Accelerating Bus Electrification: Enabling a Sustainable Transition to Low Carbon Transportation Systems

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Work Truck–Green Truck 2011

WTS2011 d2p1 rpOK:- 3/8/11 7:10 PM Page 1 WORK TRUCK SHOW & GREEN TRUCK SUMMIT WEDNESDAY, MARCH 9, 2011 Work Truck–Green Truck 2011 BAF for Knapheide Clean Energy’s BAF Technologies unit is providing the CNG fuel system for trucks by Knapheide Manufacturing –and is being promoted by Altec and Sortimo. —Page 5 BAE Taps Cat BAE Systems will use a Caterpillar trans- mission as it brings a parallel version of its successful series hybrid electric drivetrain for buses to the truck world. —Page 6 Battery Garbage The City of Chicago says it would like to be first to field an all-electric refuse truck –if a U.S. OEM would build one. Dow Kokam’s got the batteries. —Page 6 Hino Motors president Yoshiro Shirai introduces the new hybrid-electric cabover at Work Truck Show 2011. Landi for L&P Landi Renzo USA providing the CNG fuel Hino Brings a Hybrid to the U.S. Market system for Ford trucks by Leggett & Platt. —Page 7 Hino Trucks took bold strides into the U.S. market yes- Hino will begin taking orders in May for delivery to terday, announcing a new line of Class 4/5 cabovers, dealers in August for the diesels, and September for including two diesel-electric hybrid variants, a first in delivery to dealers in December for the hybrids, which Dueling Hybrids the U.S. Class 4 cab-over space. will initially be introduced in California, New York, Two start-ups targeting first retrofit and “We have a burning desire to make the world a Chicago, Atlanta, Houston, Dallas, Philadelphia and then OEM applications for their energy- better place,” proclaimed Hino Motors president Yoshiro Washington, D.C. -

Advanced Technology Equipment Manufacturers*

Advanced Technology Equipment Manufacturers* Revised 04/21/2020 On-Road (Medium/Heavy Duty, Terminal Tractors) OEM Model Technology Vocations GVWR Type Altec Industries, Inc Altec 12E8 JEMS ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 1820 and 18E20 ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 4E4 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Altec Industries, Inc Altec JEMS 6E6 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport ISX12N Engine Near-Zero Engine Truck > 33,001 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport L9N Engine Near-Zero Engine Refuse > 33,001 New Blue Bird Blue Bird Electric Powered All American School Bus Zero Emission Bus, School Bus > 30,000 New Blue Bird Blue Bird Electric Powered Vision School Bus 4x2 Configuration Zero Emission Bus, School Bus > 30,000 New BYD Motors BYD 8Y Electric Yard Tractor Zero Emission Terminal Truck 81,000 New BYD Motors BYD C10 45' All-Electric Coach Bus Zero Emission Bus 49,604 New BYD Motors BYD C10MS 45' All-Electric Double-Decker Coach Bus Zero Emission Transit Bus 45' New BYD Motors BYD C6 23' All-Electric Coach Bus Zero Emission Bus 18,331 New BYD Motors BYD K11 60' Articulated All-Electric Transit Bus Zero Emission Bus 65,036 New BYD Motors BYD K7M 30' All-Electric Transit Bus Zero Emission Bus, Transit Bus 30' New BYD Motors BYD K9 40' All-Electric Transit Bus Zero Emission -

An Examination of Heavy-Duty Trucks Drivetrain Options to Reduce GHG Emissions in British Columbia

An Examination of Heavy-duty Trucks Drivetrain Options to Reduce GHG Emissions in British Columbia S. Mojtaba Lajevardi B.Sc., K.N.Toosi University of Technology, 2005 M.Sc., Sharif University of Technology, 2008 A Dissertation Submitted in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY in the Department of Mechanical Engineering © S. Mojtaba Lajevardi, 2019 University of Victoria All rights reserved. This dissertation may not be reproduced in whole or in part, by photocopying or other means, without the permission of the author. An Examination of Heavy-duty Trucks Drivetrain Options to Reduce GHG Emissions in British Columbia S. Mojtaba Lajevardi B.Sc., K.N.Toosi University of Technology, 2005 M.Sc., Sharif University of Technology, 2008 Supervisory Committee Dr. C. Crawford, Supervisor (Department of Mechanical Engineering, UVic) Dr. Jonn Axsen, Co-Supervisor (School of Resource and Environmental Management, SFU) Dr. Andrew Rowe, Committee member (Department of Mechanical Engineering, UVic) ii Abstract Heavy-duty trucks (HDTs) are vital in delivering products to the consumers around the world and help maintain the quality of life. However, they are heavily depending on fossil diesel use, which causing global climate change as well as local air pollutions. Although they represent a small percentage of vehicle population, they emit more than 30% of GHGs in road transportation or 5% of global greenhouse gas (GHG) emissions. Furthermore, GHG emissions from this sector are expected to steadily grow due to economic growth, globalization, industrialization, online shopping, and fast delivery expectations. This study was focused on the Canadian province of British Columbia (BC) as a case study where HDTs are responsible for more than 4% of total provincial GHGs. -

ACT EXPO 2013 Wednesday, JUNE 26 Welcome to ACT Expo 2013 ANGA Promotes TA & Shell for LNG Travelcenters Plan for Trucks CNG for Detailed Here

ACT EXPO 2013 WEDNESDAY, JUNE 26 Welcome to ACT Expo 2013 ANGA Promotes TA & Shell for LNG TravelCenters plan for trucks CNG for detailed here. —Page 4 Consumers Ryder for Lighter NGVs Adds 20 CNG GreenKraft and 19 Navistar TranStar for California rent and lease. —Page 8 Trillium Wins Frito War Emerges the winner under innovative RFP. —Page 9 Landi Renzo Adds Dual Fuel Stepping up their drive to bring compressed natural gas to the masses, two advocate groups unveiled six popular automobiles Starts with 12.7-liter DDC engine here converted to run on both gasoline and CNG. Marty Durbin, president & CEO of America’s Natural Gas Alliance and Kathryn Clay, executive director of the Drive Natural Gas Initiative (a collaboration between ANGA and the American Gas Association), for OUL market. —Page 10 said the campaign is aimed to convince consumers, automakers and policymakers of the benefits of CNG as an abundant, affordable clean resource. “Manufacturers are offering bi-fuel vehicles in many other countries around the world; we want Clean Energy Buys Mansfield them in showrooms here,” said Clay. —More ANGA Roadshow on Page 18 Acquisition for $20 million brings liquid fuels capability. —Page 11 Wrightspeed Opens Show Penske for Propane California’s Wrightspeed, a developer of light to medium duty plug-in hybrid Supporting Roush-powered trucks electric trucks – including a CNG-fueled demonstrator – hosted yesterday for Chicago’s Alpha Baking. evening’s ACT Expo 2013 opening reception in the Expo Hall. Seen here —Page 20 with “The Route” drive at Booth 213 is Wrightspeed’s new sales and mar- keting VP Jonathan Randall (ex-Freightliner Custom Chassis Corp). -

Transcript the 12/02/15 Workshop on Medium and Heavy

DOCKETED Docket Number: 15-MISC-04 Project Title: Fuels and Transportation Merit Review TN #: 207132 Document Title: Transcript the 12/02/15 Workshop on Medium and Heavy Duty Vehicle Project Success Description: N/A Filer: Cody Goldthrite Organization: California Energy Commission Submitter Role: Commission Staff Submission 12/28/2015 10:54:14 AM Date: Docketed Date: 12/28/2015 CALIFORNIA ENERGY COMMISSION TRANSPORTATION LEAD COMMISSIONER WORKSHOP In the Matter of: ) Docket No. 15-MISC-04 Technology Merit Review: ) Medium and Heavy Duty Vehicle ) Project Success ) ) CALIFORNIA ENERGY COMMISSION FIRST FLOOR, ART ROSENFELD HEARING ROOM 1516 NINTH STREET SACRAMENTO, CALIFORNIA WEDNESDAY, DECEMBER 2, 2015 9:00 A.M. Reported by: Peter Petty ii APPEARANCES COMMISSIONERS PRESENT Janea Scott, Lead Commissioner, Transportation Committee CEC STAFF PRESENT Tim Olson, Fuels and Transportation Division Larry Rillera, Vehicle Technology Development, Manufacturing and Business Development Hieu Nguyen PRESENTERS Tom Hodek, Cummins Westport, Inc. Joe Impullitti, SCAQMD Ian Wright, Wrightspeed, Inc. Mike Simon, Transportation Power Inc. (TransPower) Jim Castelaz, Motiv Power Systems, Inc. Kent Leacock, Proterra, Inc. Rob Del Core, Hydrogenics USA, Inc. REVIEWERS/COMMENTERS Robert Nguyen, California Air Resources Board Kevin Walkowicz, National Renewable Energy Laboratory Kuang Wei, United States Environmental Protection Agency Margo Melendez, National Renewable Energy Laboratory Matt Miyasato, South Coast Air Quality Management District iii APPEARANCES PUBLIC COMMENT Ryan Schuchard, CalStart Jerry Wiens, Retired Annuitant, CEC 1 1 2 P R O C E E D I N G S 3 9:03 A.M. 4 SACRAMENTO, CALIFORNIA, WEDNESDAY, DECEMBER 2, 2015 5 (The meeting commenced at 9:03 a.m.) 6 COMMISSIONER SCOTT: Welcome. -

Penske Says 'Not at This Time' for NZ Automotive

VOLUME 6 ISSUE 10 NOVEMBER 2015 “DOING THE BASICS” WILL MAKE YOU MORE MONEY FIND OUT ON PAGE 22 EV pioneer switches on to trucks x-pat Kiwi engineer Ian Wright - co-founder of Tesla Eand founder of Wrightspeed - thinks much of the EV push is misdirected. Auckland mayor Len Brown, president of Penske Transportation Group International Randall Seymour While in Auck- and chairman of Penske Automotive Group Roger Penske. land in October for the transport fuels and fleet management Penske says ‘not at this summit, Wright took time from his schedule Ian Wright time’ for NZ automotive to speak to DIESELTalk editor Robert Barry. lobal automotive icon Roger sales, parts and leasing and was an He believes that when the Penske has not ruled out early investor in online vehicle sites. automotive world looked to de- Ginvesting in the New Zealand He is a motorsport legend, and velop electric vehicle solutions to automotive market, in the long term. owner of a number of teams, includ- save fossil fuels, the manufactur- Penske has interests including ing the former Dick Johnson Racing ers asked the wrong question. automotive retail, truck distribution, Continued on page 3 “They didn’t ask, how can we save the most fuel per vehicle per INSIDE year?” he says. Import dealer to list? 3 Read the full interview with Industry backs Green move 4 Wright in DIESELTalk, out Tuesday Familiar face returns to financier 6 morning. Go to DIESELTalk.co.nz New player for Auction market 8 3 6 to subscribe. GLOBAL VEHICLE LOGISTICS NZ · JAPAN · AUSTRALIA · UK · EUROPE FOUNDATION SPONSORS AutoTalk acknowledges the support of our foundation sponsors: Vehicle Inspection NZ WEEKLY PASSENGER & COMMERCIAL VEHICLE AUCTIONS 2 | AUTOTALK NOVEMBER 2015 | www.autotalk.co.nz NEWSTALK 2 Cheap to list? AutoTalk Magazine and autotalk.co.nz are published by Auto Media Group Cheap Cars has confirmed it will be self-funded,” he says. -

Brighter Sparks

ELECTRICS AND HYBRIDS Brighter sparks Hybrids, range extenders and full-electric vehicles are getting a lot of airtime and attracting significant R&D dollars. But are some developers missing an engineering trick? Brian Tinham reports ybrids, range extenders generator – strictly speaking, making it a Nikola One this vehicle also runs under (series hybrids that relinquish range-extender hybrid). electric power, in this case harnessing diesels as part of the Also in North America, Mack is a 120kW/1,800Nm electric motor and drivetrain), full electrics… working on a range extender drivetrain a reduction gearbox to drive the back The look and feel not only – in its case a Wrightspeed Route axle. However, its 66kWh battery pack is Hof commercial vehicle powertrains but 1000 hybrid powertrain in place of augmented by a 100bhp 1.6-litre Ford also of their energy storage and delivery the conventional MP7 11-litre diesel engine, which provides charging on the technologies, as well as their associated engine on its LR RCV (refuse collection move – so boosting its electric-only 100 ‘refuelling’ infrastructures, is on the move. vehicles) chassis. Drive is all electric, with mile range to circa 370. And it’s no longer just about buses Wrightspeed’s 80kW Fulcrum multi-fuel Critical to this innovative little truck’s and a few vans and lightweight chassis turbine generator and its 730kW KERS likely acceptance, however, is its PREMS cabs – the former driven by subsidies, delivering the recharge. (predictive range-extender management the latter riding on the coat-tails of Coming down the weight range, in system), which harnesses GPS to accelerating take-up in the automotive the UK there is Tevva Motors’ 7.5-tonne determine when to fire-up the diesel sector. -

Key Barriers Affecting E-Truck Adoption, Industry and Policy Implications, and Recommendations to Move the Market Forward

World Electric Vehicle Journal Vol. 8 - ISSN 2032-6653 - ©2016 WEVA Page WEVJ8-0657 EVS29 Symposium Montréal, Québec, Canada, June 19-22, 2016 2015 E-Truck Task Force: Key Barriers Affecting E-Truck Adoption, Industry and Policy Implications, and Recommendations to Move the Market Forward Tom Brotherton1, Alycia Gilde, Jasna Tomic 1CALSTART, 48 S Chester Ave, Pasadena, CA 91106, [email protected] Summary CALSTART’s E-Truck Task Force (ETTF) produced a report outlining the markets for electric drive trucks (E-Trucks), the prime barriers facing their success and provided key findings and recommendations to support expanding E-Truck adoption. Four key findings have been identified by the E-Truck Task Force as barriers currently affecting the growth and viability of E-Truck sales; 1) high incremental cost, 2) poor vehicle quality and support from supplier(s), 3) unexpected costs and energy planning with infrastructure, and 4) reduced operation in extreme climates. The E-Truck Task Force developed a set of action-oriented recommendations for overcoming each barrier. 1. E-Truck Task Force Background 1.1 Key Findings from 2012 E-TTF Report CALSTART’s E-Truck Task Force (E-TTF) was originally created in 2011 to help understand, support and expand the production and successful deployment and use of plug-in electric trucks and buses. CALSTART published E-Truck Task Force Findings and Recommendations in 2012 based on a year-long research and industry engagement process. In that report CALSTART outlined the best use profiles for successful E-Truck deployment, provided a business case calculator for fleets, highlighted early adopter user experience, developed an infrastructure planning guide, and then established industry recommendations of actions required to speed market success. -

Heavy-Duty Hybrid Vehicles – Technology Assessment

September 2, 2014 Sacramento, California 1 Background Technologies Evaluated Key Performance Parameters/Performance Goals Costs/Economics Conclusions Contacts 2 Heavy-duty Hybrids In California Today 3 Over 1,800 heavy duty hybrid vehicles in CA* Fuel Economy: Driver for hybrids Primarily Hybrid Electric Vehicles (HEV); More Recently Hydraulic Hybrid Vehicles (HHV) and Plug-in Hybrid Electric Vehicles (PHEV) Industry Manufacturers . Vehicle OEMs: Daimler, Freightliner, Hino, Kenworth, Mack, Volvo, Navistar, PACCAR, Peterbilt . Powertrain: Allison, Azure Dynamics, BAE, Eaton, Enova, Hino, Odyne, Parker Hannifin, Volvo Hybrid Technologies . Catalyst technology towards zero-emission HDVs . Improve technology/reduce costs . Market size/vehicle penetration . CO2 and NOx emissions/Certification *Data from HVIP and Transit Fleet Rule reporting database 4 Types of Hybrids, Common Elements 5 Mild Hybrid and Full Hybrid Series, Parallel & Series-Parallel Hybrids HEV HHV PHEV Micro-turbine Hybrids Catenary Hybrids 6 Mild Hybrid . Limited hybrid utilization . Engine start/stop . Regenerative braking Full Hybrid . More extensive integration . Electric motor used as tractive power source (full or partial) . Power vehicle electrical accessories . Larger battery packs . Engine start/stop . Regenerative braking 7 Both the internal combustion engine (ICE) and the electric motor have direct, independent connections to the transmission Either power source –or both together-can be used to turn the vehicle’s wheels Smaller battery pack -

04 EDF Green Roads Map Database

©2014 Environmental Defense Fund EDF Green Roads Map Database Updated: July 2014 COMPANY NAME WEBSITE CITY ZIP CODE COUNTY DESCRIPTION CATEGORY SENATE MEMBER ASSEMBLY MEMBER 44 Energy Consulting: Energy, transportation, and Technologies www.44energytech.com Oakland 94608 Alameda environmental technologies and strategies Energy Efficiency/Vehicles 09 - Hancock 15 - Skinner A-1 Alternative Fuels Development and Production: Alternative fuel Systems www.a1autoelectric/alternative-home Fresno 93271 Fresno conversions, storage and delivery systems Energy Efficiency/Vehicle 16 - Vidak 31 - Perea Sales and Mechanics: Electric vehicles and conversions, advanced technology lithium-ion AC Propulsion www.acpropulsion.com San Dimas 91773 Los Angeles battery packs Energy Efficiency/Vehicles 25 - Liu 41 - Holden AC Transit www.actransit.com Oakland 94612 Alameda Provider: Green Transportation Energy Efficiency/Vehicles 09 - Hancock 18 - Bonta Industry Support: Scientific innovation lifecycle Accelrys www.accelrys.com San Diego 92121 San Diego management software Education/Consulting 39 - Block 77 - Maienschien ACCU CHEM Conversion City of Industry 91746 Los Angeles Production: Biodiesel Fuels/Infrastructure 24 - Hernandez 57 - Calderon Research and Development: Engine, Combustion, Aftertreatment, and Alternative Fuels/Infrastructure; Achates Power www.achatespower.com San Diego 92121 San Diego Fuel Systems Energy Efficiency/Vehicles 39 - Block 77 - Maienschien Design and Manufacturing: Electric and plug-in Adomani www.adomanielectric.com Los Altos 94022 -

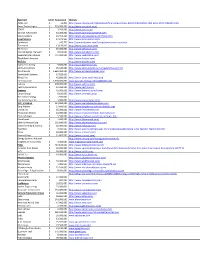

Applicant Amnt. Requested Website CVRD, LLC 12,800 $

Applicant Amnt. Requested Website CVRD, LLC $ 12,800 http://www.canada.com/nationalpost/financialpost/story.html?id=4165058b-c4c3-4264-9541-7eb61b75e652 Raser Technologies $ 520,000,000 http://www.rasertech.com/ STANT $ 3,750,000 http://www.stant.com/ Bannon Automotive $ 40,000,000 http://www.bannonautomotive.com/ Enova Systems $ 10,456,126 http://www.enovasystems.com/home.html Local Motors $ 24,341,500 http://www.local-motors.com/ Cordovano $ 345,777 http://stamford.patch.com/listings/cordovano-restoration Tinnerman $ 13,100,000 http://www.tinnerman.com/ T3 Motion $ 45,000,000 http://www.t3motion.com/ Environmental Transport $ 3,870,000 http://www.ecovelectric.com/ Severstal International $ 741,000,000 http://www.severstalna.com/ Think North America http://www.thinkev.com/ BioTrike http://www.biotrike.com/ Bailey Tool & Mfg $ 9,800,000 http://www.baileytool.com/ Johnson Controls $ 25,100,000 http://www.johnsoncontrols.com/publish/us/en.html Wind Works $ 1,680,000,000 http://www.windworkspower.com/ SmartEarth Systems $ 17,825,000 Wirco, Inc $ 40,800,000 http://www.wirco.com/index.php EV Innovations $ 1,300,000,000 www.youtube.com/watch?v=O8IGl7zezwU Valence $ 608,000,000 http://www.valence.com/ Vectrix Corporation $ 32,000,000 http://www.vectrix.com/ Brammo $ 45,000,000 http://www.brammo.com/home/ Carter Group $ 5,100,000 http://www.cartergroup.ca/ Bio-endocrenology $ 1,905,000 Key Safety Systems $ 3,900,000 http://www.keysafetyinc.com/ VVC, V-Vehicle $ 343,000,000 http://www.vvehiclelouisianajobs.com/ Borg Warner $ 27,600,000 http://www.borgwarner.com/en/default.aspx Limnia, Inc. -

Forex Creditors Urge SFO Investigation

THE TRUSTED VOICE OF THE AUTO INDUSTRY FOR MORE THAN 30 YEARS www.autofile.co.nz May 2017 Forex creditors urge Specialised training that’s SFO investigation proven to Creditors owed money from failed Forex Brokers Limited have increase profits walked away from their first meeting with liquidators still no wiser as to how Forex lost $16 million of their funds. ComCom utofile understands that creditors on the newly formed associated with Forex director warns a number of the 120-plus Forex creditors’ committee, says Russell Maher. But the properties, traders creditors hit by the Forex he wants to encourage everyone a family home in Auckland and an Acollapse are dealers operating in affected by the collapse of Forex investment property in Hasting, are p 6 the Hamilton region. to lodge a complaint with the held in trusts. One Hamilton dealer, who lost Serious Fraud Office. “There were no true answers $500,000 when Forex went into from the meeting. Do you keep liquidation on April 10, says the throwing money at it to pay the Remembering information they were given by “I didn’t learn liquidators?” Bob McMillan liquidators PKF Corporate Recovery anything new at the Darryn says he initially invested & Insolvency during the May 10 $300,000 on the foreign exchange meeting in Auckland was “pretty creditors meeting. with Forex during 2015. p 9 much what we have heard from the I don’t think we “We were sucked into that start. We are no better off”. are going to get thinking it was a good thing. We “There is no money.