European Telecom Services: Make up Or Break Up

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

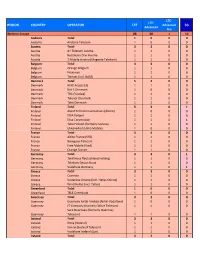

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Expte. S/0490/13 ACUERDOS TELEFÓNICA/YOIGO)

RESOLUCIÓN (Expte. S/0490/13 ACUERDOS TELEFÓNICA/YOIGO) SALA DE COMPETENCIA PRESIDENTE D. José María Marín Quemada CONSEJEROS Dª. María Ortiz Aguilar D. Fernando Torremocha y García-Sáenz D. Benigno Valdés Díaz Dª. Idoia Zenarrutzabeitia Beldarrain SECRETARIO D. Tomás Suárez-Inclán González En Madrid, a 16 de julio de 2015 La Sala de Competencia del Consejo de la Comisión Nacional de los Mercados y la Competencia ha dictado esta Resolución en el expediente S/0490/13, incoado por la extinta Dirección de Investigación de la Comisión Nacional de Competencia contra Telefónica de España, S.A.U., Telefónica Móviles de España, S.A.U. y Xfera Móviles, S.A.U. por la supuesta infracción de los artículos 1 de la Ley 15/2007, de 3 de julio, de Defensa de la Competencia y 101 del Tratado de Funcionamiento de la Unión Europea. ANTECEDENTES DE HECHO 1. Con fecha 29 de agosto de 2013, tuvo entrada en el registro de la Comisión Nacional de Competencia (CNC), un escrito de Vodafone España, S.A.U. (en adelante, VODAFONE) por el que formuló denuncia contra Telefónica de España, S.A.U., Telefónica Móviles de España, S.A.U. (conjuntamente TELEFÓNICA) y Xfera Móviles, S.A.U. (YOIGO), en relación con una serie de acuerdos firmados entre ambos operadores el 31 de julio de 2013, en el marco de los cuales se produce además la operación de concentración por la que Abertis Telecom, S.A.U. (ABERTIS) adquiere el control exclusivo de un conjunto de torres para prestar servicios de comunicaciones móviles, junto con la infraestructura adyacente, tanto de TELEFÓNICA como de YOIGO. -

Termination Rates at European Level January 2021

BoR (21) 71 Termination rates at European level January 2021 10 June 2021 BoR (21) 71 Table of contents 1. Executive Summary ........................................................................................................ 2 2. Fixed networks – voice interconnection ..................................................................... 6 2.1. Assumptions made for the benchmarking ................................................................ 6 2.2. FTR benchmark .......................................................................................................... 6 2.3. Short term evolution of fixed incumbents’ FTRs (from July 2020 to January 2021) ................................................................................................................................... 9 2.4. FTR regulatory model implemented and symmetry overview ............................... 12 2.5. Number of lines and market shares ........................................................................ 13 3. Mobile networks – voice interconnection ................................................................. 14 3.1. Assumptions made for the benchmarking .............................................................. 14 3.2. Average MTR per country: rates per voice minute (as of January 2021) ............ 15 3.3. Average MTR per operator ...................................................................................... 18 3.4. Average MTR: Time series of simple average and weighted average at European level ................................................................................................................. -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

Satisfaction of Business Customers with Mobile Phone and Internet Services in Spain$

Telecommunications Policy ∎ (∎∎∎∎) ∎∎∎–∎∎∎ Contents lists available at ScienceDirect Telecommunications Policy URL: www.elsevier.com/locate/telpol Satisfaction of business customers with mobile phone and internet services in Spain$ David Suárez a,n, Begoña García-Mariñoso a, Iván Santos b a Department of Statistics, Comisión Nacional de los Mercados y la Competencia (CNMC), Spain b Comisión Nacional de los Mercados y la Competencia (CNMC), Spain article info abstract Lately there has been a growing debate on the differences between business and resi- Keywords: dential telecom consumers. Yet, evidence on these differences is lacking. This study par- Consumer satisfaction tially fills this gap by econometrically analyzing the drivers of satisfaction with mobile and Mobile phones fixed internet services for business clients in Spain. The results reveal that the factors that Internet drive satisfaction for micro-enterprises and residential customers are similar, but the Business consumers drivers of satisfaction for small and medium-sized enterprises (SMEs) are distinct. For Econometric models example, alternative DSL operators outperform the incumbent for micro-enterprises, but not for SMEs. Overall, for both fixed internet and mobile services, operators with small market shares perform better than the incumbent, and business clients’ satisfaction levels increase when they perceive that they can switch operators. Finally, subscribing to mobile and fixed bundles and dealing only with one telecom operator increase SMEs’ satisfaction. & 2015 Elsevier -

Ofcom CEO Resists Openreach Sell-Off

CityFibre chief gets Why we should listen UK’s dark fibre ducts to Sabio on customer in a row p28 engagement p30 VOL 21 ISSUE 3 AUGUST 2016 www.comms-dealer.com ADVERTISEMENT ADVERTISEMENT 7025_Comms DealerTHE Ear April new logoHEARTBEAT UPDATED.indd13/07/2016 110:24 OF THE UK COMMS 7025_CommsINDUSTRY Dealer Ear April new logo UPDATED.indd13/07/2016 210:24 created by Cloud Billing made easy. Multiple online billing 01256 799812 solutions designed for every business requirement. www.quickstart-billing.co.uk 3-23 Industry News Catch up with events in comms channeltelecom.com 24 Business Matters Connectivity firms CommsdealerjunePRINT.pdf 1 23/06/2016 12:11 set growth pace 32 676_CT_Comms_Dealer_40x60_advert_3.inddC 28/07/2016 1 18:20 Business. Business. Business. Business. Business. Business. Business. BusineOfcomss. CEO resists Interview Business. Business. Business. Business. Business. Business. M Business. BusineYourss. success, Business. Business. Business. Business. Business. Business. Business. COLT ramps up YBusiness. Multiplied.Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. channel strategy CMBusiness. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. MY Business. Business. Business. Business. Business. Business. Business. BusineOpenreachss. sell-off Business. Business. Business. Business. Business. Business. Business. Business. CYBusiness. Business. Business. Business. Business. Business. Business. Business. 36 Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. Business. CMY OFCOM resisted the full separation of Openreach from BT Group in last Business. Business. Business. Business. Business. Business. Business. Business. News Update Business. -

Eutelsat S.A. €300,000,000 3.125% Bonds Due 2022 Issue Price: 99.148 Per Cent

EUTELSAT S.A. €300,000,000 3.125% BONDS DUE 2022 ISSUE PRICE: 99.148 PER CENT The €300,000,000 aggregate principal amount 3.125% per cent. bonds due 10 October 2022 (the Bonds) of Eutelsat S.A. (the Issuer) will be issued outside the Republic of France on 9 October 2012 (the Bond Issue). Each Bond will bear interest on its principal amount at a fixed rate of 3.125 percent. per annum from (and including) 9 October 2012 (the Issue Date) to (but excluding) 10 October 2022, payable in Euro annually in arrears on 10 October in each year and commencing on 10 October 2013, as further described in "Terms and Conditions of the Bonds - Interest"). Unless previously redeemed or purchased and cancelled in accordance with the terms and conditions of the Bonds, the Bonds will be redeemed at their principal amount on 10 October 2022 (the Maturity Date). The Issuer may at its option, and in certain circumstances shall, redeem all (but not part) of the Bonds at par plus any accrued and unpaid interest upon the occurrence of certain tax changes as further described in the section "Terms and Conditions of the Bonds - Redemption and Purchase - Redemption for tax reasons". The Bondholders may under certain conditions request the Issuer to redeem all or part of the Bonds following the occurrence of certain events triggering a downgrading of the Bonds as further described in the Section "Terms and Conditions of the Bonds — Redemption and Purchase - Redemption following a Change of Control". The obligations of the Issuer in respect of principal and interest payable under the Bonds constitute direct, unconditional, unsecured and unsubordinated obligations of the Issuer and shall at all times rank pari passu among themselves and pari passu with all other present or future direct, unconditional, unsecured and unsubordinated obligations of the Issuer, as further described in "Terms and Conditions of the Bonds - Status". -

Prepared for Upload GCD Wls Networks

LTE‐ LTE‐ REGION COUNTRY OPERATOR LTE Advanced 5G Advanced Pro Western Europe 88 68 1 10 Andorra Total 10 0 0 Andorra Andorra Telecom 10 0 0 Austria Total 33 0 0 Austria A1 Telekom Austria 11 0 0 Austria Hutchison Drei Austria 11 0 0 Austria T‐Mobile Austria (Magenta Telekom) 11 0 0 Belgium Total 33 0 0 Belgium Orange Belgium 11 0 0 Belgium Proximus 11 0 0 Belgium Telenet (incl. BASE) 11 0 0 Denmark Total 54 0 0 Denmark Hi3G Access (3) 11 0 0 Denmark Net 1 Denmark 10 0 0 Denmark TDC (YouSee) 11 0 0 Denmark Telenor Denmark 11 0 0 Denmark Telia Denmark 11 0 0 Finland Total 53 0 1 Finland Aland Telecommunications (Alcom) 10 0 0 Finland DNA Finland 11 0 0 Finland Elisa Corporation 11 0 1 Finland Telia Finland (formerly Sonera) 11 0 0 Finland Ukkoverkot (Ukko Mobile) 10 0 0 France Total 44 0 0 France Altice France (SFR) 11 0 0 France Bouygues Telecom 11 0 0 France Free Mobile (Iliad) 11 0 0 France Orange France 11 0 0 Germany Total 33 0 1 Germany Telefonica Deutschland Holding 11 0 0 Germany Telekom Deutschland 11 0 0 Germany Vodafone Germany 11 0 1 Greece Total 33 0 0 Greece Cosmote 11 0 0 Greece Vodafone Greece (incl. Hellas Online) 11 0 0 Greece Wind Hellas (incl. Tellas) 11 0 0 Greenland Total 10 0 0 Greenland TELE Greenland 10 0 0 Guernsey Total 32 0 0 Guernsey Guernsey Airtel Limited (Airtel‐Vodafone) 10 0 0 Guernsey JT Guernsey (formerly Wave Telecom) 11 0 0 Sure Guernsey (formerly Guernsey Guernsey Telecom) 11 0 0 Iceland Total 33 0 0 Iceland Nova (Iceland) 11 0 0 Iceland Siminn (Iceland Telecom) 11 0 0 Iceland Vodafone Iceland (Syn) -

European Telecom Services: the Rise of the Wholesale-Only Model

Equity Research 3 May 2018 European Telecom Services INDUSTRY UPDATE The rise of the Wholesale-Only model European Telecom Services Until recently it was almost unthinkable that any company would consider creating POSITIVE a third expensive parallel Telecom infrastructure, competing with EU incumbents Unchanged and cable, given the high barrier to entry/cost of rollout, relatively stable competition plus mature nature of the industry. However, we are now seeing European Telecom Services strategic moves across a number of European markets, with Open Fiber in Italy the Maurice Patrick highest profile case study, and others following. In this detailed report we analyse +44 (0)20 3134 3622 Open Fiber’s prospects, its key success factors, and identify risks to other EU [email protected] markets. We conclude that Italy is in many ways a “perfect storm”, creating a fertile Barclays, UK investment opportunity for alternative infrastructure. Only Germany and the UK are Mathieu Robilliard likely to see wholesale only on a similar scale, given low incumbent FTTH builds and +44 203 134 3288 high service provider interest. Today we downgraded BT to EW and upgraded TEF [email protected] DE to OW, and we believe OW-rated VOD and ORA are de-risked vs. peers. Barclays, UK Open Fiber – Driving cost-effective rollout and high penetration. Open Fiber will Daniel Morris double its FTTH footprint to c5m homes by end-2018, and 19m by 2023. The company +44 (0)20 7773 2113 sees c.50% penetration in “mature” areas, with newly built areas at c.10% and rising, [email protected] per our recent meeting. -

Consulta Yoigo CLI Móvil-Fijo

COMISIÓN DEL MERCADO DE LAS TELECOMUNICACIONES JORGE SÁNCHEZ VICENTE, Secretario del Consejo de la Comisión del Mercado de las Telecomunicaciones, en uso de las competencias que le otorga el artículo 40 del Reglamento de la Comisión del Mercado de las Telecomunicaciones, aprobado por Real Decreto 1994/1996, de 6 de septiembre, CERTIFICA Que en la Sesión número 44/12 del Consejo de la Comisión del Mercado de las Telecomunicaciones, celebrada el día 13 de diciembre de 2012, se ha adoptado el siguiente ACUERDO Por el cual se aprueba la Respuesta a la consulta formulada por Yoigo en relación a la identificación de línea llamante. (DT 2012/1489) I ANTECEDENTES Y OBJETO MATERIAL DE LA CONSULTA PRIMERO.- Con fecha 2 de julio de 2012, tuvo entrada en el Registro de la Comisión del Mercado de las Telecomunicaciones (en adelante, Comisión) escrito de Xfera Móviles S.A. (en adelante Yoigo) mediante el que plantea una consulta sobre [CONFIDENCIAL la posibilidad de modificar la identificación de línea llamante (en adelante CLI, Calling Line Identification), introduciendo como número llamante un número geográfico en determinados escenarios FIN CONFIDENCIAL]. II COMPETENCIA DE LA COMISIÓN De acuerdo con lo establecido en el artículo 48 de la Ley 32/2003, de 3 de noviembre, General de Telecomunicaciones (en adelante, LGTel), esta Comisión tiene por objeto “el establecimiento y supervisión de las obligaciones específicas que hayan de cumplir los operadores en los mercados de telecomunicaciones y el fomento de la competencia en los mercados de los servicios -

Annual and Sustainability Report 2020 Content

BETTER CONNECTED LIVING ANNUAL AND SUSTAINABILITY REPORT 2020 CONTENT OUR COMPANY Telia Company at a glance ...................................................... 4 2020 in brief ............................................................................ 6 Comments from the Chair ..................................................... 10 Comments from the CEO ...................................................... 12 Trends and strategy ............................................................... 14 DIRECTORS' REPORT Group development .............................................................. 20 Country development ........................................................... 38 Sustainability ........................................................................ 48 Risks and uncertainties ......................................................... 80 CORPORATE GOVERNANCE Corporate Governance Statement ......................................... 90 Board of Directors .............................................................. 104 Group Executive Management ............................................ 106 FINANCIAL STATEMENTS Consolidated statements of comprehensive income ........... 108 Consolidated statements of financial position ..................... 109 Consolidated statements of cash flows ............................... 110 Consolidated statements of changes in equity .................... 111 Notes to consolidated financial statements ......................... 112 Parent company income statements ................................... -

Telia Year-End Report 2000

Telia Year-End Report 2000 Telia AB (publ), SE-123 86 Farsta, Sweden Corporate Registration No. 556103-4249, Registered Office: Stockholm Telia Year-End Report 2000 Telia January–December 2000 · Strong sales in high-priority areas: Mobile Telephony +42 %, Network Wholesaling Sweden +62 %, International Carrier +32 % · The Group’s net sales totaled MSEK 54,064, an increase of 4.5 % for comparable units · The positive EBITDA trend reported in the third quarter remains unbroken. Underlying EBITDA increased by 13 % in the fourth quarter, reaching MSEK 13,087 for the full year · Operating income increased to MSEK 12,006 (MSEK 5,946) · A Letter of Intent was signed with Tele 2 concerning joint construction of the Swedish UMTS network · Letter of Intent in February 2001 on sale of the mobile operator Tess Review of Group Earnings Oct-Dec Oct-Dec Full Year Full Year MSEK 2000 1999 2000 1999 Net sales 14,540 14,887 54,064 52,121 Change in net sales (%) -2.3 7.4 3.7 5.1 Underlying EBITDA 3,790 3,343 13,087 14,059 Underlying EBITDA margin (%) 26.1 22.5 24.2 27.0 Operating income 7,930 2,505 12,006 5,946 Income after financial items 7,658 2,445 11,717 5,980 Net income 7,408 1,755 10,278 4,222 Earnings per share (SEK) 2.47 0.62 3.50 1.48 Return on equity (%) – – 23.9 14.2 Investments 10,311 4,912 47,742 12,145 of which shares and participations 3,085 1,996 8,269 4,109 Summary The Telia Group is reporting sustained robust growth in its tive prices and the high quality of the network resulted in high-priority areas.