2007 Automotive Sustainability Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

Vauxhall ,Pecial

r~---- ' VAUXHALL ,PECIAL ... VOLUME 4 NUMBER 9 60 ---·l. .. 1 ... 11®®?7 Vauxhall workers have for years been the cinderellas of the motor industry. Their wages are far lower than those received elsewhere. At the same time management, with the direct assistance of the local union officials~ have been able to enforce a regime within the factory which allows the boss · to do exactly as he likes in a way unheard of in decently organized firms. For yèars there was 'industrial peace' and Vauxhall became known to car workers as the 'cabbage patch'. But the worms have turned. Spearheaded by the militant Paint Shop (where workers have not only been able to exercise some control over the speed of the line but also to win substantial increases in wages, an unheard of situation at Vauxhall), the rest of the factory has begun to move. In the last year there have been a number of walk-outs and other 'incidents~~ Negotiations have been under way since the beginning of the year for a substantial wage increase. Even if won in full this would still not bring Vauxhall wages in line with those paid nationally. On July 10, hiding behind the government•s Incomes Policy, the management issued a number of proposals in relation to what it called 'production and efficiency aspects•. These proposals in our view would be unacceptable at any price. On September 13, workers at Luton, Dunstable and Ellesmere Port, fed up with the way things were going, initiated a work-to-rule and overtime ban. They have insisted that negotiations on the company's proposals don't drag on and that the wage_rises be obtained forthwith, without strings. -

Learning to Drive 112 Upper Parliament Street Nottingham Ng1 6Lp a Consultation Paper a Consultation on Learning to Drive

DRIVING STANDARDS AGENCY THE AXIS BUILDING LEARNING TO DRIVE 112 UPPER PARLIAMENT STREET NOTTINGHAM NG1 6LP A CONSULTATION PAPER A CONSULTATION ON A CONSULTATION LEARNING TO DRIVE LEARNING TO © Crown copyright 2008 dsa.gov.uk/learningtodrive Printed in the UK containing at least 80% recycled fibre CONTENTS MINISTERIAL FOREWORD 3 Marking system 39 Independant driving 39 EXECUTIVE SUMMARY 5 Situational judgement 40 Manoeuvres 40 HOW WE ARE CONDUCTING 11 THIS CONSULTATION Modular assessment 40 Feedback 41 1. THE CASE FOR CHANGE 15 6. STEP 2: AN IMPROVED LEARNING PROCESS 43 The problem 15 Syllabus and student workbook 43 Factors which contribute to the problem 16 New in-car learning 44 The results 18 7. STEP 3: BETTER INFORMATION 47 2. THE STARTING POSITION 21 ABOUT DRIVING INSTRUCTORS AND Learning arrangements 21 IMPROVED INSTRUCTOR TRAINING What the national driving test Reform of instructor training 49 currently involves 21 Our European Union obligations 22 8. STEP 4: FURTHER OPTIONS FOR 51 European requirements for driving examiners 22 LEARNING AND QUALIFICATIONS The risk of learner disengagement 22 New learning options - pre-test 51 Attitude advisor 51 3. OUR APPROACH TO REFORM 25 Driver discussion groups 53 Goals 25 Theory training 53 Methods 25 Using simulators 53 An improved driving test 25 Learning materials 53 An improved learning process 26 Pre-driver education in safe road use 54 Better information about driving instructors Lifelong driver development - post-test 56 and improved instructor training 26 Further qualifications 56 Further options for learning and qualifications 26 Motorway driving 57 Further benefits 27 Driving for work 57 Compliance 27 Drivers who offend 58 4. -

Ergomed Ab 01.12.2016 Bis 08.03.2020

Kraftfahrt-Bundesamt DE-24932 Flensburg ALLGEMEINE BETRIEBSERLAUBNIS (ABE) nach § 22 in Verbindung mit § 20 Straßenverkehrs-Zulassungs-Ordnung (StVZO) in der Fassung der Bekanntmachung vom 26.04.2012 (BGBl I S.679) Nummer der ABE: 91283*03 Gerät: Fahrzeugsitze (Einzelsitze) Typ: Ergomed Inhaber der ABE RECARO Automotive und Hersteller: Seating GmbH DE-73230 Kirchheim/Teck Für die oben bezeichneten reihenweise zu fertigenden oder gefertigten Geräte wird dieser Nachtrag mit folgender Maßgabe erteilt: Die sich aus der Allgemeinen Betriebserlaubnis ergebenden Pflichten gelten sinngemäß auch für den Nachtrag. In den bisherigen Genehmigungsunterlagen treten die aus diesem Nachtrag ersichtlichen Änderungen bzw. Ergänzungen ein. Kraftfahrt-Bundesamt DE-24932 Flensburg 2 Nummer der ABE: 91283*03 Die Fahrzeugsitze (Einzelsitze), Typ Ergomed, dürfen auch mit den im beiliegenden Nachtragsgutachten, genannten Einbaukonsolen (Adaptern) zur Verwendung in den dort aufgeführten Kraftfahrzeugen feilgeboten werden. In solchen Fällen, in denen entsprechend der Auflagen im Verwendungsbereich eine Begutachtung durchgeführt werden muß, ist der vorschriftsmäßige Zustand des Fahrzeuges durch einen amtlich anerkannten Sachverständigen oder Prüfer für den Kraftfahrzeugverkehr oder durch einen Prüfingenieur einer Überwachungsorganisation nach Nummer 4 der Anlage VIIIb zur StVZO unter Angabe von Fahrzeughersteller, Fahrzeugtyp und Fahrzeugidentifizierungsnummer auf einer separaten Anbaubestätigung zu bescheinigen. Im Übrigen gelten die im beiliegenden Nachtragsgutachten -

Witham (Specialist Vehicles) Ltd

Witham (Specialist Vehicles) Ltd By order of the UK Ministry of Defence MASSIVE SALE BY TENDER Monday 18th May 2015 2pm Viewing: Wednesday 13th Thursday 14th Friday 15th and Saturday 16th MAY 8:30am to 5:00pm Approx 600 + LOTS to Include MOTORCYCLES Land Rovers, Cars, Etc. Etc. AIRPORT GROUND EQUIPMENT Refueling Units, Hydrogen Trolleys, Toilet Servicing Units, Water Vehicles, Runway Sweepers, Etc. TRUCKS and HGV`s inc. Seddon Atkinson Trucks, Leyland Daf Drops 8 x 6 Trucks, 4x4 trucks. HGV`s Etc. JOHNSON RS 8000 Sweepers, Etc. FODEN 6 x 6 Heavy Recovery Vehicles with EKA Underlift, Crane and Winches TRAILERS Various inc. Penman Wide Track,Drawbar, Skip/Container, Motor- cycle, Agricultural, Etc. PLANT AND EQUIPMENT Still R7080 Diesel Fork Lifts c/w side shift, fork posi- tioner, triple mast, low hrs, Ex Reserve, Tractors, Mowers, Diesel Water Pumps, Sprayers, Etc. Etc. ARMOURED and COLLECTOR VEHICLES to include CVRT Scorpion, CVRT Spartan, CVRT Samson, CVRT Sturgeon, CVRT Sultan, CVRT Shielder, Com- bat Engineer Tractor Ex Reserve and fully Recon direct from storage unused , Very Rare Mine Plough Ex Reserve Etc. MISC. EQUIPMENT to inc. Winches, Insulated offices, workshops, Generators, Workshop Heaters, Ransomes Mowers, Lube Units, Tools, CES and Recovery Equipment, Clansman Radio Equipment, Electronic and Test Equipment, Camping Equipment, Tentage, Cam Nets, Copper Cable and Scrap Copper, Watches, Compasses, Etc Etc APPROX 400 + LOTS OF VEH SPARES inc. Recon Engines, Gearbox- es,Transmissions, Axles, Bearings, Prop shafts, Hydraulic Rams, Electrical Parts, Batteries, CVRT and FV Spares, Land Rover, Bedford, Leyland Daf, Foden, Man, Renault, JCB, Pinzgauer, RB 44, Volvo, New and Used Tyres Etc. -

Driving Standards Agency Annual Report and Accounts 2010-11 HC

ARA 10-11 final Cover 4pp :Layout 1 21/6/11 13:42 Page 1 Driving Standards Agency Annual Report and Accounts 2010 - 11 and Accounts Agency Annual Report Driving Standards Driving Standards Agency Annual Report and Accounts 2010-11 HC1104 £16.25 2010-11 Annual Report and Accounts Corporate member of Plain English Campaign 360 Committed to clearer communication 13155 HC 1104 Cover / sig1 plateA Driving Standards Agency Annual report and accounts 2010-11 Presented to Parliament Pursuant to section 4(6) of the Government Trading Funds Act 1973 as amended by the Government Trading Act 1990 Ordered by the House of Commons to be printed on 30 June 2011 HC 1104 London: The Stationery Office £16.25 © Crown copyright 2011 You may re-use this information (excluding logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit http://www.nationalarchives.gov.uk/doc/open- government-licence/ or e-mail: [email protected]. Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned. Any enquiries regarding this document should be sent to us at DSA Headquarters, The Axis, 112 Upper Parliament Street, Nottingham, NG1 6LP. This publication is also available for download at www.official-documents.gov.uk and is available from our website at dft.gov.uk/dsa ISBN: 9780102971545 Printed in the UK by The Stationery Office Limited on behalf of the Controller of Her Majesty’s Stationery Office ID 2426517 07/11 Printed on paper containing 75% recycled fibre content minimum. -

Pages for Preview

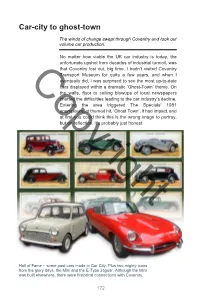

Car-city to ghost-town The winds of change swept through Coventry and took out volume car production. No matter how viable the UK car industry is today, the unfortunate upshot from decades of industrial turmoil, was that Coventry lost out, big time. I hadn’t visited Coventry Transport Museum for quite a few years, and when I eventually did, I was surprised to see the most up-to-date Copyrightcars displayed within a dramatic ‘Ghost-Town’ theme. On the walls, floor to ceiling blowups of local newspapers charted the difficulties leading to the car industry’s decline. Entering the area triggered The Specials’ 1981 unemployment themed hit, ‘Ghost Town’. It had impact, and at first you could think this is the wrong image to portray, but on reflection, it’s probably just honest. Hall of Fame – some past cars made in Car City. Plus two mighty icons from the glory days, the Mini and the E-Type Jaguar. Although the Mini was built elsewhere, there were historical connections with Coventry. 172 Copyright A year before the finish of car production, my father took part in the London to Brighton veteran car run driving a 1904 Siddeley which his department, Education and Training, maintained. As a postscript to car production ending, a special racing car had been built at Parkside for Tommy Sopwith junior – the son of the Hawker Siddeley owner. The 3.5 litre Sphinx was a massive departure from all that had gone My father in the before and was raced at Snetterton, Goodwood and 1904 Siddeley. Parked next to him Oulton Park, winning at the latter. -

Registration Document

20 REGISTRATION DOCUMENT Including the annual financial report 17 GROUPE PSA - 2017 REGISTRATION DOCUMENT -1 ANALYSIS OF THE BUSINESS AND GROUP OPERATING RESULTS IN 2017 AND OUTLOOK Capital Expenditure in Research & Development 4.4.2. Banque PSA Finance, signature of a framework agreement with the BNP Paribas Group to form a car financing Partnership for Opel Vauxhall vehicles On 6 March 2017, when the Master Agreement was concluded with BNP Paribas Personal Finance, will from an accounting point of view General Motors, the Company simultaneously signed a Framework retain the current European platform and staff of GM Financial. The Agreement with BNP Paribas and BNP Paribas Personal Finance, to Opel Vauxhall finance companies will distribute financial and organise the joint purchase of Opel Vauxhall’s finance companies insurance products over a territory initially including the following and the setting up of a car financing partnership for Opel Vauxhall countries: Germany, United Kingdom, France, Italy, Sweden, Austria, vehicles. Ireland, Netherlands, Belgium, Greece and Switzerland. The The acquisition of Opel Vauxhall’s finance companies will be cooperation may potentially be extended thereafter to other completed through a holding company. This joint venture, owned in countries where Opel Vauxhall has a presence. equal shares and on the same terms by Banque PSA Finance and 4.5. CAPITAL EXPENDITURE IN RESEARCH & DEVELOPMENT Automotive Expertise to deliver useful technologies Innovation, research and development are powerful levers for Every year, Groupe PSA invests in research and development to developing competitive advantages by addressing the major stay ahead, technologically, of environmental and market changes. challenges faced in the automotive industry (environmental, safety, emerging mobility and networking needs, etc.). -

Luton Motor Town

Contents Luton: Motor Town Luton: Motor Town 1910 - 2000 The resources in this pack focus on the major changes in the town during the 20th century. For the majority of the period Luton was a prosperous, optimistic town that encouraged forward-looking local planning and policy. The Straw Hat Boom Town, seeing problems ahead in its dependence on a single industry, worked hard to attract and develop new industries. In doing so it fuelled a growth that changed the town forever. However Luton became almost as dependant on the motor industry as it had been on the hat industry. The aim of this pack is to provide a core of resources that will help pupils studying local history at KS2 and 3 form a picture of Luton at this time. The primary evidence included in this pack may photocopied for educational use. If you wish to reproduce any part of this park for any other purpose then you should first contact Luton Museum Service for permission. Please remember these sheets are for educational use only. Normal copyright protection applies. Contents 1: Teachers’ Notes Suggestions for using these resources Bibliography 2: The Town and its buildings 20th Century Descriptions A collection of references to the town from a variety of sources. They illustrate how the town has been viewed by others during this period. Luton Council on Luton The following are quotes from the Year Book and Official Guides produced by Luton Council over the years. They offer an idea of how the Luton Council saw the town it was running. -

QUAD-CITIES BRITISH AUTO CLUB 2017 Edition / Issue 12 5 December 2017

QUAD-CITIES BRITISH AUTO CLUB 2017 Edition / Issue 12 5 December 2017 CHRISTMAS EDITION CONTENTS The QCBAC 1 THE QCBAC The QCBAC was formed to promote interest and usage of any and all British Christmas Puzzle 1 cars. The QCBAC website is at: http://www.qcbac.com QCBAC Contacts 1 Christmas Dinner 2 Clues and Puzzle Clues 2 word list are on Puzzle Word List 2 page 2. Board Meeting 3 Car of the Month 4 British Auto News 15 Crossword Answer 20 Question Answer 20 Thanks to the Board 20 QCBAC CONTACTS President Jerry Nesbitt [email protected] Vice President Larry Hipple [email protected] Secretary John Weber [email protected] Treasurer Dave Bishop [email protected] Board member Carl Jamison [email protected] Board member Gary Spohn [email protected] Autofest Chair Frank Becker [email protected] 2017 Santa Test Run Membership Chair Pegg Shepherd [email protected] Publicity Chair Glen Just [email protected] Page 1 of 20 QCBAC CHRISTMAS DINNER BRIT CAR QUESTION The QCBAC Christmas will take place on 10 December at Montana Jacks, 5400 27th St, Moline, IL. Bring a wrapped $5 gift for the traditional secret gift You are probably familiar exchange. with the British driver Malcolm Campbell who RSVP to Linda Weber: [email protected] held numerous land speed by 30 November so the appropriate space can be reserved. records from 1924 to 1935. The 1935 301.3 mph LSR was made in the 1931 Blue CHRISTMAS PUZZLE CLUES Bird powered by a 2,300 hp Rolls Royce V12. -

Appendix C. List of Consultees

Appendix C. List of Consultees C.1. Introduction C.1.1 This appendix provides a list of the organisations consulted under section 42, section 47 and section 48 of the Planning Act 2008 . C.2. Section 42(1)(a) Prescribed Consultees C.2.1 Prescribed consultees are set out under Schedule 1 of the Infrastructure Planning (Applications: Prescribed Forms and Procedure) Regulations 2009 ; these are outlined in Appendix Table A below. Any variation from the list of organisations set out in Schedule 1 is clarified within column 3 of the table. C.2.2 The Planning Inspectorate provided a list of prescribed consultation bodies in accordance with Regulation 9(1)(b) of the EIA Regulations and Advice Note three 1 (see Appendix A ), referred to as the “Regulation 9 list”. Those consultees included in the Reg 9 list are included in Table A, B and C. Those consultees that were not previously identified as a prescribed consultee as per Schedule 1 are identified with asterisk (*), and were consulted in the same way as the Schedule 1 consultees. C.2.3 The list of parish councils consulted under section 42 (1) (a) is outlined separately in Appendix Table C. The list of statutory undertakers consulted under Section 42 (1) (a) is outlined separately in Appendix Table B . C.2.4 Organisations noted in Appendix Tables A, B and C were issued with a copy of the Section 48 notice, notifying them of the proposed application and with consultation information, including the consultation brochure and details of how to respond. Appendix Table A: Prescribed Consultees Variation from the schedule where Consultee Organisation applicable The proposed application is not likely The Welsh Ministers N/A to affect land in Wales. -

GKN EVO Edrive Systems Ltd

GKN EVO eDrive Systems Ltd. 1 GKN Driveline Largest business of British global engineer GKN Broadest global footprint Market leading driveline technologies • CVJ Systems • AWD Systems Sales per region • Trans Axle Solutions • eDrive Systems Established long term global relationships Focussed engineering resource providing driveline solutions Expert customer specific account teams Sales per customer EVO Electric Originally a spinout from Imperial College London (est. 2006) Developer of high-performance axial flux electric motors Operating in automotive, motorsport, off-highway and power generation markets Achievements • London Taxi – demonstrated vehicle 56% improvement in fuel economy • Development Projects with Jaguar, Lotus and Nissan • Growing order book • Major OEMs and end-users fully engaged • Formation of partnership with GKN Driveline GKN Driveline & EVO Electric June 2011: • GKN acquires 25.1% stake in EVO Electric - UK based developer of axial flux electric motor technology • GKN and EVO form 50:50 Joint Venture – GKN EVO eDrive Systems – to industrialise and commercialise EVO’s Axial Flux motor technology for Automotive market 4 4 Electric motors in the market Hybridisation & Electrification driving demand for advanced electric motor & powertrain technology Electric motors and Drives are 40% of value in Electric Vehicle Existing technology has limited scope for improvement and is too expensive A step-change in motor technology is needed to power the new generation of vehicles Why EVO? Patented World class performance – High