The Lee Office Brief

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fall Hospitality Report Manhattan 2015

FALL HOSPITALITY REPORT (2015) MANHATTAN FALL HOSPITALITY REPORT MANHATTAN 2015 1 | P a g e FALL HOSPITALITY REPORT (2015) MANHATTAN EXECUTIVE SUMMARY According to the Starr report, Manhattan’s hotel sector has been growing by over 4.0 % since 2010 both by ADR and number of rooms. The demand still far exceeds supply especially for 5 star brands. Early in the hotel recovery in 2011, three star brands grew in number of rooms and ADR initially. As the recovery went into full swing by late 2013, four and five star hotel development continued to outpace three star hotel growth. Global investors are seeking five star hotel product in Manhattan and at $1.0 million up to $2.0 million per key. For instance, Chinese investors bought the Waldorf Astoria and the Baccarat Hotels both at substantially above $1.0 million per key. Manhattan is one of the best hotel markets in the world between growing tourism and inexpensive accommodations compared to other global gateway cities like London, Paris, Moscow, Hong Kong, etc. Any established global hotel brand also requires a presence in Manhattan. In 2014 alone, 4,348 keys were added to Manhattan’s existing 108,592 rooms. Currently, another 14,272 rooms are under construction in the city and about 4000 keys (1/3) are for boutique hotels. As of July 2015, the Manhattan market has approximately 118,000 keys. They are segmented as follows: Currently, there is a 4.0% annual compounded growth rate. Despite this growth, demand for hotel rooms from tourism, conventions, cultural events, and corporate use continues to grow as Manhattan is one of the most desirable locations for all of the above uses especially tourism from Asia and Europe. -

New York Branch Other Regulatory Disclosures

New York Branch Other Regulatory Disclosures April 2019 CIP (Customer Identification Program) Notice In order to comply with existing regulations to combat terrorist financing and money laundering activities, the regulations require all financial institutions to obtain, verify and record information that identifies each person who establishes an account or any other financial relationship with such institution. What this means for you: When you open an account or any other financial relationship with BRADESCO S.A. NEW YORK BRANCH, when an individual request to open an account, we will ask the name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your national ID, Passport, Driver’s License or other valid government issued ID that allow us to perform a verification of the identity of the person. For entities we will request documentation to prove the legal existence, ownership structure, information about the persons authorized to represent the entity as account-holder, the entity’s registration number, tax identity number (TIN) and/or registration number assigned by the registrar of companies or similar government agency where the incorporation documents were filed. We will also ask you for the names of all authorized signatories, attorneys-in- fact, officers and directors of the legal entity opening accounts and for significant beneficial owners of the legal entity account-holders (generally, all those with direct or indirect ownership interest of at least 10%). In some cases, we may request identification documents of persons or legal entities that are already customers of BRADESCO S.A. -

7. Urban Design and Visual Resources

East Midtown Rezoning and Related Actions FEIS 7. Urban Design and Visual Resources 7.1 INTRODUCTION This chapter assesses the Proposed Action’s potential effects on urban design and visual resources. As described in Chapter 1, “Project Description,” the Proposed Action involves zoning map and zoning text amendments that would affect an approximately 70-block area in the East Midtown area of Manhattan for the purpose of protecting and strengthening the area as a premier office district, as well as improving the area’s pedestrian and built environment. The Proposed Action is intended to encourage limited and targeted as-of-right commercial development in appropriate locations by establishing an East Midtown Subdistrict within the Special Midtown District. The East Midtown Subdistrict would supersede and subsume the existing Grand Central Subdistrict, focusing new commercial development with the greatest as-of-right densities on large sites with full block frontage on avenues around Grand Central Terminal, with slightly lower densities allowed along the Park Avenue corridor and elsewhere. The zoning text amendment would also streamline the system for landmark transfers within the Grand Central Subarea of the East Midtown Subdistrict and generate funding for area-wide pedestrian network improvements. The zoning map amendments would replace the existing C5-2 designation in the midblock area between East 42nd and East 43rd Streets, from Second Avenue to Third Avenue, with C5-3 and C5-2.5 designations, which would be mapped within the Special Midtown District and East Midtown Subdistrict. Subject to further analysis and public consultation, the Proposed Action may also amend the City Map to reflect a “Public Place” designation over portions of Vanderbilt Avenue to allow for the permanent development of a partially pedestrianized street. -

Appendix A: Shadows

Appendix A: Shadows Appendix A: Shadows A. INTRODUCTION As discussed in Chapter 6, “Shadows,” a detailed analysis comparing shadows in the future with the proposed project with the shadows in the future with the Previously Approved Project and with the Expanded Development Scenario was undertaken on each of the four analysis days, consistent with the methodology outlined in the CEQR Technical Manual. For a substantial number of open space and historic resources, the proposed project would not result in any incremental increase in shadow. In addition, there are a number of resources that would receive incremental shadow for fewer than 30 minutes. These resources are described in detail in this appendix. B. ASSESSMENT OF INCREMENTAL SHADOWS: PROPOSED PROJECT COMPARED WITH PREVIOUSLY APPROVED PROJECT OPEN SPACES THAT WOULD NOT RECEIVE ANY INCREMENTAL SHADOW THE SHEFFIELD RESIDENTIAL PLAZAS These plazas, located on the block bounded by Eighth and Ninth Avenues and West 56th and 57th Streets, are fully in existing shadow during the first 15 minutes of the December 21 analysis day, when the proposed project’s shadow would otherwise affect them. No incremental shadow would fall on these spaces at any time of year, and no shadow impacts would occur as a result of the proposed project. MCCAFFREY PLAYGROUND This playground is located on the north side of West 43rd Street between Eighth and Ninth Avenues. Shadow from the proposed project would be long enough to reach this playground from 6:57 AM to 7:15 AM on the June 21 analysis day; however, the portions of the space that could be affected are already in shadow at this time, and so no incremental shadow would occur. -

SIX CIRCLES TRUST Six Circles Credit Opportunities Fund 383

SIX CIRCLES TRUST Six Circles Credit Opportunities Fund 383 Madison Avenue New York, New York 10179 Collect (212) 464-2070 May 27, 2021 Dear Shareholder, The attached information statement contains important information about a new sub-advisory arrangement for the Six Circles Credit Opportunities Fund (the “Fund”), a series of the Six Circles Trust (the “Trust”). On March 12, 2021, J.P. Morgan Private Investments Inc. (the “Adviser”), the Fund’s investment adviser, entered into new Investment Sub-Advisory Agreements with each of BlueBay Asset Management LLP (“BlueBay”) and Muzinich & Co., Inc. (“Muzinich”) (each, a “New Sub-Advisory Agreement” and together the “New Sub-Advisory Agreements”), pursuant to which both BlueBay and Muzinich have been engaged by the Adviser, with the approval of the Trust’s Board of Trustees, to serve as sub-advisers to the Fund. After careful consideration at a meeting held on March 3, 2021, the Trust’s Board of Trustees approved the New Sub-Advisory Agreements between the Adviser and each of BlueBay and Muzinich and determined that the terms and conditions of the New Sub-Advisory Agreements are fair to, and in the best interests of, the Fund and its shareholders. Specifically, both BlueBay and Muzinich have been engaged by the Adviser to serve as sub-advisers to the Fund. As a matter of regulatory compliance, we are sending you this information statement. Please read this information statement carefully. It describes the current management structure of the Fund and the Trust, the terms of the two New Sub-Advisory Agreements, factors considered by the Trust’s Board of Trustees in approving the two New Sub-Advisory Agreements, and other related information. -

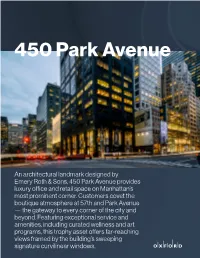

450 Park Avenue

450 Park Avenue An architectural landmark designed by Emery Roth & Sons, 450 Park Avenue provides luxury office and retail space on Manhattan’s most prominent corner. Customers covet the boutique atmosphere at 57th and Park Avenue — the gateway to every corner of the city and beyond. Featuring exceptional service and amenities, including curated wellness and art programs, this trophy asset offers far-reaching views framed by the building’s sweeping signature curvilinear windows. Luxury office connects people and commerce on Park Avenue At a glance 33 332,773 stories SF GLA Awards Energy Star Certification Wired Certified - Silver NEW JERSEY NORTH Location & access MUSEUM DEWITT OF ARTS CLINTON PARK AND DESIGN W 54TH ST W 58TH ST CENTRAL PARK HUDSON RIVER W 52ND ST PARK AVE 10TH AVE MTA - N, R, W Trains 9TH AVE 7TH AVE CARNEGIE - 5 Avenue Station - W 50TH ST BROADWAY HALL THEATRE THE PLAZA E 62ND ST 6 minute walk LINCOLN TUNNEL 8TH AVE 650 MADISON AVE SHERATON W 48TH ST NEW YORK MTA - 4, 5, 6 Trains - TIMES SQUARE 6TH AVE E 60TH ST 59 St- Lexington Av MUSEUM OF E 58TH ST MODERN ART Station - 6 minute W 46TH ST TRUMP walk TOWER 450 PARK AVE ANTHONY BRIZZI PL 11TH AVE RADIO CITY W 44TH ST MUSIC HALL 12TH AVE LINCOLN TUNNEL E 56TH ST INTERCONTINENTAL W 42ND ST NEW YORK TIMES SQUARE FDR Drive - TOP OF THE ROCK 645 5th AVE 6 minute drive 3RD AVE ROCKEFELLER MADISON AVE CENTER TIMES THE NEW YORK ST. PATRICK'S SQUARE PARK AVE MUSEUM OF CATHEDRAL CONTEMPORARY ART W 40TH ST HILTON E 54TH ST GARDEN INN W 38TH ST E 52ND ST E 50TH ST HUDSON YARDS HAMPTON -

Chapter 5: Open Space

Chapter 5: Open Space A. INTRODUCTION The 2001 New York City Environmental Quality Review (CEQR) Technical Manual guidelines indicate that an open space analysis is warranted when a proposed project would result in the physical loss of public open space or would introduce 200 or more residents or 500 or more workers to an area. Because the proposed 53 West 53rd Street project would generate approximately 462 residents, it would exceed the CEQR threshold, and therefore, an analysis of open space is warranted. As detailed in this chapter, an open space analysis was conducted to determine whether the proposed project would cause any direct or indirect significant adverse open space impacts. This chapter first assesses existing open space conditions in the study area, and then compares conditions in the future with and without the proposed project to determine potential impacts for the 2013 analysis year. Overall, the proposed project would not result in a significant adverse impact to open space. Table 5-1 compares open space ratios in the future without the proposed project (assuming completion of either the Previously Approved Project or the Expanded Development Scenario) with the ratios in the future with the proposed project. Table 5-1 Open Space Ratios Summary Open Space Ratios Percent Change Future Without the Proposed Future Without to Future Project with the Proposed Project Future Change from Change from Previously Expanded with the Previously Expanded City Existing Approved Development Proposed Approved Development Ratio Guideline Conditions Project Scenario Project Project Scenario Total/Residents 2.5 3.33 3.20 3.14 3.14 -1.8% 0% Passive/Residents 0.5 2.01 1.93 1.90 1.90 -1.8% 0% Weighted: Passive/Total 0.17 / 0.17 / Population 0.17* 0.09 0.09 0.09 0.09 0.0% 0% Active/Residents 2.0 1.31 1.26 1.23 1.23 -1.8% 0% Notes: Ratios in acres per 1,000 people. -

DENNIS I. HELLMAN MEMBER - Transactions

DENNIS I. HELLMAN MEMBER - Transactions 733 Third Avenue, New York, NY 10017 [email protected] 212-551-8408 Practice Areas Dennis I. Hellman joined Rosenberg & Estis in 1993 and is a member with Transactional Law the firm’s Transactional Department. In recent years, most of Mr. Hellman’s Real Estate Leasing practice has been concentrated on acquisitions, dispositions and develop- ments throughout the United States, as well as on representing borrowers Real Estate Development in complex financings and both owners and tenants in commercial leasing matters. Mr. Hellman’s after-hours commitments include memberships on Bar Admissions several committees of the Real Property Law Section of the New York State New York, 1975 Bar Association. U.S. District Court Eastern District of New York, 1975 Mr. Hellman’s after-hours commitments include memberships on several U.S. District Court Southern District of New committees of the Real Property Law Section of the New York State Bar York, 1975 Association. U.S. Court of Appeals 2nd Circuit, 1975 Education New York University School of Law Notable Work • J.D. - 1974 • The Durst Organization in construction loans and EB-5 financings Honors & Activities: for each of 855 Avenue of the Americas and 625 West 57th Street in an aggregate amount in excess of $900 Million. • New York University Law Review, Articles Editor, 1973 - 1974 • Somerset Partners in the acquisition, financing, leasing and sale (for City College of the City University of approximately $550 Million) of 450 Park Avenue. New York • The Durst Organization in the lease of 9 floors at 1133 Avenue of • B.A. -

3Q16 NYC Office Market Overview

3Q16 NEW YORK CITY OFFICE MARKET OVERVIEW TABLE OF CONTENTS 3 Executive Summary 22 Manhattan Development Overview 23 Commercial Development Pipeline 4 Manhattan Office Market Overview 24 Commercial Development Horizon Map 25 Manhattan Development Overview 5 Leasing Activity by Market 26 Boutique Development Overview 6 Key Leasing Activity Metrics 7 Industries Driving Demand: Employment and Leasing Trends Industries Driving Demand: 3Q16 Leasing and Tenants in the Brooklyn and Long Island City 8 Market 27 Office Market Overview 9 Composition of Tech Leasing 28 Brooklyn Office Development Map 10 Manhattan Submarket Comparison 29 Brooklyn Office Development Overview 11 Asking Rent Trends 30 Brooklyn’s Changing Inventory 12 Taking and Net Effective Rent Trends 31 Brooklyn Market Trends 13 Taking Rent Corridor and Submarket Comparisons 32 Brooklyn Submarket Snapshot 14 Concessions Analysis: Work Amount 33 Asking Rent Comparison 15 Concessions Analysis: Free Rent 34 Long Island City Trends 16 Triple-Digit Taking Rent Assets 35 Long Island City Submarket Snapshot 17 Manhattan Top-Tier Trends 18 Midtown South Top-Tier Trends 19 Midtown Deal Composition 20 Midtown South Deal Composition 21 Downtown Deal Composition 2 EXECUTIVE SUMMARY Leasing A drop in relocation activity was balanced by an uptick in renewals, particularly among large deals in Midtown. Overall leasing activity in Midtown South fell below the prior Activity year and ten-year averages. Industry FIRE activity increased in the third quarter and TAMI activity declined for the third consecutive quarter, while the types of tech tenants that were active continued to Growth diversify from recent years. Asking and Asking rents continued to increase, though at a slower rate than the annual average during this market cycle. -

Pressure Mounts for Paterson to Quit

20100301-NEWS--0001-NAT-CCI-CN_-- 2/26/2010 7:45 PM Page 1 INSIDE There’s danger in TOP STORIES crowning Say ‘Ah, not again.’ Cuomo Sick-days law back —Greg David on the presumed on council agenda ® front-runner PAGE 4 Page 11 Condé Nast leads mag publishers’ VOL. XXVI, NO. 9 WWW.CRAINSNEWYORK.COM MARCH 1-7, 2010 PRICE: $3.00 charge onto iPad PAGE 2 Pressure Why private equity queen mounts for Lynn Tilton wants to Paterson start up her own bank to quit PAGE 3 Sibling barflies Neutered guv has the Gerbers ride out little support; Ravitch the recession is waiting in the wings PAGE 2 BY ERIK ENGQUIST Scammers target PERFECT PITCHMAN: His efforts at NYC & as the political world buzzes about entrepreneurs Company are credited with bolstering tourism activity when Gov. David Paterson’s tenure SMALL BUSINESS, PAGE 9 here during tough times. will end, the question has changed from whether he can mount an election cam- NEWS paign—the answer was no—to whether he can ANALYSIS BUSINESS LIVES govern at all. With his public and political support evaporat- ing, and a problematic state budget and other crucial issues facing Albany in the next two months, the pressure on him to resign will build. In some ways, it is an acceleration of the inevitable.The Legislature was be- See PRESSURE’S ON on Page 22 EDITORIAL Bowing out, ungracefully PAGE 10 HEALTH CARE HEAVIES Docs, unions, hospitals GOTHAM GIGS ready to fight funding cuts in Albany PAGE 22 Jonathan Levy really is a trailblazer P. -

Request for Evaluation

REQUEST FOR EVALUATION Address: 445 PARK AVENUE Location: Block 1311 Lot 1 Name: 445 Park Avenue Architect: Kahn & Jacobs Constructed: 1946-1947 Summary: The first post-war office building on Park Avenue – and the first fully air-conditioned commercial structure in New York City – 445 Park Avenue set the stage for future development along Park Avenue. The prominent architecture firm Kahn & Jacobs, architects of the Landmarked Municipal Asphalt Plant (1941-44), designed this building. The rectilinear glass and limestone structure, with its dark granite base, is composed of four setbacks, adhering to the 1916 zoning law. Continuous ribbon windows and limestone spandrel panels give the building a sleekness in stark contrast to its contemporary buildings. Lever Brothers Company, Schweppes, Ford Motor Company, Monsanto Chemical Company, and Universal Pictures Corporation all leased space in the structure in the 1940s. 1 REQUEST FOR EVALUATION Address: 450 PARK AVENUE Location: Block 1292 Lot 37 Name: former Franklin National Bank Building Architect: Emery Roth & Sons Constructed: 1968-1972 Summary: This 33-story skyscraper has been called “the handsomest black skyscraper in the city.” 450 Park Avenue served as the headquarters of the Franklin National Bank from 1972-74, and its sleek black façade and dark glass set it apart from other structures on Park Avenue, especially those designed by Emery Roth & Sons in the previous decades. The building has a smooth façade treatment composed of “black granite” (likely gabbro or diabase) and graceful elliptical window segments of gray-tinted glass. Following the 1961 zoning resolution, the architects designed a privately owned public space on the west side of the structure. -

1Q16 Office Market Overview Table of Contents

1Q16 NEW YORK CITY OFFICE MARKET OVERVIEW 1Q16 Office Market Overview Table of Contents 3 Executive Summary 4 Manhattan Office Market Analysis 23 Manhattan Development Overview 5 Leasing Activity by Market 24 Commercial Development Pipeline 6 Top Transactions 1Q16 25 Commercial Development Horizon Map 7 Industries Driving Leasing 26 World Trade Center Development Overview 8 TAMI Taking Rent Comparison 27 Far West Side Development Overview 9 TAMI Deals by Submarket 28 Midtown East Development Overview 10 Manhattan Submarket Matrix 29 Boutique Development Overview 11 Asking Rent Trends 12 Taking Rent Trends Brooklyn and Long Island City 13 Taking Rent Corridor and Submarket Comparisons 30 Office Market Analysis 14 Net Effective Rent Trends 31 Brooklyn Office Developments in the Pipeline Map 15 Concessions for Select Submarkets 32 Brooklyn Office Development in the Pipeline Overview 16 Midtown Deal Composition 33 Brooklyn Inventory Pipeline 17 Midtown South Deal Composition 34 Dumbo and Downtown Brooklyn Trends 18 Downtown Deal Composition 35 Asking Rent Comparison 19 Triple-Digit Taking Assets 36 Long Island City Trends 20 Manhattan Top-Tier Trends 37 Long Island City Submarket Snapshot 21 Midtown South Top-Tier Trends 38 Long Island City Transformation Statistics 22 Midtown and Downtown Height Analysis | 2 1Q16 Office Market Overview Executive Summary Prime assets and new construction continued to attract high-profile tenants during the first quarter of 2016. Increased renewal activity made up for a drop in relocations causing overall Manhattan leasing to be stable year-over-year and with the ten-year quarterly average. Midtown and Downtown outperformed below-average leasing in Midtown South.