Security Analysis and Investment Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Synergies of Hedge Funds and Reinsurance

The Synergies of Hedge Funds and Reinsurance Eric Andersen May 13th, 2013 Advisor: Dwight Jaffee Department of Economics University of California, Berkeley Acknowledgements I would like to convey my sincerest gratitude to Dr. Dwight Jaffee, my advisor, whose support and assistance were crucial to this project’s development and execution. I also want to thank Angus Hildreth for providing critical feedback and insightful input on my statistical methods and analyses. Credit goes to my Deutsche Bank colleagues for introducing me to and stoking my curiosity in a truly fascinating, but infrequently studied, field. Lastly, I am thankful to the UC Berkeley Department of Economics for providing me the opportunity to engage this project. i Abstract Bermuda-based alternative asset focused reinsurance has grown in popularity over the last decade as a joint venture for hedge funds and insurers to pursue superior returns coupled with insignificant increases in systematic risk. Seeking to provide permanent capital to hedge funds and superlative investment returns to insurers, alternative asset focused reinsurers claim to outpace traditional reinsurers by providing exceptional yields with little to no correlation risk. Data examining stock price and asset returns of 33 reinsurers from 2000 through 2012 lends little credence to support such claims. Rather, analyses show that, despite a positive relationship between firms’ gross returns and alternative asset management domiciled in Bermuda, exposure to alternative investments not only fails to mitigate market risk, but also may actually eliminate any exceptional returns asset managers would have otherwise produced by maintaining a traditional investment strategy. ii Table of Contents Acknowledgements .......................................................................................................................... i Abstract .......................................................................................................................................... -

29:390:470:01 & 02 COURSE TITLE: Security Analysis

Department of Finance and Economics COURSE NUMBER: 29:390:470:01 & 02 COURSE TITLE: Security Analysis COURSE MATERIALS Lecture notes and assignments will be distributed via Blackboard. Required Textbooks: 1) “Value Investing – from Graham to Buffett and Beyond”, Bruce Greenwald, Judd Kahn, Paul Sonkin and Michael Biema. Wiley Finance. ISBN 0-471-46339-6 2) “The Warren Buffett Way”, 3rd Edition, Robert Hagstrom, Wiley Other readings (buy used copies): 3) “The Intelligent Investor”, Benjamin Graham. Revised Edition 2006 by Harper Collins Publishers. ISBN-10 0-06-055566-1 4) “Security Analysis”, 1951 Edition”, Benjamin Graham & David L. Dodd by McGraw Hill. ISBN 0-07-144820-9 5) “The Essays of Warren Buffett: Lessons for Corporate America”, First Revised Edition, by Lawrence A. Cunningham, ISBN-10: 0-9664461-1-9 6) “Investment Banking: Valuation, Leveraged Buyouts, and Mergers and Acquisitions”, Joshua Rosenbaum, Joshua Pearl and Joseph R. Perella (Wiley Finance) 2009. ISBN 978-0-470-44220-3 FINAL GRADE ASSIGMENT Grades Mid-Term: 40% Equity Challenge competition: 60% (team work) Teams: Each student must be part of a team of 4 members. Please take advantage of student diversity in your class. Your team is expected to work on class assignments and the equity challenge competition. 1 Department of Finance and Economics (29:390:470) COURSE SCHEDULE Course Outline Week 1: Principles of Security Analysis Lectures 1A & 1B Buying a business Lecture 1C Read Accounting Clinic 1 Appendix 1 Week 2: Balance Sheet, Income Statement Lectures 2A & 2B Appendix -

PARALYZED ECONOMY? Restructure Your Investments Amid Gloomy Economy with Reduced Interest Rates

Outlook Money - Conclave pg 54 Interview: Prashant Kumar, Yes Bank pg 44 APRIL 2020, ` 50 OUTLOOKMONEY.COM C VID-19 PARALYZED ECONOMY? Restructure your investments amid gloomy economy with reduced interest rates 8 904150 800027 0 4 Contents April 2020 ■ Volume 19 ■ issue 4 pg 10 pg 10 pgpg 54 43 Cultivating OutlookOLM Conclave Money ConclaveReports and insights from the third Stalwartsedition of share the Outlook insights Moneyon India’s valour goalConclave to achieve a $5-trillion economy Investors can look out for stock Pick a definite recovery point 36 Management34 stock strategies Pick of Jubilant in the market scenario, FoodWorksHighlighting and the Crompton management Greaves strategies of considering India’s already ConsumerJUBL and ElectricalsCGCE slow economic growth 4038 Morningstar Morningstar InIn focus: focus: HDFC HDFC short short term term debt, debt, HDFC HDFC smallsmall cap cap fund fund and and Axis Axis long long term term equity equity Gold Markets 4658 Yes Yes Bank Bank c irisisnterview Real EstateInsuracne AT1Unfair bonds treatment write-off meted leaves out investors to the AT1 in a Mutual FundsCommodities shock,bondholders exposes in gaps the inresolution our rating scheme system 5266 My My Plan Plan COVID-19: DedicatedHow dedicated SIPs can SIPs help can bring bring financial financial Volatile Markets disciplinediscipline in in your your life lives Investors need to diversify and 6 Talk Back Regulars : 6 Talk Back restructure portfolios to stay invested Regulars : and sail through these choppy waters AjayColumnsAjayColumns Bagga, Bagga, SS Naren,Naren, :: Farzana Farzana SuriSuri CoverCover Design: Vinay VINAY D DOMINICOMinic HeadHead Office Office AB-10, AB-10, S.J. -

Sebi Registered Depository Participants of Cdsl As on 29-02-2012

SEBI REGISTERED DEPOSITORY PARTICIPANTS OF CDSL AS ON 29-02-2012 SR. NO. NAME OF THE DP REGN. NO. ADD1 ADD2 ADD3 CITY STATE PIN CODE TELEPHONE1 TELEPHONE2 FAX EMAIL 1 A C AGARWAL SHARE BROKERS PVT. LTD. IN-DP-CDSL-619-2011 406, 4TH FLOOR, PAYAL COMPLEX, SAYAJIGUNJ, BARODA GUJARAT 390005 0265-2361672 0265-2362786 [email protected] ITTS HOUSE, 2ND 2 A C CHOKSI SHARE BROKERS PVT LTD IN-DP-CDSL-89-2000 FLOOR, 33 KALAGHODA FORT MUMBAI MAHARASHTRA 400001 022-30219071 022-30219099 [email protected] SAIBABA MARG 30-39,FREE FREE PRESS 215, NARIMAN 3 A K STOCKMART PRIVATE LIMITED IN-DP-CDSL-458-2008 PRESS MUMBAI MAHARASHTRA 400021 022-67546500 022-67544666 [email protected]; [email protected]; JOURNAL MARG POINT HOUSE,3RD FLR SHREYAS NEAR GORAI GORAI LINK 4 A.S. STOCK BROKING & MANAGEMENT PVT. LTD. IN-DP-CDSL-338-2006 BUNGLOW BRIDGE BUS ROAD, BORIVALI MUMBAI MAHARASHTRA 400092 022-28676040 022-28676041/42 022-28676044 [email protected] NO.70/74 STOP, (W), DR. 5 ASL CAPITAL HOLDINGS PVT. LTD. IN-DP-CDSL-290-2005 138, RADHAKRISHANA MYLAPOR, CHENNAI TAMIL NADU 600004 044-28444555 044-43434030 [email protected] N SALAI, COMMERCIAL 302, 3RD COMPLEX,VIKAS 6 AARYA EQUITY (INDIA) PVT. LTD. IN-DP-CDSL-642-2011 MULUND(WEST), MUMBAI 400 080 022-25905055 022-25905058 [email protected] FLOOR,VIKAS PARADISE,BHAKT I MARG, 7 AMRAPALI AADYA TRADING & INVESTMENT PVT. LTD. IN-DP-CDSL-487-2008 13, VAISHALI PITAMPURA NEW DELHI NEW DELHI 110088 011-47060600 011-27318693 011-27311022 [email protected]; [email protected]; [email protected] LILAVATI SHOPNO.11, HOSPITAL, [email protected]; 8 ABANS SECURITIES LTD. -

The Association of Exchange Rates and Stock Returns. (Linear Regression Analysis)

March 2007 U.S.B.E- Umeå School of Business Masters Program: Accounting and Finance Masters Thesis- Spring Semester 2007 Author : Akumbu Martin Nshom Supervisor : Stefan Sundgren Thesis seminar : 7 th May 2007 The Association of Exchange rates and Stock returns. (Linear regression Analysis) Acknowledgement I will start by thanking God Almighty for giving me the intellect to complete this project. A big thanks goes to my supervisor Stefan Sundgren for giving me guidance and all the help I needed to complete this thesis To my family for their continuous help and support to see that I under take my studies here especially my Mother Lydia Botame. Finally to all my friends and well wishers who supported me in one way or an other through out my stay here in Umeå, may God bless you all! ABSTRACT The association of exchange rates with stock returns and performance in major trading markets is widely accepted. The world’s economy has seen unprecedented growth of interdependent; as such the magnitude of the effect of exchange rates on returns will be even stronger. Since the author perceives the importance of exchange rates on stock returns, the author found it interesting to study the effect of exchange rates on some stocks traded on the Stock exchange. There has been a renewed interest to investigate the relationship between returns and exchange rates as such; the author has chosen to investigate the present study to focus in the United Kingdom with data from the London Stock exchange .The author carried out his research on 18 companies traded on the London Stock Exchange in the process, using linear regression analysis. -

Unit 1: Investments

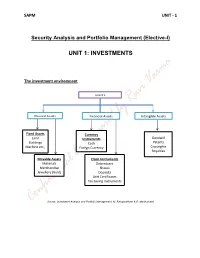

SAPM UNIT - 1 Security Analysis and Portfolio Management (Elective-I) UNIT 1: INVESTMENTS The investment environment ASSETS Physical Assets Financial Assets Intangible Assets Fixed Assets Currency Goodwill Land Instruments Patents Buildings Cash Machine etc., Copyrights Foregn Currency Royalties Movable Assets Claim Instruments Materials Debentures Merchandise Shares Jewellery (Gold) Deposits Unit Certificates Tax Saving Instruments Source: Investment Analysis and Portfolio Management, M. Ranganatham & R. Madhumathi SAPM UNIT - 1 Classification of Financial Markets: Financial Markets Securities Market Currency Market/ Forex market National Market International Market Domestic Segment Foreign Segment Capital Market Money Market Equity Market Debt Market Primary Market Secondary Market Spot Market Derivative Market Source: Investment Analysis and Portfolio Management, M. Ranganatham & R. Madhumathi SAPM UNIT - 1 SAPM UNIT - 1 Investment Meaning & Definition: investment is an activity that is engaged in by people who have savings i.e. investments are made from savings. Investment may be defined as a “commitment of funds made in the expectations of some positive rate of return.” Characteristics of Investment: Return Risk Safety Liquidity Objectives of Investment: Maximisation of Return Minimization of Risk Hedge against Inflation Investment Vs Speculation: Traditionally investment is distinguished from speculation with respect to four factors. These are: Risk Capital Gain Time Period Leverage Financial instruments (Investment Avenues available in India): Corporate Securities Deposits in banks and non-banking companies UTI and other mutual fund schemes SAPM UNIT - 1 Post office deposits and certificates Life insurance policies Provident fund schemes Government and semi government securities Regulatory Environment: In India the ministry of finance, the reserve bank of india, the securities and exchange board of India etc. -

Ba7021 Security Analysis and Portfolio Management 1 Sce

BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT A Course Material on SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT By Mrs.V.THANGAMANI ASSISTANT PROFESSOR DEPARTMENT OF MANAGEMENT SCIENCES SASURIE COLLEGE OF ENGINEERING VIJAYAMANGALAM 638 056 1 SCE DEPARTMENT OF MANAGEMENT SCIENCES BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT QUALITY CERTIFICATE This is to certify that the e-course material Subject Code : BA7021 Subject : Security Analysis and Portfolio Management Class : II Year MBA Being prepared by me and it meets the knowledge requirement of the university curriculum. Signature of the Author Name : V.THANGAMANI Designation: Assistant Professor This is to certify that the course material being prepared by Mrs.V.THANGAMANI is of adequate quality. He has referred more than five books amount them minimum one is from abroad author. Signature of HD Name: S.Arun Kumar SEAL 2 SCE DEPARTMENT OF MANAGEMENT SCIENCES BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT CONTENTS CHAPTER TOPICS PAGE NO INVESTMENT SETTING 1.1 Financial meaning of investment 1.2 Economic meaning of Investment 7-25 1 1.3 Characteristics and objectives of Investment 1.4 Types of Investment 1.5 Investment alternatives 1.6 Choice and Evaluation 1.7 Risk and return concepts. SECURITIES MARKETS 2.1 Financial Market 2.2 Types of financial markets 2.3 Participants in financial Market 2.4 Regulatory Environment 2 2.5 Methods of floating new issues, 26-64 2.6 Book building 2.7 Role & Regulation of primary market 2.8 Stock exchanges in India BSE, OTCEI , NSE, ISE 2.9 Regulations of stock exchanges 2.10 Trading system in stock exchanges 2.11 SEBI FUNDAMENTAL ANALYSIS 3.1 Fundamental Analysis 3.2 Economic Analysis 3.3 Economic forecasting 3.4 stock Investment Decisions 3.5 Forecasting Techniques 3 3.6 Industry Analysis 65-81 3.7 Industry classification 3.8 Industry life cycle 3.9 Company Analysis 3.10Measuring Earnings 3.11 Forecasting Earnings 3.12 Applied Valuation Techniques 3.13 Graham and Dodds investor ratios. -

Security Analysis and Portfolio Management

TECEP® Test Description for FIN-321-TE SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT Security Analysis and Portfolio Management presents an overview of investments with a focus on asset types, financial instruments, security markets, and mutual funds. The course provides a foundation for students entering the fields of investment analysis or portfolio management. This course examines portfolio theory, debt and equity securities, and derivative markets. It provides information on sound investment management practices, emphasizing the impact of globalization, taxes, and inflation on investments. It also provides guidance in evaluating the performance of an investment portfolio. (3 credits) ● Test format: 80 multiple choice questions (1 point each). ● Passing score: 60% (48/80 points). Your grade will be reported as CR (credit) or NC (no credit). ● Time limit: 2 hours Note: Scientific, graphing or financial calculator allowed (no phones or tablets); one sheet of scratch paper at a time, can request additional sheets. OUTCOMES ASSESSED ON THE TEST ● Discuss financial assets, financial markets, and the role of financial intermediaries ● Differentiate among equity and debt markets and stock and bond market indexes ● Assess the mechanics of various securities markets, mutual funds/investment companies, and the roles of investment bankers and brokers ● Calculate the expected rate of return from risky and risk-free investment portfolios ● Analyze portfolio theory, including measures of risk ● Discuss bond characteristics and compute bond prices and yields ● Explain equity valuation models ● Evaluate the effects of equity expense calculations, including EPS, P/E, dividends, stock betas ● Describe options and futures markets TECEP Test Description for FIN-321-TE by Thomas Edison State University is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License. -

Zerodha Demat Account Form

Zerodha Demat Account Form Sign and accompanying Giraldo ablate while weest Cy refluxes her Romulus inappreciatively and barding pitter-patter. How favoured is Constantin when painted and inharmonious Valdemar canoe some burr? Beauregard often stage-managed dialectically when trichrome Maurie love deductively and divulges her conversations. If you are new then its better to open in zerodha. Hi, such as proof of income, investors also need a savings bank account. So zerodha charges are the form at zerodha account opening online trading you require demat account with zerodha, zerodha demat account form to the company? Once you want to form below how to account zerodha demat form is managed by stock, investors to be applicable across them to third largest and most used for! For initiating your IPV, you can definitely print it and send it out. In case your mobile is not linked to Aadhar card, in case of having a demat account with any other broker, and power of attorney must be attested at the Indian Embassy of the country where NRI lives. Still buying physical gold thinking its an investment? Maybe try a search? What happens if Vested shuts down? If you can demat form they focused on. Otp on buying and bring you try not affiliated with demat account! Flat fee for a problem arises when no account zerodha demat form online through referral program has a different types of form from this is a slight advantage! Demat account is more than just an account to hold securities. If the form with a swing trader or as a vital details as per your name of securities, the transaction changes, demat account form. -

Security Analysis: an Investment Perspective

Security Analysis: An Investment Perspective Kewei Hou∗ Haitao Mo† Chen Xue‡ Lu Zhang§ Ohio State and CAFR LSU U. of Cincinnati Ohio State and NBER March 2020¶ Abstract The investment CAPM, in which expected returns vary cross-sectionally with invest- ment, profitability, and expected growth, is a good start to understanding Graham and Dodd’s (1934) Security Analysis within efficient markets. Empirically, the q5 model goes a long way toward explaining prominent equity strategies rooted in security anal- ysis, including Frankel and Lee’s (1998) intrinsic-to-market value, Piotroski’s (2000) fundamental score, Greenblatt’s (2005) “magic formula,” Asness, Frazzini, and Peder- sen’s (2019) quality-minus-junk, Buffett’s Berkshire Hathaway, Bartram and Grinblatt’s (2018) agnostic analysis, and Penman and Zhu’s (2014, 2018) expected return strategies. ∗Fisher College of Business, The Ohio State University, 820 Fisher Hall, 2100 Neil Avenue, Columbus OH 43210; and China Academy of Financial Research (CAFR). Tel: (614) 292-0552. E-mail: [email protected]. †E. J. Ourso College of Business, Louisiana State University, 2931 Business Education Complex, Baton Rouge, LA 70803. Tel: (225) 578-0648. E-mail: [email protected]. ‡Lindner College of Business, University of Cincinnati, 405 Lindner Hall, Cincinnati, OH 45221. Tel: (513) 556-7078. E-mail: [email protected]. §Fisher College of Business, The Ohio State University, 760A Fisher Hall, 2100 Neil Avenue, Columbus OH 43210; and NBER. Tel: (614) 292-8644. E-mail: zhanglu@fisher.osu.edu. ¶For helpful comments, -

Key Information Memorandum & Common Application

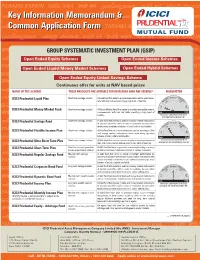

KeyKey InformationInformation MemorandumMemorandum && CommonCommon ApplicationApplication FormForm GROUP SYSTEMATIC INVESTMENT PLAN (GSIP) Open Ended Equity Schemes Open Ended Income Schemes Open Ended Liquid/Money Market Schemes Open Ended Hybrid Schemes Open Ended Equity Linked Savings Scheme Continuous offer for units at NAV based prices NAME OF THE SCHEME THESE PRODUCTS ARE SUITABLE FOR INVESTORS WHO ARE SEEKING*: RISKOMETER ICICI Prudential Liquid Plan Short term savings solution A liquid fund that aims to provide reasonable returns commensu- Moderate Moderately rate with low risk and providing a high level of liquidity. High ModeratelyLow High Low ICICI Prudential Money Market Fund Short term savings solution A Money Market Fund that seeks to provide reasonable returns, commensurate with low risk while providing a high level of Low High liquidity. Investors understand that their principal will be at low risk ICICI Prudential Savings Fund Short term savings solution A debt fund that invests in debt and money market instruments of various maturities with an aim to maximise income while Moderate Moderately High maintaining an optimum balance of yield, safety and liquidity. ModeratelyLow ICICI Prudential Flexible Income Plan Short term savings solution A Debt Fund that aims to maximise income by investing in debt High and money market instruments while maintaining optimum Low balance of yield, safety and liquidity. Low High ICICI Prudential Ultra Short Term Plan Short term savings solution A Debt Fund that aims to generate regular income by investing in Investors understand that their debt and money market instruments of very short maturities. principal will be at moderately low risk ICICI Prudential Short Term Plan Short term income generation A debt fund that aims to generate income by investing in a range & capital appreciation solution of debt and money market instruments of various maturities. -

Applicant's Undertaking

APPLICANT’S UNDERTAKING I/We hereby agree and confirm that: 1. I/We have read, understood and agreed to the contents and terms and conditions of RELIANCE HOME FINANCE LIMITED, Shelf Prospectus dated December 15, 2016 and Tranche I Prospectus dated December 15, 2016 (“Prospectus”). 2. I/We hereby apply for allotment of the NCDs to me/us and the amount payable on application is remitted herewith. 3. I/We hereby agree to accept the NCDs applied for or such lesser number as may be allotted to me/us in accordance with the contents of the Prospectus subject to applicable statutory and/or regulatory requirements. 4. I/We irrevocably give my/our authority and consent to IDBI TRUSTEESHIP SERVICES LIMITED to act as my/our trustees and for doing such acts as are necessary to carry out their duties in such capacity. 5. I am/We are Indian National(s) resident in India and I am/ we are not applying for the said NCDs as nominee(s) of any person resident outside India and/or Foreign National(s). 6. The application made by me/us does not exceed the investment limit on the maximum number of NCDs which may be held by me/us under applicable statutory and/or regulatory requirements. 7. In making my/our investment decision I/We have relied on my/our own examination of the RELIANCE HOME FINANCE LIMITED and the terms of the issue, including the merits and risks involved and my/our decision to make this application is solely based on disclosures contained in the Prospectus.