Sierra Leone Integrated Resource Plan and Tariff Study PPA Energy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CDF Trial Transcript

Case No. SCSL-2004-14-T THE PROSECUTOR OF THE SPECIAL COURT V. SAM HINGA NORMAN MOININA FOFANA ALLIEU KONDEWA WEDNESDAY, 22 FEBRUARY 2006 9.40 A.M. TRIAL TRIAL CHAMBER I Before the Judges: Pierre Boutet, Presiding Bankole Thompson Benjamin Mutanga Itoe For Chambers: Ms Roza Salibekova Ms Anna Matas For the Registry: Mr Geoff Walker For the Prosecution: Mr Desmond De Silva Mr Kevin Tavener Mr Joseph Kamara Ms Bianca Suciu (Case Manager) For the Principal Defender: NO APPEARANCE For the accused Sam Hinga Dr Bu-Buakei Jabbi Norman: Mr Alusine Sesay Ms Claire da Silva (legal assistant) Mr Kingsley Belle (legal assistant) For the accused Moinina Fofana: Mr Arrow Bockarie Mr Andrew Ianuzzi For the accused Allieu Kondewa: Mr Ansu Lansana NORMAN ET AL Page 2 22 FEBRUARY 2006 OPEN SESSION 1 [CDF22FEB06A - CR] 2 Wednesday, 22 February 2006 3 [Open session] 4 [The accused present] 09:36:33 5 [Upon resuming at 9.40 a.m.] 6 WITNESS: LIEUTENANT GENERAL RICHARDS [Continued] 7 PRESIDING JUDGE: Good morning, Dr Jabbi. Good morning, 8 Mr Witness. Dr Jabbi, when we adjourned yesterday we were back 9 at you with re-examination, if any. You had indicated that you 09:40:46 10 did have some. 11 MR JABBI: Yes, My Lord. 12 PRESIDING JUDGE: Are you prepared to proceed now? 13 MR JABBI: Yes, My Lord. 14 PRESIDING JUDGE: Please do so. 09:40:59 15 RE-EXAMINED BY MR JABBI: 16 Q. Good morning, General. 17 A. Good morning. 18 Q. Just one or two points of clarification. -

Humanist Watch Salone (Huwasal) 2012 Annual Report

HUMANIST WATCH SALONE (HUWASAL) 2012 ANNUAL REPORT 29 HUMONYA AVENUE KENEMA CITY KENEMA DISTRICT EASTERN PROVINCE OF SIERRA LEONE Email: [email protected] Contact phone Number(s): +232779075/+23276582937. P O Box 102 Kenema 2012 Annual Report on Humanist Watch Salone Activities Page 1 TABLE OF CONTENT ACKONWLEDGEMENT INTRODUCTION AND BACKGROUND OF HUMANIST WATCH SALONE ACCOMPLISHMENT GENDER EQUITY AND WOMEN EMPOWERMENT CHILD PROTECTION PROGRAMME HEALTH HUMAN RIGHTS AND GOOD GOVERNANCE YOUTH EMPOWERMENT AFFLILIATION SOURCES OF FUNDING LESSONS LEARNT/OUTCOMES CONCLUSION 2012 Annual Report on Humanist Watch Salone Activities Page 2 ACKNOWLEDGEMENT We wish to extend thanks to our generous donor partners such as UNDP Access to Justice Programme, Amnesty International Sierra Leone, International Rescue Committee (IRC/GBV Programme), International Foundation for Election System (IFES) and Global Xchange/ VSO for both financial and technical support accorded to Humanist Watch Salone towards the implementation of its programme-projects in 2012. Moreover our sincere thanks and appreciation goes to our Advisory Board for providing support towards effective and efficient running of the day –to- day affairs of Humanist Watch Salone. Special and heartfelt thanks to our civil society partners and state actors and lastly, we extend a very big thanks to all our staff members for their restless effort behind the successes of our activities in 2012. 2012 Annual Report on Humanist Watch Salone Activities Page 3 Introduction and Background of Humanist Watch Salone Humanist Watch Salone (HUWASAL) is an indigenous human rights and development organization established in 2003 by a group of visionary and courageous human rights activists and development workers. The organization started as Community-Based organization and is now registered with Ministry of Finance and Economic Development (MoFED) as National Non- Governmental Organization. -

Sierra Leone

Language: English Original: English PROJECT: REHABILITATION OF BO-BANDAJUMA ROAD COUNTRY: SIERRA LEONE ENVIRONMENTAL AND SOCIAL IMPACT ASSESSMENT SUMMARY Date: August 2015 Team Leader: : A. Mwila, Transport Engineer, OITC.1 Team Members: A. Bockarie , Transport Engineer, OITC.1/SLFO J. Aguma. Transport Economist, OITC.1 F. Koroma, Financial Management Specialist, ORPF.2 A. Abdulai, Financial Management Specialist, ORPF.2 A Nabaloga, Social Development Specialist, Consultant, ONEC.3 M. Jambawai Social Expert, OSHD S. Momoh , Procurement Officer, ORPF.1 / SLFO P. Tambah,, Transport Engineer, OITC.1/LRFO Appraisal Team N. Omagor, Environmental Specialist, Consultant, OITC.1 Sector Manager: J. Kabanguka Country Manager: Y. Baldeh Sector Director: A. Oumarou Regional Director: A. Bernoussi 1 Project Title : Rehabilitation of Bo-Bandajuma Road Project Number : P-SL-DB0-010 Country : Sierra Leone Department : Transport & ICT Department (OITC) Division : OITC.1 1. Introduction The project involves the update of feasibility studies of the road from Bo to Bandajuma in the southeast of Sierra Leone, which is part of the Freetown-Monrovia Trans-West African Coastal Highway. The rehabilitation of Bo-Bandajuma road will involve overlaying Asphalt Concrete on the existing carriage way without major realignments. However, in most trading centers, roadside businesses have encroached on the carriageway which has triggered the need for resettlement and compensation. On the state of the road, it be briefly noted that, from the Bo towards Bandajuma and for its first 3.5km, the road deterioration has ranged from loss of paved surfaces, to development of gaping pot holes, stretches of mudflats and some impassable sections. The main areas of deterioration are within 15 km from Bo with a worst portion with glaring potholes at 24+000km. -

G U I N E a Liberia Sierra Leone

The boundaries and names shown and the designations Mamou used on this map do not imply official endorsement or er acceptance by the United Nations. Nig K o L le n o G UINEA t l e a SIERRA Kindia LEONEFaranah Médina Dula Falaba Tabili ba o s a g Dubréka K n ie c o r M Musaia Gberia a c S Fotombu Coyah Bafodia t a e r G Kabala Banian Konta Fandié Kamakwie Koinadugu Bendugu Forécariah li Kukuna Kamalu Fadugu Se Bagbe r Madina e Bambaya g Jct. i ies NORTHERN N arc Sc Kurubonla e Karina tl it Mateboi Alikalia L Yombiro Kambia M Pendembu Bumbuna Batkanu a Bendugu b Rokupr o l e Binkolo M Mange Gbinti e Kortimaw Is. Kayima l Mambolo Makeni i Bendou Bodou Port Loko Magburaka Tefeya Yomadu Lunsar Koidu-Sefadu li Masingbi Koundou e a Lungi Pepel S n Int'l Airport or a Matotoka Yengema R el p ok m Freetown a Njaiama Ferry Masiaka Mile 91 P Njaiama- Wellington a Yele Sewafe Tongo Gandorhun o Hastings Yonibana Tungie M Koindu WESTERN Songo Bradford EAS T E R N AREA Waterloo Mongeri York Rotifunk Falla Bomi Kailahun Buedu a i Panguma Moyamba a Taiama Manowa Giehun Bauya T Boajibu Njala Dambara Pendembu Yawri Bendu Banana Is. Bay Mano Lago Bo Segbwema Daru Shenge Sembehun SOUTHE R N Gerihun Plantain Is. Sieromco Mokanje Kenema Tikonko Bumpe a Blama Gbangbatok Sew Tokpombu ro Kpetewoma o Sh Koribundu M erb Nitti ro River a o i Turtle Is. o M h Sumbuya a Sherbro I. -

U N I T E D N a T I O

U N I T E D N A T I O N S Office for the Coordination of Humanitarian Affairs SIERRA LEONE HUMANITARIAN SITUATION REPORT SEPTEMBER 2003 KEY EVENTS district. A concern raised in Kono is that none of the Watsan implementing partners had the facilities or machines for testing water • Yellow Fever outbreak samples. This has been reported to the MOHS. • Security Council extends UNAMSIL’s mandate • UN Agencies and GoSL celebrate World Peace Day SECURITY HIGHLIGHTS • Nigerian lawmakers call on UNAMSIL Overall security UNAMSIL (United Nations Mission in Sierra Leone) reports the overall security situation in HUMANITARIAN HIGHLIGHTS the country to be calm. However there have been some concerns about security along the Yellow Fever outbreak border regions, particularly along the Mano The Ministry of Health and Sanitation (MOHS) River Union Bridge in the south. Similarly the has reported a total of 90 cases of Yellow Sierra Leone Police (SLP) are concerned Fever, from eight districts in the country: about the porous nature of the border in the Tonkolili, Bombali, Kenema, Koinadugu, Port Kamakwie, Tambakha and Koinadugu areas, Loko, Kambia and Kono. Of the 90 reported in the Northern Province that have resulted in cases (as of 29 September) four laboratory increased smuggling of goods across the cases were confirmed, all from the Tonkolili borders. The police have also reported hunters District, where majority of the suspected cases from Guinea, coming across, poaching and emanate from. Earlier, the MOHS gave out crossing back into Guinea. 100,000 doses of vaccine in four chiefdoms in the district. They have now finally secured UNAMSIL’s mandate extended funds to carry out mass immunization The UN Security Council has extended campaign in the remaining seven chiefdoms of UNAMSIL’s mandate, which was to expire on the district. -

Sierra Leone Liberia Guinea

A B C D E F G H I J K L M N O Ebola Virus Disease (EVD) Outbreak in West Africa 1 1 SENEGAL Youkounkoun Koundara 2 2 GUINEA- Mali LABE BISSAU 3 3 Gaoual BOKE Koubia Tougue Siguiri Labé Dinguiraye MALI 4 4 Pita Boke GUINEA Port Boké Télimélé Victoria Port KINDIA Dabola 5 Kouroussa 5 Port Dalaba Mandiana MAMOU Kamsar FARANAH KANKAN "L Port Kankan Mamou Fria Boffa 6 6 Faranah "E Kindia Bindi Gberia Fotombu Dubréka Dubreka Coyah Tokonou Port "E L " L " Kabala 7 L 7 " CONAKRY"EL L" ""L Kamakwie CONAKRY ""LE E ConakryL " " Port "L Forécariah NORTHERN Kérouané "EBenty Kissidougou Alikalia Port Kambia L " 8 Seidu 8 Bumbuna E Binkolo " Mambolo "L "E Port Makeni Loko Peyima Beyla "LE"E E ""E L " "E " Tefeya Magburaka Lungi Pepel Lunsar Rokupr "ESefadu Ndoyogbo Guékédou Simbakoro L Port " L"E E ""L " Freetown Pepel "LMacenta 9 Koidu 9 Port L Yele "E""E Yonibana Voinjama"E L"L Goderich"E"L -

Sierra Leone

Sierra Leone A TAG LANCE Main Objectives and Activities Assess the protection requirements of those Liberian refugees who did not wish to repatriate; facilitate the local integration of Liberian refugees in need of international protection and identify resettle- ment opportunities; assess how national and local socio-economic, political and security factors will affect the needs of Sierra Leonean returnees; compile Returnee District Area Profiles taking into account the security needs of potential returnees to those dis- Persons of Concern tricts; facilitate and later promote Main Refugee Total Of whom Per cent Per cent Origin/Type of in UNHCR Female under 18 the voluntary repatriation of Sierra Population Country assisted Leonean refugees and help them Sierra Leone (IDPs) 300,000 - - - settle back into their communities Sierra Leone 200,000 - - - of origin; in the context of the (Returned IDPs) Brookings process, establish opera- Sierra Leone 40,900 24,900 - - tional linkages and mechanisms (Returnees) which best ensure a smooth transi- Liberia (Refugees) 6,500 6,500 - - tion from emergency relief to longer-term reconstruction and recovery. Income and Expenditure (USD) Annual Programme, Trust Funds and Supplementary Programme Budgets Impact Revised Income Other Total Total • In 2000, UNHCR undertook Budget from Funds Funds Expenditure Contributions1 Available2 Available screening of 1,872 Liberian AB/TF 941,439 879,376 431,354 1,310,730 832,471 households including new appli- SB 9,380,111 3,966,962 2,697,173 6,664,135 6,664,135 cations, in order to determine the Total 10,321,550 4,846,338 3,128,527 7,974,865 7,496,606 need of those who did not partic- 1Includes income from contributions earmarked at the country level. -

MA026 Telecoms District DDP

""Y MA026_Pujehun, Southern Province Febena Naiagolehun Faima Kamasu GUINEA Jaiama Mofuwe Bongor Madinawo Dama Masam Langrama Sumbuya Yameama Wonde NORTHERN Gamayama Jowi Gaura Lugbu Bathurst Niawa Gandorhun Mani Town EASTERN Jimi Vawahun Sierra Leone: Ebola Bo BANDAJUMASEWA Koiva Kpanda Y Kpejewa Bogboabu Outbreak - GSM SOUTHERN Bagbo Njala "" Kemo Momajo Tuala Gegbwema Bandajuma Koya Mobile Phone Network Gondama LIBERIA Mano Foutah Kobeibu Coverage in Ngaiagoehun Pejeh(Futa Baoma Fula peje Momajo Sowa Felegoma EASTERN Gambia Pujehun, Southern Mogbavai Gbongay Kundorwahun POTORU_II Kenema Malen Province N ' Potoru 0 "Y 3 " ° Map shows the GSM mobile phone 7 Tunkia network coverage for districts in Sierra Kongohun Dandabu Leone, based on data received from Gorahun the ETC. This is a combined coverage Barri map for all networks operating in the Boumu Bum Saba country. Panga Samba Note that no data was received for 3G Kabonde coverage in Sierra Leone. Bonthe Combined GSM Mobile Phone Bandajuma Network Coverage Pujehun ""YYonni Blama (October 2014) Massaquoi PUJEHUN_II Galliness Perri Y Kongo "" Africell Tower Location Gbondapi Fuhiko ZIMMI_II Zimmi 2,000 Gbongeh Pujehun Movugba Fonima ""Y Elevation Makpele Borders Panga (metres) National Kwamebai krim 0 Krim Settlement Province Capital District Chiefdom Hoya City Yakemu Town Coastline Mesima Kpukumu Baryeh SOUTHERN village River Physical Roads Lake Primary Mono Kpaka Transport Secondary Sakrim o Airport Tertiary ⛡ Port Soro 0 5 10 15 Gbema Fairo km LIBERIA Data sources OpenStreetMap, Steward Project, COD-FOD Registry, Logistics Cluster, ETC, Africell Created 2 Nov 2014 / 18:00 UTC±00:00 Semabu Map Document MA026_Telecoms_District Town Projection / Datum WGS 1984 UTM Zone 29N Bo N ° Glide Number EP-2014-000039-SLE 7 Produced by MapAction Supported by www.mapaction.org Sullima [email protected] The depiction and use of boundaries, names and associated data shown here do not imply endorsement or ´ acceptance by MapAction. -

Summary of Recovery Requirements (Us$)

National Recovery Strategy Sierra Leone 2002 - 2003 EXECUTIVE SUMMARY TABLE OF CONTENTS EXECUTIVE SUMMARY 3 4. RESTORATION OF THE ECONOMY 48 INFORMATION SHEET 7 MAPS 8 Agriculture and Food-Security 49 Mining 53 INTRODUCTION 9 Infrastructure 54 Monitoring and Coordination 10 Micro-Finance 57 I. RECOVERY POLICY III. DISTRICT INFORMATION 1. COMPONENTS OF RECOVERY 12 EASTERN REGION 60 Government 12 1. Kailahun 60 Civil Society 12 2. Kenema 63 Economy & Infrastructure 13 3. Kono 66 2. CROSS CUTTING ISSUES 14 NORTHERN REGION 69 HIV/AIDS and Preventive Health 14 4. Bombali 69 Youth 14 5. Kambia 72 Gender 15 6. Koinadugu 75 Environment 16 7. Port Loko 78 8. Tonkolili 81 II. PRIORITY AREAS OF SOUTHERN REGION 84 INTERVENTION 9. Bo 84 10. Bonthe 87 11. Moyamba 90 1. CONSOLIDATION OF STATE AUTHORITY 18 12. Pujehun 93 District Administration 18 District/Local Councils 19 WESTERN AREA 96 Sierra Leone Police 20 Courts 21 Prisons 22 IV. FINANCIAL REQUIREMENTS Native Administration 23 2. REBUILDING COMMUNITIES 25 SUMMARY OF RECOVERY REQUIREMENTS Resettlement of IDPs & Refugees 26 CONSOLIDATION OF STATE AUTHORITY Reintegration of Ex-Combatants 38 REBUILDING COMMUNITIES Health 31 Water and Sanitation 34 PEACE-BUILDING AND HUMAN RIGHTS Education 36 RESTORATION OF THE ECONOMY Child Protection & Social Services 40 Shelter 43 V. ANNEXES 3. PEACE-BUILDING AND HUMAN RIGHTS 46 GLOSSARY NATIONAL RECOVERY STRATEGY - 3 - EXECUTIVE SUMMARY ▪ Deployment of remaining district officials, EXECUTIVE SUMMARY including representatives of line ministries to all With Sierra Leone’s destructive eleven-year conflict districts (by March). formally declared over in January 2002, the country is ▪ Elections of District Councils completed and at last beginning the task of reconstruction, elected District Councils established (by June). -

Sierraleone Local Council Ward Boundary Delimitation Report

NATIONAL ELECTORAL COMMISSION Sierra Leone Local Council Ward Boundary Delimitation Report Volume Two Meets and Bounds April 2008 Table of Contents Preface ii A. Eastern region 1. Kailahun District Council 1 2. Kenema City Council 9 3. Kenema District Council 12 4. Koidu/New Sembehun City Council 22 5. Kono District Council 26 B. Northern Region 1. Makeni City Council 34 2. Bombali District Council 37 3. Kambia District Council 45 4. Koinadugu District Council 51 5. Port Loko District Council 57 6. Tonkolili District Council 66 C. Southern Region 1. Bo City Council 72 2. Bo District Council 75 3. Bonthe Municipal Council 80 4. Bonthe District Council 82 5. Moyamba District Council 86 6. Pujehun District Council 92 D. Western Region 1. Western Area Rural District Council 97 2. Freetown City Council 105 i Preface This part of the report on Electoral Ward Boundaries Delimitation process is a detailed description of each of the 394 Local Council Wards nationwide, comprising of Chiefdoms, Sections, Streets and other prominent features defining ward boundaries. It is the aspect that deals with the legal framework for the approved wards _____________________________ Dr. Christiana A. M Thorpe Chief Electoral Commissioner and Chair ii CONSTITUTIONAL INSTRUMENT No………………………..of 2008 Published: THE LOCAL GOVERNMENT ACT, 2004 (Act No. 1 of 2004) THE KAILAHUN DISTRICT COUNCIL (ESTABLISHMENT OF LOCALITY AND DELIMITATION OF WARDS) Order, 2008 Short title In exercise of the powers conferred upon him by subsection (2) of Section 2 of the Local Government Act, 2004, the President, acting on the recommendation of the Minister of Internal Affairs, Local Government and Rural Development, the Minister of Finance and Economic Development and the National Electoral Commission, hereby makes the following Order:‐ 1. -

From Emergency Evacuation to Community Empowerment Review

UNITED NATIONS HIGH COMMISSIONER FOR REFUGEES EVALUATION AND POLICY ANALYSIS UNIT From emergency evacuation to community empowerment Review of the repatriation and reintegration programme in Sierra Leone By Stefan Sperl and EPAU/2005/01 Machtelt De Vriese February 2005 Evaluation and Policy Analysis Unit UNHCR’s Evaluation and Policy Analysis Unit (EPAU) is committed to the systematic examination and assessment of UNHCR policies, programmes, projects and practices. EPAU also promotes rigorous research on issues related to the work of UNHCR and encourages an active exchange of ideas and information between humanitarian practitioners, policymakers and the research community. All of these activities are undertaken with the purpose of strengthening UNHCR’s operational effectiveness, thereby enhancing the organization’s capacity to fulfil its mandate on behalf of refugees and other displaced people. The work of the unit is guided by the principles of transparency, independence, consultation, relevance and integrity. Evaluation and Policy Analysis Unit United Nations High Commissioner for Refugees Case Postale 2500 1211 Geneva 2 Switzerland Tel: (41 22) 739 8249 Fax: (41 22) 739 7344 e-mail: [email protected] internet: www.unhcr.org/epau All EPAU evaluation reports are placed in the public domain. Electronic versions are posted on the UNHCR website and hard copies can be obtained by contacting EPAU. They may be quoted, cited and copied, provided that the source is acknowledged. The views expressed in EPAU publications are not necessarily those of UNHCR. The designations and maps used do not imply the expression of any opinion or recognition on the part of UNHCR concerning the legal status of a territory or of its authorities. -

Emis Code Council Chiefdom Ward Location School Name

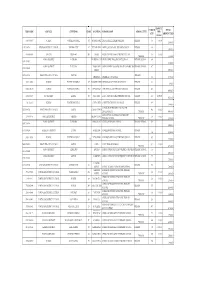

AMOUNT ENROLM TOTAL EMIS CODE COUNCIL CHIEFDOM WARD LOCATION SCHOOL NAME SCHOOL LEVEL PER ENT AMOUNT PAID CHILD 5103-2-09037 WARDC WATERLOO RURAL 391 ROGBANGBA ABDUL JALIL ACADEMY PRIMARY PRIMARY 369 10,000 3,690,000 1291-2-00714 KENEMA DISTRICT COUNCIL KENEMA CITY 67 FULAWAHUN ABDUL JALIL ISLAMIC PRIMARY SCHOOL PRIMARY 380 3,800,000 4114-2-06856 BO CITY TIKONKO 289 SAMIE ABDUL TAWAB HAIKAL PRIMARY SCHOOL 610 10,000 PRIMARY 6,100,000 KONO DISTRICT TANKORO DOWN BALLOP ABDULAI IBN ABASS PRIMARY SCHOOL PRIMARY SCHOOL 694 1391-2-02007 6,940,000 KONO DISTRICT TANKORO TAMBA ABU ABDULAI IBNU MASSOUD ANSARUL ISLAMIC MISPRIMARY SCHOOL 407 1391-2-02009 STREET 4,070,000 5208-2-10866 FREETOWN CITY COUNCIL WEST III PRIMARY ABERDEEN ABERDEEN MUNICIPAL 366 3,660,000 5103-2-09002 WARDC WATERLOO RURAL 397 KOSSOH TOWN ABIDING GRACE PRIMARY SCHOOL PRIMARY 62 620,000 5103-2-08963 WARDC WATERLOO RURAL 373 BENGUEMA ABNAWEE ISLAMIC PRIMARY SCHOOOL PRIMARY 405 4,050,000 4109-2-06695 BO DISTRICT KAKUA 303 KPETEMA ACEF / MOUNT HORED PRIMARY SCHOOL PRIMARY 411 10,000.00 4,110,000 Not found WARDC WATERLOO RURAL COLE TOWN ACHIEVERS PRIMARY TUTORAGE PRIMARY 388 3,880,000 ACTION FOR CHILDREN AND YOUTH 5205-2-09766 FREETOWN CITY COUNCIL EAST III CALABA TOWN 460 10,000 DEVELOPMENT PRIMARY 4,600,000 ADA GORVIE MEMORIAL PREPARATORY 320401214 BONTHE DISTRICT IMPERRI MORIBA TOWN 320 10,000 PRIMARY SCHOOL PRIMARY 3,200,000 KONO DISTRICT TANKORO BONGALOW ADULLAM PRIMARY SCHOOL PRIMARY SCHOOL 323 1391-2-01954 3,230,000 1109-2-00266 KAILAHUN DISTRICT LUAWA KAILAHUN ADULLAM PRIMARY