The Indian Defence Industry Redefining Frontiers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Clean Slate Airbus Pivots to Hydrogen For

November 2020 HOW NOT TO DEVELOP DEVELOP TO NOT HOW FIGHTERYOUR OWN SPACE THREATS SPACE AIR GETSCARGO LIFT A A CLEAN SLATE AIRBUS HYDROGEN TO PIVOTS FOR ZERO-CARBON ‘MOONSHOT’ www.aerosociety.com AEROSPACE November 2020 Volume 47 Number 11 Royal Aeronautical Society 11–15 & 19–21 JANUARY 2021 | ONLINE REIMAGINED The 2021 AIAA SciTech Forum, the world’s largest event for aerospace research and development, will be a comprehensive virtual experience spread over eight days. More than 2,500 papers will be presented across 50 technical areas including fluid dynamics; applied aerodynamics; guidance, navigation, and control; and structural dynamics. The high-level sessions will explore how the diversification of teams, industry sectors, technologies, design cycles, and perspectives can all be leveraged toward innovation. Hear from high-profile industry leaders including: Eileen Drake, CEO, Aerojet Rocketdyne Richard French, Director, Business Development and Strategy, Space Systems, Rocket Lab Jaiwon Shin, Executive Vice President, Urban Air Mobility Division, Hyundai Steven Walker, Vice President and CTO, Lockheed Martin Corporation Join fellow innovators in a shared mission of collaboration and discovery. SPONSORS: As of October 2020 REGISTER NOW aiaa.org/2021SciTech SciTech_Nov_AEROSPACE PRESS.indd 1 16/10/2020 14:03 Volume 47 Number 11 November 2020 EDITORIAL Contents Drone wars are here Regulars 4 Radome 12 Transmission What happens when ‘precision effects’ from the air are available to everyone? The latest aviation and Your letters, emails, tweets aeronautical intelligence, and social media feedback. Nagorno-Karabakh is now the latest conflict where a new way of remote analysis and comment. war is evolving with cheap persistent UAVs, micro-munitions and loitering 58 The Last Word anti-radar drones, striking tanks, vehicles, artillery pieces and even SAM 11 Pushing the Envelope Keith Hayward considers sites with lethal precision. -

T He Indian Army Is Well Equipped with Modern

Annual Report 2007-08 Ministry of Defence Government of India CONTENTS 1 The Security Environment 1 2 Organisation and Functions of The Ministry of Defence 7 3 Indian Army 15 4 Indian Navy 27 5 Indian Air Force 37 6 Coast Guard 45 7 Defence Production 51 8 Defence Research and Development 75 9 Inter-Service Organisations 101 10 Recruitment and Training 115 11 Resettlement and Welfare of Ex-Servicemen 139 12 Cooperation Between the Armed Forces and Civil Authorities 153 13 National Cadet Corps 159 14 Defence Cooperaton with Foreign Countries 171 15 Ceremonial and Other Activities 181 16 Activities of Vigilance Units 193 17. Empowerment and Welfare of Women 199 Appendices I Matters Dealt with by the Departments of the Ministry of Defence 205 II Ministers, Chiefs of Staff and Secretaries who were in position from April 1, 2007 onwards 209 III Summary of latest Comptroller & Auditor General (C&AG) Report on the working of Ministry of Defence 210 1 THE SECURITY ENVIRONMENT Troops deployed along the Line of Control 1 s the world continues to shrink and get more and more A interdependent due to globalisation and advent of modern day technologies, peace and development remain the central agenda for India.i 1.1 India’s security environment the deteriorating situation in Pakistan and continued to be infl uenced by developments the continued unrest in Afghanistan and in our immediate neighbourhood where Sri Lanka. Stability and peace in West Asia rising instability remains a matter of deep and the Gulf, which host several million concern. Global attention is shifting to the sub-continent for a variety of reasons, people of Indian origin and which is the ranging from fast track economic growth, primary source of India’s energy supplies, growing population and markets, the is of continuing importance to India. -

Chess Openings

Chess Openings PDF generated using the open source mwlib toolkit. See http://code.pediapress.com/ for more information. PDF generated at: Tue, 10 Jun 2014 09:50:30 UTC Contents Articles Overview 1 Chess opening 1 e4 Openings 25 King's Pawn Game 25 Open Game 29 Semi-Open Game 32 e4 Openings – King's Knight Openings 36 King's Knight Opening 36 Ruy Lopez 38 Ruy Lopez, Exchange Variation 57 Italian Game 60 Hungarian Defense 63 Two Knights Defense 65 Fried Liver Attack 71 Giuoco Piano 73 Evans Gambit 78 Italian Gambit 82 Irish Gambit 83 Jerome Gambit 85 Blackburne Shilling Gambit 88 Scotch Game 90 Ponziani Opening 96 Inverted Hungarian Opening 102 Konstantinopolsky Opening 104 Three Knights Opening 105 Four Knights Game 107 Halloween Gambit 111 Philidor Defence 115 Elephant Gambit 119 Damiano Defence 122 Greco Defence 125 Gunderam Defense 127 Latvian Gambit 129 Rousseau Gambit 133 Petrov's Defence 136 e4 Openings – Sicilian Defence 140 Sicilian Defence 140 Sicilian Defence, Alapin Variation 159 Sicilian Defence, Dragon Variation 163 Sicilian Defence, Accelerated Dragon 169 Sicilian, Dragon, Yugoslav attack, 9.Bc4 172 Sicilian Defence, Najdorf Variation 175 Sicilian Defence, Scheveningen Variation 181 Chekhover Sicilian 185 Wing Gambit 187 Smith-Morra Gambit 189 e4 Openings – Other variations 192 Bishop's Opening 192 Portuguese Opening 198 King's Gambit 200 Fischer Defense 206 Falkbeer Countergambit 208 Rice Gambit 210 Center Game 212 Danish Gambit 214 Lopez Opening 218 Napoleon Opening 219 Parham Attack 221 Vienna Game 224 Frankenstein-Dracula Variation 228 Alapin's Opening 231 French Defence 232 Caro-Kann Defence 245 Pirc Defence 256 Pirc Defence, Austrian Attack 261 Balogh Defense 263 Scandinavian Defense 265 Nimzowitsch Defence 269 Alekhine's Defence 271 Modern Defense 279 Monkey's Bum 282 Owen's Defence 285 St. -

Ordnance Factory Organisation

Report No. 44 of 2015 (Defence Services) CHAPTER-VII: ORDNANCE FACTORY ORGANISATION 7.1 Performance of Ordnance Factory Board 7.1.1 Introduction 7.1.1.1 Ordnance Factories are the oldest and largest organization in India’s defence industry with a history that dates back to 1787. There are 4158 Factories divided under five Table-27 clusters or operating groups Operating group Number of (Table-27) produce a range of factories arms, ammunitions, weapons, Ammunition & Explosives 10 armoured & infantry combat Weapons, vehicles and equipment 10 vehicles and clothing items Materials & Components 8 Armoured vehicles 6 including parachutes for the Ordnance equipment group 5 defence services. They function Total 39 under the Ordnance Factory Source : Annual Accounts of Ordnance Factories Board which is under the – 2013-14 administrative control of the Department of Defence Production of the Ministry of Defence of Government of India. The Board comprises a Chairman and eight members59. 7.1.1.2 The objectives of the Ordnance Factory Board60 are: x To supply quality arms, ammunition, tanks and equipment to armed forces; x To modernise production facilities to improve quality; x To absorb latest technology through Transfer of Technology61 and in- house Research & Development; x To meet customer satisfaction and expand consumer base. 7.1.1.3 In addition, the policy objectives of the Government on Defence Production and Procurement, list the following objectives which have a bearing on the Ordnance Factory Board: x To ensure expeditious procurement of the approved requirements of the armed forces, in terms of capabilities sought and timeframe prescribed by optimally utilizing the allocated budgetary resources; 58 2 OFs at Nalanda and Korwa are under construction. -

Creating a Competitive Environment for Defense Aerospace in a Protectionist Multipolar World: a Study of India and Israel

Beyond: Undergraduate Research Journal Volume 4 Article 1 Creating a Competitive Environment for Defense Aerospace in a Protectionist Multipolar World: A Study of India and Israel Shlok Misra Embry-Riddle Aeronautical University, [email protected] Tanish Jain University of California San Diego, [email protected] Follow this and additional works at: https://commons.erau.edu/beyond Part of the Technology and Innovation Commons Recommended Citation Misra, Shlok and Jain, Tanish () "Creating a Competitive Environment for Defense Aerospace in a Protectionist Multipolar World: A Study of India and Israel," Beyond: Undergraduate Research Journal: Vol. 4 , Article 1. Available at: https://commons.erau.edu/beyond/vol4/iss1/1 This Article is brought to you for free and open access by the Journals at Scholarly Commons. It has been accepted for inclusion in Beyond: Undergraduate Research Journal by an authorized administrator of Scholarly Commons. For more information, please contact [email protected]. Creating a Competitive Environment for Defense Aerospace in a Protectionist Multipolar World: A Study of India and Israel Cover Page Footnote Shlok Misra is an undergraduate at Embry-Riddle Aeronautical University, Daytona Beach. He is currently pursuing a Bachelor of Science in Aeronautical Science, with a minor in Airline Operations and Business Administration. Shlok is passionate about using technology for enhancing airspace efficiency and safety. Shlok’s research also focuses on studying human factors to enhance aviation safety. Shlok is currently a Commercial Pilot with an instrument rating. Tanish Jain is an undergraduate at the University of California, San Diego. He is currently pursuing a Bachelor of Science in Electrical Engineering, with a focus on Machine Learning and Controls. -

The Old Indian Move by Move

Junior Tay The Old Indian move by move www.everymanchess.com About the Author is a FIDE Candidate Master and an ICCF Senior International Master. He is a for- Junior Tay mer National Rapid Chess Champion and represented Singapore in the 1995 Asian Team Championship. A frequent opening surveys contributor to New in Chess Yearbook, he lives in Balestier, Singapore with his wife, WFM Yip Fong Ling, and their dog, Scottie. He used the Old Indian Defence exclusively against 1 d4 in the 2014 SportsAccord World Mind Games Online event, which he finished in third place out of more than 3000 participants. Also by the Author: The Benko Gambit: Move by Move Ivanchuk: Move by Move Contents About the author 3 Series Foreword 5 Bibliography 6 Introduction 7 1 The Classical Tension Tussle 17 2 Sämisch-Style Set-Ups and Early d4-d5 Systems 139 3 Various Ideas in the Fianchetto System 274 4 Marshalling an Attack with 4 Íg5 and 5 e3 395 5 Navigating the Old Indian Trail: 20 Questions 456 Solutions 467 Index of Variations 490 Index of Games 495 Foreword Move by Move is a series of opening books which uses a question-and-answer format. One of our main aims of the series is to replicate – as much as possible – lessons between chess teachers and students. All the way through, readers will be challenged to answer searching questions and to complete exercises, to test their skills in chess openings and indeed in other key aspects of the game. It’s our firm belief that practising your skills like this is an excellent way to study chess openings, and to study chess in general. -

The King's Indian Attack

Neil McDonald The King’s Indian attack move by move www.everymanchess.com About the Author English Grandmaster Neil McDonald has firmly established himself as one of the world's leading chess writers, with many outstanding works to his name. He is also a respected chess coach, who has trained many of the UK's strongest junior players. Also by the author: Break the Rules! Chess Secrets: The Giants of Power Play Chess Secrets: The Giants of Strategy Concise Chess Endings Concise Chess Middlegames Concise Chess Openings Dutch Leningrad French Winawer How to Play against 1 e4 Main Line Caro Kann Modern Defence Play the Dutch Positional Sacrifices Practical Endgame Play Rudolf Spielmann: Master of Invention Starting Out: 1 e4 Starting Out: Queen's Gambit Declined Starting Out: The Dutch Defence Starting Out: The English Starting Out: The Réti The Ruy Lopez: Move by Move Contents About the Author 3 Introduction 5 1 KIA versus the French 7 2 KIA versus the Sicilian 70 3 KIA versus the Caro-Kann 118 4 KIA versus the Reversed King’s Indian Defence 162 5 KIA versus the ...Íf5 System 186 6 KIA versus the ...Íg4 System 240 7 KIA versus the Queen’s Indian 299 8 KIA versus the Dutch (and King’s Indian) 322 Index of Variations 344 Index of Complete Games 350 Introduction The King’s Indian Attack (or KIA) is a flexible opening system that can be employed by White after 1 Ìf3 or against the French, Sicilian, and Caro-Kann if he chooses to begin with 1 e4. -

Chess Pieces – Left to Right: King, Rook, Queen, Pawn, Knight and Bishop

CCHHEESSSS by Wikibooks contributors From Wikibooks, the open-content textbooks collection Permission is granted to copy, distribute and/or modify this document under the terms of the GNU Free Documentation License, Version 1.2 or any later version published by the Free Software Foundation; with no Invariant Sections, no Front-Cover Texts, and no Back-Cover Texts. A copy of the license is included in the section entitled "GNU Free Documentation License". Image licenses are listed in the section entitled "Image Credits." Principal authors: WarrenWilkinson (C) · Dysprosia (C) · Darvian (C) · Tm chk (C) · Bill Alexander (C) Cover: Chess pieces – left to right: king, rook, queen, pawn, knight and bishop. Photo taken by Alan Light. The current version of this Wikibook may be found at: http://en.wikibooks.org/wiki/Chess Contents Chapter 01: Playing the Game..............................................................................................................4 Chapter 02: Notating the Game..........................................................................................................14 Chapter 03: Tactics.............................................................................................................................19 Chapter 04: Strategy........................................................................................................................... 26 Chapter 05: Basic Openings............................................................................................................... 36 Chapter 06: -

![Air-To-Air Missile [UPSC Notes for GS III]](https://docslib.b-cdn.net/cover/7987/air-to-air-missile-upsc-notes-for-gs-iii-1297987.webp)

Air-To-Air Missile [UPSC Notes for GS III]

Air-to-Air Missile [UPSC Notes for GS III] An air-to-air missile (AAM) is a missile fired from an aircraft for the purpose of destroying another aircraft. AAMs are typically powered by one or more rocket motors, usually solid fueled but sometimes liquid- fueled. The topic finds relevance in GS-3 of the UPSC exam. Types of Air-to-Air Missiles Air-to-air missiles are broadly categorized into two groups: “Short range missiles” and “medium or long range missiles”. o The missiles designed to engage opposing aircraft at a range of less than 30 km are known as short-range or "within visual range" missiles. o The medium- or long-range missiles, both fall under the category of “beyond visual range” missiles, and often rely upon radar guidance. The short-range missiles are sometimes called "dogfight" missiles because they are designed to optimize their agility rather than range. Astra Air-to-Air Missile It is an all-weather missile developed by the Defence Research and Development Organisation, and its production began in 2017. Astra is the smallest missile in terms of size and weight, developed by the DRDO. Type of missile: It is a Beyond-Visual Range Air-to-Air indigenously developed missile (BVRAAM). Specifications: o It has a terminal Active Radar Homing (ARH). ARH is a missile guidance method in which a missile contains a radar transceiver and the electronics necessary for it to find and track its target autonomously. o The missile is capable of engaging targets at varying ranges and altitudes for engagement with short-range and long-range targets. -

Report of Working Group on Defence Equipment

REPORT OF WORKING GROUP ON DEFENCE EQUIPMENT 1 INDEX 1. OVERVIEW 1.1 DEFENCE SPENDING 1.2 DPSUs AND OFB 1.3 PRIVATE SECTOR 1.4 FDI IN DEFENCE SECTOR 1.5 DEFENCE EXPORTS 1.6 LAND SYSTEMS 1.7 SHIPYARDS 1.8 ELECTRONICS SYSTEMS 2. OPPORTUNITIES 2.1 GROWTH POTENTIAL IN 12TH PLAN 2.2 LAND SYSTEMS 2.3 NAVAL SYSTEMS 2.4 ELECTRONICS SYSTEMS 3. CHALLENGES 3.1 RESTRICTED TECHNOLOGIES 3.2 HIGH R&D COST 3.3 LOW R&D EXPENDITURE 3.4 MONOPSONIC DEFENCE MARKET 3.5 SHIPYARD INFRASTRUCTURE AND FACILITIES 3.6 LOW VOLUMES OF HIGH TECHNOLOGY REQUIREMENTS 4. RECOMMENDATIONS 4.1 R&D ACTIVITY SUPPORT 4.2 DEFENCE ELECTRONICS 4.3 INDUSTRY – ACADEMIA CO-OPERATION 4.4 STRENGTHENING OF CERTIFICATION ORGANIZATIONS 4.5 PPP MODEL 4.6 VENDOR DEVELOPMENT 4.7 SECTOR SKILL COUNCIL 2 1. OVERVIEW 1.1 DEFENCE SPENDING India’s defence spending in the 11th Plan period (2007-12) has grown at a CAGR of 13%. (Source: Annual Defence Services Estimates Reports) Defence Equipment Production in India is primarily aimed at meeting internal demand. India's total defence spending in the 11th Plan Period (2007-12) has grown at a CAGR of 13% (Table I). Growth in procurement of defence equipment (both capital and revenue) in 2010-11 was about 13% over 2009-10 and 20% in 2009-10 over 2008-09. Imports in defence equipment procurement have averaged 30% of total procurement in last 3 years. Table - I (Values in Rs./ Crores ) Head 2007-08 2008-09 2009-10 2010-2011 2011-12 (Actual) (Actual) (Actual) (Revised Es- (Budget Es- timates) timates) Revenue Expen- 54218.61 73304.80 90668.72 90748.43 95216.68 diture# Capital Expendi- 37461.67 40918.48 51112.36 60833.26 69198.81 ture Revenue & Capi- 91680.28 114223.28 141781.08 151581.69 164415.49 tal Expenditure #- The revenue expenditure figures include pay & allowances, transportation, revenue civil works in addition to the revenue purchase of Stores & Equipment. -

समाचार प से च यत अंश Newspapers Clippings

Dec 2020 समाचार प से चयत अशं Newspapers Clippings A Daily service to keep DRDO Fraternity abreast with DRDO Technologies, Defence Technologies, Defence Policies, International Relations and Science & Technology खंड : 45 अंक : 283 10 दसंबर 2020 Vol.: 45 Issue : 283 10 December 2020 ररा ववानान प ुपतकालयु तकालय DefenceDefence Science Science Library Library रार वैा वैानाकन कस चूसनूचान ाए एवव ं ं लेखनलेखन कक DefenceDefence Scientific Scientific Information Information & & Documentation Documentation Centre Centre , 110 054 मेटकॉफ हाउसहाउस, ददलल - - 110 054 MetcalfeMetcalfe House, House, Delhi Delhi - -110 110 054 054 CONTENTS S. No. TITLE Page No. DRDO News 1-11 DRDO Technology News 1-11 1. Quantum Communication between two DRDO Laboratories 1 2. दो डीआरडीओ योगशालाओं के बीच वांटम संचार 2 3. ' ' 3 ండ ఆఓ ప గాలల మధ ాంట కమష 4. DRDO successfully tests quantum key distribution tech for secure communication 4 between 2 facilities 5. डीआरडीओ ने दो योगशालाओं के बीच वांटम संचार का सफल परण कया 5 6. Bringing together top Scientists, Researchers on one platform 6 7. India offers LCA Tejas trainer variant to US Navy: Report 8 8. Big 2020 for Indian Armed Forces: China escalation to indigenisation push, 10 9 developments Defence News 11-15 Defence Strategic National/International 11-15 9. With China factor in play, Modi govt now open to Navy’s third aircraft carrier 11 demand 10. Submarine Day, celebrating the memory of INS Kalvari 12 11. -

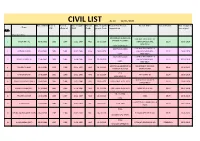

CIVIL LIST As on 12/01/2021

CIVIL LIST As on 12/01/2021 Date of Birth Year of Year of Date of apptt to Present Date of apptt to Present Post/ Present Present Office Present Station Date of apptt to Name CSE allotment IDAS Grade present Grade Organization present post Sl.No. (Kum/Smt/Shri) CONTROLLER GENERAL OF CONTROLLER GENERAL OF 1 SANJIV MITTAL 02-06-1962 1983 1984 21-12-1984 APEX 01-05-2019 DEFENCE ACCOUNTS DEFENCE ACCOUNTS, DELHI 01-05-2019 NEW DELHI CGDA , NEW DELHI ADDITIONAL CGDA CONTROLLER GENERAL OF 2 RAJNISH KUMAR 01-07-1962 1983 1984 01-01-1985 HAG+ 19-07-2019 DEFENCE ACCOUNTS, DELHI 19-07-2019 CGDA NEW DELHI ADDITIONAL CGDA CONTROLLER GENERAL OF 3 ALOK CHATURVEDI 11-06-1961 1984 1985 26-08-1985 HAG+ 01-10-2020 DEFENCE ACCOUNTS, DELHI 01-10-2020 CGDA NEW DELHI ADDITIONAL SECRETARY & DEPARTMENT OF RURAL 4 SANJEEV KUMAR 16-01-1961 1985 1986 02-01-1987 HAG 06-11-2013 DELHI 09-04-2019 FINANCIAL ADVISOR DEVELOPMENT PIFA 5 AVINASH DIKSHIT 10-06-1964 1985 1986 29-12-1986 HAG 23-01-2014 PIFA (ARMY-O) DELHI 28-08-2019 PIFA (ARMY-O) MINISTRY OF LABOUR & 6 ANURADHA PRASAD (SMT) 23-01-1964 1985 1986 22-12-1986 HAG 01-07-2014 ADDITIONAL SECRETARY DELHI 11-07-2018 EMPLOYMENT 7 RASIKA CHAUBE (SMT) 31-10-1963 1985 1986 25-08-1986 HAG 23-01-2014 ADDITIONAL SECRETARY MINISTRY OF STEEL DELHI 09-07-2018 SR. JT. CGDA 8 PRAVEEN KUMAR 12-04-1963 1986 1987 28-12-1987 HAG 14-09-2016 CGDA DELHI 28-08-2019 CGDA COMPETITION COMMISSION OF 9 SG DASTIDAR 13-07-1965 1986 1987 18-12-1987 HAG 29-05-2017 SECRETARY DELHI 09-12-2020 INDIA PCDA 10 DEVIKA RAGHUVANSHI (SMT) 06-02-1965 1987