Multistandard Charger Deployment and Usage in Europe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chademo Statement on European Commission Clean Power for Transport Package

January 24, 2013 CHADEMO STATEMENT ON EUROPEAN COMMISSION CLEAN POWER FOR TRANSPORT PACKAGE The European Commission today (January 24, 2013) published the Clean Power for Transport (CPT) package, including a policy paper on an alternative fuels strategy and the recommendation for standardization on recharging infrastructure for electric vehicles. It is encouraging to see clear targets for the deployment of a minimum number of recharging stations at a national level, which signals the momentum to pick up on Zero Emissions mobility. However, the CHAdeMO association would like to ensure that the CHAdeMO standard is not excluded from the DC fast charging specification. The CHAdeMO standard is used by more than 600 chargers across Europe in Norway, Netherlands, UK, France, and Estonia. There are more than 20,000 CHAdeMO-equipped vehicles on the road in Europe, demonstrating that customers and investors have taken a vested interest in the adoption of electric vehicles. They should not be excluded from this initiative. The CHAdeMO quick-charger is expected to be included in the International Electrotechnical Commission (IEC) standard in the second half of 2013 and the process will be expanded to allow for third party certification to increase the availability of CHAdeMO quick chargers. We request the European Commission consider a dual charging system for DC fast charging with CHAdeMO and CCS (combined charging system) that will allow use by the majority of current and future electric vehicles. From a cost point of view, there are significant commonalities between the two devices of more than 80%, with the only difference relating to communication protocol and charging gun. -

Optimal Locations of Us Fast Charging Stations for Long

He, Kockelman, Perrine 1 1 OPTIMAL LOCATIONS OF U.S. FAST CHARGING STATIONS FOR LONG- 2 DISTANCE TRIPS BY BATTERY ELECTRIC VEHICLES 3 4 Yawei He 5 Graduate Research Assistant 6 Department of Management Science and Engineering 7 Beijing Institute of Technology 8 Tel: +86 18611915120; [email protected] 9 10 Kara M. Kockelman, Ph.D., P.E. 11 Corresponding Author 12 Professor, and E.P. Schoch Professor in Engineering 13 Department of Civil, Architectural and Environmental Engineering 14 The University of Texas at Austin 15 Tel: 512-471-0210; Fax: 512-475-8744; [email protected] 16 17 Kenneth A. Perrine 18 Research Associate 19 Center for Transportation Research 20 The University of Texas at Austin 21 [email protected] 22 23 Presented at the 97th Annual Meeting of the Transportation Research Board, Washington, D.C., 24 January 2018 and published in Journal of Cleaner Production 214: 452-461 (2019) 25 26 ABSTRACT 27 Due to environmental and energy challenges, promoting battery electric vehicles (BEVs) is 28 a popular policy for many countries. However, lack of fast recharging infrastructure and 29 limitations on BEV range moderate their purchase and use. It is important to have a well- 30 designed charging station network, so this paper uses U.S. long-distance travel data to place 31 charging stations in order to maximize long-distance trip completions. Each scenario assumes a 32 certain number of charging stations (from 50 to 250, across the U.S.) and vehicle range (from 60 33 mi to 250 mi). 34 The problem is formulated as a mixed integer program, and a modified flow-refueling 35 location model (FRLM) model is solved via a branch-and-bound algorithm. -

Fast Charging: an In-Depth Look at Market Penetration, Charging Characteristics, and Advanced Technologies

EVS27 Barcelona, Spain, November 17-20, 2013 Fast Charging: An In-Depth Look at Market Penetration, Charging Characteristics, and Advanced Technologies Satish Rajagopalan1, Arindam Maitra1, John Halliwell1, Morgan Davis1, Mark Duvall1 1Electric Power Research Institute (EPRI), USA Abstract Plug-in Electric Vehicles (PEVs) are now available in many North American and European markets, with more models expected to become available to consumers in the coming years. These vehicles will present utilities with opportunities as well as challenges as their numbers potentially grow to hundreds of thousands of vehicles connected to the electric grid for charging. In order to support PEV adoption in the market place, it is expected that consumers will demand faster charge rates especially for the all electric vehicles. Faster charge rates require higher power electrical charging systems and the infrastructure to support these fast charging systems. With a view to comprehensively understand the impact of DC fast charging on the customer as well as the electric utility, Electric Power Research Institute (EPRI) has been conducting detailed research into the market potential, technical capabilities, and installation costs. Demand charges and installation costs are currently the most significant barriers widespread adoption of fast charging. Creating a sustainable business case for fast charging will require economics that match utilization. This paper will discuss these findings in depth and will also provide an update on the status of DC fast charging related standards. With a view to address these shortcomings, EPRI has developed a direct medium-voltage fed all solid-state fast charging system, the Utility Direct Medium Voltage Fast Charger (UDFC). -

EV Charging Infrastructure Market Research

Service Abstract – EVSE Charging Points ($6,000) Power Technology Research LLC ©2018 Introduction With the increasing number of Electric Vehicles (EV) on a global scale, EV charging has become an essential aspect of car ownership. To compete with internal combustion engine (ICE) vehicles, the charging time of EVs needs to be at similar levels as refueling conventional vehicles. Historically speaking, charging stations technology dates to the same time as EVs. Charging stations in the early 1900s utilized bulky mercury-arc rectifiers, essentially glass bulbs containing liquid mercury. However, today’s technology has improved exponentially with advancements in power electronics. In the modern era, EV chargers started the technological journey as a device that could recharge a car overnight. This advancement did not come cheap as they were a result of significant investment in research and development . The result has made the recharging experience comparable to a refueling stop for a conventional car. EVSE in Europe - 2017 35000 30000 25000 20000 15000 10000 5000 0 Level 1 Level 2 CHAdeMO CCS Tesla SC Service Description In this service, PTR covers EV charging infrastructure market in five major regions/countries around the globe. Market growth outlook for all charging power capacities will be tracked in this coverage. Forecast Countries Base Year 2014-2018 APAC Cyprus Luxembourg Forecast 2019-2024 China Czech Republic Malta Capacity (kW) India Denmark Norway 0-3 kW Japan Estonia The Netherlands 4-22 kW South Korea Finland Poland 23-60 kW North America France Portugal 61-150 kW United States Germany Romania 151-350 kW Canada Greece Slovakia Standards Mexico Hungary Slovenia Tesla SC Europe Iceland Spain CCS Austria Ireland Sweden CHAdeMO Belgium Italy Switzerland Bulgaria Latvia Turkey Croatia Lithuania United Kingdom Excel Output Tables Customers can download the excel tables at any point in time. -

Electric Vehicles – Country Update from Ireland

Electric Vehicles – Country Update from Ireland Graham Brennan Transport Programme Manager IA-HEV Task 1 Information Exchange 30th April 2015 Gwangju Overview • Progress in Ireland – Introduction to Ireland – Cars – Infrastructure • Technology Perspective Energy Infrastructure of Ireland • 4.7GW peak elect demand 250-500MW DC to Scotland – 2GW of wind Corrib Gas Gas Field – Gas, Coal, Peat £ Connections • Energy Imports 89% to Scotland • RE potential >> 100% AC Inter- • Single Electricity System connectors 500MW DC operator to Wales – Very supportive of EVs € – Faster decisions and consistent approach • (No car industry) Design Study for 700MW DC to France Rep. of Ireland v Rep. of Korea • Republic of Ireland – 4.7GW – 4.5m people – 2m cars – Electrical Energy (2012) • 18.2% Renewables • Republic of Korea – 80.5GW – 51m people – 19m cars – Electrical Energy (2012) • 1.8% Renewables Source: IEA 2012 Country Statistics EV Registrations in Ireland - 850 EVs in Total (Ireland has 2m Passenger Cars) 900 x3? 800 700 600 500 x2? 400 x5 300 200 EV Registrations Per Annum Per EV Registrations 100 0 2011 2012 2013 2014 2015 Cars Registered per Manufacturer 600 500 400 300 200 100 0 Public Charging Infrastructure • Ireland – AC Charge Points (22kW) = 820 – Fast Chargers (Chademo with some Combo) = 69 • Northern Ireland – AC Charge Points (22kW) = 320 – Fast Chargers (Chademo) = 14 • EU TEN-T (First EU Country) – 50% Funding for Chargers on main interurban routes & modal hubs Charge Point Management & Billing System • RFID Card • Roaming – Republic -

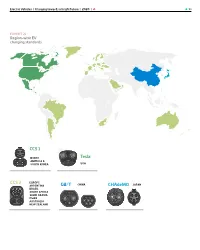

^ GB/T Chademo JAPAN CCS 2 Tesla CCS 1

Electric Vehicles Charging towards a bright future 2020 ^ 51 EXHIBIT 21 Region-wise EV charging standards CCS 1 NORTH Tesla AMERICA & SOUTH KOREA USA CCS 2 EUROPE ARGENTINA GB/T CHINA CHAdeMO JAPAN BRAZIL SOUTH AFRICA SAUDI ARABIA OMAN AUSTRALIA NEW ZEALAND Electric Vehicles Charging towards a bright future 2020 ^ 52 EXHIBIT 22 EV charging standards summary PARAMETER SLOW CHARGERS FAST CHARGERS LEVEL Level 1 Level 2 Level 3 Level 3 AC OR DC AC AC/DC AC DC POWER RANGE <3.7 kW 3.7 – 22 kW 22 – 43.5 kW <400 kW MODE Mode 1 and 2 Mode 3 Mode 3 Mode 4 TYPE Domestic sockets IEC Type 1 IEC Type 2 CCS Combo 1 & 2 IEC Type 2 IEC Type 3 CHAdeMO, GB/T DC and Tesla connector PLACE OF USE Home Home/Public Public Public VEHICLES 2W, 3W, Cars 2W, 3W, Cars Cars and Buses Cars and Buses CUSTOMERS OEM/Retail OEM/Retail, Charging Charging Charging Operators Operators Operators India's stance India has still not formally adopted any specific charging standard. Over the years, the central on EV Charging government has tried to come up with guidelines to assist the charging ecosystem. The government has been flexible around standards and OEMs have been making their choice independently. As the industry picks up and adoption increases, a formal charging standard might be adopted by the country. Electric Vehicles Charging towards a bright future 2020 ^ 53 03 Global EV 54 EV — A common dream across the world Industry 57 Evolution of key markets — China, United States, Europe and Japan 66 Global battery industry Electric Vehicles Charging towards a bright future 2020 ^ 54 Global EV Industry Electric Vehicles — A common dream across the world The first electric cars were developed in the early Tesla has been a game changer for electric vehicles. -

Frequently Asked Questions

Frequently Asked Questions FLEETS What vehicles are available to purchase in Minnesota? PlugInConnect posts an updated guide on electric vehicles available for purchase in the Midwest. It covers both battery electric vehicles and plug-in hybrid electric vehicles. The guide can be accessed at www.pluginconnect.com/mnpevmodels Which electric vehicles are the most commonly sold in Minnesota? The Tesla Model S is the most frequently sold EV in Minnesota, but its high cost can make it unattractive for city fleets. There are many battery electric vehicles and plug-in hybrid electric vehicles with fewer sales but are fantastic for fleet use. More affordable examples include the Nissan Leaf, Chevy Bolt, and Mitsubishi Outlander, to name a few. Which electric vehicles are the best ones for Minnesota’s cold climate? It’s a common misconception that EVs have poor performance in winter since they’re primarily front-wheel drive vehicles. Anecdotally, however, we’ve heard from several EV owners that an EV with snow tires outperforms an all-wheel drive vehicle with all-weather tires. That being said, newer vehicles are better suited to cold weather because of constantly evolving battery technology. While you shouldn’t expect to slip and slide in an EV in the winter, you should anticipate a 30% drop in battery range. Planning ahead, utilizing the heated seats and steering wheel, and minimizing cabin heat can improve the impact felt by winter battery range. Additionally, keep in mind that Norway and Iceland are currently leading the world in number of EVs sold, and they have much colder climates than ours! What vehicles are covered in the State Contract? Vehicles included in the state contract can be found on the Office of State Procurement website and can only be purchased by Cooperative Purchasing Venture members. -

Interoperability of Public Electric Vehicle Charging Infrastructure

Interoperability of Public Electric Vehicle Charging Infrastructure INTRODUCTION This paper is a cooperative effort of the Electric Power Research Institute (EPRI), the Edison Electric Institute (EEI), the Alliance for Transportation Electrification (ATE), the American Public Power Association (APPA), and the National Rural Electric Cooperative Association (NRECA) to identify challenges, create awareness, and provide perspective to achieve greater interoperability and open standards in the burgeoning U.S. electric vehicle (EV) charging market. By definition,interoperability is the MOTIVATION ability for multiple systems to work The electric vehicle market is rapidly accelerating, as is investment together without restriction. With in the charging infrastructure needed to support this growing regards to electric vehicle charging market. While the vast majority of EV charging now takes place infrastructure, interoperability refers at home and at work, widespread, open-access public charging to the compatibility of key system infrastructure will be essential to support EV drivers beyond components—vehicles, charging early adopters. Visible public infrastructure is a must for more stations, charging networks, and the customers to consider EVs as viable for meeting all of their driving grid—and the software systems that needs—from daily commutes to major expeditions—while also support them, allowing all components supporting drivers who might not have access to workplace or home charging (such as apartment dwellers and other drivers to work seamlessly and effectively. without dedicated residential parking). As a general expectation, Research and stakeholder engagement over the last decade have public EV charging infrastructure should be convenient and shown that interoperable, transparent, open standards-based reliable for drivers to use. -

Electric Vehicle Charging Study

DriveOhio Team Patrick Smith, Interim Director Luke Stedke, Managing Director, Communications Julie Brogan, Project Manager Authors Katie Ott Zehnder, HNTB Sam Spofforth, Clean Fuels Ohio Scott Lowry, HNTB Andrew Conley, Clean Fuels Ohio Santos Ramos, HNTB Cover Photograph By Bruce Hull of the FRA-70-14.56 (Project 2G) ODOT roadway project in coordination with which the City of Columbus, through a competitive bid, hired GreenSpot to install a DCFC on Fulton Street immediately off I-70/I-71 and adjacent to the Columbus Downtown High School property between Fourth Street and Fifth Street. Funding support for the electric vehicle DCFC was provided by AEP Ohio and Paul G. Allen Family Foundation. Table of Contents List of Abbreviations ................................................................................................................................................... v Executive Summary ..................................................................................................................................................... 1 Charging Location Recommendations................................................................................................................................................... 1 Cost Estimate ........................................................................................................................................................................................... 4 Next Steps ............................................................................................................................................................................................... -

Overview and Characteristics of the Ev Fast Charging Connector Systems

Maszyny Elektryczne - Zeszyty Problemowe Nr 3/2017 (115) 91 Damian Dobrzański Politechnika Lubelska OVERVIEW AND CHARACTERISTICS OF THE EV FAST CHARGING CONNECTOR SYSTEMS PRZEGLĄD I CHARAKTERYSTYKA STANDARDÓW ZŁĄCZY SZYBKIEGO ŁADOWANIA POJAZDÓW EV Abstract: The paper presents the existing connector systems designed for fast charging EV battery. The work has paid particular attention for differences between charging systems like nominal voltage, speed of charging, plug type and place of occurrences. Streszczenie: Artykuł przedstawia przegląd istniejących systemów złączy do ładowania akumulatorów pojazdów elektrycznych. Zwrócono w nim szczególną uwagę na różnice pomiędzy poszczególnymi standardami takimi jak typ złącza, napięcie ładowania, dokonano również analizy ich popularności oraz możliwości rozwoju. Keywords: Fast charging connectors, Tesla Supercharger, CHAdeMO, SAE CCS, SAE J1772, AC charging, DC fast charging, EV Słowa kluczowe: złącza szybkie ładowanie, Tesla Supercharger, CHAdeMO, SAE CCS, SAE J1772 , ładowanie AC, szybkie ładowanie DC, pojazdy elektryczne 1. Introduction Converters [1] as well as Control Strategies and In the last few years, the automotive world has topologies of DC/DC converters [2]. witnessed a real revolution. Decade ago On this moment we have a few fast charging nobody even thought that diesel engines which systems, in this paper was presented a first- are dominated a market in first years of XXI dominating 3 systems Japanese CHAdeMO, century will be gradually withdrawn from the American SAE J1772 Combo (IEC type 1) and automotive solutions. European IEC 62196-2 type 2 Combo Charging Universal striving to reduce climate changes System ( IEC CCS type 2) all types of charging forces car producers to use hybrid powertrains systems are divided to 4 mode: or to completely abandon their conventional -Mode 1- directly passive connection between internal combustion engines for electrical or grid and EV, only AC charging in EU 250V for hydrogen solutions. -

EPD's Presentation on EV Charging Facilities

Development of Electric Vehicle Charging Network (Technical Guidelines On Charging Facilities For Electric Vehicles) 14 September 2018 Environmental Protection Department Why Electric Vehicles ? • Electric vehicles (EVs) have no tailpipe emissions • Replacing conventional vehicles with EVs can improve roadside air quality • Commercial vehicles account for 95% of emissions from vehicle fleet. Promoting wider use of commercial EVs and use of public transport should take priority. 2 Promoting EV – the Challenges • Problems – Cost – Service life of battery – Charging time – Land and space – Spare electricity supply Spare Electricity Supply - Concern on spare power supply to existing buildings - The two power companies provide one-stop services for EV chargers - If additional power supply is required, the two power companies may provide assistance Solutions • Key parties should work together Government Industry / Research & Business Development sector Institutes Success of Promotion on EVs Charging support for EVs • EVs should preferably be charged at homes or workplaces. Role of Public Charging Network • Public chargers are for opportunity charging, topping up batteries to complete remaining journeys of EVs when necessary. • Medium chargers should form backbone of Government public charging network Charging support for EVs • As at end June 2018, there are some 1,970 public EV chargers (Government & private ones), including – 739 medium chargers – 385 quick chargers Technical Guidelines On Charging Facilities For Electric Vehicles Issued by the Electrical and Mechanical Services Department Purpose of the Technical Guidelines • Set out the statutory requirements and general guidelines for installation of charging facilities for EVs in Hong Kong. Statutory Requirements • EV charging facilities are fixed electrical installations (FEI) and shall comply with the relevant requirements of the Electricity Ordinance (Cap. -

Wait the Opportunities Around Electric Vehicle Charge Points in the UK Contents

Hurry up and… wait The opportunities around electric vehicle charge points in the UK Contents 1. Executive summary 01 2. Introduction 02 3. How many chargers will be needed? 04 4. Charging segments 05 5. DC or not DC? That is the question 07 6. The infrastructure value chain 09 7. Models seen elsewhere 12 8. Next steps 14 9. Appendix: Investment calculations 15 10. Key contacts 17 Hurry up and… wait | The opportunities around electric vehicle charge points in the UK 1. Executive summary How quickly electric vehicles (EVs) will become The EV charging infrastructure market is young and fragmented, a major form of transport is a source of much and companies from a variety of different sectors are entering it. Those looking to get into this market need to act fast, but then be debate. A shortage of public charge points will prepared to wait: it is expected to become profitable only when deter adoption. EVs make up at least five per cent of vehicles in circulation, or about two million units. The key question for participants is where to play We modelled three scenarios for what the UK market will need to and what activity areas to be part of. 2030: a low case if uptake is slower than expected (two million EV units); the central case; and a high uptake case if the EV adoption We expect to see three business models prevail in the UK in the coming rate exceeds expectations (10.5 million units). In our central years. A public model, where government bodies offer funding that estimates, we assume seven million EVs in circulation, requiring private companies use to recover at least a portion of the investment around 28,000 public charging points, and capital expenditure of costs.