Flemish Broadcasting VRT with External Parties to Produce

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIVA - a Software Live Video & Audio Production Framework Team’S Presentation

Presentation of the Stars4Media Initiative: LIVA - a software live video & audio production framework Team’s presentation Video Snackbar Hub: exchanging knowledge on new technologies, ideas and workflows to support content creators and part of the Future Media Hubs. An international network of media companies that strengthen each other and collaborate on innovative and/or strategic topics. Chosen representatives for the Stars4Media-project were: ● Morten Brandstrup, Head of news technology – TV2 Denmark ● Hugo Ortiz, IP Broadcast Coach – RTBF ● Floris Daelemans, Innovation Researcher – VRT ● Henrik Vandeput, Software developer (freelancer) – VRT ● Sarah Geeroms, Strategic partnerships and Head of FMH – VRT ● Coralie Villeret, Software engineer and UX designer – RTBF [email protected] Initiative’s summary ● To explore the boundaries of standard broadcast technology ● Building custom components in a creative software (TouchDesigner) ● Exploring the significant profit of a new workflow (both financially and creatively) ● Learning some interesting insights and different approaches from junior profiles ● Expanding our skill-sets https://www.videosnackbarhub.com [email protected] Initiative’s results ● Added experience to the junior profiles within our media organizations ● Resourced our community of like-minded media players ● Resulting components with lots of possibilities ● Helped us explore Github and TouchDesigner in-depth ● Applied new and creative software to our broadcast ● Received constructive feedback from our international -

European Public Service Broadcasting Online

UNIVERSITY OF HELSINKI, COMMUNICATIONS RESEARCH CENTRE (CRC) European Public Service Broadcasting Online Services and Regulation JockumHildén,M.Soc.Sci. 30November2013 ThisstudyiscommissionedbytheFinnishBroadcastingCompanyǡYle.Theresearch wascarriedoutfromAugusttoNovember2013. Table of Contents PublicServiceBroadcasters.......................................................................................1 ListofAbbreviations.....................................................................................................3 Foreword..........................................................................................................................4 Executivesummary.......................................................................................................5 ͳIntroduction...............................................................................................................11 ʹPre-evaluationofnewservices.............................................................................15 2.1TheCommission’sexantetest...................................................................................16 2.2Legalbasisofthepublicvaluetest...........................................................................18 2.3Institutionalresponsibility.........................................................................................24 2.4Themarketimpactassessment.................................................................................31 2.5Thequestionofnewservices.....................................................................................36 -

Minority-Language Related Broadcasting and Legislation in the OSCE

University of Pennsylvania ScholarlyCommons Other Publications from the Center for Global Center for Global Communication Studies Communication Studies (CGCS) 4-2003 Minority-Language Related Broadcasting and Legislation in the OSCE Tarlach McGonagle Bethany Davis Noll Monroe Price University of Pennsylvania, [email protected] Follow this and additional works at: https://repository.upenn.edu/cgcs_publications Part of the Critical and Cultural Studies Commons Recommended Citation McGonagle, Tarlach; Davis Noll, Bethany; and Price, Monroe. (2003). Minority-Language Related Broadcasting and Legislation in the OSCE. Other Publications from the Center for Global Communication Studies. Retrieved from https://repository.upenn.edu/cgcs_publications/3 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/cgcs_publications/3 For more information, please contact [email protected]. Minority-Language Related Broadcasting and Legislation in the OSCE Abstract There are a large number of language-related regulations (both prescriptive and proscriptive) that affect the shape of the broadcasting media and therefore have an impact on the life of persons belonging to minorities. Of course, language has been and remains an important instrument in State-building and maintenance. In this context, requirements have also been put in place to accommodate national minorities. In some settings, there is legislation to assure availability of programming in minority languages.1 Language rules have also been manipulated for restrictive, sometimes punitive ends. A language can become or be made a focus of loyalty for a minority community that thinks itself suppressed, persecuted, or subjected to discrimination. Regulations relating to broadcasting may make language a target for attack or suppression if the authorities associate it with what they consider a disaffected or secessionist group or even just a culturally inferior one. -

List of Public Broadcasting Decisions

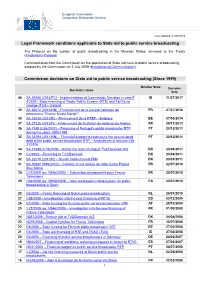

European Commission Competition Directorate-General Last updated: 01/07/2019 Legal Framework conditions applicable to State aid to public service broadcasting The Protocol on the system of public broadcasting in the Member States, annexed to the Treaty (Amsterdam Protocol). Communication from the Commission on the application of State aid rules to public service broadcasting, adopted by the Commission on 2 July 2009 (Broadcasting Communication). Commission decisions on State aid to public service broadcasting (Since 1999) Member State Decision Decision name date 40 SA.39346 (2014/FC) - Implementation of Commission Decision in case E IE 11/07/2017 4/2005 - State financing of Radio Teilifís Éireann (RTÉ) and Teilifís na Gaeilge (TG4) - Ireland 39 SA.36672 (2013/NN) - Financement de la société nationale de FR 27/07/2016 programme "France Media Monde" 38 SA.32635 (2012/E) – Financement de la RTBF – Belgique BE 07/05/2014 37 SA.37136 (2013/N) - Financement de la station de radio locale France FR 08/11/2013 36 SA.7149 (C85/2001) – Financing of Portugal's public broadcaster RTP PT 20/12/2011 during the years 1992-1998 35 SA.33294 (2011/NN) – Financial support to restructure the accumulated PT 20/12/2011 debt of the public service broadcaster RTP – Amendment of decision NN 31/2006 34 SA.27688 (C19/2009) - Aid for the restructuring of TV2/Danmark A/S DK 20/04/2011 33 C2/2003 – Financing of TV2/Danmark DK 20/04/2011 32 SA.32019 (2010/N) – Danish radio channel FM4 DK 23/03/2011 31 SA.30587 (N95/2010) – Création d’une station de radio locale France FR 22/07/2010 Bleu Maine 30 C27/2009 (ex. -

Ibc Accelerators

www.ibc.org IBC ACCELERATORS Supporting collaborative innovation across the Media Entertainment Ecosystem May 2021 W: show.ibc.org/accelerators E: [email protected] About IBC § IBC is an independent and authoritative international organisation serving the global Media, Entertainment & Technology industry. § For over 50 years IBC has run the world’s biggest, most influential annual event for the industry. § It is simply the must-attend event in the Media, Entertainment and Technology industry’s calendar! § IBC’s event in Amsterdam attracts more than 56,000+ attendees from 150 countries around the world, 1,700 exhibitors - the world’s key technology suppliers and has a thought-leading conference at the core § 6 leading international bodies form the ownership behind IBC, representing both Exhibitors and Visitors, these include IEEE, IABM, IET, RTS, SCTE and SMPTE 2 The Accelerator Framework for Media & Entertainment Innovation IBC created the Accelerator programme in 2019, to support the media & entertainment technology sector with a framework for agile, collaborative and fast-track innovation. The programme is designed to address a wide range of business and technology challenges disrupting the sector, for example… § Transition to software and IP across the content supply chain § Rapid evolution of new technologies e.g. AI, Voice, IoT, Cloud etc. § Potential for immersive & experiential tech e.g. VR/AR/ XR, 8K etc § Onset of 5G and a vast array of new creative, production & distribution opportunities § A boom in direct to consumer platform plays and an original content § Regulatory disparity with online platforms and the value of trust § Fragmenting audiences across platforms, screens and devices § Accelerated remote & distributed production strategies The IBC Accelerators take on ’bite size’ challenges in a project based, multi-company approach, developing innovative solutions to common pain points, with invaluable ‘hands on’ experimentation. -

The Value of Public Service Media

The Value of Public Service Media T he worth of public service media is under increasing scrutiny in the 21st century as governments consider whether the institution is a good investment and a fair player in media markets. Mandated to provide universally accessible services and to cater for groups that are not commercially attractive, the institution often con- fronts conflicting demands. It must evidence its economic value, a concept defined by commercial logic, while delivering social value in fulfilling its largely not-for-profit public service mission and functions. Dual expectations create significant complex- The Value of ity for measuring PSM’s overall ‘public value’, a controversial policy concept that provided the theme for the RIPE@2012 conference, which took place in Sydney, Australia. This book, the sixth in the series of RIPE Readers on PSM published by NORDI- Public Service Media COM, is the culmination of robust discourse during that event and the distillation of its scholarly outcomes. Chapters are based on top tier contributions that have been revised, expanded and subject to peer review (double-blind). The collection investi- gates diverse conceptions of public service value in media, keyed to distinctions in Gregory Ferrell Lowe & Fiona Martin (eds.) the values and ideals that legitimate the public service enterprise in media in many countries. Fiona Martin (eds.) Gregory Ferrell Lowe & RIPE 2013 University of Gothenburg Box 713, SE 405 30 Göteborg, Sweden Telephone +46 31 786 00 00 (op.) Fax +46 31 786 46 55 E-mail: -

Must-Carry Rules, and Access to Free-DTT

Access to TV platforms: must-carry rules, and access to free-DTT European Audiovisual Observatory for the European Commission - DG COMM Deirdre Kevin and Agnes Schneeberger European Audiovisual Observatory December 2015 1 | Page Table of Contents Introduction and context of study 7 Executive Summary 9 1 Must-carry 14 1.1 Universal Services Directive 14 1.2 Platforms referred to in must-carry rules 16 1.3 Must-carry channels and services 19 1.4 Other content access rules 28 1.5 Issues of cost in relation to must-carry 30 2 Digital Terrestrial Television 34 2.1 DTT licensing and obstacles to access 34 2.2 Public service broadcasters MUXs 37 2.3 Must-carry rules and digital terrestrial television 37 2.4 DTT across Europe 38 2.5 Channels on Free DTT services 45 Recent legal developments 50 Country Reports 52 3 AL - ALBANIA 53 3.1 Must-carry rules 53 3.2 Other access rules 54 3.3 DTT networks and platform operators 54 3.4 Summary and conclusion 54 4 AT – AUSTRIA 55 4.1 Must-carry rules 55 4.2 Other access rules 58 4.3 Access to free DTT 59 4.4 Conclusion and summary 60 5 BA – BOSNIA AND HERZEGOVINA 61 5.1 Must-carry rules 61 5.2 Other access rules 62 5.3 DTT development 62 5.4 Summary and conclusion 62 6 BE – BELGIUM 63 6.1 Must-carry rules 63 6.2 Other access rules 70 6.3 Access to free DTT 72 6.4 Conclusion and summary 73 7 BG – BULGARIA 75 2 | Page 7.1 Must-carry rules 75 7.2 Must offer 75 7.3 Access to free DTT 76 7.4 Summary and conclusion 76 8 CH – SWITZERLAND 77 8.1 Must-carry rules 77 8.2 Other access rules 79 8.3 Access to free DTT -

As of August 27Th COUNTRY COMPANY JOB TITLE

As of August 27th COUNTRY COMPANY JOB TITLE AFGHANISTAN MOBY GROUP Director, channels/acquisitions ALBANIA TVKLAN SH.A Head of Programming & Acq. AUSTRALIA AUSTRALIAN BROADCASTING CORPORATION Acquisitions manager AUSTRALIA FOXTEL Acquisitions executive AUSTRALIA SBS Head of Network Programming AUSTRALIA SBS Channel Manager Main Channel AUSTRALIA SBS Head of Unscripted AUSTRALIA SBS Australia Channel Manager, SBS Food AUSTRALIA SBS Television International Content Consultant AUSTRALIA Special Broadcast Service Director TV and Online Content AUSTRALIA SPECIAL BROADCASTING SERVICE CORPORATION Acquisitions manager (unscripted) AUSTRIA A1 TELEKOM AUSTRIA AG Head of Broadcast & SAT AUSTRIA A1 TELEKOM AUSTRIA AG Broadcast & SAT AZERBAIJAN PUBLIC TELEVISION & RADIO BROADCASTING AZERBAIJAN Director general COMPANY AZERBAIJAN PUBLIC TELEVISION & RADIO BROADCASTING AZERBAIJAN Head of IR COMPANY AZERBAIJAN PUBLIC TELEVISION & RADIO BROADCASTING AZERBAIJAN Deputy DG COMPANY AZERBAIJAN GAMETV.AZ PRODUCER CENTRE General director BELARUS MEDIA CONTACT Buyer BELARUS MEDIA CONTACT Ceo BELGIUM NOA PRODUCTIONS Ceo ‐ producer BELGIUM PANENKA NV Managing partner RTBF RADIO TELEVISION BELGE COMMUNAUTE BELGIUM Head of Acquisition Documentary FRANCAISE RTBF RADIO TELEVISION BELGE COMMUNAUTE BELGIUM Responsable Achats Programmes de Flux FRANCAISE RTBF RADIO TELEVISION BELGE COMMUNAUTE BELGIUM Buyer FRANCAISE RTBF RADIO TELEVISION BELGE COMMUNAUTE BELGIUM Head of Documentary Department FRANCAISE RTBF RADIO TELEVISION BELGE COMMUNAUTE BELGIUM Content acquisition -

Selection Spring/Summer 2018 Ars E Y

ars e y 25 Selection Spring/Summer 2018 ars e y Selection Spring/Summer 2018 25 .. 2 .. ars e y Selection Spring/Summer 2018 25 Highlight — Preschool KiKANiNCHEN Animation 26 x 1’ + 10 x 3’ Preschool Rating hit KiKANiNCHEN is a successful, multimedia preschool programme on KiKA, the public service children’s channel run by ARD / ZDF in Germany. It is tailored to the development and needs of our youngest newcomers to media. The darling of every child is Kikaninchen, an animated 3D figure that accompanies the children throughout the program. Its grown-up friends Anni, Christian and Jule, who have great ideas, know stories and provide motivation, are always by the rabbit’s side. The popular bite-sized adventures and stories have been specifically developed for children aged between three and six, and take place in a 2D world of paper snippets. These appealing aesthetics for children as well as the catchy songs provide a high level of audiovisual recognition value. KiKANiNCHEN is a trusted brand and also well-known for outstanding merchandising products in Germany. As seen on: KiKA Produced by: Studio.TV.Film Web: www.kikaninchen.de Preschool School of Roars Animation 52 x 7’ Preschool Rating hit Multiple language versions available School of Roars … Where monsters go to growl and grow! Going to school for the first time is one of the biggest things you’ll do in your life. You’re away from home, fitting in with routines and learning so many new things … whilst also getting along with a class full of new friends. -

VRT and RTBF Host PBI Virtual CEO Meeting

VRT and RTBF host PBI Virtual CEO meeting In a different world, this week Brussels would be hosting the annual Public Broadcasters International media conference. Unfortunately, due to the corona pandemic that event has been postponed for a year. However, broadcasters VRT and RTBF have come up with a plan that allows everyone to get together now by arranging an interim, online round table discussion on Tuesday afternoon. At the head of that table are hosts VRT CEO Frederik Delaplace and RTBF Jean-Paul Philippot. How does it feel for the VRT CEO to be sitting on the other side of the table for once, and asking the questions himself? “Quite pleasant”, he laughs. “This is the first time I will be meeting my international colleagues. But it is also a pity we have to organise it in this way. We don’t have a choice of course, but I would have preferred to let it take place here physically. Soon I will be dealing with an agenda item about cooperation, which is something I find extremely important for the future. And I'm not just talking about the public broadcasters. Our real competitors are not called DPG Media or Mediahuis. They are called Google, Facebook and WeChat. We will have to join forces, just think of what Scandinavia is already doing in the field of fiction. This is an example we will soon be following in a co-production with Germany.” What is taking place today is also a good example. VRT and RTBF are joining forces. “In recent months, the strong bond between the public media and the public has become more apparent,” said Jean-Paul Philippot, CEO of RTBF. -

Confirmed 2021 Buyers / Commissioners

As of April 13th Doc & Drama Kids Non‐Scripted COUNTRY COMPANY NAME JOB TITLE Factual Scripted formats content formats ALBANIA TVKLAN SH.A Head of Programming & Acq. X ARGENTINA AMERICA VIDEO FILMS SA CEO XX ARGENTINA AMERICA VIDEO FILMS SA Acquisition ARGENTINA QUBIT TV Acquisition & Content Manager ARGENTINA AMERICA VIDEO FILMS SA Advisor X SPECIAL BROADCASTING SERVICE AUSTRALIA International Content Consultant X CORPORATION Director of Television and Video‐on‐ AUSTRALIA ABC COMMERCIAL XX Demand SAMSUNG ELECTRONICS AUSTRALIA Head of Business Development XXXX AUSTRALIA SPECIAL BROADCASTING SERVICE AUSTRALIA Acquisitions Manager (Unscripted) X CORPORATION SPECIAL BROADCASTING SERVICE Head of Network Programming, TV & AUSTRALIA X CORPORATION Online Content AUSTRALIA ABC COMMERCIAL Senior Acquisitions Manager Fiction X AUSTRALIA MADMAN ENTERTAINMENT Film Label Manager XX AUSTRIA ORF ENTERPRISE GMBH & CO KG content buyer for Dok1 X Program Development & Quality AUSTRIA ORF ENTERPRISE GMBH & CO KG XX Management AUSTRIA A1 TELEKOM AUSTRIA GROUP Media & Content X AUSTRIA RED BULL ORIGINALS Executive Producer X AUSTRIA ORF ENTERPRISE GMBH & CO KG Com. Editor Head of Documentaries / Arts & AUSTRIA OSTERREICHISCHER RUNDFUNK X Culture RTBF RADIO TELEVISION BELGE BELGIUM Head of Documentary Department X COMMUNAUTE FRANCAISE BELGIUM BE TV deputy Head of Programs XX Product & Solutions Team Manager BELGIUM PROXIMUS X Content Acquisition RTBF RADIO TELEVISION BELGE BELGIUM Content Acquisition Officer X COMMUNAUTE FRANCAISE BELGIUM VIEWCOM Managing -

Covid-19 and Public Service Media: Impact of the Pandemic on Public Television in Europe Miguel Túñez-López; Martín Vaz-Álvarez; César Fieiras-Ceide

Covid-19 and public service media: Impact of the pandemic on public television in Europe Miguel Túñez-López; Martín Vaz-Álvarez; César Fieiras-Ceide Nota: Este artículo se puede leer en español en: http://www.elprofesionaldelainformacion.com/contenidos/2020/sep/tunez-vaz-fieiras_es.pdf How to cite this article: Túñez-López, Miguel; Vaz-Álvarez, Martín; Fieiras-Ceide, César (2020). “Covid-19 and public service media: Impact of the pandemic on public television in Europe”. Profesional de la información, v. 29, n. 5, e290518. https://doi.org/10.3145/epi.2020.sep.18 Manuscript received on 16th June 2020 Accepted on 11th August 2020 Miguel Túñez-López * Martín Vaz-Álvarez https://orcid.org/0000-0002-5036-9143 https://orcid.org/0000-0002-4848-9795 Universidade de Santiago de Compostela, Universidade de Santiago de Compostela, Facultad de Ciencias de la Comunicación, Facultade de Ciencias da Comunicación, Depto. de Ciencias de la Comunicación Depto. de Ciencias da Comunicación Av. de Castelao, s/n. Campus Norte Av. Castelao, s/n. Campus Norte 15782 Santiago de Compostela, Spain 15782 Santiago de Compostela, Spain [email protected] [email protected] César Fieiras-Ceide https://orcid.org/0000-0001-5606-3236 Universidade de Santiago de Compostela, Grupo Novos Medios Ronda de la Muralla, 142 27004 Lugo, España [email protected] Abstract This article analyses the response of European Public Service Media to the crisis caused by Covid-19, especially the impact of the pandemic on Europe’s major public broadcasters, with a particular focus on technical and professional constraints, alterations in audience volume and habits, production strategies, type of broadcast content and journalists’ routines.