Infrastructure Investment & Finance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 Majalah Kiprah

MAJALAH KIPRAH 1 VOL 68 TH XV | JUN-JUL 2015 2 MAJALAH KIPRAH VOL 68 TH XV | JUN-JUL 2015 NUANSA KESIAPAN HUNIAN, INFRASTRUKTUR, KOTA DAN LINGKUNGAN INFRASTRUKTUR JALAN Dewan Redaksi: UNTUK MUDIK LEBARAN Setia Budhy Algamar Rido Matari Ichwan TEKS LISNIARI MUNTHE Amwazi Idrus Dedy Permadi AK terasa Lebaran sudah di depan mata. Tradisi mudik Lebaran merupakan Pemimpin Umum: tradisi tahunan dalam rangka pulang kampung, terutama oleh para pendatang Velix Wanggai Tyang tinggal di kota-kota besar ke tempat asal mereka. Fenomena mudik Lebaran adalah tradisi khas Indonesia yang memiliki ragam cerita menarik. Dan satu Pemimpin Redaksi: Lisniari Munthe hal yang tak dapat dipungkiri bahwa hingga saat ini pergerakan manusia antarkota ataupun kota-desa tersebut masih 90% bertumpu pada jaringan jalan. Sehingga Redaktur Pelaksana: selama mudik Lebaran, jaringan jalan yang ada menjadi andalan bagi pemudik Sambiyo • Djuwanto untuk melakukan pergerakan. Redaksi: Etty Winarni • Yunaldi • Warjono Rubrik Laporan Utama KIPRAH menyoroti tentang kesiapan dan pemantapan jalur • Krisno Yuwono utama mudik Lebaran. Menyadari pentingnya pelayanan dan kenyamanan mudik • Maretha Ayu K. • Gustav melewati infrastruktur jalan, Menteri Pekerjaan Umum dan Perumahan Rakyat (PUPR) • Rendhy • Noorman W • Marcelina Wahyuni • Tatiek Basuki Hadimuljono menginstruksikan kepada para Staf Ahli Menteri dan Pejabat Eselon 2 Kementerian PUPR untuk melakukan pemantauan kegiatan di sepanjang Editor: ruas jalan yang akan dilalui para pemudik. Kegiatan pemantauan itulah yang dapat Wayan Yoke • Endah Prihatiningtyas disimak dalam edisi KIPRAH kali ini, mulai dari jalur mudik di Pulau Sumatera, Jawa, • Hideko Kalimantan, Sulawesi, hingga Bali. Desain/Artistik: E Prananta • Eko Wahono Catatan penting dari Menteri PUPR Basuki Hadimuljono adalah pada H-30 hingga H+10 Idul Fitri kali ini, pekerjaan utama di badan jalan akan dihentikan dengan Fotografer: Suseno kondisi jalan dalam keadaan baik. -

Malaysia Berhad (Plus)

SUSTAINABILITY REPORT 2020 BREAKING THROUGH DISRUPTION TABLE OF CONTENTS ABOUT THIS REPORT 1 FROM OUR LEADERS 2 WE ARE PLUS 14 RISING TOGETHER - BRAVING THE 36 COVID-19 FIGHT OUR SUSTAINABILITY JOURNEY 48 OUR ENVIRONMENTAL STEWARDSHIP 60 OUR COMMITMENT TO SOCIETY 78 OUR STRENGTH OF OUR GOVERNANCE 116 OUR JOURNEY OF ACHIEVEMENTS 136 GRI CONTENT INDEX 147 MOVING FORWARD 149 COVER RATIONALE The cover for our inaugural voluntary Sustainability Report, themed ‘Breaking Through Disruption’, reflects our success in connecting people and communities, as well as providing a safe and comfortable journey to our customers despite the challenges faced in 2020. Furthermore, it underscores the vital role we play in Nation-building as we strive to deliver sustainable value not only for our business, but also for society and the environment as a whole. Set against the backdrop of over 1,130km of highways we manage in Peninsular Malaysia, the cover of this Sustainability Report visualises our purpose of Taking Good Care of You, Every Step of the Way. ABOUT THIS REPORT This is PLUS Malaysia Berhad’s (PLUS) inaugural Sustainability Report following the formalisation of our sustainability agenda and aspirations in 2020. In this Report, we disclose our approach to sustainability, the governance functions we have put in place, the matters identified as material to our business and our stakeholders, as well as the efforts we have taken to address those matters. This Report provides our stakeholders with a balanced and fair view on the value we created across the Environmental, Social and Governance (ESG) spectrum. It also steers us towards ingraining best practices in all aspects of our business to ensure its sustainability, as well as that of our stakeholders and the environment, as we aspire to lead by example as the Nation’s leading highway operator and a Government-Linked Company (GLC). -

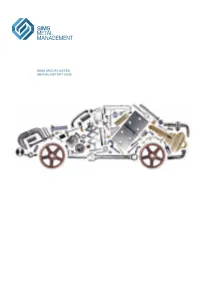

SIMS GROUP LIMITED Annual REPORT 2008 SIM S G R O U P L IM IT E D a N N U a L RE P O R T 2 0

SIMS GROUP LIMITED GROUP SIMS ANN U a L REPORT2008 L ThE average motor vEhIcle SIMS GROUP LIMITED Lasts 13.5 yEars anD comprises annUaL report 2008 approximately 15,000 IndividuaL Parts, Of whIch 80% are potentially recOverable. Approximately 68% Of a vEhIcle’S Parts by weighT aRE steel, followed by plastic (9%) anD nOn ferrous metals (8%), with ThE remaInder rubber, glass anD other materials. www.simsMM.cOM finanCiaL Summary Corporate DireCtory For the year ended 30 June 2008 SeCuritieS exChange LiSting Shareholder enquirieS The Company’s ordinary shares are quoted Enquiries from investors regarding their $7.67 b 38% $433m 81% 306¢ 60% 130¢ 8% on the Australian Securities Exchange under share holdings should be directed to: the ASX Code ‘SGM’. Computershare Investor Services Pty Limited TotaL REvEnue Profit after Tax EaRnIngs per ShaRE DIvidends per Share The Company’s American Depositary Shares Level 3 (ADSs) are quoted on the New York Stock 60 Carrington Street Exchange under the symbol ‘SMS’. The Company Sydney NSW 2000 has a Level II ADS program, and the Depositary Postal Address: is the Bank of New York Mellon Corporation. GPO Box 7045 ADSs trade under cusip number 829160100 Sydney NSW 2001 with each ADS representing one (1) ordinary Telephone: 1300 855 080 share. Further information and investor Facsimile: (02) 8235 8150 enquiries on ADSs may be directed to: Company SeCretarieS $181m 42% 14.6% 22% 10.9% 43% $8.02 72% The Bank of New York Mellon Corporation Frank Moratti Depositary Receipts Division Scott Miller Net caSh flowS Return -

Social Impact Insight Report December 2020

Vicinity Centres Social Impact Insight Report December 2020 Corporate Citizenship - LBG Australia & New Zealand Annual Company Benchmarking Report 2020 2020 Social Impact Insight Report Thank you for participating in the LBG benchmarking for 2020. The LBG methodology allows a company to form a reliable and holistic view of its community investment, from what is contributed, what happens and what changes as a result. LBG is the globally recognised methodology used by hundreds of the world’s leading companies to articulate and measure the positive impact they have in the world. The LBG Framework currently underpins the Community & Philanthropy question in the DJSI questionnaire, is reflected in the GRI standard and is recognised by the UN Global Compact as evidence for a company’s social impact narrative to stakeholders. LBG acts as a; • management tool, • a private benchmark, • and a network of professionals This report is designed to provide you with valuable benchmarking insights for program improvements. We encourage all members to arrange to meet with us to discuss the report in more detail and highlight the opportunities it demonstrates. The infographic page of this report acts as a summary of your results for you to use when sharing your results internally as well as a source of pointers where you could evolve your current program. The seismic events of 2020 such as Covid-19 and the Black Lives Matter movement have accelerated stakeholder expectations for companies to play a leading role in creating a more inclusive and robust society. The ‘S’ in ESG has become even more important. The fact that LBG is transforming in 2021 to provide a holistic management model is timely. -

Annual Report 2018 ABOUT CCB

Vision To become a first-class medium to large bank in Hong Kong Core Values Integrity Impartiality Prudence Mission Creation Provide better service to our customers Create higher value to our shareholders Build up broader career path for our associates Assume full responsibilities as a corporate citizen 28/F, CCB Tower, 3 Connaught Road Central Central, Hong Kong Tel: 3918 6939 www.asia.ccb.com CONTENTS About Us 02 About CCB 03 Our History 04 To Customers and Shareholders 06 Board of Directors and Executive Management 08 Subsidiary, Joint Venture and Associated Companies 15 Corporate Social Responsibility 16 Awards and Honors 22 Report of the Board of Directors 24 Independent Auditor’s Report 27 Consolidated Statement of Profit or Loss 34 Consolidated Statement of Comprehensive Income 35 Consolidated Statement of Financial Position 36 Consolidated Statement of Changes in Equity 38 Consolidated Statement of Cash Flows 40 Notes to the Consolidated Financial Statements 41 Unaudited Supplementary Financial Information 176 Service Network 205 This annual report is printed on environmentally friendly paper. ABOUT US China Construction Bank (Asia) China Construction Bank (Asia) Corporation Limited (“CCB (Asia)”) is the comprehensive and integrated commercial banking platform of China Construction Bank Corporation (“CCB”) in Hong Kong. Currently, CCB (Asia) has over 50 service outlets in Hong Kong and offers a wide array of banking products and services to customers, including consumer banking services, commercial banking services, corporate -

Fund Factsheet

31 August 2021 Russell Investments Managed Portfolio – Diversified 50 Asset allocation as at Portfolio objective 31 August 20212 To provide returns over the medium term, with moderate volatility, consistent with a diversified mix of defensive and growth oriented assets. Portfolio strategy The Portfolio typically invests in a diversified investment mix with exposure to growth investments of around 50% and defensive investments of around 50% over the long term, however the allocations will be actively managed within the allowable ranges depending on market conditions. Performance review Period ending 31/08/2021 1 3 1 2 3 5 Since month months year years years years inception % % % p.a. % p.a. % p.a. % p.a. % p.a. Total return 1.5 4.3 15.4 7.5 _ _ 7.8 Performance is net of fees and charges. Assumes reinvestments of income. Past performance is not a reliable indicator of future performance. Fund Facts Growth of $10,000 Inception date 19 June 2019 Portfolio manager Daniel Choo Recommended investment timeframe 4 years Fund Performance results are net of management fees for both the Managed Portfolio and the underlying managers’ fees and costs. These results do not take into account any third party platform fees charged to individual investors or transaction costs (which include buy/sell spread and brokerage fees). They assume income received is reinvested without any tax deduction. An individual investor’s actual performance will differ from this performance depending on a range of factors including the amount invested in the Managed Portfolio, transaction timing, transaction costs, actual underlying manager fees and costs, any exclusions selected by the investor, whether income is paid in cash and any divergence by the investor from Managed Portfolio weightings. -

Stocks List U Ethical Australian Equities Portfolio

All stocks list U Ethical Australian Equities Portfolio Below is a list of all holdings within the portfolio as at 31 March 2019. Stock holdings The A2 Milk Company G8 Education Reliance Worldwide Amcor Goodman Group ResMed Australia and New Zealand Banking GUD Holdings Seek Group Bingo Industries Invocare Sonic Healthcare Bluescope Steel JB Hi-Fi Suncorp Group Boral Lendlease Group Transurban Group Carsales.com Macquarie Group Telstra Challenger Monash IVF Group Wesfarmers Coles Oil Search Westpac Banking Corporation Commonwealth Bank of Australia QBE Insurance Group Woodside Petroleum CSL Ramsay Health Care Fortescue Metals Group REA Group This document dated 31 March 2019 is issued by UCA Growth Fund Limited (UCA Growth) for the U Ethical Australian Equities Portfolio (the Portfolio). U Ethical (a registered business name of Uniting Ethical Investors Limited ABN 46 102 469 821 AFSL 294147) is the Manager and Administrator of the Portfolio. The information provided is general information only. It does not constitute financial, tax or legal advice or an offer or solicitation to subscribe for units in any fund of which U Ethical is the Manager, Administrator, Issuer, Trustee or Responsible Entity. This information has been prepared without taking account of your objectives, financial situation or needs. Before acting on the information or deciding whether to acquire or hold a product, you should consider the appropriateness of the information based on your own objectives, financial situation or needs or consult a professional adviser. You should also consider the relevant Product Disclosure Statement (PDS) or Offer Document which can be found on our website www.uethical.com or by calling us on 1800 996 888. -

EQUITIES MTR Corporation Ltd (66 HK) CONGLOMERATES

8 March 2017 EQUITIES MTR Corporation Ltd (66 HK) CONGLOMERATES Reduce: Resilient business but stock is fully valued Hong Kong FY16 underlying earnings ahead on property development; MAINTAIN REDUCE recurrent earnings was in-line with expectation. Strong land tender pipeline to capture Mainland demand TARGET PRICE (HKD) PREVIOUS TARGET (HKD) 35.00 33.50 Maintain Reduce, but raise TP to HKD35 (from HKD33.5) SHARE PRICE (HKD) UPSIDE/DOWNSIDE Resilient core business, but stock is fully valued. MTR’s underlying earnings 41.45 -15.6% came in ahead of our expectation; recurrent profit (which excludes property (as of 07 Mar 2017) development) was in-line with our expectation. Outlook for the core business remains resilient, with full-year contribution from the new lines underpinning patronage and MARKET DATA Market cap (HKDm) 244,790 Free float 24% EBITDA growth in 2017e, despite having a negative impact on net profit due to Market cap (USDm) 31,526 BBG 66 HK depreciation charges. Despite stable fundamentals, we see potential downside to the 3m ADTV (USDm) 16 RIC 0066.HK stock given premium valuation, with the stock trading at close to par with our NAV, or FINANCIALS AND RATIOS (HKD) 27x 2017e PE, while offering a 2.7% (excl. special) dividend yield. Year to 12/2016a 12/2017e 12/2018e 12/2019e HSBC EPS 1.61 1.53 1.49 1.60 FY16 earnings ahead on property development. MTR reported FY16 underlying HSBC EPS (prev) 1.56 1.55 1.48 - Change (%) 3.2 -1.3 0.7 - earnings of HKD9,446m, down 13% y-o-y, and 3%/4% above consensus/HSBC Consensus EPS 1.58 1.61 1.64 - estimate. -

PPP Case Studies – People's Republic of China

1 PPP Case Studies People’s Republic of China Craig Sugden, Principal PPP Specialist East Asia Department 13 May 2015 The views expressed in this presentation are the views of the author and do not necessarily reflect the views or policies of the Asian Development Bank Institute (ADBI), the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. 2 Background PPP Case Studies: the PRC PRC’s PPP projects 3 EIU’s 1,186 infrastructure PPPs finalised in the Infrascope PRC from 1990 to 2014 highlighted the PRC’s Compared to 838 in India, 126 in the Philippines, 108 in Indonesia, 73 in Sri Lanka, “phenomenal” 65 in Bangladesh wealth of project 648 active PPPs in the UK, 567 in the experience Republic of Korea, 127 in Australia (as of 2013) Source: World Bank. 2015. Private Participation in Infrastructure Projects Database and Burger P. and I. Hawkesworth. 2013. Capital Budgeting and Procurement Practices. Organization for Economic Cooperation and Development. Paris. PPP Case Studies: the PRC PPP activity in the PRC 4 Note: Excludes projects that are led by a majority-state owned enterprise Source: World Bank PIAF Database and IMF PPP Case Studies: the PRC Case studies 5 • Beijing Subway Line 4 The PRC has • Shanghai Huadian Xinzhuang Industrial Park combined cycle heat and power project • Baiyinchagan-Yongtaigong -

12 December 2017 Cimic's Cpb Contractors to Construct

12 DECEMBER 2017 CIMIC’S CPB CONTRACTORS TO CONSTRUCT WEST GATE TUNNEL CIMIC Group company, CPB Contractors, has achieved contractual close on Victoria’s multi- billion dollar West Gate Tunnel. CPB Contractors was selected by Transurban and the State Government of Victoria as the preferred contractor for the project in April 2017, in a 50:50 joint venture with John Holland. The design and construct contract will generate revenue to CPB Contractors of approximately $2.49 billion. Major construction work is expected to start in early 2018 with the project scheduled to open to traffic in 2022. CIMIC Group Chief Executive Officer Michael Wright said: “Delivering complex roads and transport projects are core capabilities for CIMIC and CPB Contractors. We are the largest tunnelling contractor in Australia, with considerable experience in creating transforming infrastructure such as the West Gate Tunnel. “We are privileged to be working with Transurban and the Victorian Government to deliver this exciting project that is so integral to the State’s vision for sustainable roads systems, and so vitally important for its people and communities.” CPB Contractors Managing Director Juan Santamaria said: “With many decades of roads and tunnelling experience in Australia, our capabilities will ensure minimal disruption, a safe and effective works program, and certainty of delivery for our client. “We are focused on ensuring opportunities for local workers, and providing a value for money procurement program that includes Indigenous business and social enterprises to achieve broader community benefits.” The West Gate Tunnel project, one of Victoria’s largest ever urban road projects, will deliver a vital alternative to the West Gate Bridge, provide quicker and safer journeys, and remove thousands of trucks from residential streets. -

MTR Corporation (66 HK) EQUITIES

Flashnote 6 January 2017 EQUITIES MTR Corporation (66 HK) CONGLOMERATES Reduce: Outlook remains lacklustre Hong Kong Pre-blackout meeting confirmed lacklustre business outlook REDUCE Valuation still rich despite recent share price weakness TARGET PRICE (HKD) PREVIOUS TARGET (HKD) Maintain Reduce with an unchanged TP of HKD33.5 33.50 Pre-blackout meeting provided little encouragement. MTR hosted a pre-blackout SHARE PRICE (HKD) UPSIDE/DOWNSIDE analyst meeting on 5 January 2017 in which management outlined the company’s 38.30 -12.5% performance in 2H16 and its outlook for 2017. We saw little evidence of a significant (as of 04 Jan 2017) improvement in MTR’s fundamental outlook over our current expectation. Share price MARKET DATA has been weak in recent months, but the stock remain expensive in our view, trading Market cap (HKDm) 226,155 Free float 24% at a 4% discount to our NAV estimate, or 25x 2017e PE, despite flat earnings growth Market cap (USDm) 29,162 BBG 66 HK 3m ADTV (USDm) 22 RIC 0066.HK to 2018e and offering just a 2.9% regular dividend yield in 2017e (based on the current share price on an ex-div basis, i.e. after the upcoming special dividend FINANCIALS AND RATIOS (HKD) (HKD2.2/sh) in July). Year to 12/2015a 12/2016e 12/2017e 12/2018e HSBC EPS 1.87 1.56 1.55 1.48 HSBC EPS (prev) - - - - Core business outlook remains lacklustre. 1) patronage growth remained sluggish Change (%) - - - - in 2H16 (+0.4% through 11M16, vs +0.2% in 1H16) and we expect organic patronage Consensus EPS 1.83 1.55 1.65 1.65 PE (x) 20.5 24.6 24.7 -

PLUS EXPRESSWAYS BERHAD 13 September 2011 COUNTRY OVERVIEW

THE WORLD, Expansion and Modernization of Road Infrastructure II by PLUS EXPRESSWAYS BERHAD 13 September 2011 COUNTRY OVERVIEW COMPANY OVERVIEW MAJOR PROGRAM/ PROJECT IN THE COUNTRY INDUSTRY CHALLENGES PLUS North-South Expressway, Kuala Lumpur bound 2 Country Overview Land area: 329,847 square kilometres (127,350 sq mi) separated by the South China Sea into two regions, Peninsular Malaysia and Malaysian Borneo (slightly smaller than the size of Germany and slightly bigger than Italy). Land borders: Thailand, Indonesia, and Brunei Population 2010: 27,565,821 (Department of Statistics Malaysia) GDP (PPP) : USD442.01 billion - 2010 est (Source: IMF) GDP per capita : USD8,620 - 2010 est (Source: IMF) 3 GDP Growth 2010: 7.2% Country Overview MALAYSIA GDP GROWTH 2000-2011 (est) POPULATION IN MALAYSIA 10.0% 8.3% 30.0 27.1 27.6 7.1% 7.2% 25.0 8.0% 6.3% 5.3% 25.0 22.3 5.2% 6.0% 4.2% 4.6% 19.6 20.0 17.2 5.9% 15.0 4.0% 5.0% 13.2 15.0 11.7 2.0% 10.3 Million 10.0 GDPGrowth 0.0% 0.4% 5.0 -2.0% -1.7% 0.0 -4.0% NEW VEHICLES REGISTERED IN MALAYSIA NUMBER OF TOURIST ARRIVALS IN MALAYSIA 30.0 600 552 548 523 23.6 491 503 25.0 20.9 435 488 487 500 24.6 396 406 20.0 22.0 400 343 15.7 15.0 13.2 17.4 300 16.4 Million 200 10.0 12.7 10.2 10.5 Thousand Vehicles Thousand 100 5.0 0 0.0 COUNTRY OVERVIEW COMPANY OVERVIEW MAJOR PROGRAM/ PROJECT IN THE COUNTRY INDUSTRY CHALLENGES Persada PLUS, Corporate Office 5 Primary toll road operator in Malaysia As at 12 May 2011 # 15.5% 100% r 38.5% Domestic 100% 100% 100% 100% 100% 100% 20% Projek Lebuhraya Expressway Linkedua