The Retail Absorption of Sears and Target's Former

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Niche Market Study Beaumont, Alberta

TOWN OF BEAUMONT NICHE MARKET STUDY FINAL REPORT June 24, 2011 1 NICHOLS Applied Management Table of Contents Page 1. Introduction – The Importance of Community Sustainability 3 2. Retail and Commercial Expenditure Pattern Survey and Analysis 6 3. Economic Development Opportunities Roadmap 24 4. Key Objectives 32 5. High-Potential Growth Areas 37 6. Priorities, Directions and Recommended Action Items 44 2 NICHOLS Applied Management 1. Introduction – The Importance of Community Sustainability Retention and growth of existing businesses, new business attraction, jobs, investment, residential development and new commercial/industrial assessment – these are just some of the benefits to be realized through a well-focused economic and community development strategy. They are also essential, some would say critical, for the Town of Beaumont at this point in time. Long term community sustainability depends on the ability to maintain a healthy balance and harmony between economic, municipal fiscal/financial, social and environmental sustainability. While each is equally important, many would argue that economic sustainability is the ‘engine’ that ultimately drives and sustains a community. Building Blocks of a Sustainable Community 3 NICHOLS Applied Management Research has shown that ‘communities of choice’ are increasingly replacing ‘communities of necessity’ for many highly-skilled workers in the more suburban parts of North America. These individuals are increasingly looking to live in affordable, high quality of life communities – with excellent recreational amenities and clean, safe and family-oriented neighbourhoods – but they are also looking to minimize commuting times associated with travel to and from work. Beaumont’s well-developed social and community infrastructure, natural environment and close proximity to Alberta’s main urban centres all contribute to the Town’s overall quality of life. -

Best Shopping Centers/Malls in Edmonton"

"Best Shopping Centers/Malls in Edmonton" Created by: Cityseeker 5 Locations Bookmarked Edmonton City Centre "Shop Till You Drop" Edmonton City Centre is where you can head to if you are looking to spend your precious vacation time shopping. For this City Centre is a one stop shopping hub with an wide array of shops to get all your shopping done in a jiffy. The mall has stores which sell varied items like groceries, clothes, accessories and kitchenware to name a few, as also chocolates by IQRemix and cakes. Multiple restaurant options lined up within the premises help satiate your hunger after a tiring shopping spree. After you are done for the day, your weary bones will not have to drag the heavy bags to the public car park, for they have a private one in the basement. +1 780 426 8444 www.edmontoncitycentre. edmontoncitycentre@oxfor 10088 102A Avenue com/ dproperties.com Northwest, Edmonton AB Kingsway Mall "Fit For a King" Situated in close proximity to Edmonton's Downtown district, the Kingsway Mall has approximately 250 top stores including one of the few Disney stores in Edmonton. There are a host of other stores catering to fashion, children's wear, electronics, gifts, health and beauty and footwear apart from a range of dining options. The mall itself is a low-slung, three- by mastermaq story turreted brickwork building with a glass front. Ample parking is available. +1 780 477 5756 www.kingswaymall.com/ sdenney@oxfordproperties 109 Street Northwest, .com Edmonton AB Southgate Centre "Refurbished Mall" The Southgate Centre Mall is located to the south and over the river from Edmonton's downtown district, just to the north of the major Whitemud Drive Highway. -

Quebec, Canada

MIRABEL (MONTRÉAL), QUEBEC, CANADA PROPERTY OVERVIEW PREMIUM OUTLETS® –MONTRÉAL JOINT VENTURE WITH CALLOWAY REAL ESTATE INVESTMENT TRUST AND SMART CENTRES MIRABEL (MONTRÉAL), QUEBEC, CANADA MAJOR METROPOLITAN AREAS SELECT TENANTS MONT-TREMBLANT Montréal: 24 miles Hudson’s Bay Outlet, Bench, Calvin Klein Company Store, Coach, 15 40 The Cosmetics Company Store, David’s Tea, Desigual, Diesel, Gucci, CANADA 30 HUGO BOSS, Jack & Jones, LACOSTE Outlet, Levi’s Outlet Store, 640 RETAIL 55 MIRABEL MaxMara, Michael Kors Outlet, Polo Ralph Lauren Factory Store, Puma, MONTRÉAL 520 GLA (sq. ft.) 366,000 Rudsak, Sarah Pacini, Vans 417 10 OTTAWA 20 15 OPENING DATES MARKET INFORMATION / TOURISM Opened October 2014 VT Montréal is the largest city in the province of Quebec, the second largest NY city in Canada, and the 15th largest in North America. Montréal is located RADIUS POPULATION in the southwest of the Quebec province at the confluence of the Saint Lawrence Seaway and the Ottawa River. Montréal has an estimated 10 miles: 474,470 PREMIUM OUTLETS– metropolitan area population of about four million residents which ranks MONTRÉAL 25 miles: 3,642,393 as the second most populous city in Canada and the 10th most populous MIRABEL (MONTRÉAL), 50 miles: 4,575,120 city in North America. With the second largest economy in Canada and QUEBEC, CANADA the 41st in the world, Montréal is an important center of commerce, AVERAGE HH INCOME finance, technology, and world affairs. 10 miles: $82,588 The Port of Montréal is the largest inland port in the world. Montréal 25 miles: $72,783 is home to 11 institutions of higher learning and has the highest 50 miles: $73,103 concentration of post-secondary students of all major cities in North America. -

Liste Des Immeubles Nom De L'immeuble / Building's Name Adresse / Address Ville / City Code Postal / Postal Code 1001, Rue Sherb

Liste des immeubles Nom de l'immeuble / Building's name Adresse / Address Ville / City Code postal / Postal Code 1001, rue Sherbrooke 1001, rue Sherbrooke Montréal h2l 1l3 1100, boulevard René-Lévesque 1100, boulevard René-Lévesque Ouest Montréal H3B 4N4 1250, boulevard René-Lévesque 1250, boulevard René-Lévesque Ouest, 27e étage Montréal H3B 4W8 150 des commandeurs 150 des commandeurs Lévis g6v8m6 2001 Robert-Bourassa 2001 Robert-Bourassa Montreal H3A 2A6 204, boul. de Montarville 204, boul. de Montarville Boucherville J4B 6S2 600 de Maisonneuve Ltée (Tour KPMG) 600, boul. de Maisonneuve Ouest, bureau 510 Montréal H3A 3J2 7001, boul. St-Laurent 7001, boul. St-Laurent Montréal H2S 3E3 85, St-Charles Ouest 85, St-Charles Ouest Longueuil J4H 1C5 ALLIED - 111 boulevard Robert-Bourassa 75 rue Queen, Bureau 3100 Montreal H3C 2N6 ALLIED – 50 Queen 75 rue Queen, Bureau 3100 Montreal H3C 2N6 ALLIED - 5445 avenue de Gaspé 5445 avenue de Gaspé, Bureau 250 Montreal H2T 3B2 ALLIED - 5455 avenue de Gaspé 5445 avenue de Gaspé, Bureau 250 Montreal H2T 3B2 ALLIED - 5505 ST-LAURENT 75 rue Queen, Bureau 3100 Montreal H3C 2N6 ALLIED - 6300 Avenue du Parc 6300 Avenue du Parc Montreal H2V 4S6 ALLIED – 700 Wellington & 75 Queen 75 rue Queen, Bureau 3100 Montreal H3C 2N6 ALLIED – 80 Queen & 87 Prince 75 rue Queen, Bureau 3100 Montreal H3C 2N6 Carrefour du Nord-Ouest 1801 3e Avenue Val-d'Or j9p5k1 Centre d'affaires le Mesnil 1170, boul. LeBourgneuf Québec G2K 2E3 Centre de commerce mondial de Montréal 380, rue Saint-Antoine Ouest, bureau 1100 Montréal H2Y 3X7 Centre Manicouagan 600 boul. -

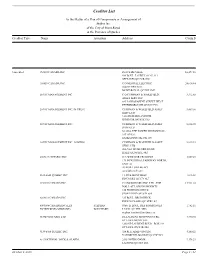

Allcreditorlist - 2020 09 08, 3

Dynamite - AllCreditorList - 2020 09 08, 3 Creditor Address1 Address2 Address3 Address4 Address5 1 Model Management, LLC 42 Bond St, 2nd Fl New York, NY 10012 10644579 Canada Inc 5592 Ferrier St Mount Royal, QC H4P 1M2 Canada 10644579 Canada Inc 5592 Ferrier St Mount-Royal, QC H4P 1M2 Canada 10927856 Canada Inc Apt 4, 7579 Rue Edouard Lasalle, QC H8P 1S6 Canada 11429876 Canada Inc 10 Ocean Ridge Dr Brampton, ON L6R 3K6 Canada 11588524 Canada Inc 4291 Rue Messier Montreal, QC H2H 2H6 Canada 1367826 Ontario Ltd 319 Brooke Ave Toronto, ON M5M 2L4 Canada 167081 Canada Inc 1625 Chabanel St, Ste 600 Montreal, QC H4N 2S7 Canada 174541 Canada Inc Laveurs De Vitres De L'Outaouais Inc 251 Rue Laramee Gatineau, QC J8Y 2Z4 Canada 1-800-Got-Junk? 887 Great Northern Way, Suite 301 Vancouver, BC V5T 4T5 Canada 1-800-Got-Junk? 9 Dibble St Toronto, ON M4M 2E7 Canada 1-800-Got-Junk? Commercial Services (Usa) LLC Dept 3419, P.O. Box 123419 Dallas, TX 75312-3419 1Ds Collective 11935 King St No. 22 Valley Village, CA 91607 1St Mechanical Services 303 Urie Dr Alpharetta, GA 30005 2422745 Ontario Inc 66 Sanders Dr Markham, ON L6B 0M3 Canada 2521506 Ontario Inc 120 Birkdale Rd Scarborough, ON M1P 3R5 Canada 2615476 Ontario Inc 169 Westphalia Ave Kianata, ON K2V 0E3 Canada 2Dev Inc 375-4000 Rue Saint-Ambroise Montreal, QC H4C 2C7 Canada 2Kw Enterprises LLC P.O. Box 5923 Concord, CA 94524 3249026 Canada Inc-Total Events 2360, 23E Ave Lachine, QC H8T 0A3 Canada 437 Inc (Adrien Bettio) 602 Richmond St W Toronto, ON M5V 1Y9 Canada 4450329 Canada Inc 5592, Rue Ferrier Ville Mont-Royal, QC H4P 1M2 Canada 5025045 Ontario Inc (Old 105620) 5387 Pl Belfield Montreal, QC 751797473 Canada 6053726 Canada Inc O/A Fuze Reps 69 Pelham Ave Toronto, ON M6N 1A5 Canada 7000766 Canada Inc 9655 Meilleur St Montreal, QC H3L 0A1 Canada 713949 Ontario Ltd Ottawa Management Office 1200 StLaurent Blvd Box 199 Ottawa, ON K1K 3B8 Canada 7599978 Canada Inc 54 Rue St-Jaques St. -

Reaching Over 5 Million People, Minutes on the Contest Page and Growing Their Facebook Fan Base

ICSC CANADIAN SHOPPING CENTRE AWARDS PRESENTS Reaching N E W Heights SEPTEMBER 23, 2014 2014 AWARD WINNERS GOLDEN MOMENT Congratulations to this year’s ICSC Award winners and nominees for their outstanding achievements in excellence and innovation. Oxford Properties Group portfolio includes office developments in major urban centres, luxury resort hotels across the country, and some of Canada’s most prestigious shopping centres. SQUARE ONE, SOUTHCENTRE, SCARBOROUGH TOWN CENTRE, YORKDALE, KINGSWAY MALL, PROMENADES CATHÉDRALE, HILLCREST MALL, UPPER CANADA MALL, LES PROMENADES GATINEAU, EDMONTON CITY CENTRE, LES GALERIES DE LA CAPITALE www.oxfordproperties.com 2014 CANADIAN SHOPPING CENTRE AWARD WINNERS The ICSC Canadian Shopping Centre Awards are designed to honour our industry’s brightest and best. The Awards bring information and insight to the entire industry on what it takes to achieve high levels of success. MARKETING ADVERTISING Centres 150,000 to 400,000 sq. ft. of total retail space SILVER SILVER Get Your Red On It’s The Little Things Cottonwood Mall Eglinton Square Shopping Centre Chilliwack, British Columbia Toronto, Ontario Management Company: Morguard Management Company: Bentall Kennedy (Canada) LP Owner: 2046459 Ontario Inc. Owner: Kingsett Capital Investments Cottonwood Mall had three events wrapped in an effective ad Eglinton Square’s 2013 campaign “It’s The Little Things” was the answer campaign titled “Get Your Red On” which reduced the creative and to a demographic shift in the PTA that saw young families moving into placement costs. The combined media mix drove over 3.2 million post-war bungalows. Family traffic and related tenant sales grew in audience impressions, 9.5% more than projected, and retail sales the double-digits by altering the Centre’s voice to one that was more volume increased an incredible 12.3% for November and 8.6% for family-oriented. -

Court File No.: CV-15-10832-00CL

Court File No.: CV-15-10832-00CL ONTARIO SUPERIOR COURT OF JUSTICE COMMERCIAL LIST IN THE MATTER OF THE COMPANIES’ CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED AND IN THE MATTER OF A PLAN OF COMPROMISE OR ARRANGEMENT OF TARGET CANADA CO., TARGET CANADA HEALTH CO., TARGET CANADA MOBILE GP CO., TARGET CANADA PHARMACY (BC) CORP., TARGET CANADA PHARMACY (ONTARIO) CORP. TARGET CANADA PHARMACY CORP., TARGET CANADA PHARMACY (SK) CORP., AND TARGET CANADA PROPERTY LLC. THIRD REPORT OF THE MONITOR ALVAREZ & MARSAL CANADA INC. FEBRUARY 27, 2015 TABLE OF CONTENTS 1.0 INTRODUCTION.......................................................................................................................... 1 2.0 TERMS OF REFERENCE AND DISCLAIMER ....................................................................... 4 3.0 REAL PROPERTY PORTFOLIO SALES PROCESS ............................................................. 6 4.0 LEASE TRANSACTION AGREEMENT ................................................................................... 6 5.0 TERMINATION OF THE SUBLEASE/LEASEBACK ARRANGEMENTS WITH TARGET CANADA PROPERTY LLC .................................................................................... 16 6.0 CASH FLOW RESULTS RELATIVE TO FORECAST ......................................................... 18 7.0 MONITOR’S ACTIVITIES ....................................................................................................... 20 8.0 MONITOR’S RECOMMENDATION ..................................................................................... -

Retail Snapshot Q2 2016 Edmonton, AB

MARKETBEAT Retail Snapshot Q2 2016 Edmonton, AB ECONOMIC INDICATORS Spending per person in Alberta is still well above the average for Canada. The national average for spending in March 2016 was National 12-Month $1,214 per person whereas Albertans spent $1,433 – the highest 2015 2016F Forecast amongst all of the provinces. Restaurants and bars remained GDP Growth 1.1% 1.4%* stable in Q2 despite the current downturn, with Albertans CPI Growth 1.1% 1.6%* spending upwards of $720 million in March 2016 alone. Alberta Consumer Spending will see a shift in the restaurant and bar industry resulting in the 1.9% 2.1%* Growth demand for different offerings and concepts. The retail industry Retail Sales Growth 1.7% 3.4%* as a whole has continued to see a shift away from mid-priced retailers. A clear divide in consumer spending has become glaringly obvious where we are seeing strong growth exhibited in 12-Month Regional 2015 2016F Forecast polar opposite segments of the retail market – extreme discount Household Income $104,113 $117,416* retailers and luxury and premium priced retailers. Population Growth 1.9% 1.2%* Outlook Unemployment 5.8% 7.9%* Edmonton has seen some popular additions to its fashion Sources: RBC Economics, Scotia Economics, Finance Ministry of Alberta *2016 industry. Londonderry Mall will be home to Edmonton’s second Forecast Simons department store, with a scheduled opening in Q4 2017, while Saks Fifth Avenue is entering the Edmonton market with two of its “Saks Off Fifth” outlet stores. One will be located in Economy South Edmonton Common (opening Q3 2016) and the other at While most of Alberta’s economy continues to adjust to lower oil Skyview Power Centre (opening Q2 2017). -

Products Offered by Mall

PRODUCTS OFFERED BY MALL 24-09-2021 Page 1 of 8 100+ SHOPPING MALLS 660+ HD SCREENS 700+ POSTERS & BANNERS Toll free 1-877-987-2334 In 8 provinces Across Canada From coast to coast www.neo-ooh.com ONTARIO KINGSTON - BELLEVILLE ANNUAL DIGITAL SPECIALTY DIGITAL 3 MALLS BANNERS POSTERS TRAFFIC DISPLAYS MEDIA SPECTACULAR Cataraqui Centre Kingston 6,000,000 X X X X Lansdowne Place Peterborough 5,000,000 X X X X Quinte Mall Belleville 3,909,400 X X X X NORTH WESTERN ONTARIO ANNUAL DIGITAL SPECIALTY DIGITAL 1 MALL BANNERS POSTERS TRAFFIC DISPLAYS MEDIA SPECTACULAR Heritage Place Owen Sound 3,600,000 X X OTTAWA ANNUAL DIGITAL SPECIALTY DIGITAL 4 MALLS BANNERS POSTERS TRAFFIC DISPLAYS MEDIA SPECTACULAR Billings Bridge Ottawa 7,500,000 X X X X Carlingwood Shopping Ottawa 7,800,000 Centre X X X X CF Rideau Centre Ottawa 18,000,000 X X Place D’Orleans Ottawa 5,824,000 X X X X SOUTH WESTERN ONTARIO ANNUAL DIGITAL SPECIALTY DIGITAL 7 MALLS BANNERS POSTERS TRAFFIC DISPLAYS MEDIA SPECTACULAR CF Lime Ridge Hamilton 9,432,885 X X CF Masonville London 6,786,675 Place X X Devonshire Windsor 7,088,550 X X X X X Eastgate Square Stoney Creek 8,008,000 X Lambton Mall Sarnia 4000000 X X Lynden Park Brantford 3,847,068 X X Tecumseh Windsor 3,450,000 X X X 24-09-2021 Page 2 of 8 100+ SHOPPING MALLS 660+ HD SCREENS 700+ POSTERS & BANNERS Toll free 1-877-987-2334 In 8 provinces Across Canada From coast to coast www.neo-ooh.com TORONTO (GTA) ANNUAL DIGITAL SPECIALTY DIGITAL 16 MALLS BANNERS POSTERS TRAFFIC DISPLAYS MEDIA SPECTACULAR Bathurst College Toronto 1 047 800 Centre X Burlington Centre Burlington 5,452,521 X X X CF Fairview Mall Toronto 14,100,000 X X X CF Markville Markham 9,817,149 Shopping Centre X X Dixie Outlet Mall Mississauga 4,615,236 X X X X Dufferin Mall Toronto 10,886,074 X X X X X Eglinton Square Scarborough 3,000,000 X X X Erin Mills Town Mississauga 9,000,000 Centre X X X X X Georgian Mall Barrie 5,665,163 X X X Oakville Place Oakville 3,780,099 X X X One Queen Street Toronto 2,964,000 X X X X Pen Centre St. -

THE FUTURE of RETAIL in DOWNTOWN EDMONTON DOWNTOWN BUSINESS ASSOCIATION of EDMONTON 10121 Jasper Ave NW Edmonton, AB T5J 4X6

2018 THE FUTURE OF RETAIL IN DOWNTOWN EDMONTON DOWNTOWN BUSINESS ASSOCIATION OF EDMONTON 10121 Jasper Ave NW Edmonton, AB T5J 4X6 www.edmontondowntown.com To Support, Connect, and Enrich Edmonton’s Downtown Community REPORT RESEARCHED AND WRITTEN BY: Mohammed Siddique Photo Credit: Jeff Wallace CONTENTS 2 Introduction 3 Methodology 01. BACKGROUND 4 History of Shopping 5 Shifts in the Customer Shopping Habits 02. DOWNTOWN PROFILE 8 Downtown Profile 11 Retail in Downtown 03. SURVEY & ANALYSIS 14 Survey & Analysis 04. STRATEGIES FOR RETAIL 28 Strategies for Retail 30 Popular Retail Streets in Canada 32 Key Takeaways 34 Think Residential DOWNTOWN BUSINESS ASSOCIATION 2018 REPORT 1 INTRODUCTION The Downtown Business Association (DBA) of Edmonton is proud to be providing value to our members and wants to ensure that we continue channelling our efforts to make Downtown more vibrant and inviting. Every year since 2004, the DBA has compiled a report on a topic of relevance to Edmonton’s Downtown business community. In this year’s report, we discuss the changes OBJECTIVE in consumer shopping habits and analyze The Future of Retail and a growing the preferences of consumers for shopping Downtown, the theme outlined here is in Downtown Edmonton. We also discuss the based on an assessment of the current factors that affect consumer shopping and retail landscape in Downtown Edmonton. how we can better prepare for the population The objective of the report is to study the infill that will be happening Downtown over the Downtown neighbourhood, consumer next 5-10 years to increase the quality of living preferences and shopping habits of the in the Downtown neighbourhood. -

Edmonton, AB Retail Q4 2017

MARKETBEAT Edmonton, AB Retail Q4 2017 ECONOMIC INDICATORS Retailers have responded with increased leasing activity and sales volumes through the final two quarters of 2017. Rents have National 12-Month also seen a general increase in the past two quarters as retailers 2016 2017F Forecast seek newer or better located space in a competitive market, GDP Growth 1.5% 2.6%* especially as several new developments located on the periphery CPI Growth 1.4% 2.0%* of Edmonton continue construction. Podium spaces in new Consumer Spending developments downtown have generally been filled, although 2.4% 3.1%* Growth some options remain for motivated tenants seeking a high Retail Sales Growth 1.7% 2.3%* visibility and high traffic location. A notable trend towards more restaurants, both quick service and sit-down options, entering the downtown area is noticeable. A significant number of fitness 12-Month Regional 2016 2017F Forecast tenants have also been moving into high profile spaces Household Income $104,750 $107,470* throughout the city. Population Growth 1.8% 1.6%* High profile mixed-use developments on Whyte Avenue are Unemployment 8.1% 6.8%* underway, as well as several newer projects downtown which are expected to have retail podiums. Densification efforts along Sources: RBC Economics, TD Economics, Finance Ministry of Alberta *2017 several high streets in Edmonton, including Whyte and Jasper Forecast Avenues and 124th Street, will make these areas more attractive for retailers. Housing starts have picked up over the past year, a good sign for community retail developers and tenants seeking Economy entry into those markets. -

Creditor List

Creditor List In the Matter of a Plan of Compromise or Arrangement of Stokes Inc. of the City of Mont-Royal in the Province of Quebec Creditor Type Name Attention Address Claim $ Unsecured 152810 CANADA INC. PLACE DE VILLE 16,497.16 690 BOUL. LAURE,LOCAL 213 SEPT-ILES QC G4R 4N8 158858 CANADA INC. C/O MISTRAL ELECTRIC 24,614.44 5660 FERRIER ST. MONT-ROYAL QC H4P 1M7 20 VIC MANAGEMENT INC C/O CUSHMAN & WAKEFIELD, 3,312.88 ASSET SERV.INC. 645 LANDSDOWNE STREET WEST PETERBOROUGH ON K9J 7Y5 20 VIC MANAGEMENT INC. IN TRUST CUSHMAN & WAKEFIELD ASSET 5,469.60 SERV.LTD. 3100 HOWARD AVENUE WINDSOR ON N8X 3Y8 20 VIC MANAGEMENT INC.. CUSHMAN & WAKEFIELD ASSET 8,214.65 SERVICES S.1200A THE TOWER,MIDTOWN 201, 1ST AVE.S. SASKATOON SK S7K 1J5 20 VIC MANAGEMENT INC.-ADMIN.O CUSHMAN & WAKEFIELD ASSET 9,824.53 SERV. LTD 203-7001 MUMFORD ROAD HALIFAX NS B3L 4R3 2467847 ONTARIO INC. O/A WINDSOR CROSSING 3,609.89 170 INDUSTRIAL PARKWAY NORTH, UNIT A1 AURORA ON L4G 4C3 [email protected] 2635-6642 QUEBEC INC 11, RUE MONT BLEU 1,816.61 PINCOURT QC J7V 8E7 3934390 CANADA INC. C/O MORGUARD INV. LTD., THE 15,931.03 MALL AT LAWSON HEIGHTS 134 PRIMROSE DRIVE SASKATOON SK S7K 5S6 4269811 CANADA INC 335 BOUL. BRUNSWICK POINTE-CLAIRE QC H9R 1A7 6095054 CANADA INC.(LES STEPHAN 5566- B BOUL. DES ROSSIGNOLS 1,782.11 ENTREPRISES MIDZONE) BOUCHARD LAVAL QC H7L 5W6 [email protected] 713949 ONTARIO LTD ST-LAURENT SHOPPING CTRE, 7,770.78 OTTAWA MGMT OFF.