Reliance Jio's 5G Push to Be India's Answer to Huawei

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Press Release Reliance Industries Limited

Press Release Reliance Industries LImited March 30, 2020 Ratings Amount Facilities Rating1 Rating Action (Rs. crore) CARE AAA; Non-Convertible Debentures 10,386 Stable(Triple A; Assigned Outlook: Stable) Details of instruments/facilities in Annexure-1 Other Ratings Instruments Amount (Rs.Crore) Ratings Non-Convertible Debenture 40,000 CARE AAA; Stable Commercial Paper 34,500 CARE A1+ Detailed Rationale& Key Rating Drivers On March 18, 2020, the company announced that the Hon’ble National Company Law Tribunal (NCLT), Ahmedabad Bench has approved the Scheme, for transfer of certain identified liabilities from Reliance Jio Infocomm Limited (RJIL; rated CARE AAA; Stable/ CARE A1+, CARE AAA (CE); Stable) to Reliance Industries Limited (RIL). Pursuant to the Scheme of Arrangement amongst RJIL and certain classes of its creditors (the “Scheme”) as sanctioned by the Hon’ble National Company Law Tribunal, Ahmedabad Bench, vide its order dated March 13, 2020, RIL has assumed the NCDs issued by RJIL. The rating continues to factor in the immensely experienced and resourceful promoter group, highly integrated nature of operations with presence across the entire energy value chain, diversified revenue streams, massive scale of downstream business with one of the most complex refineries, established leadership position in the petrochemical segment as well as strong financial risk profile characterized by robust capital structure, stable cash flows and healthy liquidity position. The rating also factors in the increasing wireless subscriber base which has led its digital services business to attain a leadership position in the industry as well as the various steps announced by the management to reduce the debt on a consolidated level. -

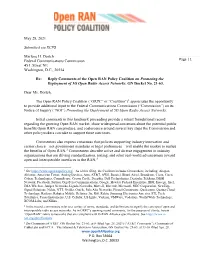

Strong Sequential Rebound Across All Businesses

Strong Sequential Rebound Across All Businesses CONSOLIDATED RESULTS FOR QUARTER ENDED 30TH SEPTEMBER, 2020 STRONG SEQUENTIAL REBOUND ACROSS ALL BUSINESSES CONSOLIDATED QUARTERLY REVENUE WAS HIGHER BY 27.2% AT ` 128,385 CRORE CONSOLIDATED QUARTERLY EBITDA GREW BY 7.9% TO ` 23,299 CRORE CONSOLIDATED QUARTERLY PAT BEFORE EXCEPTIONAL ITEM AT ` 10,602 CRORE HIGHER BY 28% CONSUMER BUSINESSES CONTRIBUTED 49.6% OF CONSOLIDATED SEGMENT EBITDA RECORD QUARTERLY EBITDA FOR DIGITAL SERVICES AT ` 8,345 CRORE ROBUST RECOVERY IN RETAIL EBITDA TO ` 2,006 CRORE HIGHER BY 85.9% CAPITAL RAISE OF ` 152,056 CRORE IN JIO PLATFORMS LIMITED CAPITAL RAISE OF ` 37,710 CRORE IN RELIANCE RETAIL VENTURES LIMITED FIRST TELECOM OPERATOR OUTSIDE CHINA TO CROSS 400 MN SUBSCRIBERS IN A SINGLE COUNTRY MARKET ADDED IN EXCESS OF 30,000 TO ITS WORKFORCE Registered Office: Corporate Communications Telephone : (+91 22) 2278 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 2278 5185 3rd Floor, 222, Nariman Point 9th Floor, Nariman Point Internet : www.ril.com; [email protected] Mumbai 400 021, India Mumbai 400 021, India CIN : L17110MH1973PLC019786 Page 1 of 19 STRATEGIC UPDATES • Jio Platforms Limited, a wholly owned subsidiary of Reliance Industries Limited, raised ₹ 152,056 crore from leading global investors including Facebook, Google, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, TPG, L Catterton, PIF, Intel Capital and Qualcomm Ventures. • Reliance Retail Ventures Limited (RRVL), a wholly owned subsidiary of Reliance Industries Limited, raised ` 37,710 crore of investments from leading global investors including Silver Lake, KKR, General Atlantic, Mubadala, GIC, TPG and ADIA. -

Media-Release-JIO-Q1-FY-2018-19

Media Release Mumbai, 27 th July 2018 CROSSED 200 MILLION SUBSCRIBERS WITHIN 21 MONTHS FROM COMMENCEMENT OF SERVICES INDUSTRY LEADING GROWTH IN SUBSCRIBER BASE TO 215.3 MILLION HEALTHY CUSTOMER TRACTION ON POST-PAID OFFERINGS DATA CONSUMPTION AT RECORD 642 CRORE GB IN THE QUARTER; 10.6GB PER USER PER MONTH; GROWING RAPIDLY STRONG FINANCIAL PERFORMANCE DESPITE COMPETITIVE INTENSITY EBITDA GROWTH OF 16.8% QOQ TO ₹3,147 CRORE IN Q1 FY 2018-19 HIGHLIGHTS OF QUARTER ’S (Q1 – FY 2018-19) PERFORMANCE Standalone Financials 1Q’ 18-19 4Q’ 17-18 QoQ Growth (₹ crore) Value of Services 9,567 8,404 13.8% Operating revenue 8,109 7,128 13.8% EBITDA 3,147 2,694 16.8% EBITDA margin 38.8% 37.8% 101bps EBIT 1,708 1,495 14.3% Net Profit 612 510 19.9% Standalone revenue from operations of ₹8,109 crore (13.8% QoQ growth) Standalone EBITDA of ₹3,147 crore (16.8% QoQ growth) and EBITDA margin of 38.8% Standalone Net Profit of ₹612 crore Subscriber base as on 30th June-18 of 215.3 million Lowest churn in the industry at 0.30% per month ARPU during the quarter of ₹134.5/ subscriber per month Total wireless data traffic during the quarter of 642 crore GB Total voice traffic during the quarter of 44,871 crore minutes Registered Office: Corporate Communications Telephone : (+91 22) 6255 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 6255 5185 9th Floor, 222, Nariman Point 9th Floor, 222, Nariman Point CIN : U72900MH2007PLC234712 Mumbai 400 021, India Mumbai 400 021, India Website : www.jio.com and www.ril.com Page 1 of 7 Media Release Commenting on the results, Shri Mukesh D. -

Reliance Industries

14 April 2020 Company Update Reliance Industries Investment in consumer business paying BUY off, upgrade to Buy CMP (as on 13 Apr 20) Rs 1,191 Target Price Rs 1,400 RIL stock has corrected by 25% from its peak over the past 4 months driven by global economic slowdown concerns. Our view that the stock price correction NIFTY 8,994 is overdone, and the stock should outperform, is premised on 1) Non-cyclical domestic consumer business accounting for 56% of FY21E EBITDA (31% in KEY CHANGES OLD NEW FY19), 2) The stock factoring only an USD 3.0/bbl FY21E refining margin, 49% Rating ADD BUY lower than Global Financial Crises (GFC) quarterly trough and 3) Interest Price Target Rs 1,566 Rs 1,400 Coverage ratio of 4.3x and Net Debt/EBITDA of 1.6x in FY22E (12-35% better FY21E FY22E than the FY19 lows). The stock offers 18% upside at our TP of INR 1,400. EPS % -27% -10% No financial stress even under economic slowdown conditions KEY STOCK DATA We estimate that even with refining margins of USD 5.9/bbl (lowest quarterly Bloomberg code RIL IN margin during the Global Financial Crises and 36% lower than 3QFY20) and Petchem margins at a discount of 29% to 3QFY20 (lowest quarterly margin in No. of Shares (mn) 6,339 last 13 years), RIL’s FY21E EBITDA would be INR 775bn, more than adequate to MCap (Rs bn) / ($ mn) 7,737/101,358 service its INR 2.9trn of debt. 6m avg traded value (Rs mn) 17,400 52 Week high / low Rs 1,618/876 Jio: Next catalysts-Mobile revenue growth, fibre broadband ramp-up With about USD 50bn (50% of market cap) invested in telecom, Jio’s revenue STOCK PERFORMANCE (%) market share growth and monetisation continues to drive a significant 3M 6M 12M proportion of the value creation opportunity for RIL’s shareholders. -

The US-India Strategic Relations: a Brief Report by Dr

The US-India Strategic Relations: A Brief Report By Dr. Sohail Mahmood Tensions between India and China increased after skirmishes in the contested Pangong Lake region of eastern Ladakh in the Kashmir region bordering the two countries in the Himalayas. On June 15 there occurred a border clash between the two countries in the contested Galwan valley in the Ladakh region in which 20 Indian soldiers were killed, and several Chinese casualties but it is yet to give out details. According to a US intelligence report, the number of casualties on the Chinese side was 35.i The fighting was the first-time soldiers were killed over the border dispute since 1967. China and India went to war over their disputed border issues in a 1962 conflict that spilled into Ladakh and ended with an uneasy truce. Since then, troops from opposing sides have guarded the undefined, mountainous 2,200-mile border area, occasionally clashing. Today, Indian and Chinese officials are holding talks to try to resolve a months-long standoff along their disputed frontier, where the two countries have deployed tens of thousands of soldiers. There was a wave of nationalism sweeping India, the likes of which has not been seen before. After the Galwan Valley border clash between the two countries, there was a popular call for a boycott of Chinese products. Although there is a stalemate on the border, tensions between the two countries continue to escalate, resultantly. The Indian- controlled territory runs along the Line of Actual Control (LAC), a loose demarcation line created after the 1962 China-Indian War and now the de facto border between the two countries. -

May 28, 2021 Submitted Via ECFS

May 28, 2021 Submitted via ECFS Marlene H. Dortch Federal Communications Commission Page | 1 45 L Street NE Washington, D.C., 20554 Re: Reply Comments of the Open RAN Policy Coalition on Promoting the Deployment of 5G Open Radio Access Networks, GN Docket No. 21-63. Dear Ms. Dortch, The Open RAN Policy Coalition (“ORPC” or “Coalition”)1 appreciates the opportunity to provide additional input to the Federal Communications Commission (“Commission”) on its Notice of Inquiry (“NOI”) Promoting the Deployment of 5G Open Radio Access Networks. Initial comments in this landmark proceeding provide a robust foundational record regarding the growing Open RAN market, show widespread consensus about the potential public benefits Open RAN can produce, and coalescence around several key steps the Commission and other policymakers can take to support these outcomes. Commenters also express consensus that policies supporting industry innovation and carrier choice – not government mandates or legal preferences – will enable the market to realize the benefits of Open RAN.2 Commenters describe active and diverse engagement in industry organizations that are driving standardization, testing, and other real-world advancement toward open and interoperable interfaces in the RAN.3 1 See https://www.openranpolicy.org/. As of this filing, the Coalition includes 60 members, including: Airspan, Altiostar, American Tower, Analog Devices, Arm, AT&T, AWS, Benetel, Bharti Airtel, Broadcom, Ciena, Cisco, Cohere Technologies, CommScope, Crown Castle, DeepSig, Dell Technologies, Deutsche Telekom, DISH Network, Facebook, Fujitsu, GigaTera Communications, Google, Hewlett Packard Enterprise, IBM, Inseego, Intel, JMA Wireless, Juniper Networks, Ligado Networks, Marvell, Mavenir, Microsoft, NEC Corporation, NewEdge Signal Solutions, Nokia, NTT, Nvidia, Oracle, Palo Alto Networks, Pivotal Commware, Qualcomm, Quanta Cloud Technology, Radisys, Rakuten Mobile, Reliance Jio, Rift, Robin, Samsung Electronics America, STL Tech, Telefónica, Texas Instruments, U.S. -

Reliance Industries Companyname

COMPANY UPDATE RELIANCE INDUSTRIES Déjà vu: Downgrade in order India Equity Research| Oil, Gas and Services COMPANYNAME We turned very bullish on Reliance Industries (RIL) with our BRAVEHEART EDELWEISS 4D RATINGS ‘BUY’ in 2016; four years on and a 4x rally since, we believe the stock’s Absolute Rating HOLD primary triggers—deleveraging, asset monetisation and digital Rating Relative to Sector Outperform momentum—have played out. We also believe the pendulum has swung Risk Rating Relative to Sector Medium entirely: from extreme pessimism to exuberance, infallible expectations Sector Relative to Market Equalweight on execution and a peak analyst ‘Buy’ ratio (80%). That the valuation is pricing in overly high growth expectations when its WACC is rising and economic spread being negative suggest risks lie on the downside. This is MARKET DATA (R: RELI.BO, B: RIL IN) CMP : INR 2,146 not RIL’s first brush with euphoria: 1994 (India liberalisation), 2000 (Y2K) Target Price : INR 2,105 and 2008 (KG-D6/Refining). The current exuberance gives us a sense of déjà vu; downgrade to ‘HOLD’ with a target price of INR2,105. 52-week range (INR) : 2,163 / 867 Share in issue (mn) : 6,339.4 M cap (INR bn/USD mn) : 14,148 / 70,157 Ten-year Jio 35% CAGR, eh; high WACC; negative economic spread Avg. Daily Vol.BSE/NSE(‘000) : 11,335.2 Our two-stage reverse-DCF analysis shows the market is baking in high EPS growth, particularly for Jio Platforms (35% CAGR sustaining for ten years). We believe the SHARE HOLDING PATTERN (%) associated risk is high, and despite its strong past execution, even RIL is not infallible. -

USCIS - H-1B Approved Petitioners Fis…

5/4/2010 USCIS - H-1B Approved Petitioners Fis… H-1B Approved Petitioners Fiscal Year 2009 The file below is a list of petitioners who received an approval in fiscal year 2009 (October 1, 2008 through September 30, 2009) of Form I-129, Petition for a Nonimmigrant Worker, requesting initial H- 1B status for the beneficiary, regardless of when the petition was filed with USCIS. Please note that approximately 3,000 initial H- 1B petitions are not accounted for on this list due to missing petitioner tax ID numbers. Related Files H-1B Approved Petitioners FY 2009 (1KB CSV) Last updated:01/22/2010 AILA InfoNet Doc. No. 10042060. (Posted 04/20/10) uscis.gov/…/menuitem.5af9bb95919f3… 1/1 5/4/2010 http://www.uscis.gov/USCIS/Resource… NUMBER OF H-1B PETITIONS APPROVED BY USCIS IN FY 2009 FOR INITIAL BENEFICIARIES, EMPLOYER,INITIAL BENEFICIARIES WIPRO LIMITED,"1,964" MICROSOFT CORP,"1,318" INTEL CORP,723 IBM INDIA PRIVATE LIMITED,695 PATNI AMERICAS INC,609 LARSEN & TOUBRO INFOTECH LIMITED,602 ERNST & YOUNG LLP,481 INFOSYS TECHNOLOGIES LIMITED,440 UST GLOBAL INC,344 DELOITTE CONSULTING LLP,328 QUALCOMM INCORPORATED,320 CISCO SYSTEMS INC,308 ACCENTURE TECHNOLOGY SOLUTIONS,287 KPMG LLP,287 ORACLE USA INC,272 POLARIS SOFTWARE LAB INDIA LTD,254 RITE AID CORPORATION,240 GOLDMAN SACHS & CO,236 DELOITTE & TOUCHE LLP,235 COGNIZANT TECH SOLUTIONS US CORP,233 MPHASIS CORPORATION,229 SATYAM COMPUTER SERVICES LIMITED,219 BLOOMBERG,217 MOTOROLA INC,213 GOOGLE INC,211 BALTIMORE CITY PUBLIC SCH SYSTEM,187 UNIVERSITY OF MARYLAND,185 UNIV OF MICHIGAN,183 YAHOO INC,183 -

Reliance Industries Limited: Ratings Reaffirmed

February 26, 2021 Reliance Industries Limited: Ratings reaffirmed Summary of rating action Previous Rated Amount Current Rated Amount Instrument* Rating Action (Rs. crore) (Rs. crore) Non-convertible Debentures 57,000.00 57,000.00 [ICRA]AAA (Stable); reaffirmed Commercial Paper program 10,000.00 10,000.00 [ICRA]A1+; reaffirmed Total 67,000.00 67,000.00 *Instrument details are provided in Annexure-1 Rationale The ratings factor in the robust financial profile of the company reflected by healthy profitability, strong debt protection metrics, low working capital intensity and moderate leverage levels. The ratings also factor in the company’s exceptional financial flexibility derived from its healthy liquid investment portfolio and superior fund-raising ability from the domestic and global banking as well as the capital markets. In YTD FY2021, RIL has raised significant funds through stake sales of its digital services (Jio Platforms Limited, JPL) and retail business (Reliance Retail Ventures Limited, RRVL) along with a Rs. 53, 125 crore rights issue which was fully subscribed. By December 2020, RIL has raised Rs. 220,231 crore through its fund-raising programs and will also receive Rs. 39, 843.0 crore in FY2022 as balance pay-in from the rights issue. As a result, RIL’s credit profile has strengthened significantly over the course of the year. ICRA also takes note of the announced reorganization of RIL’s Oil to Chemicals business also known as O2C segment into a Wholly Owned Subsidiary (WOS) of RIL with assets of the refining & marketing and the petrochemical businesses being transferred to the WOS. -

Subsidiary Company Having 31St December As Reporting Date

Name of the Enterprise Proportion of Ownership Interest ABC Cable Network Private Limited 44.00% Adhunik Cable Network Limited (Formerly known as Adhunik Cable Network Private 78.58% Limited) Adventure Marketing Private Limited 100.00% AETN18 Media Private Limited 21.27% Affinity Names Inc. * 100.00% Affinity USA Inc. * 100.00% Ambika DEN Cable Network Private Limited 78.58% Amogh Broad Band Services Private Limited 78.58% Angel Cable Network Private Limited 44.00% Antique Communications Private Limited 78.58% Asteria Aerospace Private Limited 74.57% Augment Cable Network Private Limited 78.58% Aurora Algae Inc. * 100.00% Bali Den Cable Network Limited (Formerly known as Bali Den Cable Network Private 40.11% Limited) Bee Network and Communication Private Limited 71.96% Bhadohi DEN Entertainment Private Limited 20.44% Big Den Entertainment Private Limited 78.58% Binary Technology Transfers Private Limited 71.96% Blossom Entertainment Private Limited 78.58% Cab-i-Net Communications Private Limited 40.09% Channels India Network Private Limited 67.56% Chennai Cable Vision Network Private Limited 54.68% Colorful Media Private Limited 100.00% Colosceum Media Private Limited 73.15% Crystal Vision Media Private Limited 40.07% C-Square Info Solutions Private Limited 89.45% Den A.F. Communication Private Limited 78.58% Den Aman Entertainment Private Limited 78.58% DEN Ambey Cable Networks Private Limited 47.93% Den Ashu Cable Limited (Formerly known as Den Ashu Cable Private Limited) 40.07% DEN BCN Suncity Network Limited (Formerly known as DEN -

Reliance Jio Infocomm Limited: Update on Material Event

November 05, 2019 Reliance Jio Infocomm Limited: Update on material event Summary of rated instruments Previous Rated Current Rated Instrument Amount Amount Rating Action (Rs. crore) (Rs. crore) Non-Convertible Debenture Programme 35,500 35,500 [ICRA]AAA (Stable); outstanding Material Event Reliance Industries Limited (RIL), the parent holding company of Reliance Jio Infocomm Limited (RJIL), on October 25, 2019 announced a business reorganisation which involved formation of a new Wholly Owned Subsidiary (WOS) to hold all digital business assets including RJIL. Impact of material event As per the proposed business reorganisation, the newly created subsidiary WOS would hold all the digital businesses of the group, including RJIL’s telecom assets among other assets such as the application bouquet of Jio and investments in digital assets like Haptik, Radisys, etc and other assets like Hathway, Den, etc. The WOS will acquire the existing equity as well as the optionally convertible preference shares (OCPS) totalling to Rs. 65,000 crore from RIL. In addition, the WOS will also subscribe to OCPS of RJIL worth Rs. 108,000 crore and in return, RJIL will transfer its long-term debt and other liabilities amounting to Rs. 108,000 crore to RIL. RJIL has already transferred its fibre and tower assets to separate infrastructure investment trusts (InvIT). The debt on the books of RJIL as on September 30, 2019 is estimated at around Rs. 116,700 crore, including spectrum debt of around Rs. 26,400 crore (spectrum debt includes interest accrued component). Post the completion of this transaction, the debt is expected to come down significantly, which along with additional equity infusion in the form of OCPS from WOS is expected to result in material improvement in credit metrics of the company. -

C. P1-56.Indd

PARTICIPANT DIRECTORY Data from a total of 312 Northwest companies are included in this survey. The following list includes 140 publicly traded & 172 privately held/other companies. BANKING / FINANCIAL - PRIVATELY HELD Pacifi c NW Federal Credit Union Heritage Bank Rentrak Corporation* Advantis Credit Union Peoples Bank HomeStreet Bank Starbucks Corporation* Alaska USA Federal Credit Union Pioneer Trust Bank, N.A. MBank URM Stores, Inc. ALPS Federal Credit Union Point West Credit Union Northrim Bank Willamette Valley Vineyards, Inc.* Bank of Eastern Oregon Riverbank Oregon Pacifi c Bank zulily, inc.* bankcda SaviBank Pacifi c Continental Bank Zumiez, Inc.* Cascade Federal Credit Union Security State Bank People's Bank of Commerce ELECTRONICS / TECHNOLOGY Cashmere Valley Bank SELCO Community Credit Union Plaza Bank Coastal Community Bank Skagit Bank Premier Community Bank Array Health Commencement Bank Solarity Credit Union Puget Sound Bank Base2 Solutions Community Bank Sound Credit Union Riverview Bancorp, Inc. BlackPoint IT Services Community First Bank - Kennewick Spirit of Alaska Federal Credit Union Sound Financial Bancorp, Inc.* Blucora Inc.* Craft3 St. Helens Community Credit Union Summit Bank - Oregon BSQUARE Corporation* Credit Union 1 State Bank Northwest Timberland Bank Cascade Microtech, Inc. * D.L. Evans Bank The Bank of Oswego Umpqua Holdings Corporation Chef Software, Inc. Denali Alaskan Federal Credit Union True North Federal Credit Union Washington Federal Clearsign Combustion Corp* Evergreen Federal Bank Unitus Community