1. The purpose of the Generic Enemy Force (GENFORCE) is to provide a basis for the generation of enemy forces for all except the most specialised training needs. It is designed to be used flexibly, in a modular fashion, to craft enemy requirements for training. 2. GENFORCE offers three types of artificial, yet challenging and realistic, opposing force options. It has been issued in a series of three packages: Basic Forces: This enemy has heavy and light armoured forces, predominantly equipped along Former Soviet Union (FSU) lines. -

Corporate Governance in Ukraine / Not Gone with the Wind / May 2013

Ukraine| Research Corporate Governance Corporate Governance in Ukraine Not gone with the wind July 2013 Аlexander Paraschiy, Zenon Zawada, Roman Topolyuk, Roman Dmytrenko +380 44 391 5577 CONCORDE CAPITAL Corporate Governance in Ukraine July 2013 FOREWORD Companies not gone with the winds of change and hurricanes of crisis – upholding and preserving high standards of relations with investors and practices of corporate governance – are the foundation of our securities market, without exaggeration. And we’d like them to become the main heroes of our new story about corporate governance. Despite many disappointments in the history of the relatively young Ukrainian stock market, and in the history of our even younger study of corporate governance practices, they are there nevertheless. There are companies out there that are pleasant to work with for analysts and investors alike. There are companies that have stood the test of time and preserved the ability to be financed by capital markets. Despite noticing that high standards and practices are enforced mainly from without, and such standards are not always entirely grasped by the founders of Ukrainian business, we are satisfied that the number of companies striving to be better is increasing. It is increasing mainly owing to newcomers to the securities market: those who dared to take on the increasing requirements for Ukrainian issuers and those who are ready to adopt better practices in order to conform to international standards. We realize that a part of the newcomers (and newcomers, as our research shows, always behave themselves exemplarily) can loosen their high standards shown at their beginnings.