Bahrain's Fiscal Position and Regional Lifelines by Muizz Alaradi

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bahrain Country Report BTI 2012

BTI 2012 | Bahrain Country Report Status Index 1-10 5.89 # 56 of 128 Political Transformation 1-10 4.35 # 87 of 128 Economic Transformation 1-10 7.43 # 21 of 128 Management Index 1-10 4.18 # 91 of 128 scale: 1 (lowest) to 10 (highest) score rank trend This report is part of the Bertelsmann Stiftung’s Transformation Index (BTI) 2012. The BTI is a global assessment of transition processes in which the state of democracy and market economy as well as the quality of political management in 128 transformation and developing countries are evaluated. More on the BTI at http://www.bti-project.org Please cite as follows: Bertelsmann Stiftung, BTI 2012 — Bahrain Country Report. Gütersloh: Bertelsmann Stiftung, 2012. © 2012 Bertelsmann Stiftung, Gütersloh BTI 2012 | Bahrain 2 Key Indicators Population mn. 1.3 HDI 0.806 GDP p.c. $ - Pop. growth1 % p.a. 7.6 HDI rank of 187 42 Gini Index - Life expectancy years 75 UN Education Index 0.747 Poverty3 % - Urban population % 88.6 Gender inequality2 0.288 Aid per capita $ - Sources: The World Bank, World Development Indicators 2011 | UNDP, Human Development Report 2011. Footnotes: (1) Average annual growth rate. (2) Gender Inequality Index (GII). (3) Percentage of population living on less than $2 a day. Executive Summary Bahrain’s democratic reform process has come to a standstill since 2009, which marked the 10th anniversary of King Hamad bin Isa Al Khalifa’s accession to power. The positive developments in civil and political liberties observed with the start of the reform process in 2002 have in recent years been counteracted by repressive state tactics in which freedoms of expression and assembly have suffered most. -

FAO Country Name ISO Currency Code* Currency Name*

FAO Country Name ISO Currency Code* Currency Name* Afghanistan AFA Afghani Albania ALL Lek Algeria DZD Algerian Dinar Amer Samoa USD US Dollar Andorra ADP Andorran Peseta Angola AON New Kwanza Anguilla XCD East Caribbean Dollar Antigua Barb XCD East Caribbean Dollar Argentina ARS Argentine Peso Armenia AMD Armeniam Dram Aruba AWG Aruban Guilder Australia AUD Australian Dollar Austria ATS Schilling Azerbaijan AZM Azerbaijanian Manat Bahamas BSD Bahamian Dollar Bahrain BHD Bahraini Dinar Bangladesh BDT Taka Barbados BBD Barbados Dollar Belarus BYB Belarussian Ruble Belgium BEF Belgian Franc Belize BZD Belize Dollar Benin XOF CFA Franc Bermuda BMD Bermudian Dollar Bhutan BTN Ngultrum Bolivia BOB Boliviano Botswana BWP Pula Br Ind Oc Tr USD US Dollar Br Virgin Is USD US Dollar Brazil BRL Brazilian Real Brunei Darsm BND Brunei Dollar Bulgaria BGN New Lev Burkina Faso XOF CFA Franc Burundi BIF Burundi Franc Côte dIvoire XOF CFA Franc Cambodia KHR Riel Cameroon XAF CFA Franc Canada CAD Canadian Dollar Cape Verde CVE Cape Verde Escudo Cayman Is KYD Cayman Islands Dollar Cent Afr Rep XAF CFA Franc Chad XAF CFA Franc Channel Is GBP Pound Sterling Chile CLP Chilean Peso China CNY Yuan Renminbi China, Macao MOP Pataca China,H.Kong HKD Hong Kong Dollar China,Taiwan TWD New Taiwan Dollar Christmas Is AUD Australian Dollar Cocos Is AUD Australian Dollar Colombia COP Colombian Peso Comoros KMF Comoro Franc FAO Country Name ISO Currency Code* Currency Name* Congo Dem R CDF Franc Congolais Congo Rep XAF CFA Franc Cook Is NZD New Zealand Dollar Costa Rica -

List of Currencies of All Countries

The CSS Point List Of Currencies Of All Countries Country Currency ISO-4217 A Afghanistan Afghan afghani AFN Albania Albanian lek ALL Algeria Algerian dinar DZD Andorra European euro EUR Angola Angolan kwanza AOA Anguilla East Caribbean dollar XCD Antigua and Barbuda East Caribbean dollar XCD Argentina Argentine peso ARS Armenia Armenian dram AMD Aruba Aruban florin AWG Australia Australian dollar AUD Austria European euro EUR Azerbaijan Azerbaijani manat AZN B Bahamas Bahamian dollar BSD Bahrain Bahraini dinar BHD Bangladesh Bangladeshi taka BDT Barbados Barbadian dollar BBD Belarus Belarusian ruble BYR Belgium European euro EUR Belize Belize dollar BZD Benin West African CFA franc XOF Bhutan Bhutanese ngultrum BTN Bolivia Bolivian boliviano BOB Bosnia-Herzegovina Bosnia and Herzegovina konvertibilna marka BAM Botswana Botswana pula BWP 1 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Brazil Brazilian real BRL Brunei Brunei dollar BND Bulgaria Bulgarian lev BGN Burkina Faso West African CFA franc XOF Burundi Burundi franc BIF C Cambodia Cambodian riel KHR Cameroon Central African CFA franc XAF Canada Canadian dollar CAD Cape Verde Cape Verdean escudo CVE Cayman Islands Cayman Islands dollar KYD Central African Republic Central African CFA franc XAF Chad Central African CFA franc XAF Chile Chilean peso CLP China Chinese renminbi CNY Colombia Colombian peso COP Comoros Comorian franc KMF Congo Central African CFA franc XAF Congo, Democratic Republic Congolese franc CDF Costa Rica Costa Rican colon CRC Côte d'Ivoire West African CFA franc XOF Croatia Croatian kuna HRK Cuba Cuban peso CUC Cyprus European euro EUR Czech Republic Czech koruna CZK D Denmark Danish krone DKK Djibouti Djiboutian franc DJF Dominica East Caribbean dollar XCD 2 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Dominican Republic Dominican peso DOP E East Timor uses the U.S. -

ANNEX a to the 1998 FX and CURRENCY OPTION DEFINITIONS AMENDED and RESTATED AS of NOVEMBER 19, 2017 I

ANNEX A to the 1998 FX and Currency Option Definitions _________________________ Amended and Restated November 19, 2017 Amended March 16, 2020 INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. EMTA, INC. TRADE ASSOCIATION FOR THE EMERGING MARKETS Copyright © 2000-2020 by INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. EMTA, INC. ISDA and EMTA consent to the use and photocopying of this document for the preparation of agreements with respect to derivative transactions and for research and educational purposes. ISDA and EMTA do not, however, consent to the reproduction of this document for purposes of sale. For any inquiries with regard to this document, please contact: INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. 10 East 53rd Street New York, NY 10022 www.isda.org EMTA, Inc. 405 Lexington Avenue, Suite 5304 New York, N.Y. 10174 www.emta.org TABLE OF CONTENTS Page INTRODUCTION TO ANNEX A TO THE 1998 FX AND CURRENCY OPTION DEFINITIONS AMENDED AND RESTATED AS OF NOVEMBER 19, 2017 i ANNEX A CALCULATION OF RATES FOR CERTAIN SETTLEMENT RATE OPTIONS SECTION 4.3. Currencies 1 SECTION 4.4. Principal Financial Centers 6 SECTION 4.5. Settlement Rate Options 9 A. Emerging Currency Pair Single Rate Source Definitions 9 B. Non-Emerging Currency Pair Rate Source Definitions 21 C. General 22 SECTION 4.6. Certain Definitions Relating to Settlement Rate Options 23 SECTION 4.7. Corrections to Published and Displayed Rates 24 INTRODUCTION TO ANNEX A TO THE 1998 FX AND CURRENCY OPTION DEFINITIONS AMENDED AND RESTATED AS OF NOVEMBER 19, 2017 Annex A to the 1998 FX and Currency Option Definitions ("Annex A"), originally published in 1998, restated in 2000 and amended and restated as of the date hereof, is intended for use in conjunction with the 1998 FX and Currency Option Definitions, as amended and updated from time to time (the "FX Definitions") in confirmations of individual transactions governed by (i) the 1992 ISDA Master Agreement and the 2002 ISDA Master Agreement published by the International Swaps and Derivatives Association, Inc. -

Currencies of the World

The World Trade Press Guide to Currencies of the World Currency, Sub-Currency & Symbol Tables by Country, Currency, ISO Alpha Code, and ISO Numeric Code € € € € ¥ ¥ ¥ ¥ $ $ $ $ £ £ £ £ Professional Industry Report 2 World Trade Press Currencies and Sub-Currencies Guide to Currencies and Sub-Currencies of the World of the World World Trade Press Ta b l e o f C o n t e n t s 800 Lindberg Lane, Suite 190 Petaluma, California 94952 USA Tel: +1 (707) 778-1124 x 3 Introduction . 3 Fax: +1 (707) 778-1329 Currencies of the World www.WorldTradePress.com BY COUNTRY . 4 [email protected] Currencies of the World Copyright Notice BY CURRENCY . 12 World Trade Press Guide to Currencies and Sub-Currencies Currencies of the World of the World © Copyright 2000-2008 by World Trade Press. BY ISO ALPHA CODE . 20 All Rights Reserved. Reproduction or translation of any part of this work without the express written permission of the Currencies of the World copyright holder is unlawful. Requests for permissions and/or BY ISO NUMERIC CODE . 28 translation or electronic rights should be addressed to “Pub- lisher” at the above address. Additional Copyright Notice(s) All illustrations in this guide were custom developed by, and are proprietary to, World Trade Press. World Trade Press Web URLs www.WorldTradePress.com (main Website: world-class books, maps, reports, and e-con- tent for international trade and logistics) www.BestCountryReports.com (world’s most comprehensive downloadable reports on cul- ture, communications, travel, business, trade, marketing, -

IATA Rates of Exchange (IROE) ISO Local Deci ISO Code Other Lim Country Currency Name Code from NUC Curr

Page 1 Prepared by A. Khreis IATA Rates of Exchange (IROE) ISO Local Deci ISO Code Other Lim Country Currency Name Code From NUC Curr. mal Notes Numeric Charges Alpha Fares Units Afghanistan US Dollar USD 840 1.000000 1 0.1 2 + Afghanistan Afghani AFN 971 49.500000 1 1 0 2, 8 Albania euro EUR 978 0.810635 1 0.01 2 + Albania Lek ALL 8 NA 1 1 0 22 + Algeria Algerian Dinar DZD 12 86.906400 10 1 0 American Samoa US Dollar USD 840 1.000000 1 0.1 2 5 Angola US Dollar USD 840 1.000000 1 0.1 2 5 + Angola Kwanza AOA 973 101.834000 1 1 0 2, 8 Anguilla US Dollar USD 840 1.000000 1 0.1 2 5 Anguilla East Caribbean Dollar XCD 951 2.700000 1 0.1 2 2,5 Antigua Barbuda East Caribbean Dollar XCD 951 2.700000 1 0.1 2 2 Antigua Barbuda US Dollar USD 840 1.000000 1 0.1 2 5 Argentina US Dollar USD 840 1.000000 1 0.1 2 5 + Argentina Argentine Peso ARS 32 8.546600 1 0.1 2 1, 2, 5, Armenia euro EUR 978 0.810635 1 0.01 2 + Armenia Armenian Dram AMD 51 452.500000 1 1 0 8, 22 Aruba Aruban Guilder AWG 533 1.790000 1 1 0 Australia Australian Dollar AUD 36 1.199437 1 0.1 2 8, 17 Austria euro EUR 978 0.810635 1 0.01 2 + Azerbaijan Azerbaijanian Manat AZN 944 0.783840 0.01 0.1 2 8, 22 Azerbaijan euro EUR 978 0.810635 1 0.01 2 Bahamas US Dollar USD 840 1.000000 1 0.1 2 5 Bahamas Bahamian Dollar BSD 44 NA 1 0.1 2 2 Bahrain Bahraini Dinar BHD 48 0.376100 1 0.1 3 Bangladesh US Dollar USD 840 1.000000 1 0.1 2 5 + Bangladesh Taka BDT 50 77.311000 1 1 0 2,19 Barbados US Dollar USD 840 1.000000 1 0.1 2 5 + Barbados Barbados Dollar BBD 52 NA 1 0.1 2 2 + Belarus Belarussian Ruble -

Manama, Bahrain Destination Guide

Manama, Bahrain Destination Guide Overview of Manama First mentioned in Islamic chronicles in the year 1345, historical Manama is now the capital and largest city of Bahrain at the north-eastern tip of the Persian Gulf island state. There is a strong colonial influence in the area, with Portuguese occupation in 1521 followed by Persian dominance in 1602. This lovely city is a great base from which to enjoy the stunning beaches, buildings and sites in the area. The economy of Manama was traditionally based on pearling, fishing, boat building, and trade, displays of which can now be seen in local museums. In 1932, the discovery of petroleum boosted the city's economy, which has recently diversified into tourism and retail. Open-minded and tolerant of other cultures, Manama is visited by a large number of foreigners each year. These visitors can enjoy a vast array of attractions, from souks(markets) and shopping malls to forts and pearl museums. There is also an active nightlife with many popular restaurants, bars, and clubs to choose from, making this a splendid vacation destination. Key Facts Language: Arabic is the official language in Bahrain, although English is widely understood and is used by most businesses. Passport/Visa: All persons who wish to enter Bahrain need a visa, except citizens of the Gulf Cooperation Council (Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates). Visas can be obtained on arrival or online at www.evisa.gov.bh. Not all nationalities qualify for visas on arrival. A passport valid for duration of stay is required, but it is recommended that passports be valid for at least six months beyond intended travel. -

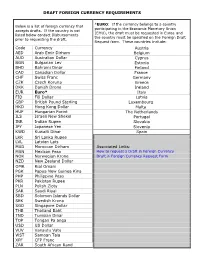

Below Is a List of Foreign Currency That Accepts Drafts

DRAFT FOREIGN CURRENCY REQUIREMENTS *EURO: If the currency belongs to a country Below is a list of foreign currency that participating in the Economic Monetary Union accepts drafts. If the country is not (EMU), the draft must be requested in Euros and listed below contact Disbursements the country must be specified on the Foreign Draft prior to requesting the draft. Request form. These countries include: Code Currency Austria AED Arab Emir Dirham Belgium AUD Australian Dollar Cyprus BGN Bulgarian Lev Estonia BHD Bahraini Dinar Finland CAD Canadian Dollar France CHF Swiss Franc Germany CZK Czech Koruna Greece DKK Danish Drone Ireland EUR Euro* Italy FJD Fiji Dollar Latvia GBP British Pound Sterling Luxembourg HKD Hong Kong Dollar Malta HUF Hungarian Forint The Netherlands ILS Israeli New Shekel Portugal INR Indian Rupee Slovakia JPY Japanese Yen Slovenia KWD Kuwaiti Dinar Spain LKR Sri Lanka Rupee LVL Latvian Lats MAD Moroccan Dirham Associated Links: MXN Mexican Peso How to request a Draft in Foreign Currency NOK Norwegian Krone Draft in Foreign Currency Request Form NZD New Zealand Dollar OMR Rial Omani PGK Papua New Guinea Kina PHP Philippine Peso PKR Pakistan Rupee PLN Polish Zloty SAR Saudi Riyal SBD Solomon Islands Dollar SEK Swedish Krona SGD Singapore Dollar THB Thailand Baht TND Tunisian Dinar TOP Tongan Pa anga USD US Dollar VUV Vanautu Vatu WST Samoan Tala XPF CFP Franc ZAR South African Rand . -

List of Currencies Sorted by Iso Currency Code and Country Or Area Name

ANNEX F.II LIST OF CURRENCIES SORTED BY ISO CURRENCY CODE AND COUNTRY OR AREA NAME Currency ISO code Currency name Country name AED UAE Dirham United Arab Emirates AFN Afghani Afghanistan ALL Lek Albania AMD Armeniam Dram Armenia ANG Netherlands Antillian Guilder Curaçao ANG Netherlands Antillian Guilder Sint Maarten AOA Kwanza Angola ARS Argentine Peso Argentina AUD Australian Dollar Australia AUD Australian Dollar Christmas Island AUD Australian Dollar Cocos (Keeling) Islands AUD Australian Dollar Kiribati AUD Australian Dollar Nauru AUD Australian Dollar Tuvalu AWG Aruban Florin Aruba AZN Azerbaijanian Manat Azerbaijan BAM Convertible Mark Bosnia and Herzegovina BBD Barbados Dollar Barbados BDT Taka Bangladesh BGN Bulgarian Lev Bulgaria BHD Bahraini Dinar Bahrain BIF Burundi Franc Burundi BMD Bermudian Dollar Bermuda BND Brunei Dollar Brunei Darussalam BOB Boliviano Bolivia (Plurinat.State) BRL Brazilian Real Brazil BSD Bahamian Dollar Bahamas BTN Ngultrum Bhutan BWP Pula Botswana BYN Belarusian Ruble Belarus BZD Belize Dollar Belize CAD Canadian Dollar Canada CDF Congolese Franc Congo, Dem. Rep. of the CHF Swiss Franc Liechtenstein CHF Swiss Franc Switzerland CLP Chilean Peso Chile CNY Yuan Renminbi China COP Colombian Peso Colombia CRC Costa Rican Colón Costa Rica CUP Cuban Peso Cuba CVE Cabo Verde Escudo Cabo Verde CZK Czech Koruna Czechia DJF Djibouti Franc Djibouti DKK Danish Krone Denmark DKK Danish Krone Faroe Islands DKK Danish Krone Greenland DOP Dominican Peso Dominican Republic DZD Algerian Dinar Algeria EGP Egyptian Pound -

Appendix N: Currency Codes

PERSHING STANDARD FILE LAYOUTS APPENDIX N: CURRENCY CODES USED IN THE FOLLOWING STANDARD FILES: ACCT/F, ALTI, AMSI, CAPS/CAPT, FT10, FT20, FT90, GACT/GAC1, GCUS/GCS1, GSDE/GTDE, GTOE, ISCA, OELG, SWFF CURRENCY CODE CURRENCY DESCRIPTION ADP Andorran Peseta AED United Arab Emirates (UAE) Dirham AFN Aghanistan Afgani (New) ALL Albania Lek AMD Armenia Dram ANG Netherlands Antilles Guilder AOA Angolan Kwanza ARS Argentine Peso ATS Austrian Shilling AUD Australian Dollar AWG Aruban Guilder AZM Azerbaijan Manat (New) BAM Bosnia and Herzegovina Convertible Marka BBD Barbados Dollar BDT Bangladesh Taka BEF Belgian Franc BGN Bulgarian Lev BHD Bahraini Dinar BIF Burundi Franc BMD Bermudian Dollar BND Brunei Darussalam Dollar BOB Bolivian Boliviano BRL Brazil Real BSD Bahamas Dollar BTN Bhutan Ngultrum BWP Botswana Pula BYR Belarus Ruble BZD Belize Dollar CAD Canadian Dollar CDF Congo/Kinshasa Franc CHF Switzerland (Liechtenstein) Franc CLP Chilean Peso CNY China Renminbi Pershing Proprietary Information Appendix N © 2018 Pershing LLC Page 1 Currency Codes 03-06-2018 PERSHING STANDARD FILE LAYOUTS CURRENCY CODE CURRENCY DESCRIPTION COP Colombian Peso CRC Costa Rican Colon CUP Cuban Peso CVE Cape Verde Escudo CYP Cypriot Pound CZK Czech Republic Koruna DEM German Mark DJF Djibouti Franc DKK Danish Krone DOP Dominican Republic Peso DZD Algerian Dinar ECS Ecuadoran Sucre EEK Estonian Kroon EGP Egyptian Pound ERN Eritrea Nakfa ESP Balearic Is Peseta ETB Ethiopian Birr EUR Euro FIM Finnish Markka FJD Fiji Dollar FKP Falkland Islands Pound FRF French Franc -

Important Notice

IMPORTANT NOTICE IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer applies to the attached base offering circular following this notice, and you are therefore advised to read this disclaimer carefully before reading, accessing or making any other use of the attached base offering circular (the “Base Offering Circular”). In accessing the Base Offering Circular, you agree to be bound by the following terms and conditions, including any modifications to them from time-to-time, each time you receive any information from the Issuer, the Arrangers or the Dealers (each as defined in the Base Offering Circular) as a result of such access. Confirmation of Your Representation: By accessing the Base Offering Circular you have confirmed to the Issuer, the Arrangers and the Dealers that (i) you understand and agree to the terms set out herein, (ii) you are either (a) a person who is outside the United States and that the electronic mail address you have given is not located in the United States, its territories and possessions, or (b) a person that is a “Qualified Institutional Buyer” (a “QIB”) within the meaning of Rule 144A under the U.S. Securities Act of 1933, as amended (the “Securities Act”), (iii) you consent to delivery by electronic transmission, (iv) you will not transmit the Base Offering Circular (or any copy of it or part thereof) or disclose, whether orally or in writing, any of its contents to any other person except with the consent of the Arrangers and the Dealers, and (v) you acknowledge that you will make your own assessment regarding any legal, taxation or other economic considerations with respect to your decision to subscribe for or purchase any of the Notes. -

2021 Currency Exchange Rates

2021 NRHA Currency Exchange Rates Must be used on all monies and fees pertaining to NRHA events. Refer to NRHA RESOLUTION #03-09. Mid Market Rates 2021-01-01 17:00 UTC Currency Unit Units per USD USD per Unit USD US Dollar 1 1.00000 EUR Euro 0.82301 1.21505 GBP British Pound 0.74108 1.34939 INR Indian Rupee 73.05904 0.01369 AUD Australian Dollar 1.30364 0.76708 CAD Canadian Dollar 1.27227 0.78600 SGD Singapore Dollar 1.32214 0.75635 CHF Swiss Franc 0.89159 1.12160 MYR Malaysian Ringgit 4.02250 0.24860 JPY Japanese Yen 103.21549 0.00969 CNY Chinese Yuan Renminbi 6.53059 0.15313 Currency Unit Units per USD USD per Unit AFN Afghan Afghani 77.57000 0.01289 ALL Albanian Lek 100.88309 0.00991 DZD Algerian Dinar 132.11383 0.00757 AOA Angolan Kwanza 654.56065 0.00153 ARS Argentine Peso 84.07071 0.01189 AMD Armenian Dram 522.58922 0.00191 AWG Aruban or Dutch Guilder 1.79000 0.55866 AUD Australian Dollar 1.30364 0.76708 AZN Azerbaijan Manat 1.69898 0.58859 BSD Bahamian Dollar 1.00000 1.00000 BHD Bahraini Dinar 0.37600 2.65957 BDT Bangladeshi Taka 84.67726 0.01181 BBD Barbadian or Bajan Dollar 2.00000 0.50000 LSL Basotho Loti 14.70662 0.06800 BYN Belarusian Ruble 2.61271 0.38274 BZD Belizean Dollar 2.01307 0.49675 BMD Bermudian Dollar 1.00000 1.00000 BTN Bhutanese Ngultrum 73.05904 0.01369 BOB Bolivian Bolíviano 6.88659 0.14521 BAM Bosnian Convertible Mark 1.60968 0.62124 BWP Botswana Pula 10.79050 0.09267 BRL Brazilian Real 5.19395 0.19253 GBP British Pound 0.74108 1.34939 BND Bruneian Dollar 1.32214 0.75635 BGN Bulgarian Lev 1.60968 0.62124 MMK