Intermediated Securities: Who Owns Your Shares? a Scoping Paper

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

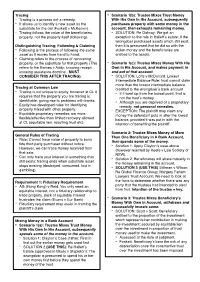

Tracing Is a Process Not a Remedy

Tracing - Scenario 1(b): Trustee Mixes Trust Money - Tracing is a process not a remedy. With His Own In His Account, subsequently - It allows us to identify a new asset as the purchases property with some money in the substitute for the old (Foskett v McKeown). account, then exhausts remaining money. - Tracing follows the value of the beneficiaries - SOLUTION: Re Oatway: We get an property, not the property itself (following). exception to the rule in Hallett’s estate: if the wrongdoer purchased assets which still exist, Distinguishing Tracing; Following & Claiming then it is presumed that he did so with the - Following is the process of following the same stolen money and the beneficiaries are asset as it moves from hand to hand. entitled to the assets. - Claiming refers to the process of recovering property, or the substitute for that property (This - Scenario 1(c): Trustee Mixes Money With His refers to the Barnes v Addy; knowing receipt, Own In His Account, and makes payment in knowing assistance doctrine - MUST and out of that account. CONSIDER THIS AFTER TRACING). - SOLUTION: Lofts v McDonald: Lowest Intermediate Balance Rule: trust cannot claim more than the lowest intermediate balance Tracing at Common Law - credited to the wrongdoer’s bank account Tracing is not unique to equity, however at CL it - If it went up from the lowest point, that is requires that the property you are tracing is not the trust’s money. identifiable, giving rise to problems with banks. - - Although you are deprived of a proprietary Equity has developed rules for identifying remedy, not personal remedies. -

The Functions of Trust Law: a Comparative Legal and Economic Analysis, 73 N.Y.U

University of California, Hastings College of the Law UC Hastings Scholarship Repository Faculty Scholarship 1998 The uncF tions of Trust Law: A Comparative Legal and Economic Analysis Ugo Mattei UC Hastings College of the Law, [email protected] Follow this and additional works at: http://repository.uchastings.edu/faculty_scholarship Part of the Comparative and Foreign Law Commons, and the Estates and Trusts Commons Recommended Citation Ugo Mattei, The Functions of Trust Law: A Comparative Legal and Economic Analysis, 73 N.Y.U. L. Rev. 434 (1998). Available at: http://repository.uchastings.edu/faculty_scholarship/529 This Article is brought to you for free and open access by UC Hastings Scholarship Repository. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of UC Hastings Scholarship Repository. For more information, please contact [email protected]. Faculty Publications UC Hastings College of the Law Library Mattei Ugo Author: Ugo Mattei Source: New York University Law Review Citation: 73 N.Y.U. L. Rev. 434 (1998). Title: The Functions of Trust Law: A Comparative Legal and Economic Analysis Originally published in NEW YORK UNIVERSITY LAW REVIEW. This article is reprinted with permission from NEW YORK UNIVERSITY LAW REVIEW and New York University School of Law. THE FUNCTIONS OF TRUST LAW: A COMPARATIVE LEGAL AND ECONOMIC ANALYSIS HENRY HANSMANN* UGO MATTEI** In this Article, ProfessorsHenry Hansmann and Ugo Mattei analyze the functions served by the law of trusts and ask, first, whether the basic tools of contract and agency law could fulfill the same functions and, second, whether trust law provides benefits that are not provided by the law of corporations. -

The Presumption of Resulting Trust and Beneficiary Designations: What’S Intention Got to Do With

The presumption of resulting trust and beneficiary designations: What’s intention got to do with it? Jason M. Chin University of Toronto Faculty of Law; Dentons Canada LLP Archie Rabinowitz & Aoife Quinn Dentons Canada LLP *The authors heartily acknowledge the gracious support of Ian Colvin, research librarian. - 2 - Abstract When opening an RRSP or RRIF, investors typically designate a beneficiary. We expect that, when making this choice, most investors intend that their designated beneficiary will indeed benefit from the investment on their death. And further, if there is a dispute between the designated beneficiary and the investor’s estate, we expect investors intend that their choice of beneficiary will prevail. Surprisingly, this is not the case in many provincial appellate courts, which in fact favour the estate in such disputes. More specifically, most Canadian courts apply the presumption of resulting trust to beneficiary designations: they assume, absent other evidence, that the designated beneficiary holds the proceeds of the RRSP or RRIF in trust for the deceased investor’s estate. Only Saskatchewan has taken a contrary position. The Alberta Court of Queen’s Bench in Morrison v Morrison recently weighed both options and endorsed the approach that applies the presumption of resulting trust. In the present article, we analyze the doctrine of resulting trust, its rationale as presented by several leading cases, and empirical evidence evaluating the intentions of Canadian investors. We conclude that applying the presumption of resulting trust to beneficiary designations betrays both the theory and purpose of the presumption. It also runs counter to the intentions of most Canadians and creates uncertainties in millions of beneficiary designations. -

Trust Law in the United States. a Basic Study of Its Special Contribution Ugo Mattei UC Hastings College of the Law, [email protected]

University of California, Hastings College of the Law UC Hastings Scholarship Repository Faculty Scholarship 1998 Trust Law in the United States. A Basic Study of Its Special Contribution Ugo Mattei UC Hastings College of the Law, [email protected] Henry Hansmann Follow this and additional works at: http://repository.uchastings.edu/faculty_scholarship Recommended Citation Ugo Mattei and Henry Hansmann, Trust Law in the United States. A Basic Study of Its Special Contribution, 46 Am. J. Comp. L. Supp. 133 (1998). Available at: http://repository.uchastings.edu/faculty_scholarship/1290 This Article is brought to you for free and open access by UC Hastings Scholarship Repository. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of UC Hastings Scholarship Repository. For more information, please contact [email protected]. TOPIC II.A.3 HENRY HANSMANN & UGO MATTEI Trust Law in the United States. A Basic Study of Its Special Contribution In the United States, academic commentary and law school cur- ricula continue to focus on the private trust in its historical role as a device for intrafamily wealth transfers, a rather technical and nar- row ground to approach our topic. Vastly more important is today the enormous - though commonly neglected - role that private trusts have come to play in the American capital markets.' To take just the most conspicuous examples, pension funds and mutual funds, both of which are generally organized as trusts, together now hold roughly forty per cent of all U.S. equity securities and thirty per cent of corpo- rate and foreign bonds.2 Similarly, turning from the demand side to the supply side of the securities markets, asset securitization trusts are now the issuers of a large fraction of all outstanding American debt securities - more than $2 trillion worth.3 This report rather then following the details of trust law as de- scribed in American law books will focus on the general economic functions served by a separate law of trusts. -

Landmark Cases in Tracing – a Pitch

Landmark Cases in Tracing – A Pitch Landmark Cases in Tracing A pitch for an edited collection of in-depth case analyses Dr Derek Whayman, Newcastle University. [email protected] Prof Katy Barnett, University of Melbourne. [email protected] Theme and Justification Tracing is a process and claim used for recovering misappropriated property, mainly that originally held on trust or by a corporation. It allows claimants to recover not only the original misappropriated property, but also its substitute – what the property was exchanged for in a subsequent transaction. Since this claim is a right of property, it brings the claimant the advantage of priority over other creditors in insolvency and access to any increase in value, either in the property itself or from the substitute. If the property is passed to or from another person or, say, a shell company, the right to claim follows that property and is not left on the person. From this, it is no wonder it is popular with claimants. However, tracing is still under-researched and under-theorised. There is little agreement as to how this claim can be justified theoretically, what its limits are and how they vary in accordance with the multitude of different facts the courts have seen and will see in the future. Academics and judges are still feeling their way around its fundamental questions. Yet not only are the answers to these theoretical questions controverted, they go to the heart of what every litigant wants to know: what may or may not be claimed? These questions are of fundamental importance on a practical basis too. -

Memorandum of Law for the International Swaps and Derivatives Association, Inc

MEMORANDUM OF LAW FOR THE INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. Collateral Provider Insolvency: Validity and Enforceability under English Law of Collateral Arrangements under the ISDA Credit Support Documents 13 November 2018 Allen & Overy LLP One Bishops Square London E1 6AD United Kingdom Tel +44 (0)20 3088 0000 Fax +44 (0)20 3088 0088 Allen & Overy LLP is a limited liability partnership registered in England and Wales with registered number OC306763. It is authorised and regulated by the Solicitors Regulation Authority of England and Wales. The term partner is used to refer to a member of Allen & Overy LLP or an employee or consultant with equivalent standing and qualifications. A list of the members of Allen & Overy LLP and of the non-members who are designated as partners is open to inspection at its registered office, One Bishops Square, London E1 6AD. Allen & Overy LLP or an affiliated undertaking has an office in each of: Abu Dhabi, Amsterdam, Antwerp, Bangkok, Barcelona, Beijing, Belfast, Bratislava, Brussels, Bucharest (associated office), Budapest, Casablanca, Doha, Dubai, Düsseldorf, Frankfurt, Hamburg, Hanoi, Ho Chi Minh City, Hong Kong, Istanbul, Jakarta (associated office), Johannesburg, London, Luxembourg, Madrid, Milan, Moscow, Munich, New York, Paris, Perth, Prague, Riyadh (cooperation office), Rome, São Paulo, Seoul, Shanghai, Singapore, Sydney, Tokyo, Warsaw, Washington, D.C. and Yangon. ICM:28162951.19 [This page left intentionally blank.] TABLE OF CONTENTS I. INTRODUCTION .................................................................................................................... -

Claims Against Third-Party Recipients of Trust Property

Cambridge Law Journal, 76(2), July 2017, pp. 399–429 © Cambridge Law Journal and Contributors 2017. This is an Open Access article, distributed under the terms of the Creative Commons Attribution-NonCommercial-ShareAlike licence (http:// creativecommons.org/licenses/by-nc-sa/4.0/), which permits non-commercial re-use, distribution, and reproduction in any medium, provided the same Creative Commons licence is included and the original work is properly cited. The written permission of Cambridge University Press must be obtained for commercial re-use. doi:10.1017/S0008197317000423 CLAIMS AGAINST THIRD-PARTY RECIPIENTS OF TRUST PROPERTY DAVID SALMONS* ABSTRACT. This article argues that claims to recover trust property from third parties arise in response to a trustee’s duty to preserve identifiable property, and that unjust enrichment is incompatible with such claims. First, unjust enrichment can only assist with the recovery of abstract wealth and so it does not assist in the recovery of specific property. Second, it is difficult to identify a convincing justification for introducing unjust enrich- ment. Third, it will work to the detriment of innocent recipients. The article goes on to show how Re Diplock supports this analysis, by demonstrating that no duty of preservation had been breached and that a proprietary claim should not have been available in that case. The simple conclusion is that claims to recover specific property and claims for unjust enrichment should be seen as mutually exclusive. KEYWORDS: trusts, third parties, proprietary claims, knowing receipt, res- titution, unjust enrichment, Re Diplock. I. INTRODUCTION According to orthodox trust principles, where property is transferred in breach of trust, a beneficiary can either bring a proprietary claim to recover the property or a personal claim against a knowing recipient of the trust property (hereinafter, the combination of these two claims will be referred to as the “equitable regime”). -

Obligation and Property in Tracing Claims

CORE Metadata, citation and similar papers at core.ac.uk Provided by Newcastle University E-Prints Obligation and Property in Tracing Claims Derek Whayman* [email protected] Newcastle Law School Newcastle University 21–24 Windsor Terrace Newcastle upon Tyne NE1 7RU Abstract Tracing is said to be merely a process and separate from claiming. It is then characterised as a set of pure property identification rules which cannot vary from claim to claim. However, the development of tracing in equity relied heavily on the fiduciary obligation to support its rules. While many of tracing’s rules can be justified independently of the fiduciary obligation or rationalised as evidential presumptions, others cannot. This means it is impossible to detach the process from the claim. Furthermore, it would be undesirable to do so because it would reduce the flexibility of tracing. Introduction Tracing, according to the present conventional wisdom, is a process used to support a number of separate, mostly proprietary, claims. “[A] clear distinction must be drawn between the rules of following and tracing, which are essentially evidential in nature, and rules [of claiming] which determine substantive rights.”1 Any peculiarities of the claim should remain there and not fall in the rules of tracing. All tracing does is make the link – it identifies where the value is, whether it passes through a link between old property and its new substitute and to what extent. For example, if I spend £100 on a vase, tracing only says that the vase is subject to any claim that the £100 was. -

Tracing in the Age of Restitution 377

2003 Tracing in the Age of Restitution 377 TRACING IN THE AGE OF RESTITUTION MARGARET STONE∗ AND ALISTAIR MCKEOUGH∗∗ Restitution is a remedy by which a plaintiff may recover a benefit, enrichment or value that the defendant has obtained at the expense of the plaintiff. Although variously described as a right, a remedy and a mechanism, tracing is generally accepted as being more in the nature of a process1 and is a precursor to the assertion of a personal or a proprietary claim either at common law or in equity.2 Described in general terms, it is a process for identifying value that the defendant has received, whether or not in the form of specific assets, and establishing a link between that value and the plaintiff. Essentially, tracing and restitution are directed to the same issue.3 Expressed at a level of generality sufficient to comprehend both doctrines, the issue is the position of a person at whose expense another person has been benefited in circumstances where, for one or other reason, it is unjust that the beneficiary should retain the benefit. Both doctrines are directed to vesting that benefit, in some form or other, in the person at whose expense it was obtained and are limited to that benefit or to its equivalent value.4 The value of the benefit (be it property or otherwise) may be greater or less than the loss suffered or the expense occasioned and thus they differ from compensatory remedies which are directed to restoring the person’s former position irrespective of whether any benefit was received by the party obliged to make compensation or the value of any such benefit.5 ∗ Judge, Federal Court of Australia. -

Trusts & Equity Fall Term 2018 Lecture Notes – No. 16 ARE THIRD

Trusts & Equity Fall Term 2018 Lecture Notes – No. 16 ARE THIRD PARTIES LIABLE TO SUFFER A REMEDY? In Barnes v Addy (1874) L.R. 9 Ch. APP. 244, Lord Selborne L.C. described two distinct equitable actions available against a third party (i.e. someone outside the trust) popularly known as ‘knowing receiPt’ (available against a third party possessed of trust property in his or her personal capacity; i.e. not as an agent) and ‘knowing assistance’ (against a third party who is an accessory to breach of trust of fiduciary duty). • In both the areas of ‘knowing receipt’ and ‘knowing assistance’, the courts and commentators are drawn between two positions: are these forms of liability ‘wrongs’ (based on some degree of fault) or restitutionary responses based on unjust enrichment (favouring strict liability, subject to a defence of ‘change of position’)? • The claim of a bona fide purchaser for fair value without notice of the trust supersedes claims by the trustee or beneficiary; Nelson v Larholt [1948] 1 KB 339; Macmillan Inc v Bishopsgate Investment Trust (No 3) [1995] 3 All ER 747. • The third party in receipt of trust property disposed of in breach of trust by the trustee must be distinguished from the liability of a third party as a ‘trustee de son tort’; that is, a third party who is a stranger to the trust and who intermeddles with trust property and does acts characteristic of a trustee and commits a breach of trust. The trustee de son tort is personally liable to account to B as well as to hold any trust property on a constructive trust; Mara v Brown [1896] 1 Ch 199; Williams-Ashman v Price & Williams [1942] Ch 219; Re Barney [1892] 2 Ch 265. -

And Turner V Jacob (2006)

Landmark Cases in Tracing A Sample Chapter Re Tilley’s Will Trusts (1967) and Turner v Jacob (2006) Derek Whayman, Newcastle University: [email protected] 1. Introduction Many landmark cases have, if not grand facts, rather grand parties to them. This is a consequence of many of them having been decided a century or more ago, where, in practice, the services the courts provided were to mainly the wealthy and often grand. A case in point is seen in the first chapter of this (proposed) collection concerning Kirk v Webb (1698),1 which features a cast of post-restoration senior clergy, aristocrats and of course Barbara Palmer, Countess of Castlemaine, perhaps the most notorious of Charles II’s mistresses, and their son. The parties in Re Tilley’s Will Trusts (1967)2 and Turner v Jacob (2006)3 are from a time where the middle class had sufficient wealth and opportunities to invest, and our interest in these cases arises because their protagonists did not structure their investments – at least legally – wisely. Moreover, in Turner v Jacob we see a remarkable and thoroughly modern woman in Dorothy Turner in the events leading up to the case, one whose acts and intentions, it seems, influenced a modern court of equity to apply the law very carefully in a manner sensitive to her position. That these decisions are controversial in recent times is another piece of evidence supporting the proposition that equity in general, and tracing in particular, are still searching for their fundamental principles even today. For this reason, we must also look to the rather less grand- looking cases and those lower down in the hierarchy of the courts. -

The Remarkable Power of Appointment Device: Planning and Drafting Considerations

Mortimer H. Hess Memorial Lecture New York City Bar Association May 22, 2012 The Remarkable Power of Appointment Device: Planning and Drafting Considerations By Professor Ira Mark Bloom Justice David Josiah Brewer Distinguished Professor of Law Albany Law School 80 New Scotland Avenue Albany, NY 12208-3494 [email protected] © 2012 by Ira Mark Bloom. All Rights Reserved. The Remarkable Power of Appointment Device: Planning and Drafting Considerations Ira Mark Bloom “The power of appointment is the most efficient dispositive device that the ingenuity of Anglo-American lawyers has ever worked out.”1 I. Introduction Consider how the power of appointment device can be used by contemporary estate planners to achieve important non-tax dispositive goals: flexibility, control and creditor protection. As an example, Client wants to create a testamentary trust for Client’s Child for life, and then to Client’s Grandchildren. Client does not like the rigidity of fixed remainders that would result if the remainder was simply left to his grandchildren. Rather he wants Child to decide up until his death how the trust principal will be enjoyed by Client’s Grandchildren. One solution is to give Child a special (nongeneral), exclusive (exclusionary) testamentary power of appointment pursuant to which Child will name in his will who among the Client’s Grandchildren will take and in what proportions. In this way, the trust remains flexible until the Child dies and gives the Child control over the principal without subjecting the principal to the Child’s creditors.2 In addition, the trust principal will not be subject to federal estate taxation on the Child’s death.