Europe Agrifood Tech Investing Report 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The State of European Food Tech 2021

The State of European Food Tech 2021 MARCH 2021 2020 marked an inflection point Covid-19 accelerated egrocery Food production and for foodtech, as consumers adoption, and the emergence of transformation is catching up reassessed how they eat new food distribution models with consumer-facing foodtech The pandemic has driven radical changes in We believe the egrocery to be bigger than food B2B food companies may take longer to unlock consumer behaviour and accelerated adoption delivery, as total market for groceries is $2.1tn growth than B2C but the opportunity could be of meal and grocery deliveries, some of which is compared to $0.6tn for restaurants. Egrocery bigger representing €1.7bn of capital investment in 2020 . here to stay. It also highlighted big inefficiencies companies have seen skyrocketing growth in in the food supply chain and raised awareness 2020 (3x to 10x vs 2019), as convenience turned The pandemic highlighted inefficiencies in the for a healthier and sustainable food system. into necessity. food supply chain and the need for new technology solutions. Investments to enable 2020 saw continued growth in food startup As demand shifted away from food services, supply chain automation, or funding to indoor investor interest, with €2.4bn invested in 2020 meal kits companies efficiently stepped in and vertical farming have been on the rise. (+12x vs 2013) and an increase of foodtech together with virtual/dark kitchens, and Insect production and food waste management also attracted large VC funding. startup valuations (+156% vs 2019). removed previous doubts over these models. Quick-commerce startups (the 15 minute As consumer interest in sustainable alternatives European foodtech unicorns are now large, delivery from local dark stores), the last grows, so do investments and valuations in the international players, catching up with their US newborn in the grocery space, drew most plant-based and cell-based sector (10x in 5 counterparts (i.e. -

Gig Economy and Processes of Information, Consultation, Participation and Collective Bargaining"

Paper on the European Union co-funded project VS/2019/0040 "Gig economy and processes of information, consultation, participation and collective bargaining". By Davide Dazzi (translation from Italian to English by Federico Tani) Updated the 20th of July 2020 Sommario Introduction ....................................................................................................................................................... 2 Gig Economy : a defining framework ................................................................................................................. 2 Platforms and Covid-19 ..................................................................................................................................... 6 GIG workers: a quantitative dimension ........................................................................................................... 10 On line outsourcing ..................................................................................................................................... 11 Crowdworkers and Covid-19 ....................................................................................................................... 14 Working conditions of GIG workers ................................................................................................................ 17 Covid 19 laying bare the asymmetry of social protections ............................................................................. 21 Towards a protection system for platform workers .................................................................................. -

Elektronik Ticaretve Rekabet Hukuku Kapsaminda Çok Tarafli Pazaryerleri

ELEKTRONİK TİCARETVE REKABET HUKUKU KAPSAMINDA ÇOK TARAFLI PAZARYERLERİ Tuğba Çelik 141102111 YÜKSEK LİSANS TEZİ Özel Hukuk Anabilim Dalı Özel Hukuk Yüksek Lisans Programı Danışman: Dr. Öğr. Üyesi Mete Tevetoğlu İstanbul T.C. Maltepe Üniversitesi Sosyal Bilimler Enstitüsü Ağustos 2019 i JÜRİ VE ENSTİTÜ ONAYI ii ETİK İLKE VE KURALLARA UYUM BEYANI iii TEŞEKKÜR Tüm bu süreçte desteğini esirgemeyen başta babam Celal Çelik ve annem Selda Çelik olmak üzere, tez danışmanım Dr. Öğr. Üyesi Mete Tevetoğlu’na, tüm dostlarıma ve yol arkadaşıma en içten teşekkürlerimi sunuyorum. Tuğba Çelik Ağustos 2019 iv ÖZ ELEKTRONİK TİCARET VE REKABET HUKUKU KAPSAMINDA ÇOK TARAFLI PAZARYERLERİ Tuğba Çelik Yüksek Lisans Tezi Özel Hukuk Anabilim Dalı Özel Hukuk Yüksek Lisans Programı Danışman: Dr. Öğr. Üyesi Mete Tevetoğlu Maltepe Üniversitesi Sosyal Bilimler Enstitüsü, 2019 İnternet ortamındaki gelişmelere bağlı olarak, ulusal ve uluslararası ekonomi çevrelerinde, hızla artan bir biçimde ağırlığını hissettiren elektronik ticaret ve elektronik pazaryerleri kavramının, kapsamı ve genel olarak ekonomik etkileri açısından önemi her geçen gün artmaktadır. Bu gelişmeler ile birlikte, elektronik pazaryerlerinde üreticiler, satıcılar ve alıcılar gibi talep sahiplerinin karşılıklı arz ve taleplerini kısa sürede ve daha avantajlı şartlarda buluşturan platformlar yani aracı hizmet sağlayıcıları, önemli bir figür olarak karşımıza çıkmaktadır. Aracılık hizmetleri sağlayan bu platformlar, regülâsyonlara ve özellikle de rekabet kurallarına uyum sağlama sürecinde bazı yapısal, -

Just Eat/Hungryhouse Appendices and Glossary to the Final Report

Anticipated acquisition by Just Eat of Hungryhouse Appendices and glossary Appendix A: Terms of reference and conduct of the inquiry Appendix B: Delivery Hero and Hungryhouse group structure and financial performance Appendix C: Documentary evidence relating to the counterfactual Appendix D: Dimensions of competition Appendix E: The economics of multi-sided platforms Appendix F: Econometric analysis Glossary Appendix A: Terms of reference and conduct of the inquiry Terms of reference 1. On 19 May 2017, the CMA referred the anticipated acquisition by Just Eat plc of Hungryhouse Holdings Limited for an in-depth phase 2 inquiry. 1. In exercise of its duty under section 33(1) of the Enterprise Act 2002 (the Act) the Competition and Markets Authority (CMA) believes that it is or may be the case that: (a) arrangements are in progress or in contemplation which, if carried into effect, will result in the creation of a relevant merger situation, in that: (i) enterprises carried on by, or under the control of, Just Eat plc will cease to be distinct from enterprises carried on by, or under the control of, Hungryhouse Holdings Limited; and (ii) the condition specified in section 23(2)(b) of the Act is satisfied; and (b) the creation of that situation may be expected to result in a substantial lessening of competition within a market or markets in the United Kingdom for goods or services, including in the supply of online takeaway ordering aggregation platforms. 2. Therefore, in exercise of its duty under section 33(1) of the Act, the CMA hereby makes -

The MARU/Matchbox Brand Awareness Rankings By

Which of the following online personal care retailers have you ever heard of? Total 18+ Millennials 18-34 Gen X 35-49 Boomers 50-64 Seniors 65+ Male 18+ Female 18+ Category Brand awareness awareness awareness awareness awareness awareness awareness Personal care Dollar Shave Club 71% 70% 77% 74% 63% 73% 70% Personal care Birchbox 42% 54% 52% 35% 22% 28% 54% Personal care Harry’s 34% 37% 34% 34% 26% 46% 23% Personal care Smile Direct Club 32% 43% 39% 27% 19% 29% 36% Personal care Peloton 28% 29% 26% 30% 27% 27% 30% Personal care Ipsy 26% 40% 29% 20% 10% 17% 34% Personal care Rodan+Fields 21% 32% 28% 14% 6% 13% 28% Personal care PillPack 16% 19% 14% 14% 15% 17% 15% Personal care Noom 15% 21% 13% 13% 11% 12% 18% Personal care Hims 13% 20% 11% 10% 7% 20% 6% Personal care Hubble 12% 22% 13% 8% 5% 13% 11% Personal care ColourPop 9% 23% 9% 3% 1% 6% 12% Personal care eSalon 9% 18% 8% 6% 2% 10% 7% Personal care Glossybox 9% 17% 10% 4% 3% 10% 8% Personal care Lola 9% 22% 7% 3% 1% 8% 9% Personal care Glossier 8% 21% 7% 3% 0% 9% 8% Personal care Quip 8% 16% 7% 6% 1% 11% 6% Personal care Silk Therapeutics 8% 16% 9% 5% 1% 10% 7% Personal care BoxyCharm 8% 20% 8% 2% 0% 8% 8% Personal care 4moms 8% 19% 7% 3% 0% 9% 6% Personal care Native 7% 17% 7% 3% 1% 9% 6% Personal care Zocdoc 7% 21% 4% 2% 0% 10% 4% Personal care REN Clean Skincare 7% 15% 6% 3% 2% 8% 6% Personal care LunaPads 7% 18% 5% 1% 1% 9% 5% Personal care Thinx 7% 19% 6% 0% 0% 7% 6% Personal care Walker and Company 6% 16% 6% 2% 1% 9% 4% Personal care Keeps 6% 13% 6% 3% 2% 10% 3% Personal care -

Delivering the Multisensory Experience of Dining-Out, for Those Dining-In, During the Covid Pandemic

REVIEW published: 21 July 2021 doi: 10.3389/fpsyg.2021.683569 Delivering the Multisensory Experience of Dining-Out, for Those Dining-In, During the Covid Pandemic Charles Spence 1*, Jozef Youssef 2 and Carmel A. Levitan 3 1 Department of Experimental Psychology, Oxford University, Oxford, United Kingdom, 2 Chef/Patron, Kitchen Theory, London, United Kingdom, 3 Department of Cognitive Science, Occidental College, Los Angeles, CA, United States In many parts of the world, restaurants have been forced to close in unprecedented numbers during the various Covid-19 pandemic lockdowns that have paralyzed the hospitality industry globally. This highly-challenging operating environment has led to a rapid expansion in the number of high-end restaurants offering take-away food, or home-delivery meal kits, simply in order to survive. While the market for the home delivery of food was already expanding rapidly prior to the emergence of the Covid pandemic, the explosive recent growth seen in this sector has thrown up some intriguing issues and challenges. For instance, concerns have been raised over where many of the meals that are being delivered are being prepared, given the rise of so-called “dark kitchens.” Furthermore, figuring out which elements of the high-end, fine-dining experience, and of the increasingly-popular multisensory experiential dining, can be captured by those Edited by: Igor Pravst, diners who may be eating and drinking in the comfort of their own homes represents an Institute of Nutrition, Slovenia intriguing challenge for the emerging field of gastrophysics research; one that the chefs, Reviewed by: restaurateurs, restaurant groups, and even the food delivery companies concerned Alexandra Wolf, are only just beginning to get to grips with. -

Technology Report

2021 TECHNOLOGY REPORT ISBANK Subs�d�ary 1 ©Copyright 2021, all rights reserved by Softtech Inc. No part or paragraph may be reproduced, published, represented, rented, copied, reproduced, be transmitted through signal, sound, and/or image transmission including wired/wireless broadcast or digital transmission, be stored for later use, be used, allowed to be used and distributed for commercial purposes, be used and distributed, in whole or in part or summary in any form. Quotations that exceed the normal size cannot be made. If it is desired to do so, Softtech A.Ş.’s written approval is required. In normal and legal quotations, citation in the form of “© Copyright 2021, all rights reserved by Softtech A.Ş.” is mandatory. The information and opinions of each author included in the report do not represent any institution and organization, especially Softtech and the institution they work with, they contain the opinions of the authors themselves. 2021 TECHNOLOGY REPORT ISBANK Subs�d�ary Colophon Preamble Jale İpekoğlu Umut Yalçın M. Murat Ertem Leyla Veliev Azimli Ussal Şahbaz Lucas Calleja Volkan Sözmen Mehmet Güneş Prof. Dr. Vasıf Hasırcı Authors Mehtap Özdemir Att. Yaşar K. Canpolat Ahmet Usta Mert Bağcılar Ali Can Işıtman Muhammet Özmen Editors Bahar Tekin Shirali Mustafa Dalcı Aylin Öztürk Berna Gedik Mustafa İçer Fatih Günaydın Burak Arık Mükremin Seçkin Yeniel Selçuk Sevindik Burak İnce Onur Koç Umut Esen Burcu Yapar Onur Yavuz Demet Zübeyiroğlu Ömer Erkmen Design Didem Altınbilek Assoc. Prof. Dr. Özge Can Emrah Yayıcı Qi Yin & Jlian Sun 12 Yapım Eren Hükümdar Rüken Aksakallı Temel Selçuk Sevindik Fatih Günaydın Salih Cemil Çetin GPT-3 Sara Holyavkin Contact Görkem Keskin Selçuk Sevindik Gül Çömez Prof. -

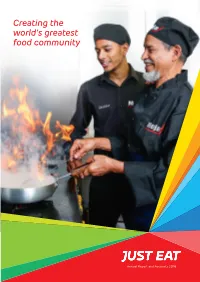

Creating the World's Greatest Food Community

Creating the world’s greatest food community Just Eat plc Annual Report and Accounts 2016 Annual Report Annual Report and Accounts 2016 Front cover At Just Eat we operate a leading global Father and son team at Moja Indian & Bangladeshi marketplace for online food delivery, Takeaway, Stockton- on-Tees. Finalist, North East region, at providing customers with an easy the British Takeaway and secure way to order and pay for Awards 2016. food from our Restaurant Partners. Since we launched in Denmark in 2001, we have expanded globally into 11 other markets, with a strategy to be market leader in each country in which we operate. Our scale creates compelling network effects. Our values Make Razor Big Happy Sharp Hearted See page 2 See page 12 See page 34 5 Annual Report & Accounts 2016 Contents Our vision Strategic report Our vision is to create 4 Highlights 2016 the world’s greatest food 6 Chairman’s statement community. We’ll achieve this 8 At a glance through our purpose, which is 10 Chief Executive Officer’s review 14 Our business model to make food discovery exciting 16 Market overview for everyone. 18 Our strategy 19 Our key performance indicators For our customers it is about 20 Principal risks and uncertainties discovering the widest choice 24 Chief Financial Officer’s review and facilitating what they 32 Operational review want to eat, when and where. 36 Our people and community For our Restaurant Partners Corporate governance it is about working with them 40 Corporate governance report to help them reach more 42 Our Board customers, supporting their 44 Report of the Board business and driving 51 Report of the Audit Committee 56 Report of the Nomination Committee standards in the industry. -

Boston San Francisco Munich London

Internet & Digital Media Monthly August 2018 BOB LOCKWOOD JERRY DARKO Managing Director Senior Vice President +1.617.624.7010 +1.415.616.8002 [email protected] [email protected] BOSTON SAN FRANCISCO HARALD MAEHRLE LAURA MADDISON Managing Director Senior Vice President +49.892.323.7720 +44.203.798.5600 [email protected] [email protected] MUNICH LONDON INVESTMENT BANKING Raymond James & Associates, Inc. member New York Stock Exchange/SIPC. Internet & Digital Media Monthly TECHNOLOGY & SERVICES INVESTMENT BANKING GROUP OVERVIEW Deep & Experienced Tech Team Business Model Coverage Internet / Digital Media + More Than 75 Investment Banking Professionals Globally Software / SaaS + 11 Senior Equity Research Technology-Enabled Solutions Analysts Transaction Processing + 7 Equity Capital Markets Professionals Data / Information Services Systems | Semiconductors | Hardware + 8 Global Offices BPO / IT Services Extensive Transaction Experience Domain Coverage Vertical Coverage Accounting / Financial B2B + More than 160 M&A and private placement transactions with an Digital Media Communications aggregate deal value of exceeding $25 billion since 2012 E-Commerce Consumer HCM Education / Non-Profit + More than 100 public equities transactions raising more than Marketing Tech / Services Financial $10 billion since 2012 Supply Chain Real Estate . Internet Equity Research: Top-Ranked Research Team Covering 25+ Companies . Software / Other Equity Research: 4 Analysts Covering 40+ Companies RAYMOND JAMES / INVESTMENT BANKING OVERVIEW . Full-service firm with investment banking, equity research, institutional sales & trading and asset management – Founded in 1962; public since 1983 (NYSE: RJF) – $6.4 billion in FY 2017 revenue; equity market capitalization of approximately $14.0 billion – Stable and well-capitalized platform; over 110 consecutive quarters of profitability . -

Submission to the CMA on Deliveroo

CCIA’s submission to the UK Competition & Markets Authority on the CMA’s provisional findings in Amazon / Deliveroo 11 May 2020 1. Introduction The Computer and Communications Industry Association (“CCIA”) is grateful for this opportunity to share its views on the Competition & Markets Authority (“CMA”) provisional findings regarding Amazon’s acquisition of a minority shareholding in Deliveroo (“the Transaction”).1 CCIA represents large, medium, and small companies in the high technology products and services sectors, including computer hardware and software, electronic commerce, telecommunications, and Internet products and services.2 CCIA is committed to protecting and advancing the interests of our members, the industry as a whole, as well as society’s beneficial interest in open markets, open systems and open networks.3 CCIA agrees with the conclusion of the Provisional Findings that the Transaction would not be expected to result in a substantial lessening of competition.4 However, CCIA believes there is significant evidence of competitive constraints faced by both Amazon and Deliveroo (the “Parties”), and the dynamic nature of the markets. Accordingly, CCIA submits that, even in the absence of the current crisis,5 the Transaction would not have resulted in a substantial lessening of competition (“SLC”) and would not have harmed customers.6 2. Competitive Constraint of Potential Entry and Expansion In its 11 December 2019 Phase I decision,7 the CMA found an SLC to the detriment of customers and referred the case for an in-depth investigation. As the CMA correctly notes in its Provisional Findings, “[a]n SLC occurs when rivalry is substantially less intense after a merger than would otherwise have been the case, resulting in a worse outcome for customers (through, for example, higher prices, reduced quality or reduced choice).”8 CCIA understands that the market for online food delivery in the UK is highly competitive and likely to become more competitive in the future. -

Annual Report 2019

ANNUAL REPORT 2019 – HelloFresh SE – HELLOFRESH AT A GLANCE 3 months 3 months 12 months 12 months ended ended ended ended Key Figures 31-Dec 19 31-Dec 18 YoY growth 31-Dec 19 31-Dec-18 YoY growth Key Performance Indicators Group Active customers (in millions) 2.97 2.04 45.3% Number of orders (in millions) 10.54 7.42 42.0% 37.45 27.07 38.3% Orders per customer 3.6 3.6 - Meals (in millions) 79.6 54.7 45.6% 281.1 198.4 41.7% Average order value (EUR) (Exc. Retail) 48.6 48.6 0.0% Average order value constant currency (EUR) (Exc. Retail) 47.8 48.6 (1.7%) USA Active customers (in millions) 1.78 1.09 63.0% Number of orders (in millions) 5.98 3.84 55.7% 20.74 14.94 38.8% Orders per customer 3.4 3.5 (4.5%) Meals (in millions) 40.5 25.2 60.4% 138.2 99.2 39.3% Average order value (EUR) (Exc. Retail) 49.1 50.6 (3.0%) Average order value constant currency (EUR) (Exc. Retail) 47.6 50.6 (5.9%) International Active customers (in millions) 1.18 0.95 24.9% Number of orders (in millions) 4.56 3.58 27.4% 16.71 12.13 37.8% Orders per customer 3.9 3.8 2.0% Meals (in millions) 39.1 29.4 32.9% 142.9 99.2 44.0% Average order value (EUR) (Exc. Retail) 48.0 46.4 3.3% Average order value constant currency (EUR) (Exc. -

Just Eat/Hungryhouse Food Ordering Platforms

Just Eat and Hungryhouse A report on the anticipated acquisition by JUST EAT plc of Hungryhouse Holdings Limited 16 November 2017 © Crown copyright 2017 You may reuse this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit www.nationalarchives.gov.uk/doc/open-government- licence/ or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected]. Website: www.gov.uk/cma Members of the Competition and Markets Authority who conducted this inquiry Professor Martin Cave (Chair of the Group) Katherine Holmes John Krumins Jayne Scott Chief Executive of the Competition and Markets Authority Andrea Coscelli The Competition and Markets Authority has excluded from this published version of the report information which the Inquiry Group considers should be excluded having regard to the three considerations set out in section 244 of the Enterprise Act 2002 (specified information: considerations relevant to disclosure). The omissions are indicated by []. Some numbers have been replaced by a range. These are shown in square brackets. Non-sensitive wording is also indicated in square brackets. Contents Page Summary .................................................................................................................... 3 Findings ...................................................................................................................... 9 1. The reference ......................................................................................................