Ch 8- Defence Audit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

T He Indian Army Is Well Equipped with Modern

Annual Report 2007-08 Ministry of Defence Government of India CONTENTS 1 The Security Environment 1 2 Organisation and Functions of The Ministry of Defence 7 3 Indian Army 15 4 Indian Navy 27 5 Indian Air Force 37 6 Coast Guard 45 7 Defence Production 51 8 Defence Research and Development 75 9 Inter-Service Organisations 101 10 Recruitment and Training 115 11 Resettlement and Welfare of Ex-Servicemen 139 12 Cooperation Between the Armed Forces and Civil Authorities 153 13 National Cadet Corps 159 14 Defence Cooperaton with Foreign Countries 171 15 Ceremonial and Other Activities 181 16 Activities of Vigilance Units 193 17. Empowerment and Welfare of Women 199 Appendices I Matters Dealt with by the Departments of the Ministry of Defence 205 II Ministers, Chiefs of Staff and Secretaries who were in position from April 1, 2007 onwards 209 III Summary of latest Comptroller & Auditor General (C&AG) Report on the working of Ministry of Defence 210 1 THE SECURITY ENVIRONMENT Troops deployed along the Line of Control 1 s the world continues to shrink and get more and more A interdependent due to globalisation and advent of modern day technologies, peace and development remain the central agenda for India.i 1.1 India’s security environment the deteriorating situation in Pakistan and continued to be infl uenced by developments the continued unrest in Afghanistan and in our immediate neighbourhood where Sri Lanka. Stability and peace in West Asia rising instability remains a matter of deep and the Gulf, which host several million concern. Global attention is shifting to the sub-continent for a variety of reasons, people of Indian origin and which is the ranging from fast track economic growth, primary source of India’s energy supplies, growing population and markets, the is of continuing importance to India. -

Ordnance Factory Organisation

Report No. 44 of 2015 (Defence Services) CHAPTER-VII: ORDNANCE FACTORY ORGANISATION 7.1 Performance of Ordnance Factory Board 7.1.1 Introduction 7.1.1.1 Ordnance Factories are the oldest and largest organization in India’s defence industry with a history that dates back to 1787. There are 4158 Factories divided under five Table-27 clusters or operating groups Operating group Number of (Table-27) produce a range of factories arms, ammunitions, weapons, Ammunition & Explosives 10 armoured & infantry combat Weapons, vehicles and equipment 10 vehicles and clothing items Materials & Components 8 Armoured vehicles 6 including parachutes for the Ordnance equipment group 5 defence services. They function Total 39 under the Ordnance Factory Source : Annual Accounts of Ordnance Factories Board which is under the – 2013-14 administrative control of the Department of Defence Production of the Ministry of Defence of Government of India. The Board comprises a Chairman and eight members59. 7.1.1.2 The objectives of the Ordnance Factory Board60 are: x To supply quality arms, ammunition, tanks and equipment to armed forces; x To modernise production facilities to improve quality; x To absorb latest technology through Transfer of Technology61 and in- house Research & Development; x To meet customer satisfaction and expand consumer base. 7.1.1.3 In addition, the policy objectives of the Government on Defence Production and Procurement, list the following objectives which have a bearing on the Ordnance Factory Board: x To ensure expeditious procurement of the approved requirements of the armed forces, in terms of capabilities sought and timeframe prescribed by optimally utilizing the allocated budgetary resources; 58 2 OFs at Nalanda and Korwa are under construction. -

Report of Working Group on Defence Equipment

REPORT OF WORKING GROUP ON DEFENCE EQUIPMENT 1 INDEX 1. OVERVIEW 1.1 DEFENCE SPENDING 1.2 DPSUs AND OFB 1.3 PRIVATE SECTOR 1.4 FDI IN DEFENCE SECTOR 1.5 DEFENCE EXPORTS 1.6 LAND SYSTEMS 1.7 SHIPYARDS 1.8 ELECTRONICS SYSTEMS 2. OPPORTUNITIES 2.1 GROWTH POTENTIAL IN 12TH PLAN 2.2 LAND SYSTEMS 2.3 NAVAL SYSTEMS 2.4 ELECTRONICS SYSTEMS 3. CHALLENGES 3.1 RESTRICTED TECHNOLOGIES 3.2 HIGH R&D COST 3.3 LOW R&D EXPENDITURE 3.4 MONOPSONIC DEFENCE MARKET 3.5 SHIPYARD INFRASTRUCTURE AND FACILITIES 3.6 LOW VOLUMES OF HIGH TECHNOLOGY REQUIREMENTS 4. RECOMMENDATIONS 4.1 R&D ACTIVITY SUPPORT 4.2 DEFENCE ELECTRONICS 4.3 INDUSTRY – ACADEMIA CO-OPERATION 4.4 STRENGTHENING OF CERTIFICATION ORGANIZATIONS 4.5 PPP MODEL 4.6 VENDOR DEVELOPMENT 4.7 SECTOR SKILL COUNCIL 2 1. OVERVIEW 1.1 DEFENCE SPENDING India’s defence spending in the 11th Plan period (2007-12) has grown at a CAGR of 13%. (Source: Annual Defence Services Estimates Reports) Defence Equipment Production in India is primarily aimed at meeting internal demand. India's total defence spending in the 11th Plan Period (2007-12) has grown at a CAGR of 13% (Table I). Growth in procurement of defence equipment (both capital and revenue) in 2010-11 was about 13% over 2009-10 and 20% in 2009-10 over 2008-09. Imports in defence equipment procurement have averaged 30% of total procurement in last 3 years. Table - I (Values in Rs./ Crores ) Head 2007-08 2008-09 2009-10 2010-2011 2011-12 (Actual) (Actual) (Actual) (Revised Es- (Budget Es- timates) timates) Revenue Expen- 54218.61 73304.80 90668.72 90748.43 95216.68 diture# Capital Expendi- 37461.67 40918.48 51112.36 60833.26 69198.81 ture Revenue & Capi- 91680.28 114223.28 141781.08 151581.69 164415.49 tal Expenditure #- The revenue expenditure figures include pay & allowances, transportation, revenue civil works in addition to the revenue purchase of Stores & Equipment. -

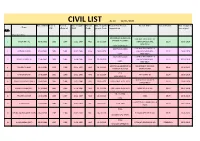

CIVIL LIST As on 12/01/2021

CIVIL LIST As on 12/01/2021 Date of Birth Year of Year of Date of apptt to Present Date of apptt to Present Post/ Present Present Office Present Station Date of apptt to Name CSE allotment IDAS Grade present Grade Organization present post Sl.No. (Kum/Smt/Shri) CONTROLLER GENERAL OF CONTROLLER GENERAL OF 1 SANJIV MITTAL 02-06-1962 1983 1984 21-12-1984 APEX 01-05-2019 DEFENCE ACCOUNTS DEFENCE ACCOUNTS, DELHI 01-05-2019 NEW DELHI CGDA , NEW DELHI ADDITIONAL CGDA CONTROLLER GENERAL OF 2 RAJNISH KUMAR 01-07-1962 1983 1984 01-01-1985 HAG+ 19-07-2019 DEFENCE ACCOUNTS, DELHI 19-07-2019 CGDA NEW DELHI ADDITIONAL CGDA CONTROLLER GENERAL OF 3 ALOK CHATURVEDI 11-06-1961 1984 1985 26-08-1985 HAG+ 01-10-2020 DEFENCE ACCOUNTS, DELHI 01-10-2020 CGDA NEW DELHI ADDITIONAL SECRETARY & DEPARTMENT OF RURAL 4 SANJEEV KUMAR 16-01-1961 1985 1986 02-01-1987 HAG 06-11-2013 DELHI 09-04-2019 FINANCIAL ADVISOR DEVELOPMENT PIFA 5 AVINASH DIKSHIT 10-06-1964 1985 1986 29-12-1986 HAG 23-01-2014 PIFA (ARMY-O) DELHI 28-08-2019 PIFA (ARMY-O) MINISTRY OF LABOUR & 6 ANURADHA PRASAD (SMT) 23-01-1964 1985 1986 22-12-1986 HAG 01-07-2014 ADDITIONAL SECRETARY DELHI 11-07-2018 EMPLOYMENT 7 RASIKA CHAUBE (SMT) 31-10-1963 1985 1986 25-08-1986 HAG 23-01-2014 ADDITIONAL SECRETARY MINISTRY OF STEEL DELHI 09-07-2018 SR. JT. CGDA 8 PRAVEEN KUMAR 12-04-1963 1986 1987 28-12-1987 HAG 14-09-2016 CGDA DELHI 28-08-2019 CGDA COMPETITION COMMISSION OF 9 SG DASTIDAR 13-07-1965 1986 1987 18-12-1987 HAG 29-05-2017 SECRETARY DELHI 09-12-2020 INDIA PCDA 10 DEVIKA RAGHUVANSHI (SMT) 06-02-1965 1987 -

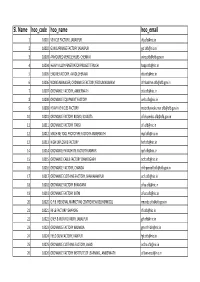

Sl. Name Hoo Code Hoo Name Hoo Email

Sl. Name hoo_code hoo_name hoo_email 1 10001 VEHICLE FACTORY, JABALPUR [email protected] 2 10002 GUN CARRIAGE FACTORY JABALPUR [email protected] 3 10003 ARMOURED VEHICLE HQRS. CHENNAI [email protected] 4 10004 HEAVY ALLOY PENETRATOR PROJECT TIRUCHI [email protected] 5 10005 ENGINE FACTORY, AVADI,CHENNAI [email protected] 6 10006 WORKS MANAGER, ORDNANCE FACTORY,YEDDUMAILARAM [email protected] 7 10007 ORDNANCE FACTORY, AMBERNATH [email protected] 8 10008 ORDNANCE EQUIPMENT FACTORY [email protected] 9 10009 HEAVY VEHICLES FACTORY [email protected] 10 10010 ORDNANCE FACTORY BOARD, KOLKATA [email protected] 11 10011 ORDNANCE FACTORY ITARSI [email protected] 12 10012 MACHINE TOOL PROTOTYPE FACTORY AMBERNATH [email protected] 13 10013 HIGH EXPLOSIVE FACTORY [email protected] 14 10014 ORDNANCE PARACHUTE FACTORY KANPUR [email protected] 15 10015 ORDNANCE CABLE FACTORY CHANDIGARH [email protected] 16 10016 ORDNANCE FACTORY, CHANDA [email protected] 17 10017 ORDNANCE CLOTHING FACTORY, SHAHJAHANPUR [email protected] 18 10018 ORDNANCE FACTORY BHANDARA [email protected] 19 10019 ORDNANCE FACTORY KATNI [email protected] 20 10020 O.F.B. REGIONAL MARKETING CENTRE NEW DELHI(RMCDL) [email protected] 21 10021 RIFLE FACTORY ISHAPORE [email protected] 22 10022 GREY & IRON FOUNDRY, JABALPUR [email protected] 23 10023 ORDNANCE FACTORY NALANDA gm‐ofn‐[email protected] 24 10024 FIELD GUN FACTORY, KANPUR [email protected] 25 10025 ORDNANCE CLOTHING FACTORY, AVADI [email protected] 26 10026 ORDNANCE FACTORY INSTITUTE OF LEARNING , AMBERNATH ofilam‐[email protected] 27 10027 OFB, -

Indian Army 19 4

Ministry of Defence Annual Report 2014-15 ANNUAL REPORT 2014-2015 Ministry of Defence Government of India Helicopter based small team operation C-130J, Hercules Aircraft of IAF in a fl ying formation C-130J, Hercules Aircraft of IAF in a fl Armour Fire Power LCA Tejas taking off at an Air Base Front Cover : Long Range Cruise Missile “Nirbhay” being launched (Clockwise) KASHIN Class Destroyer “INS RAJPUT” Back Cover : A Mig 29K aircraft approaching for Guns in action in High Altitude Area landing on board INS Vikramaditya Annual Report 2014-15 Ministry of Defence Government of India Contents 1. Security Environment 1 2. Organisation and Functions of the Ministry of Defence 11 3. Indian Army 19 4. Indian Navy 31 5. Indian Air Force 39 6. Indian Coast Guard 45 7. Defence Production 53 8. Defence Research and Development 71 9. Inter Service Organisations 93 10. Recruitment and Training 111 11. Resettlement and Welfare of Ex-Servicemen 133 12. Cooperation between the Armed Forces and Civil Authorities 143 13. National Cadet Corps 151 14. Defence Cooperation with Foreign Countries 159 15. Ceremonial and Other Activities 167 16. Activities of Vigilance Units 179 17. Empowerment and Welfare of Women 187 Appendices I Matters dealt with by the Departments of the Ministry of Defence 194 II Ministers, Chiefs of Staff and Secretaries who were in 198 Position from January 1, 2014 onwards III Summary of latest Comptroller & Auditor General (C&AG) 200 Report on the working of Ministry of Defence IV Position of Action Taken Notes (ATNs) as 213 on 31.12.2014 in respect of observations made in the C&AG Reports/PAC Reports V Results Framework Document (RFD) of Department of 214 Defence Production for the year 2013-2014 3 1 Security Environment 1 ndia’s defence strategy and policies aim at providing a Ipeaceful environment by addressing the wide spectrum of conventional and non-conventional security challenges faced by the country. -

India: Annual Report 2011-2012

ANNUAL REPORT 2011-2012 Ministry of Defence Government of India Joint Army-Air Force Exercise ‘Vijayee Bhava’ Army-Air Force Exercise ‘Vijayee Joint Front Cover :- Contingent of the Para-Regiment at the Republic Day Parade-2012 (Clockwise) AGNI-IV Test IAF’s Mi-17 V5 Helicopter Coast Guard Interceptor Boat ICGS C-153 Annual Report 2011-12 Ministry of Defence Government of India CONTENTS 1. Security Environment 1 2. Organisation and Functions of the Ministry of Defence 9 3. Indian Army 17 4. Indian Navy 33 5. Indian Air Force 43 6. Coast Guard 49 7. Defence Production 57 8. Defence Research and Development 93 9. Inter Service Organizations 113 10. Recruitment and Training 131 11. Resettlement and Welfare of Ex-Servicemen 153 12. Cooperation between the Armed Forces and Civil Authorities 167 13. National Cadet Corps 177 14. Defence Relations with Foreign Countries 189 15. Ceremonial, Academic and Adventure Activities 199 16. Activities of Vigilance Units 213 17. Empowerment and Welfare of Women 219 Appendices I Matters dealt with by the Departments of the Ministry of Defence 227 II Ministers, Chiefs of Staff and Secretaries who were in 231 position from January 1, 2011 onwards III Summary of latest Comptroller & Auditor General 232 (C&AG) Report on the working of Ministry of Defence IV Position of Action Taken Notes (ATNs) as on 31.12.2011 in respect 245 of observations made in the C&AG Reports/PAC Reports 3 4 1 SECURITY ENVIRONMENT IAF SU-30s dominating the air space 1 The emergence of ideology linked terrorism, the spread of small arms and light weapons(SALW), the proliferation of WMD (Weapons of Mass Destruction) and globalisation of its economy are some of the factors which link India’s security directly with the extended neighbourhood 1.1 India has land frontiers extending Ocean and the Bay of Bengal. -

Ordnance Factories, Def Organisation, Directora Ce Factories, Defence Research and Develo Ation, Directorate General of Quality

22 STANDING COMMITTEE ON DEFENCE (2020-21) (SEVENTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2021-22) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NOS. 19 AND 20) TWENTY SECOND REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2021 / Phalguna , 1942 (Saka) i TWENTY SECOND REPORT STANDING COMMITTEE ON DEFENCE (2020-21) (SEVENTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2021-22) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NO. 20) Presented to Lok Sabha on 16.03.2021 Laid in Rajya Sabha on 16.03.2021 LOK SABHA SECRETARIAT NEW DELHI March, 2021 / Phalguna , 1942 (Saka) ii CONTENTS PAGE COMPOSITION OF THE COMMITTEE (2020-21)………………………………….(iv) INTRODUCTION ……………………………………………………………………….(vi) REPORT PART I Chapter I Ordnance Factories Board .......................................................... 1 Chapter II Defence Research and Development Organisation.................. 18 Chapter III Directorate General of Quality Assurance................................. 28 Chapter IV National Cadet Corps............................................................... 36 PART II Observations/Recommendations....................................................................... 42 ANNEXURES Minutes of the Sittings of the Standing Committee on Defence (2020-21) held on 17.02.2021, 18.02.2021, 19.02.2021, 9.03.2021 and 15.3.2021………… 66 iii COMPOSITION OF THE STANDING COMMITTEE ON DEFENCE (2020-21) SHRI JUAL ORAM - CHAIRPERSON Lok Sabha 2. Shri Deepak (Dev) Adhikari 3. Kunwar Danish Ali 4. Shri Ajay Bhatt 5. Shri Devusinh Jesingbhai Chauhan 6. Shri Nitesh Ganga Deb 7. Shri Rahul Gandhi 8. Shri Annasaheb Shankar Jolle 9. Choudhary Mehboob Ali Kaiser 10. Prof. (Dr.) Ram Shankar Katheria 11. Smt. (Dr.) Rajashree Mallick 12. -

The Indian Defence Industry Redefining Frontiers

MUMBAI SILICON VALLEY BANGALOR E SINGAPORE MUMBAI BKC NEW DELHI MUNICH N E W Y ORK The Indian Defence Industry Redefining Frontiers January 2018 © Copyright 2018 Nishith Desai Associates www.nishithdesai.com The Indian Defence Industry Redefining Frontiers January 2018 MUMBAI SILICON VALLEY BANGALORE SINGAPORE MUMBAI BKC NEW DELHI MUNICH NEW YORK [email protected] The Indian Defence Industry Redefining Frontiers Contents 1. HISTORY 01 2. INDUSTRY OVERVIEW 03 I. India’s Defence Industrial Base 03 II. International involvement in India 04 III. Defence Procurement Procedure 2016 04 IV. Licensing Policy 05 V. Foreign Direct Investment 05 VI. Level Playing Field 06 VII. Transfer of Technology 06 VIII. Exports 06 IX. Private Sector 06 X. Concerns 07 3. INDUSTRY BREAKTHROUGHS 08 4. LEGAL AND REGULATORY FRAMEWORK 10 I. Ministry of Defence (MOD) 10 II. Industries (Development And Regulation) Act, 1951 (IDR ACT) 11 III. Defence Procurement Procedure, 2016 13 IV. Regulatory Agencies 21 5. FOREIGN DIRECT INVESTMENT 23 6. PUBLIC SECTOR 28 I. Ordnance Factories 28 II. Defence Public Sector Undertakings (DPSUs) 28 III. The Defence Research and Development Organization (DRDO) 30 7. PRIVATE SECTOR 31 I. Few Private Sector Breakthroughs 31 II. Scope of the Private Sector 36 III. The way forward 36 8. OFFSETS 39 I. Discharge of an offset obligation 40 II. Important Aspects of Offset Contracts 41 III. Penalties and Clarifications 42 IV. Efficacy of offsets 42 © Nishith Desai Associates 2018 The Indian Defence Industry Redefining Frontiers 9. EXPORTS 44 I. International Regulatory Framework 44 II. Domestic Regulatory Framework 44 III. Strategy for Defence Exports: 46 IV. -

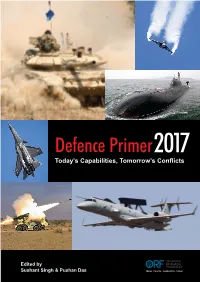

Defence Primer 2017

Defence Primer2017 Today’s Capabilities, Tomorrow’s Conflicts Edited by Sushant Singh & Pushan Das © 2017 BY OBSERVER RESEARCH FOUNDATION ISBN: 978-81-86818-24-4 Copy Editor: Udita Chaturvedi Cover Photographs: Angad Singh Designed by: Simijaisondesigns Printed by: Vinset Advertising Contents Today’s Capabilities, Tomorrow’s Conflicts ............................................................................................. 2 Pushan Das and Sushant Singh Filling the Capability Deficit .................................................................................................................. 6 Avinash Paliwal Future Challenges for the Army 2030 .................................................................................................... 15 Vipin Narang and Shashank Joshi Modernising of the Indian Army: Future Challenges .............................................................................. 26 Lt. Gen. (Retd.) Philip Campose India’s Air Force at a Pivotal Crossroads: Challenges and Choices Looking to 2032 ............................... 35 Benjamin S. Lambeth Future Challenges for the Indian Air Force: Innovations & Capability Enhancements ........................... 45 Justin Bronk Doctrinal and Technological Innovations in the Indian Armed Forces: Countering Future Terrorism and Asymmetric Threats ........................................................................................................ 52 C. Christine Fair Preparing for the Future Indian Ocean Security Environment: Challenges and Opportunities for -

Ordnance Factories, Defence Research and Development Organisation, Directorate General of Quality Assurance and National Cadet Corps

8 STANDING COMMITTEE ON DEFENCE (2019-20) (SEVENTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2020-21) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NOS. 19 AND 20) EIGHTH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2020/Phalguna, 1941 (Saka) 1 EIGHTH REPORT STANDING COMMITTEE ON DEFENCE (2019-20) (SEVENTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2020-21) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NOS. 19 AND 20) Presented to Lok Sabha on 13.03.2020 Laid in Rajya Sabha on 13.03.2020 LOK SABHA SECRETARIAT NEW DELHI March, 2020/Phalguna, 1941 (Saka) 2 CONTENTS PAGE COMPOSITION OF THE COMMITTEE (2019-20)………………………………….(iii) INTRODUCTION ……………………………………………………………………….(v) REPORT PART I Chapter I Ordnance Factories ..................................................................10 Chapter II Defence Research and Development Organisation.................30 Chapter III Directorate General of Quality Assurance.................................49 Chapter IV National Cadet Corps................................................................54 PART II Observations/Recommendations.......................................................................59 APPENDICES Minutes of the Sittings of the Standing Committee on Defence (2019-20) held on 17.02.2020, 18.02.2020, 19.02.2020, 20.02.2020, 21.02.2020 and 12.03.2020……………..76 3 COMPOSITION OF THE STANDING COMMITTEE ON DEFENCE (2019-20) Shri Jual Oram - Chairperson Lok Sabha 2. Shri Deepak Adhikari (Dev) 3. Shri Hanuman Beniwal 4. Shri Ajay Bhatt 5. Shri Devusinh J. Chauhan 6. Shri Nitesh Ganga Deb 7. Shri Rahul Gandhi 8. Shri Annasaheb Shankar Jolle 9. Prof (Dr.) Ram Shankar Katheria 10. Smt. (Dr.) Rajashree Mallick 11. -

Ordnance Factories, Defence Research and Development Organisation, Directorate General of Quality Assurance and National Cadet Corps

30 STANDING COMMITTEE ON DEFENCE (2016-2017) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2017-18) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NO. 20) THIRTIETH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2017 / Phalguna, 1938 (Saka) THIRTIETH REPORT STANDING COMMITTEE ON DEFENCE (2016-2017) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2017-18) ORDNANCE FACTORIES, DEFENCE RESEARCH AND DEVELOPMENT ORGANISATION, DIRECTORATE GENERAL OF QUALITY ASSURANCE AND NATIONAL CADET CORPS (DEMAND NO. 20) Presented to Lok Sabha on 09 .03.2017 Laid in Rajya Sabha on .03.2017 LOK SABHA SECRETARIAT NEW DELHI March, 2017 / Phalguna, 1938 (Saka) CONTENTS PAGE COMPOSITION OF THE COMMITTEE (2016-17)………………………………….(iii) INTRODUCTION ……………………………………………………………………….(v) REPORT PART I Chapter I Ordnance Factories Board .......................................................... Chapter II Defence Research and Development Organisation.................. Chapter III Directorate General of Quality Assurance................................. Chapter IV National Cadet Corps................................................................ PART II Observations/Recommendations....................................................................... APPENDICES Minutes of the Sitting of the Standing Committee on Defence (2016-17) held on 22.02.2017, 23.02.2017 and 03.03.2017………………………………………… COMPOSITION OF THE STANDING COMMITTEE ON DEFENCE ( 2016-17 ) Maj Gen B C Khanduri, AVSM (Retd) - Chairperson Lok Sabha 2. Shri Dipak Adhikari (Dev) 3. Shri Suresh C Angadi 4. Shri Shrirang Appa Barne 5. Shri Thupstan Chhewang 6. Col Sonaram Choudhary(Retd) 7. Shri H D Devegowda 8. Shri Sher Singh Ghubaya 9.* Shri B. Senguttuvan 10. Dr Murli Manohar Joshi 11. Km Shobha Karandlaje 12. Shri Vinod Khanna 13. Dr Mriganka Mahato 14. Shri Rodmal Nagar 15. Shri A P Jithender Reddy 16.