Achieving an Integrated Electricity Market in Southeast Asia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Suhakam's Report on the Murum Hydroelectric

SUHAKAM’S REPORT ON THE MURUM HYDROELECTRIC PROJECT AND ITS IMPACT TOWARDS THE ECONOMIC, SOCIAL AND CULTURAL RIGHTS OF THE AFFECTED INDIGENOUS PEOPLES IN SARAWAK LEVEL 29, MENARA TUN RAZAK, JALAN RAJA LAUT 50350 KUALA LUMPUR, MALAYSIA 603-2612 5600 (T) 603-2612 5620 (F) [email protected] (E) Book.indd 2 7/17/2009 11:26:35 AM Cetakan Pertama / First Printing, 2009 ©Hak Cipta Suruhanjaya Hak Asasi Manusia (SUHAKAM), 2009 ©Copyright Human Rights Commission of Malaysia (SUHAKAM) 2009 Diterbitkan di Malaysia oleh / Published in Malaysia by SURUHANJAYA HAK ASASI MANUSIA / HUMAN RIGHTS COMMISSION OF MALAYSIA E-mail: [email protected] URL: http://www.suhakam.org.my Dicetak di Malaysia oleh / Printed in Malaysia by LEGASI PRESS SDN. BHD. NO. 60 (GROUND FLOOR), JALAN METRO PERDANA TIMUR II, KEPONG ENTREPRENEUR PARK, 52100 KUALA LUMPUR. 603-6250 5190 (T) 603-6250 8190 (F) Hak cipta laporan ini adalah milik SUHAKAM. Laporan ini boleh disalin dengan syarat mendapat kebenaran daripada SUHAKAM. The copyright of this report belongs to SUHAKAM. This report may be reproduced with SUHAKAM’s permission. Perpustakaan Negara Malaysia Data-Pengkatalogan-dalam-Penerbitan National Library of Malaysia Cataloguing-in-Publication-Data SUHAKAM’S REPORT ON THE MURUM HYDROELECTRIC PROJECT AND ITS IMPACT TOWARDS THE ECONOMIC, SOCIAL AND CULTURAL RIGHTS OF THE AFFECTED INDIGENOUS PEOPLES IN SARAWAK Includes bibliographical references ISBN 978-983-2523-55-0 1. Murum Hydroelectric Project and Its Impact. 2. Indigenous People 3. Suruhanjaya Hak Asasi Manusia -

Kenyah-Badeng in Bakun Resettlement Malaysia

Development and displacement: Kenyah-Badeng in Bakun Resettlement Malaysia Inaugural-Dissertation zur Erlangung der Doktorwürde der Philosophischen Fakultät der Rheinischen Friedrich-Wilhelms-Universität zu Bonn vorgelegt von WELYNE JEFFREY JEHOM aus Sarawak, Malaysia Bonn 2008 Gedruckt mit Genehmigung der Philosophischen Fakultät der Rheinischen Friedrich-Wilhelms-Universität Bonn Zusammensetzung der Prüfungskommission: Prof. Dr. Stephan Conermann (Vorsitzender) Prof. Dr. Solvay Gerke (Betreuerin und Gutachterin) Prof. Dr. Hans-Dieter Evers (Gutachter) Prof. Dr. Werner Gephart (weiteres prüfungsberechtigtes Mitglied) Tag der mündlichen Prüfung: 26.06.2008 ZUSAMMENFASSUNG Im Zentrum dieser Forschungsarbeit steht die Umsiedlung der indigenen Einwohner vom Stamme der Kenyah-Badeng aus dem Dorf Long Geng in die neue Siedlung Sg. Asap in Sarawak, Malaysia. Grund für die Umsiedlung war der Bau eines Staudamms, des Bakun Hydro-electric Projektes (BHEP). Neben den Kenyah-Badeng, wurden weitere 16 Dörfer in der neuen Siedlung angesiedelt. Die Umsiedlung begann 1998 und bereits im darauffolgenden Jahr waren die neuen Langhäuser in Sg. Asap vollständig bewohnt. I. Hintergrund Umsiedlungen als Folge von Bauprojekten oder Infrastrukturmaßnahmen sind keine Seltenheit. In diesem Zusammenhang wird oft argumentiert, dass solche Projekte Arbeitsplätze für die lokale Bevölkerung schaffen und die Entwicklung fördern. Andererseits vertreibt ein solche Projekt die vor Ort lebenden Menschen von ihrer Heimstatt und ihrem traditionellen Lebensunterhalt. Im Kern der vorliegenden Studie steht der Aspekt der Zwangsumsiedlung: die Dorfbewohner von Long Geng siedelten sich ausschließlich wegen des Baus des Bakun Wasserkraftwerks in Sg. Asap an. Dies muss als Zwangsumsiedlung angesehen werden, da die indigenen Gemeinden, die früher in dem für das BHP vorgesehenen Gebiet lebten, keine andere Wahl hatten als wegzuziehen und sich anderswo wieder anzusiedeln, denn ihre Dörfer und ihr angestammtes Land wurden von der Staatsregierung für den Bau des BHP beansprucht. -

KEMENTERIAN TENAGA, TEKNOLOGI HIJAU DAN AIR Arkib

KEMENTERIAN TENAGA, TEKNOLOGI HIJAU DAN AIR ý, FEASIBILITY STUDY FOR GREENENERGY ISLAN FINAL REPOR -w `hor Azhaili Baharun - - Arkib Author Wan Azian Wan Zainal Abidin, Kismet A ak Hong Ping, TJ Affandi, Hazrul Mohamed Basri, Abg Mohd Nizarn 808 Ting Sim Nee F288 2013 Vol. 1 Pusat Khidmat Maklumat Akademik UNIVERSITI MALAYSIA SARAWAK P.KNIDMAT MAKLUMATAKADEMIK 1000247427 FEASIBILITY STUDY FOR GREEN ENERGY ISLAND FINAL REPORT VOL. 1 Pusat Khidmat Maklumat Akademik UNIVERSITI MALAYSIA SARAWAK TABLE OF CONTENTS Contents Page Table of Contents i Acknowledgements iv List of Tables V List of Figures V1 Executive Summary 1 1.0 Background 3 1.1 The Sarawak Energy Scenario 3 1.1.1 Map of Sarawak 4 1.1.2 Income Generation Activities in Sarawak 4 1.1.3 Average Income in Sarawak 6 1.1.4 Percentage Access to Energy Services of Sarawakians 6 1.1.5 Current Forms of Energy in Sarawak 6 1.2 World Energy Outlook 7 1.2.1 Trend towards Renewable Energy 7 1.3 Renewable Energy ResourcesAvailable in Sarawak 9 i 1.3.1 Jatropha (Biomass) 9 1.3.2 Solar 9 1.3.3 Wind 10 1.3.4 Hydropower 10 1.3.5 Geothermal power 10 2.0 Green Energy Island as Energy Intervention Solution 11 3.0 Site Selection Procedures 14 4.0 Selection Criteria 17 4.1 Sites Selected 20 5.0 Site study 22 5.1 Rh. Ambah, Bintulu 22 5.2 Rh. Edward Mamut, Kpg Langgir, Lingga, Sri Aman 32 5.3 Kpg. Assum, Borneo Heights, Padawan, Kuching 44 5.4 Rh. -

45076-001: an Evaluation of the Prospects for Interconnections

AN EVALUATION OF THE PROSPECTS FOR INTERCONNECTIONS AMONG THE BORNEO AND MINDANAO POWER SYSTEMS AN EVALUATION OF THE PROSPECTS FOR INTERCONNECTIONS AMONG THE BORNEO AND MINDANAO POWER SYSTEMS Final Report November 2014 The views expressed in this publication are those of the authors and do not necessarily reflect the views and policies of the Asian Development Bank (ADB) or its Board of Governors or the governments they represent. ADB does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. By making any designation of or reference to a particular territory or geographic area, or by using the term “country” in this document, ADB does not intend to make any judgments as to the legal or other status of any territory or area. ADB encourages printing or copying information exclusively for personal and noncommercial use with proper acknowledgment of ADB. Users are restricted from reselling, redistributing, or creating derivative words for commercial purposes without the express, written consent of ADB. Contents Abbreviation v Common Technical and Financial Acronyms used in this Report vii Currency viii Physical Measurement Units and their Application ix Acknowledgments x Report Summary and Recommendations xi 1 Overview and Study Objectives 1 2 Eastern ASEAN Grid Development Planning 2 2.1 Overview of ASEAN Region Power Development Plans 2 2.2 Energy Security within the ASEAN Power Market 4 2.3 Grouping of ASEAN and BIMP/EAGA sub-regional power systems 4 2.4 Eastern -

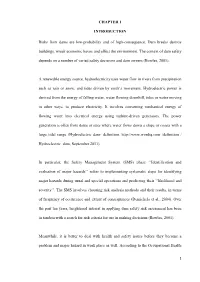

2017 Annual Report

Sustaining VALUE & Continuous growth A N N U A L R E P O R T 2 0 Our 2,400MW Bakun Hydroelectric Plant 1 7 The year 2017 will be remembered for the acquisition of Sarawak Hidro from the Ministry of Finance through a RM2.5 billion share sale agreement, enabling Sarawak Energy to assume control of Sarawak Hidro. As owner and operator of the 2,400MW Bakun Hydroelectric Plant (HEP), the largest hydropower plant in the country, Sarawak Energy can integrate operations of Bakun HEP into the Group, resulting in better reliability of power supply and efficiency in resource allocation. Sarawak Energy can also have greater flexibility to maximise and operate electricity supply in Sarawak and power sustainable growth and prosperity in the state. Sustaining VALUE & Continuous growth Sarawak Energy Excellence 2020 FUTURE PRESENT (2020 and beyond) PAST (2017 to 2019) (2010 to 2016) VALUE GROWTH & REGIONAL EXPANSION SUSTAINING VALUE & CONTINUOUS GROWTH • Strengthening equity of Sarawak SIGNIFICANT Energy Group for further growth GROWTH & VALUE CREATION • Sustainability of value for realisation • State’s growth and development in the next stage • Revenue increase – 3 times • Borneo Grid • Consolidate and protect value created • Generation capacity increase A over past years > 3,000MW • Continuing the growth agenda N • More than 2,500 manpower recruited N U A L R E P O R T 2 0 1 7 Sustaining Value & Continuous Growth As Sarawak Energy marches towards achieving its ambition of becoming a regional powerhouse, we aim to uphold the high standards and operational momentum that our internal and external partners and industry players throughout the region have come to expect. -

Baleh-Natural-Capital-Valuation-Final

Background 6 Introduction 6 Chapter 1. Ecological and hydrological context 8 1.1 Ecological context 8 1.1.1 Terrestrial fauna 8 1.1.2 Aquatic fauna 8 1.1.3 Terrestrial flora 8 1.2 Hydrological context 9 Chapter 2. Cultural and economic context 10 2.1 Population 10 2.2 Cultural and social context 12 2.3 Education 12 2.4 Health care 14 2.5 Economic activity 15 2.5.1 Water supply 15 2.5.2 Commercial navigation and port services 18 2.5.3 Shipbuilding 22 2.5.4 Aquaculture 22 2.5.5 Tourism 23 2.5.6 Coal mining and sand mining 24 2.6 Revenue of municipal and district councils 24 Chapter 3. Policy and institutional context 26 3.1 Sarawak Corridor of Renewable Energy 26 3.2 Protected Area 26 3.3 Master Plan for Wildlife in Sarawak 27 3.4 Forestry 27 3.5 Oil palm 28 3.6 Water 28 3.7 Heart of Borneo Initiative 29 Chapter 4. Key ecosystem services valued in the study 31 Chapter 5. Spatial modelling of ecosystem services 37 5.1 Methods and data 37 5.1.1 Land Use scenarios 37 5.1.2 Ecosystem services 46 5.2 Baseline provision of ecosystem services 50 5.3 Land use change scenarios and provision of ecosystem services 50 Chapter 6. Survey design and implementation 57 6.1 Survey and questionnaire development 57 6.2 Survey implementation 59 Chapter 7. Longhouse survey results 61 7.1 Sample description 61 7.2 Income and use of natural resources 61 7.3 Perception of environmental change 64 7.4 Social capital and migration 66 7.5 Tourism development 68 7.6 Preferences for environmental conservation 68 Chapter 8. -

Center for Southeast Asian Studies, Kyoto University Subscriptions

http://englishkyoto-seas.org/ Andrew Aeria Economic Development via Dam Building: The Role of the State Government in the Sarawak Corridor of Renewable Energy and the Impact on Environment and Local Communities Southeast Asian Studies, Vol. 5, No. 3, December 2016, pp. 373-412. (<Special Focus> “Global Powers and Local Resources in Southeast Asia: Political and Social Dynamics of Foreign Investment Ventures,” edited by Akiko Morishita) How to Cite: Aeria, Andrew. Economic Development via Dam Building: The Role of the State Government in the Sarawak Corridor of Renewable Energy and the Impact on Environment and Local Communities. In “Global Powers and Local Resources in Southeast Asia: Political and Social Dynamics of Foreign Investment Ventures,” edited by Akiko Morishita, special focus, Southeast Asian Studies, Vol. 5, No. 3, December 2016, pp. 373-412. Link to this article: https://englishkyoto-seas.org/2016/12/vol-5-no-3-andrew-aeria/ View the table of contents for this issue: https://englishkyoto-seas.org/2016/12/vol-5-no-3-of-southeast-asian-studies/ Center for Southeast Asian Studies, Kyoto University Subscriptions: http://englishkyoto-seas.org/mailing-list/ For permissions, please send an e-mail to: [email protected] u.ac.jp Center for Southeast Asian Studies, Kyoto University Economic Development via Dam Building: The Role of the State Government in the Sarawak Corridor of Renewable Energy and the Impact on Environment and Local Communities Andrew Aeria* Since 1970, as a consequence of Malaysia’s New Economic Policy (NEP) and its integration into the global economy, the development achievements and per capita GDP growth of the resource-rich state of Sarawak have been impressive—although not without problems. -

Downloaded It

Economic Development via Dam Building: The Role of the State Government in the Sarawak Corridor of Renewable Energy and the Impact on Environment and Local Communities Andrew Aeria* Since 1970, as a consequence of Malaysia’s New Economic Policy (NEP) and its integration into the global economy, the development achievements and per capita GDP growth of the resource-rich state of Sarawak have been impressive—although not without problems. Since timber and petroleum resources are exhaustible, and there is a concern with finding new sources of growth and revenue, the federal and state governments advocated industrial diversification in 2008 via the development of a multibillion-ringgit regional development corridor called the Sarawak Corridor of Renewable Energy (SCORE). Central to the success of the huge developmental corridor was cheap hydroelectric power (HEP). For the Sarawak government, SCORE’s launch and eventual success were based on the availability of abundant water resources and suitable hydropower dam sites in the state. Yet, SCORE is likely to contribute to further environmental degradation and impact negatively upon the livelihoods and welfare of local communities. This paper examines this recent development trend and its consequences. Specifically, it examines the role of the Sarawak state government in advocating the construction of numerous HEP dams, the role of foreign and local investment in SCORE, and their collective impact upon the environment and local communities. What this paper reveals is the nexus of close relationships that binds key politicians in the state administration with crony businesses associated with foreign-linked contracts that has proven to be destruc- tive socially and environmentally. -

Energy, Economic and Environmental Impact of Hydropower in Malaysia

International Journal of Advanced Scientific Research and Management, Vol. 2 Issue 4, Apr 2017. www.ijasrm.com ISSN 2455-6378 Energy, Economic and Environmental Impact of Hydropower in Malaysia M. Faizal1,2, L. J. Fong1, J. Chiam1 and A. Amirah3 1 ADP, SLAS, Taylor's University Lakeside Campus, 47500 Selangor, Malaysia 2 FIA, SLAS, Taylor's University Lakeside Campus, 47500 Selangor, Malaysia 3Department of Park and Ecotourism, Faculty of Forestry, Universiti Putra Malaysia, 43400 Serdang, Malaysia Abstract Fossil fuel has occupied 78.4% of the total Malaysia is rich with natural resources, a true gem worldwide energy consumption whereas 19% comes with plenty of water and receives high rain volume from renewables, which are broken down into per year which is used to generate power. Hence, the different renewables used (See Figure 1) [2]. The use use of hydropower becomes relevant in this country. of non-renewable resources has been inducing Hydropower is a renewable source of energy which negative impact to the environment such as acid rain, produces very little greenhouse gasses. Besides that, air pollution, global warming, ozone layer depletion, it is the least costly way of storing large amounts of and emission of radioactive substances [3]. Other electricity. Utilization of electrical energy is an than that, it contributes to an increase in the rate of important aspect to the economic growth for a diminishing fossil fuel resources and detrimental to country and improvement in people’s living public health [4]. standards, especially in developing countries. The growing demand for electrical energy, the To tackle the numerous adversities faced by non- environmental effects of fossil fuel usage as well as renewables, we should focus on a renewable energy fear of losing fossil fuels, are the main topics driving resource which is one of the cleanest source of us towards the direction of focusing on hydropower energy and curbs the following negative impacts as a source of renewable technology. -

Assessment of Heavy Metals in Water, Sediment, and Fishes of a Large Tropical Hydroelectric Dam in Sarawak, Malaysia

Hindawi Publishing Corporation Journal of Chemistry Volume 2016, Article ID 8923183, 10 pages http://dx.doi.org/10.1155/2016/8923183 Research Article Assessment of Heavy Metals in Water, Sediment, and Fishes of a Large Tropical Hydroelectric Dam in Sarawak, Malaysia Siong Fong Sim, Teck Yee Ling, Lee Nyanti, Norliza Gerunsin, Yiew Ee Wong, and Liang Ping Kho FacultyofResourceScience&Technology,UniversitiMalaysiaSarawak,94300KotaSamarahan,Sarawak,Malaysia Correspondence should be addressed to Siong Fong Sim; [email protected] Received 11 November 2015; Accepted 18 January 2016 Academic Editor: Yuangen Yang Copyright © 2016 Siong Fong Sim et al. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. Bakun Hydroelectric Dam in Sarawak is one of the world highest concrete rock filled dams. This paper reports the heavy metals concentrations in water, sediment, and fishes of Bakun Dam. Water and sediment samples were collected from 11 stations and 6 fish species were caught. The samples were digested with open acid digestion and the metals contents were analysed using an atomic absorption spectrophotometer and mercury analyser. The method was validated based on certified reference materials. A higher concentration of Fe and Mn was detected in downstream water with significant longitudinal variation. Cu, Zn, and Hg were present in trace amount. All elements analysed were consistently found in sediment with no risk of contamination. For fish, Hemibagrus planiceps was characterised by higher affinity for Hg accumulation. The concentrations detected in all fish species were withinthe permissible guideline of 0.5 mg/kg. -

1 CHAPTER 1 INTRODUCTION Risks from Dams Are Low-Probability And

CHAPTER 1 INTRODUCTION Risks from dams are low-probability and of high-consequence. Dam breaks destroy buildings, wreak economic havoc and affect the environment. The context of dam safety depends on a number of varied safety decisions and dam owners (Bowles, 2001). A renewable energy source, hydroelectricity uses water flow in rivers from precipitation such as rain or snow, and tides driven by earth’s movement. Hydroelectric power is derived from the energy of falling water, water flowing downhill, tides or water moving in other ways, to produce electricity. It involves converting mechanical energy of flowing water into electrical energy using turbine-driven generators. The power generation is often from dams or sites where water flows down a slope or coasts with a large tidal range (Hydroelectric dam- definition. http://www.wordiq.com /definition / Hydroelectric_dam, September 2011). In particular, the Safety Management System (SMS) phase ‘‘Identification and evaluation of major hazards’’ refers to implementing systematic steps for identifying major hazards during usual and special operations and predicting their ‘‘likelihood and severity’’. The SMS involves choosing risk analysis methods and their results, in terms of frequency of occurrence and extent of consequences (Demichela et al., 2004). Over the past ten years, heightened interest in applying dam safety risk assessment has been in tandem with a search for risk criteria for use in making decisions (Bowles, 2001). Meanwhile, it is better to deal with health and safety issues before they become a problem and major hazard in work place as well. According to the Occupational Health 1 and Safety Department of Malaysia, an OSH policy is a document in writing expressing an organization’s dedication to employee health, well being and safety. -

Energy Planning and Development in Malaysian Borneo: Assessing the Benefits of Distributed Technologies Versus Large Scale Energy Mega-Projects

Energy Planning and Development in Malaysian Borneo: Assessing the Benefits of Distributed Technologies versus Large Scale Energy Mega-projects Rebekah Shirley1*, Daniel Kammen1,2 1Energy and Resources Group, University of California, Berkeley, California, USA 2Goldman School of Public Policy, University of California, Berkeley, California, USA * Corresponding Author: [email protected] 310 Barrows Hall, Mail Code: #3050, University of California, Berkeley, CA 94720-3050 Phone: (510) 642 - 1640/ Fax: (510) 642 - 1085 Abstract Malaysian Borneo is the currently the subject of contentious state-led development plans that involve a series of mega-dams to stimulate industrial demand. There is little quantitative analysis of energy options or cost and benefit trade-offs in the literature or the public discussion. We use the commercial energy market software PLEXOS to prepare a long term capacity expansion model for the state of Sarawak which includes existing generation, resource constraints and operability constraints. We also incorporate the indirect costs of greenhouse gas emissions and direct forest loss. We devise and model different scenarios to observe the technically feasible options for electricity supply that satisfy future demand under four growth assumptions and then observe their economic and environmental trade-offs. Our central finding is that local resources including solar and biomass waste technologies can contribute to the generation mix at lower cost and environmental impact than the additional dam construction. Our case study of Borneo represents many energy related megaprojects being developed in emerging economies and our proposed method of assessment can support the current conversations on development of natural resources and potential sustainable solutions. Keywords: Renewable Energy, Economic Development, Development Tradeoffs, Borneo 1.