Plan and Budget Guidelines for 2012/13 in the Implementation Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE UNITED REPUBLIC of TANZANIA Tanzania Airports Authority

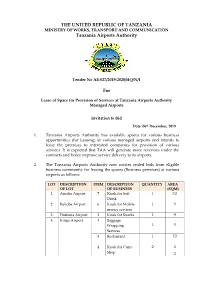

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION Tanzania Airports Authority Tender No AE-027/2019-2020/HQ/N/1 For Lease of Space for Provision of Services at Tanzania Airports Authority Managed Airports Invitation to Bid Date: 06th December, 2019 1. Tanzania Airports Authority has available spaces for various business opportunities (for Leasing) at various managed airports and intends to lease the premises to interested companies for provision of various services. It is expected that TAA will generate more revenues under the contracts and hence improve service delivery to its airports. 2. The Tanzania Airports Authority now invites sealed bids from eligible business community for leasing the spaces (Business premises) at various airports as follows: LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 1. Arusha Airport 7 Kiosk for Soft 1 33 Drink 2. Bukoba Airport 6 Kiosk for Mobile 1 4 money services 3. Dodoma Airport 3 Kiosk for Snacks 1 4 4. Iringa Airport 1 Baggage Wrapping 1 4 Services 3 Restaurant 1 72 4 Kiosk for Curio 2 3 Shop 3 LOT DESCRIPTION ITEM DESCRIPTION QUANTITY AREA OF LOT OF BUSINESS (SQM) 5 Kiosk for Retail 1 3.5 shop 5. Kigoma Airport 1 Baggage Wrapping 1 4 Services 2 Restaurant 1 19.49 3 Kiosk for Retail 2 19.21 shop 4 Kiosk for Snacks 1 9 5 Kiosk for Curio 1 6.8 Shop 6. Kilwa Masoko 1 Restaurant 1 40 Airport 2 Kiosk for soft 1 9 drinks 7. Lake Manyara 2 Kiosk for Curio 10 84.179 Airport Shop 3 Kiosk for Soft 1 9 Drink 4 Kiosk for Ice 1 9 Cream and Beverage Outlet 5 Car Wash 1 49 6 Kiosk for Mobile 1 2 money services 8. -

National Environment Management Council (Nemc)

NATIONAL ENVIRONMENT MANAGEMENT COUNCIL (NEMC) NOTICE TO COLLECT APPROVED AND SIGNED ENVIRONMENTAL CERTIFICATES Section 81 of the Environment Management Act, 2004 stipulates that any person, being a proponent or a developer of a project or undertaking of a type specified in Third Schedule, to which Environmental Impact Assessment (EIA) is required to be made by the law governing such project or undertaking or in the absence of such law, by regulation made by the Minister, shall undertake or cause to be undertaken, at his own cost an environmental impact assessment study. The Environmental Management Act, (2004) requires also that upon completion of the review of the report, the National Environment Management Council (NEMC) shall submit recommendations to the Minister for approval and issuance of certificate. The approved and signed certificates are returned to NEMC to formalize their registration into the database before handing over to the Developers. Therefore, the National Environment Management Council (NEMC) is inviting proponents/developers to collect their approved and signed certificates in the categories of Environmental Impact Assessment, Environmental Audit, Variation and Transfer of Certificates, as well as Provisional Environmental Clearance. These Certificates can be picked at NEMC’s Head office at Plot No. 28, 29 &30-35 Regent Street, Mikocheni Announced by: Director General, National Environment Management Council (NEMC), Plot No. 28, 29 &30-35 Regent Street, P.O. Box 63154, Dar es Salaam. Telephone: +255 22 2774889, Direct line: +255 22 2774852 Mobile: 0713 608930/ 0692108566 Fax: +255 22 2774901, Email: [email protected] No Project Title and Location Developer 1. Construction of 8 storey Plus Mezzanine Al Rais Development Commercial/Residential Building at plot no 8 block Company Ltd, 67, Ukombozi Mtaa in Jangwani Ward, Ilala P.O. -

THE UNITED REPUBLIC of TANZANIA PRIME MINISTER’S OFFICE, REGIONAL ADMINISTRATION and LOCAL GOVERNMENTS Public Disclosure Authorized

THE UNITED REPUBLIC OF TANZANIA PRIME MINISTER’S OFFICE, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENTS Public Disclosure Authorized P.O. Box 1923 P.O. Box 1923, Tel: 255 26 2321607, Fax: 255 26 2322116 DODOMA Public Disclosure Authorized CONTRACT No. ME/022/2012/2013/CR/11 FOR FEASIBILITY STUDY AND DETAILED ENGINEERING DESIGN OF DAR ES SALAAM LOCAL ROADS FOR MUNICIPAL COUNCILS OF KINONDONI, ILALA AND TEMEKE IN SUPPORT OF PREPARATION OF THE PROPOSED DAR ES SALAAM METROPOLITANT DEVELOPMENT PROJECT(DMDP) Public Disclosure Authorized THE ENVIRONMENTAL AND SOCIAL IMPACT ASSESSMENT REPORT (ESIA) OF THE PROPOSED LOCAL ROADS SUBPROJECTS IN ILALA MUNICIPALITY (25.5 KM) DECEMBER 2014 CONSULTANT: Public Disclosure Authorized RUBHERA RAM MATO Crown TECH-Consult Ltd Consulting Engineers, Surveyors & Project Managers P. O. Box 72877, Telephone (022) Tel. 2700078, 0773 737372, Fax 2771293, E-mail: [email protected], [email protected] DAR ES SALAAM, Tanzania ESIA Report for the Proposed Upgrading of the Ilala Local Roads PMO-RALG STUDY TEAM NAME POSITION SIGNATURE Dr. Rubhera RAM Mato Environmentalist and ESIA Team Leader Mr. George J. Kimaro Environmental Engineer Anna S. K. Mwema Sociologist The following experts also participated in this study, Mr. Yoswe Msongwe - Sociologist Ms. Anna Msofe - Sociologist Mr. Aman D. Ancelm - Sociologist i ESIA Report for the Proposed Upgrading of the Ilala Local Roads PMO-RALG EXECUTIVE SUMMARY Environmental and Social Impact Assessment Report for the proposed Local Roads Subproject in Ilala Municipality (25.5 Km) Under the Dar Es Salaam Metropolitan Development Project (DMDP) Proponent: The United Republic of Tanzania, Prime Minister's Office, Regional Administration and Local Governments Proponent’s Contact: P.O. -

Crime and Policing Issues in Dar Es Salaam Tanzania Focusing On: Community Neighbourhood Watch Groups - “Sungusungu”

CRIME AND POLICING ISSUES IN DAR ES SALAAM TANZANIA FOCUSING ON: COMMUNITY NEIGHBOURHOOD WATCH GROUPS - “SUNGUSUNGU” PRESENTED AT THE 1st SUB SAHARAN EXECUTIVE POLICING CONFERENCE INTERNATIONAL ASSOCIATION OF CHIEFS OF POLICE (IACP) DURBAN, SOUTH AFRICA: 27 – 30 AUGUST, 2000 Contents PREFACE:.........................................................................................................................................................................................I EXECUTIVE SUMMARY............................................................................................................................................................III 1.0 INTRODUCTION............................................................................................................................................................ 7 DAR ES SALAAM IN BRIEF............................................................................................................................................................. 7 1.1 GEOGRAPHICAL LOCATION:......................................................................................................................................... 7 1.2 HISTORICAL:.................................................................................................................................................................. 7 1.3 SOCIO-ECONOMIC AND ENVIRONMENTAL SETTING:.................................................................................................. 9 1.4 ORGANISATIONAL SETTING:.......................................................................................................................................13 -

Citywide Action Plan for Upgrading Unplanned and Unserviced Settlements in Dar Es Salaam

Citywide Action Plan for Upgrading Unplanned and Unserviced Settlements in Dar es Salaam DAR ES SALAAM LOCAL AUTHORITIES The designations employed and the presentation of the material in this report do not imply the expression of any opinion whatsoever on the part of the United Nations Secretariat concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. Reference to names of firms and commercial products and processes does not imply their endorsement by the United Nations, and a failure to mention a particular firm, commercial product or process is not a sign of disapproval. Excerpts from the text may be reproduced without authorization, on condition that the source is indicated. UN-HABITAT Nairobi, 2010 HS: HS/163/10E ISBN: 978-92-1-132276-7 An electronic version of the final version of this publication will be available for download from the UN-HABITAT web-site at http://www.unhabitat.org /publications UN-HABITAT publications can be obtained from our Regional Offices or directly from: United Nations Human Settlements Programme (UN-HABITAT) P.O. Box 30030, Nairobi 00100, KENYA Tel: 254 20 7623 120 Fax: 254 20 7624 266/7 E-mail: [email protected] Website: http://www.unhabitat.org Photo credits: Rasmus Precht (front cover), Samuel Friesen (back cover) Layout: Godfrey Munanga & Eugene Papa Printing: Publishing Services Section, Nairobi, ISO 14001:2004 - certified. Citywide Action Plan for Upgrading Unplanned and Unserviced Settlements in Dar -

In Search of Urban Recreational Ecosystem Services in Dar Es Salaam, Tanzania

Environment for Development Discussion Paper Series March 2018 EfD DP 18-06 In Search of Urban Recreational Ecosystem Services in Dar es Salaam, Tanzania Byela Tibesigwa, Razack Lokina, Fred Kasalirwe, Richard Jacob, Julieth Tibanywana, and Gabriel Makuka Environment for Development Centers Central America Chile China Research Program in Economics and Research Nucleus on Environmental and Environmental Economics Program in China Environment for Development in Central Natural Resource Economics (NENRE) (EEPC) America Tropical Agricultural Research and Universidad de Concepción Peking University Higher Education Center (CATIE) India Colombia Ethiopia Centre for Research on the Economics of The Research Group on Environmental, Environment and Climate Research Center Climate, Food, Energy, and Environment, Natural Resource and Applied Economics (ECRC) (CECFEE), at Indian Statistical Institute, New Studies (REES-CEDE), Universidad de los Ethiopian Development Research Institute Delhi, India Andes, Colombia (EDRI) Kenya South Africa Sweden School of Economics Environmental Economics Policy Research Environmental Economics Unit University of Nairobi Unit (EPRU) University of Gothenburg University of Cape Town Tanzania USA (Washington, DC) Vietnam Environment for Development Tanzania Resources for the Future (RFF) University of Economics University of Dar es Salaam Ho Chi Minh City, Vietnam In Search of Urban Recreational Ecosystem Services in Dar es Salaam, Tanzania Byela Tibesigwa, Razack Lokina, Fred Kasalirwe, Richard Jacob, Julieth Tibanywana, -

Formal and Informal Practices for Affordale Urban Housing

FORMAL AND INFORMAL PRACTICES FOR AFFORDALE URBAN HOUSING Case study: Dar es Salaam, Tanzania MEDARD Z. MUSHUMBUSI Doctoral Thesis in Infrastructure Stockholm, Sweden, 2011 Doctoral Thesis 2011 Kungliga Tekniska högskolan Royal Institute of Technology School of Architecture and the Built Environment Department of Urban Planning and Environment Division of Urban and Regional Studies S-100 44 Stockholm http://www.kth.se/ TRITA-SoM 2011-02 ISSN 1653-6126 ISRN KTH/SoM/11-02/SE ISBN 978-91-7415-882-3 © Medard Z. Mushumbusi i CHAPTER BREAKDOWN CHAPTER - Introduction…………………………………….... 1 1.1 Problem setting………………………………………………...... 1 1.2 Research Problem……………………………………………...... 3 1.3 Aim of the Research. ………………………………………….... 4 1.4 Objectives of the Research………………………..…………...... 4 1.5 Research Questions. …………………………………………..... 4 1.6 Delimitation of the Research scope…………………………...... 5 1.7 Structure of the Thesis………………………………………...... 5 1.8 Significance of the Study……………………………………...... 6 CHAPTER 2 –Conceptual and Theoretical Framework …..... 8 2.1 Introduction ……………………………………………………..... 8 2.2 Formality………………………………………………………...... 10 2.3 Informality……………………………………………………....... 12 2.4 Self Help……………………………...………..………….…….... 15 2.5 Governance……………………………………………………...... 18 2.6 Relation between Formality and Informality................................... 20 2.7 Concluding Remarks…………………………………………........ 23 CHAPTER 3 –An Overview of Urban Housing and Its Regulatory Framework in Tanzania………………………...... 24 3.1 Introduction……………………………………………………...... 24 3.2 Urbanization and its Influence on Housing …………………….. 24 3.3 The National Shelter Strategies………………………………....... 27 3.4 Regulating Urban Land for Housing …………………………...... 35 3.5 Regulating Human Settlements ………………………………...... 38 3.6 Regulatory Reforms in Tanzania- Salient Features ……………… 40 3.7 Housing in Dar es Salaam within the Planning Context ……........ 42 3.8 Concluding Remarks …………………………………………...... 52 CHAPTER 4 – Research Design and Methodology for the Empirical Study……………………………... -

Tanzania Travel Guide

Tanzania Travel Guide Lake Malawi in Africa Tanzania is located in the eastern region of Africa. It shares its borders with Kenya, Rwanda, Uganda, Congo, Burundi, Zambia, Mozambique, and Malawi. The Indian Ocean also borders the country. Dodoma is the capital city of Tanzania, and Dar Es Salaam is the commercial capital of the country. The country achieved its independence from Britain on December 9th, 1961. The official languages of Tanzania are Swahili and English. Arabic is also spoken widely in Tanzania. Tanzania is divided into 26 regions or " mkoa" like Arusha, Dodoma, Dar Es Salaam, Kigoma, etc. The best time to visit the country is between May to July, or you could also go between the months November to March. Try and avoid going to Tanzania during the rainy season, which begins from April and lasts for a month. Some of the tourist attractions in Tanzania are: National Museum, Dar es Salaam Serengeti National Park Mikumi National Park Selous Game Reserve Gombe National Park Ngorongoro Crater Mount Kilimanjaro Getting In Tanzania can be accessed not only with the help of flights but, trains, buses, etc., are available to the outsiders with the help of which the people can connect with this country. The country with its two international airports of Julius Nyerere International Airport and Kilimanjaro International Airport, is responsible for maintaining relations with a lot of other countries on the globe. The international airlines which frequently brings the foreigners from the distant countries are: Air Comores International -

Dar Report 2 2Full

Service Provision Governance in the Peri-urban Interface of Metropolitan Areas Research Project WSS PRACTICES AND LIVING CONDITIONS IN THE PERI-URBAN INTERFACE OF METROPOLITAN DAR ES SALAAM: THE CASES OF TUNGI AND STAKISHARI DRAFT FOR DISCUSSION University College of Lands and Architectural Studies (UCLAS) Dar es Salaam, Tanzania For more information, please contact: Peri-urban Research Project Team Development Planning Unit University College London 9 Endsleigh Gardens London WC1H 0ED United Kingdom Tel. +44 (0)20 76791111 Fax: +44 (0)20 76791112 E-mail project: [email protected] Email paper authors: [email protected] PUI website: http://www.ucl.ac.uk/dpu/pui ãThe Development Planning Unit Disclaimer: This document is an output from a project funded by the UK Department for International Development (DFID) for the benefit of developing countries. The views expressed are not necessarily those of DFID. DPU Service Provision Governance in the Peri-urban Interface of Metropolitan Areas ABOUT THE PROJECT This report is one of several outputs from the project Service provision governance in the peri- urban interface of metropolitan areas. This is a three-year project run by the Development Planning Unit, University College London in collaboration with a number of institutions from developing countries and with support from the UK Government’s Department for International Development (DFID). The purpose of the project is to improve guidance on governance and management of water and sanitation in the peri-urban interface (PUI) of metropolitan areas, in order to increase access by the poor and promote environmental sustainability. Presently there is a gap in the operating knowledge of implementing agencies on the specific problems that arise in the PUI. -

Tender Notice for Non Consultancy Services

TENDER NOTICE FOR NON CONSULTANCY SERVICES Ilala Municipal Council Tender No LAG/015/MIC/2019-2020/HQ/NCS/24 LOT 16 – 36 For UWAKALA WA KUFANYA USAFI, KUKUSANYA TAKA NGUMU KWENYE MAKAZI YA WATU, MAJENGO YA BIASHARA, MITAA NA OFISI MBALIMBALI,KUZOA TAKA NA KUZIPELEKA KATIKA DAMPO LA PUGU KINYAMWEZI NA KUKUSANYA ADA ZA TAKA KATIKA KATA ZA PEMBEZONI ZA HALMASHAURI YA MANISPAA YA ILALA Invitation to Tender Date 28/03/2020 1. This Invitation for Tenders follows the General Procurement Notice for this Project which appeared in TANEPS Issue no. 4 dated 24/03/2020. 2. The Government of the United Republic of Tanzania has set aside funds for the operation of the Ilala Municipal Council during the financial year 2019/2020. It is intended that part of the proceeds of the fund will be used to cover eligible payment under the contract for the UWAKALA WA KUFANYA USAFI, KUKUSANYA TAKA NGUMU KWENYE MAKAZI YA WATU, MAJENGO YA BIASHARA, MITAA NA OFISI MBALIMBALI,KUZOA TAKA NA KUZIPELEKA KATIKA DAMPO LA PUGU KINYAMWEZI NA KUKUSANYA ADA ZA TAKA KATIKA KATA ZA PEMBEZONI ZA HALMASHAURI YA MANISPAA YA ILALA. 4. The Ilala Municipal Council now invites sealed Tenders from eligible Service providers of UWAKALA WA KUFANYA USAFI, KUKUSANYA TAKA NGUMU KWENYE MAKAZI YA WATU, MAJENGO YA BIASHARA, MITAA NA OFISI MBALIMBALI,KUZOA TAKA NA KUZIPELEKA KATIKA DAMPO LA PUGU KINYAMWEZI NA KUKUSANYA ADA ZA TAKA KATIKA KATA ZA PEMBEZONI ZA HALMASHAURI YA MANISPAA YA ILALA as follows: Lot No. Lot Name Description 1 KATA YA KINYEREZI LOT 16 2 KATA YA SEGEREA LOT 17 3 KATA YA KIPAWA A. -

Dar Es Salaam, Tanzania

Volume 5, Issue 7, July – 2020 International Journal of Innovative Science and Research Technology ISSN No:-2456-2165 Assessment of the Refuse Collection Charges in Covering Waste Management Cost: The Case of ILALA Municipality -Dar Es Salaam, Tanzania TP. Dr. Hussein M. Omar, Registered Town Planner and Environmental Officer, Vice President Office-Division of Environment (United Republic of Tanzania), P.O .Box 2502, Dodoma, Tanzania. Abstract:- The world urban population is expected to II. OBJECTIVE increase by 72 per cent by 2050, to reach nearly 6 billion in 2050 from 3 billion in 2011 (UN, 2012, Hussein 2019). The study aimed at assessing RCCs collection By mid-century the world urban population will likely efficiency in covering solid waste management Cost in Ilala be the same size as the world’s total population was in Municipality. 2002 (UN, 2011, and Hussein, 2018). Although the global average in 2014 reached 54 per cent, the Specific Objectives percentages are already around 80% in the Americas, To analyse waste management database for Ilala and over 70% in Europe and Oceania, but only 48% in Municipality Asia and 40% in Africa (UN, 2014, Hussein, 2019). To analyses the challenges for effective RCCs collection in Ilala Municipality I. INTRODUCTION To recommend on the best practice In Tanzania statistical trend indicates that proportion III. LITERATURE REVIEW of the population living in urban areas is ever-increasing. According to URT, 2002 in Bakanga 2014, the urbanisation A. Theories and Concepts rate increased from 5% in 1967 to 13% in 1978 and from Governance Concept 21% in 1988 to 27% in 2002. -

The United Republic of Tanzania Ministry of Works, Transport and Communication Tanzania Airports Authority Proposed Projects

THE UNITED REPUBLIC OF TANZANIA MINISTRY OF WORKS, TRANSPORT AND COMMUNICATION TANZANIA AIRPORTS AUTHORITY PROPOSED PROJECTS WRITE UP FOR THE BELGIAN TRADE MISSION TO TANZANIA NOVEMBER, 2 0 1 6 , S No. REMARKS I. PROJECT NAME Upgrading of MWANZA AIRPORT PROJECT CODE 4209 PROJECT LOCATION IATA:MWZ; ICA0:1-1.TMW; with elevation above mean sea level (AMSL) 3763ft/1147m FEASIBILITY STUDY Feasibility Study for construction of new terminal building REMARKS and landside pavements, parallel taxiway, widening of runway 45wide to 60m including relocation of AGL System and improvement of storm water drainage was completed in June, 2016 STATUS Contractor for extension of runway, rehabilitation of taxiway to bitumen standard, extension of existing apron and cargo apron, construction of control tower, cargo building, power house and water supply system has resumed to site. ncti, ahold03-)3 ConSkiNclp4) N_ Teicyrri2 WORKS REQUIRING and landside paveThents, parallel taxiway, widening of runway FUNDING 45wide to 60m including relocation of AGL System and improvement of storm water drainage PROJECT COST ESTIMATES/ USD.113 Million FINANCING GAP1 • Improved efficiency and comfort upon construction of new terminal building. • Improved efficiency upon installation of AGL and NAVAIDS • Improved safety upon Construction of Fire Station and PROJECT BENEFITS associated equipment • Improved safety and security upon construction of Control Tower • Improved security upon implementation of security programs. FINANCING MODE PPP, EPC, Bilateral and Multilateral Financing