Ncsoft (036570 KS ) a Compelling Buy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ncsoft (036570 KS ) Rally to Be Stronger in 2019 Than in 2017

NCsoft (036570 KS ) Rally to be stronger in 2019 than in 2017 Games 4Q18 preview: Lineage M to continue QoQ growth Earnings Preview For 4Q18, we forecast NCsoft to deliver revenue of W407bn (-23.7% YoY, +0.7% QoQ) January 17, 2019 and operating profit of W131bn (-30.9% YoY, -6.0% QoQ). For Lineage M , which exhibited its highest user indicators of 2018 following its update on September 28 th , we estimate 4Q18 revenue grew 0.6% QoQ to W218bn. Despite the slight revenue gain QoQ, we believe operating profit contracted QoQ, due (Maintain) Buy to: 1) a one-off payment for the signing of new players for the NC Dinos baseball team; and 2) advertising spending on Lineage Remastered . Target Price (12M, W) 700,000 Why 2019 is likely to be even stronger than 2017 Share Price (01/16/19, W) 465,500 In 2017, NCsoft’s stock gained 85.3% (vs. +22.0% for the KOSPI), boosted by expectations on Lineage M (released on June 21 st ). In 2019, we believe the stock will Expected Return 50% experience an even bigger rally. As we outline in <Table 3>, Lineage M was the only new title the company launched in 2017, and revenue was predominately concentrated in the domestic market. OP (18F, Wbn) 633 In 2019, NCsoft has two to five new mobile titles set for release, including Lineage II M Consensus OP (18F, Wbn) 634 (1H19). We also expect overseas expansion to gather steam in 2019. We note that EPS Growth (18F, %) 3.1 Lineage II , Aion , and Blade & Soul have seen overseas revenues either comparable to Market EPS Growth (18F, %) 6.2 or much higher than their domestic revenues. -

Units Result Record Roi Total Units

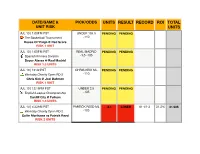

DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI TOTAL UNIT RISK UNITS JUL 10 | 1:00PM PST UNDER 155.5 PENDING PENDING � The Basketball Tournament -110 House Of ‘Paign @ Red Scare RISK 1 UNIT JUL 10 | 1:00PM PST REAL MADRID PENDING PENDING ⚽ Spanish Primera División -1.5 -135 Depor Alaves @ Real Madrid RISK 1.5 UNITS JUL 10 | 12:42 PST CHRIS KIRK ML PENDING PENDING ⛳ Workday Charity Open RD 2 -110 Chris Kirk @ Joel Dahmen RISK 1 UNIT JUL 10 | 12:15PM PST UNDER 2.5 PENDING PENDING ⚽ English League Championship -135 Cardiff City @ Fulham RISK 1.5 UNITS JUL 10 | 4:23AM PST PARTICK REED ML -2.1 LOSER 61-41-3 31.3% 31.925 ⛳ Workday Charity Open RD 2 -105 Collin Morikawa vs Patrick Reed RISK 2 UNITS DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI TOTAL UNIT RISK UNITS JUL 10 | 2:30AM PST NC DINOS RL -1.5 2 WINNER 61-40-3 33.9% 34.025 ⚾ Korean Baseball -110 NC Dinos @ LG Twins RISK 2 UNITS JUL 10 | 2:30AM PST OVER 9.5 1 WINNER 60-40-3 32% 32.025 ⚾ Korean Baseball -115 SK Wyverns @ Hanwha Eagles RISK 1 UNIT JUL 10 | 2:00AM PST HIROSHIMA CARP -2.025 LOSER 59-40-3 31.5% 31.175 ⚾ Japan Baseball ML -135 Hiroshima Carp @ Chunichi Dragons RISK 1.5 UNITS JUL 10 | 1:00AM PST OVER 188.5 -1.1 LOSER 59-39-3 33.9% 33.2 � Chinese Basketball Association -110 Bayi Rockets @ Jiangsu Dragons RISK 1 UNIT JUL 9 | 5:00PM PST MONTREAL -1.8 LOSER 59-38-3 35.4% 34.3 ⚽ Major League Soccer IMPACT +.5 -120 NE Revolution @ Montreal Impact RISK 1.5 UNITS DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI TOTAL UNIT RISK UNITS JUL 9 | 4:55AM PST XANDER 1.5 WINNER 59-37-3 37.6% 36.1 -

Units Result Record Roi Total Units

DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI TOTAL UNIT RISK UNITS JUL 21 | 5:00PM PST COLUMBUS PENDING PENDING ⚽ Major League Soccer CREW ML +115 Columbus Crew @ Atlanta United RISK 1.5 UNITS JUL 21 | 12:15PM PST OVER 2.5 -2.7 LOSER 105-85-9 15.4% 29.3 ⚽ English Premier League -135 Arsenal @ Aston Villa RISK 2 UNITS JUL 21 | 11:00AM PST UNDER 2.5 1 WINNER 104-85-9 19.9% 32 ⚽ Portuguese Liga -105 Victoria Setubal @ Sporting Lisbion RISK 1 UNIT JUL 21 | 10:00AM PST OVER 3.5 1.3 WINNER 103-85-9 16.5% 31 ⚽ English Premier League +130 Manchester City @ Watford RISK 1 UNIT JUL 21 | 2:30AM PST NC DINOS -1 LOSER 102-85-9 15.9% 29.7 ⚾ Korean Baseball RL -1.5 +115 Samsung Lions @ NC Dinos RISK 1 UNIT (RUN LINE) OVER 10.5 3 WINNER 102-84-9 16.5% 30.7 RISK 3 UNITS (TOTAL) -120 DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI TOTAL UNIT RISK UNITS JUL 21 | 2:30AM PST KIA TIGERS RL 0.5 WINNER 101-84-9 15% 27.7 ⚾ Korean Baseball -1.5 -130 Kia Tigers @ Hanwha Eagles RISK .5 UNIT JUL 21 | 2:00AM PST SEIBU LIONS 1.4 WINNER 100-84-9 14.9% 27.2 ⚾ Japan Baseball RL -1.5 +140 Chiba Lotte Marines @ Seibu Lions RISK 1 UNIT JUL 21 | 2:00AM PST OVER 8.5 1 WINNER 99-84-9 14.1% 25.8 ⚾ Japan Baseball -115 Yakult Swallow @ Yokohama Baystars RISK 1 UNIT JUL 20 | 5:00PM PST PHILA UNION PK 0 PUSH 98-84-9 13.6% 24.8 ⚽ Major League Soccer -115 Orlando City FC @ Philadelphia Union RISK 2 UNITS JUL 20 | 12:15AM PST WOLVES -1 1.5 WINNER 98-84-8 13.6% 24.8 ⚽ English Premier League -120 Crystal Palace @ Wolverhampton RISK 1.5 UNITS DATE/GAME & PICK/ODDS UNITS RESULT RECORD ROI -

Internationalisation Strategy (“GCA’S Internationalisation Strategy”)

Ref. Ares(2019)4111434 - 28/06/2019 Global Content Alliance Grant Agreement n° 783405 Internationalisation Strategy (“GCA’s Internationalisation Strategy”) Grant Agreement Deliverable D4.1 Actual Date submission date: 07/01/2019 Due date of deliverable: M11 Start date of the Project: 01/01/2018 Duration: 18 months 06/01/2019 GCA D4.1 Internationalisation Strategy – PUBLIC DOCUMENT Page 1 of 64 Credits This document has been elaborated in the frame of the GCA - Global Content Alliance - project (Agreement N°783405) co-funded by the European Commission COSME programme (2014-2020). The contributors to this Document: Editor: Emre Koca, GCA WP4 leader at Transmedia Bayern, Germany Coached by Philippe Dubois, in-house consultant at Transmedia Bayern, Germany Contributors: Egbert Van Wyngaarden, CEO at Transmedia Bayern, Germany Pierre Collin, CEO at Cluster TWIST, Belgium Pervenche Beurier, CEO at Pôle Média Grand Paris, France Pernilla Lavesson, Community Manager at Media Evolution, Sweden Disclaimer The content of this document represents the views of the authors only and is their sole responsibilities; it cannot be considered to reflect the views of the European Commission and/or the Executive Agency for Small and Medium-sized Enterprises (EASME) or any other body of the European Union. The European Commission and the Agency do not accept any responsibility for use that may be made of the information it contains. This document is part of the project GCA which has received funding from the European Commission COSME programme (2014-2020) - grant agreement No. 783405. 06/01/2019 GCA D4.1 Internationalisation Strategy – PUBLIC DOCUMENT Page 2 of 64 Table of Contents 1 THE KEY CHALLENGES FOR INTERNATIONALISATION ............................................................................................................. -

Esg Playbook

ESG PLAYBOOK NCSOFT SUSTAINABILITY REPORT NCSOFT’s First Sustainability Report NCSOFT aspires to create a future where everyone is connected by joy. Contents Overview of NC PLAY for Sustainability 04 Governance 44 Who We Are 06 46 What We Create Care for Employees 48 08 Communication with Customers 54 10 Local Community 55 56 ESG Appendix 14 Materiality Test 60 A Healthy Corporate Culture, Unbiased Joy 16 61 28 01 Blade & Soul 2 Overview of NC CEO Message 04 Who We Are 06 What We Create Highlights ‘PUSH, PLAY’ 08 Value and Future of the Games Industry 10 Overview of NC PLAY for Sustainability ESG Appendix 4 CEO Message Overview of NC PLAY for Sustainability ESG Appendix 5 “ NCSOFT ceaselessly pusHes aHead, continuing on its Journey of growth.” Dear Stakeholders, improving shareholder value and protecting shareholder rights and interests, and creating As the CEO of NCSOFT, it is my great pleasure social value along the way. Going forward, we will advance sustainability management in the best sustainability report. possible way to our fullest capacity, and remain focused on giving back to society in a genuine way Since our inception back in 1997, all of us at while elevating our corporate value. NCSOFT have weathered a myriad of storms and have continued to rise up to new challenges to progress this far. Throughout it all, we have and encouragement in our journey ahead. transparent and responsible governance, Best regards, CEO Overview of NC PLAY for Sustainability ESG Appendix Who We Are 6 Ushering in a brand new future where all are connected by joy, Who We Are NC aspires to assist in the creation of a new frontier where truly impressive experiences await. -

Chris Flexen Changeup 23

Chris Flexen End of Season Report By: Ben Howell Email: [email protected] Twitter: @benhowell71 Website: benhowell71.com Contents Introduction 2 Stats and Graphics 3 Chris Flexen 4-Seam Fastball 8 Chris Flexen Cutter 14 Chris Flexen Curveball 18 Chris Flexen Changeup 23 Resources 26 1 Introduction Vitals Pitch Type Avg MPH Usg% Throws: RHP 4-Seam 92.6 61.8% Age: 26 Cutter 87.2 16.9% DOB: 7/01/1994 Curveball 76.1 12.5% Height: 6’ 3" Changeup 81.1 8.8% Weight: 249 lbs In his first KBO season, Chris Flexen, a former New York Mets pitcher and prospect, turned in a fantastic season with the Doosan Bears. Over 116.2 regular-season innings and 28.1 playoff innings (145 total IP), Flexen flashed his swing and miss ability and increased confidence in some of his secondary pitches, and helped pull the Bears to the Korean Series, where they fell to the dominant NC Dinos in six games. Flexen was the second-hardest throwing starting pitcher in the KBO in 2020 (behind teammate Raúl Alcántara), which has always been a strength for him. In a bullpen role with the Mets, Flexen’s fastball averaged around 94 mph; with Doosan, he averaged about 92.6 mph on his 4-seam, getting stronger as the season continued. He was able to ride that velocity to the highest K% in the KBO among starting pitchers. Flexen’s stellar season in the KBO, which included an IL stint partway through, was likely good enough to draw MLB interest in him as a potential reliever/swing-man or from a team interested in developing him as a starter. -

Inter-Varsity Stock Research Challenge 2018 Building a League of Hidden Champions

Inter-Varsity Stock Research Challenge 2018 Building a League of Hidden Champions Disclaimer 1. The booklet and its contents contain the opinions and the ideas of its authors. It is not a recommendation to purchase or sell the securities of any of the companies or investments herein discussed. The booklet is sold with the understanding that the authors and the organisers are not engaged in rendering legal, accounting, investment or other professional services. If the reader of this booklet requires expert financial or other assistance or legal advice, a competent professional should be consulted. Neither the authors nor the organisers can guarantee the accuracy of the information contained herein the booklet and its contents. 2. The organisers are not in any way related to the companies mentioned in the booklet. 3. The authors and organisers specifically disclaim any responsibility for any liability, loss or risk, professional or otherwise, which is incurred as consequence, directly or indirectly, or the use and application of any of the contents of the booklet. i Preface “Strive not to be a success, but rather to be of a value.” - Albert Einstein Impact. Impact is created when one strives to be of value to They will be passing on the plaque to the next craft insightful research reports on outstanding champion which will be unveiled in our 2nd companies to leave an indelible mark of benefit to Intervarsity Stock Research Challenge. It will be held the business and investment community. within the 7th Value Investing Summit (VIS), a two- day event which attracts a 1,500-strong community Impact is delivered by Warren Buffett, long before of like-minded value investors to participate and is he was the billionaire Chairman of Berkshire held on 27-28 January 2018 at the Singapore Expo. -

Exploratory Study on Professional Baseball Fan Experience Management: Based on In-Depth Interview and Customer Journey Map

International Journal of Advanced Smart Convergence Vol.10 No.1 176-183 (2021) http://dx.doi.org/10.7236/IJASC.2021.10.1.176 IJASC 21-1-19 Exploratory Study on Professional Baseball Fan Experience Management: Based on In-Depth Interview and Customer Journey Map Se-yun Kim1, Kyung-Won Byun2 1Assistant Professor, Department of Sport management, Dankook University, Korea 2Assistant Professor, Department of graduate school of business Administration, Dankook University, Korea E-mail: [email protected], [email protected] Abstract The purpose of this study is was to analyze customer experience attribute of professional baseball. To achieve objectives of this study, a method was used the in-depth interview and experts' consultation which understanding the attributes and structure of customer experience attribute of professional baseball. As a result, the professional baseball customer experience attributes are 'viewing plan & purchase', 'stadium movement', 'entrance stadium', 'move to seat', 'game viewing', 'amenities/services', 'events/cheering', ‘move after match'. The review of the experience section and attributes derived through in-depth interviews with professional baseball fans was verified through an expert’ consultation to secure content validity. Through this process, 8 experience section and 41 attributes were analyzed. The customer experience journey was analyzed for a more in-depth analysis of the viewing experience of professional baseball fans. The customer experience journey was presented based on the needs of fans and discomfort in each experience section activity. Keywords: Professional Baseball, Customer Experience Management, In-Depth Interview, Customer Experience Journey 1. Introduction Seattle Sounders FC is a soccer team that has more than doubled the average audience of the Major League Soccer(MLS) and in 2013 it showed a capacity of crowd mobilization with 43,124, higher than the average audience of Chelsea, a popular English premier league club. -

Agendapunt 6 a Jaarverslag 2017

Vastlegging Jaar 2017 Inhoudsopgave ALGEMEEN ....................................................................................................................................................... 4 2017: MISSCHIEN WEL HET DRUKSTE JAAR IN DE GESCHIEDENIS! ...................................................................................... 4 BESTUUR ............................................................................................................................................................... 5 WERKORGANISATIE .................................................................................................................................................. 7 BONDSBUREAU ....................................................................................................................................................... 8 SPORTTECHNISCH KADER ........................................................................................................................................... 9 CONGRES KNBSB.................................................................................................................................................... 9 BONDSRAAD ........................................................................................................................................................... 9 LEDENTAL............................................................................................................................................................. 11 INTERNATIONALE ORGANISATIES EN VERTEGENWOORDIGERS -

Sustainable Sport Scheduling Approach Considering Team Equity for the Korean Professional Baseball League

sustainability Article Sustainable Sport Scheduling Approach Considering Team Equity for the Korean Professional Baseball League Young Dae Ko 1,* ID , Seung Hwan Jung 2, Sung Hee Kim 2 and Sung Wook Lee 2 1 Department of Hotel and Tourism Management, College of Hospitality and Tourism, Sejong University, Seoul 05006, Korea 2 Data Analytics Group, Deloitte Consulting, Seoul 07326, Korea; [email protected] (S.H.J.); [email protected] (S.H.K.); [email protected] (S.W.L.) * Correspondence: [email protected]; Tel.: +82-2-6935-2490 Received: 30 October 2017; Accepted: 6 February 2018; Published: 7 February 2018 Abstract: Since the Korea Baseball League (KBL) had nine teams, an odd number, in the 2013 season, one team was unable to compete at certain times in the rotation while the other eight teams played games. Therefore, it was necessary to consider several elements to generate an annual match schedule in terms of team equity. However, the annual match schedule created by the conventional method could not fully reflect the elements regarding team equity, and there were a great many complaints from teams and fans. As a result, applying an optimization technique was decided upon to derive an efficient annual match schedule for the 2014 season. All the required conditions for scheduling are formulated as one or more equations and several parameter values concerning team equity are calculated with the related equations. Due to the complicated scheduling conditions, a sequential solution approach is applied by dividing the overall planning horizon in three parts. The derived annual match schedule was used for the 2014 season after some modifications, and the staff of the KBL was satisfied with the performance of the proposed scheduling methodology. -

Baseball Baseball 野球

Daily Report Protocol Protocole de rapport quotidien デイリーレポートプロトコル WED 28 JUL 2021 Baseball Baseball 野球 Fukushima Azuma Stadium Stade de baseball d'Azuma 福島あづま球場 BSBMBBLTEAM9 ----------------------_B58 1 Report Created WED 28 JUL 2021 16:00 Page 1/1 Baseball/Softball 野球・ソフトボール / Baseball/Softball Baseball 野球 / Baseball Team Roster チームロースター / Composition de l’équipe As of TUE 27 JUL 2021 DOM - Dominican Republic Height Bat Throw No. Name Date of Birth Pos. Club m / ft in Hand Hand 2 NUNEZ Gustavo 8 FEB 1988 1.80/5'11" IF S R Estrellas Orientales San Pedro de Macoris (DOM) 3 PEREZ Yefri 24 FEB 1991 1.80/5'11" U S R Aguilas Cibaenas Santiago de los Caballeros (DOM) 6 MEJIA Erick 9 NOV 1994 1.80/5'11" U S R Kansas City Royals AAA Papillion, Nebraska (USA) 7 VALERIO Charlie 7 NOV 1990 1.82/6'0" C S R Sioux Falls Canaries Sioux Falls, South Dakota (USA) 10 GUZMAN Jeison 8 OCT 1998 1.87/6'2" IF S R Kansas City Royals A+ Davenport, Iowa (USA) 14 CABRERA Melky 11 AUG 1984 1.77/5'10" OF S L Aguilas Cibaenas Santiago de los Caballeros (DOM) 15 MERCEDES Cristopher 8 MAR 1994 1.87/6'2" P L L Yomiuri Giants Tokyo (JPN) 16 BALDWIN Roldani 16 MAR 1996 1.80/5'11" C R R Boston Red Sox AAA Portland, Maine (USA) 18 RODRIGUEZ Julio 29 DEC 2000 1.90/6'3" OF R R Seattle Mariners A+ North Little Rock, Arkansas (USA) 19 BAUTISTA Jose 19 OCT 1980 1.82/6'0" OF R R Diablos Rojos del Mexico Ciudad de Mexico, CDMX (MEX) 23 ROSSO Ramon 9 JUN 1996 1.93/6'4" P R R Lehigh Valley Iron Pigs Lehigh Valley, Pennsylvania (USA) 28 GARCIA Junior 1 OCT 1995 1.80/5'11" P L L Arizona -

Trenčania Trénujú Zadarmo Zrejme Márne Pozerá Na Namontované Olympijské Kruhy Na Svojom Strope

Napriek odkladu alebo zrušeniu takmer všetkých športových podujatí na svete, každý deň vám naďalej prinášame zaujímavé Ostaňte športové čítanie. Vaša priazeň bude pre nás v týchto ťažkých dňoch veľmi dôležitá. Pomôžte nám prekonať toto ťažké nám verní! obdobie a ostaňte nám verní. Vaša redakcia Štvrtok 21. 5. 2020 74. ročník • číslo 116 cena 0,80 pre predplatiteľov 0,70 App Store pre iPad a iPhone / Google Play pre Android O rok ťažšiaStrana 21skupina Hokejistov nepotešili včerajšie správy o súperoch na MS v Minsku 2021 Strana 20 Strana 8 Kruhy len na strope „Aj po štyroch rokoch bez tréningu som na Slovensku najlepší,“ vyhlasuje maďarský rodák István Lévai. Zápasník by sa teoreticky mohol uchádzať o štart na olympiáde v Tokiu, no každý večer pred spaním sa Trenčania trénujú zadarmo zrejme márne pozerá na namontované olympijské kruhy na svojom strope. Dopingového hriešnika Z koronakrízy sa prebúdza aj hokej. Dukla Trenčín je prvý klub, ktorý sa začal spoločne pripravovať. Tréning po dlhšej pauze bol pre hokejistov v slovenskej reprezentácii nechcú. náročný, no prišli ochotne, hoci zadarmo. „Do spoločnej prípravy sme ich nenútili. Hráčov teraz neplatíme. S desiatimi máme ústnu dohodu,“ povedal FOTO TASR/MARTIN BAUMANN športový riaditeľ klubu Branko Radivojevič. FOTO ŠPORT/JANO KOLLER Viac na strane 22 2 FUTBAL štvrtok 21. 5. 2020 TÉMA UŽ V ŠIESTICH EURÓPSKYCH KRAJINÁCH SA ROZHODLI PRE PREDČASNÉ UKONČENIE SEZÓNY 2019/ všetky členské krajiny pred neu- Fanúšikovia Celticu oslavovali predvčerom váženým predčasným ukonče- pred bránami štadióna deviaty titul svojho ním sezóny a zdôraznila, že to klubu po sebe. FOTO TASR/AP Polovica s titulom, môže viesť ku komplikáciám s účasťou mužstiev v nasledujú- com ročníku európskych pohá- rov.