The Long Tail / Chris Anderson

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Excesss Karaoke Master by Artist

XS Master by ARTIST Artist Song Title Artist Song Title (hed) Planet Earth Bartender TOOTIMETOOTIMETOOTIM ? & The Mysterians 96 Tears E 10 Years Beautiful UGH! Wasteland 1999 Man United Squad Lift It High (All About 10,000 Maniacs Candy Everybody Wants Belief) More Than This 2 Chainz Bigger Than You (feat. Drake & Quavo) [clean] Trouble Me I'm Different 100 Proof Aged In Soul Somebody's Been Sleeping I'm Different (explicit) 10cc Donna 2 Chainz & Chris Brown Countdown Dreadlock Holiday 2 Chainz & Kendrick Fuckin' Problems I'm Mandy Fly Me Lamar I'm Not In Love 2 Chainz & Pharrell Feds Watching (explicit) Rubber Bullets 2 Chainz feat Drake No Lie (explicit) Things We Do For Love, 2 Chainz feat Kanye West Birthday Song (explicit) The 2 Evisa Oh La La La Wall Street Shuffle 2 Live Crew Do Wah Diddy Diddy 112 Dance With Me Me So Horny It's Over Now We Want Some Pussy Peaches & Cream 2 Pac California Love U Already Know Changes 112 feat Mase Puff Daddy Only You & Notorious B.I.G. Dear Mama 12 Gauge Dunkie Butt I Get Around 12 Stones We Are One Thugz Mansion 1910 Fruitgum Co. Simon Says Until The End Of Time 1975, The Chocolate 2 Pistols & Ray J You Know Me City, The 2 Pistols & T-Pain & Tay She Got It Dizm Girls (clean) 2 Unlimited No Limits If You're Too Shy (Let Me Know) 20 Fingers Short Dick Man If You're Too Shy (Let Me 21 Savage & Offset &Metro Ghostface Killers Know) Boomin & Travis Scott It's Not Living (If It's Not 21st Century Girls 21st Century Girls With You 2am Club Too Fucked Up To Call It's Not Living (If It's Not 2AM Club Not -

The Weekly Newsletter of Ucsd Connect

TUESDAY MARCH 31,1998 ISSUE 8-12 HTTP://WWW.CONNECT.ORG/CONNECT [email protected] connectTHE WEEKLY NEWSLETTER OF UCSD CONNECT GEORGE GILDER TO PEEK INTO COMMQUEST/IBM TO CREATE NEW FUTURE AT MAY 27 TELCOM EVENT GENERATION OF MOBILE APPLIANCES By Debbie Andersen, QUALCOMM ([email protected]) By Ann Marsh ([email protected]) George Gilder has spoken at the Vatican, testified before United On February 11 of this year, IBM announced a $180 million States Senate sub-committees on Science and Technology, and buyout merger agreement with CommQuest Technologies, Inc., a Commerce, Science and Transportation, been quoted by Ronald privately held company based in Encinitas, California, which designs Reagan more than any other living author, written speeches for Ri- and markets advanced semiconductors for wireless and digital com- chard Nixon and Nelson Rockefeller, studied under Henry munications applications such as cellular phones and satellite com- Kissinger at Harvard and been interviewed in Playboy. One of his munications. Once the merger is completed, CommQuest will be- books, "The Spirit of Enterprise", is credited with sparking the entre- come part of IBM's Microelectronics Division, speeding development preneurial growth of technology investment and of Silicon Valley. His book "Microcosm" \s a history of that growth and his next book, of a new generation of multifunction, low-cost, mobile "information "Telecosm" is the eagerly awaited look into the future of the appliances," such as single chip, watch-size cellular phones and prod- communication's industry. On May 27,1998, George Gilder will be ucts that combine cell phone, e-mail and Internet access functions giving San Diego a peek into that future, as the luncheon speaker at in a single, hand-held package. -

To Make Claims About Or Even Adequately Understand the "True Nature" of Organizations Or Leadership Is a Monumental Task

BooK REvrnw: HERE CoMES EVERYBODY: THE PowER OF ORGANIZING WITHOUT ORGANIZATIONS (Clay Shirky, Penguin Press, 2008. Hardback, $25.95] -CHRIS FRANCOVICH GONZAGA UNIVERSITY To make claims about or even adequately understand the "true nature" of organizations or leadership is a monumental task. To peer into the nature of the future of these complex phenomena is an even more daunting project. In this book, however, I think we have both a plausible interpretation of organ ization ( and by implication leadership) and a rare glimpse into what we are becoming by virtue of our information technology. We live in a complex, dynamic, and contingent environment whose very nature makes attributing cause and effect, meaning, or even useful generalizations very difficult. It is probably not too much to say that historically the ability to both access and frame information was held by the relatively few in a system and structure whose evolution is, in its own right, a compelling story. Clay Shirky is in the enviable position of inhabiting the domain of the technological elite, as well as being a participant and a pioneer in the social revolution that is occurring partly because of the technologies and tools invented by that elite. As information, communication, and organization have grown in scale, many of our scientific, administrative, and "leader-like" responses unfortu nately have remained the same. We find an analogous lack of appropriate response in many followers as evidenced by large group effects manifested through, for example, the response to advertising. However, even that herd like consumer behavior seems to be changing. Markets in every domain are fragmenting. -

Adult Contemporary Radio at the End of the Twentieth Century

University of Kentucky UKnowledge Theses and Dissertations--Music Music 2019 Gender, Politics, Market Segmentation, and Taste: Adult Contemporary Radio at the End of the Twentieth Century Saesha Senger University of Kentucky, [email protected] Digital Object Identifier: https://doi.org/10.13023/etd.2020.011 Right click to open a feedback form in a new tab to let us know how this document benefits ou.y Recommended Citation Senger, Saesha, "Gender, Politics, Market Segmentation, and Taste: Adult Contemporary Radio at the End of the Twentieth Century" (2019). Theses and Dissertations--Music. 150. https://uknowledge.uky.edu/music_etds/150 This Doctoral Dissertation is brought to you for free and open access by the Music at UKnowledge. It has been accepted for inclusion in Theses and Dissertations--Music by an authorized administrator of UKnowledge. For more information, please contact [email protected]. STUDENT AGREEMENT: I represent that my thesis or dissertation and abstract are my original work. Proper attribution has been given to all outside sources. I understand that I am solely responsible for obtaining any needed copyright permissions. I have obtained needed written permission statement(s) from the owner(s) of each third-party copyrighted matter to be included in my work, allowing electronic distribution (if such use is not permitted by the fair use doctrine) which will be submitted to UKnowledge as Additional File. I hereby grant to The University of Kentucky and its agents the irrevocable, non-exclusive, and royalty-free license to archive and make accessible my work in whole or in part in all forms of media, now or hereafter known. -

Annexes Etude Sur Les Relations Entre Tf1 Et Metropole Television Et La Production Phonographique

ANNEXES ETUDE SUR LES RELATIONS ENTRE TF1 ET METROPOLE TELEVISION ET LA PRODUCTION PHONOGRAPHIQUE ANNEXE 1............................................................................................................................................... 2 LES DIVERTISSEMENTS MUSICAUX OU À COMPOSANTE MUSICALE SUR M6..................................................... 2 JUILLET ..................................................................................................................................................... 2 ANNEXE 2............................................................................................................................................. 10 LES DIVERTISSEMENTS MUSICAUX OU À COMPOSANTE MUSICALE SUR M6................................................... 10 NOVEMBRE.............................................................................................................................................. 10 ANNEXE 3............................................................................................................................................. 18 LES DIVERTISSEMENTS MUSICAUX OU À COMPOSANTE MUSICALE SUR M6................................................... 18 DÉCEMBRE .............................................................................................................................................. 18 ANNEXE 4............................................................................................................................................. 25 LES DIVERTISSEMENTS MUSICAUX OU À -

Women's Experimental Autobiography from Counterculture Comics to Transmedia Storytelling: Staging Encounters Across Time, Space, and Medium

Women's Experimental Autobiography from Counterculture Comics to Transmedia Storytelling: Staging Encounters Across Time, Space, and Medium Dissertation Presented in partial fulfillment of the requirement for the Degree Doctor of Philosophy in the Graduate School of Ohio State University Alexandra Mary Jenkins, M.A. Graduate Program in English The Ohio State University 2014 Dissertation Committee: Jared Gardner, Advisor Sean O’Sullivan Robyn Warhol Copyright by Alexandra Mary Jenkins 2014 Abstract Feminist activism in the United States and Europe during the 1960s and 1970s harnessed radical social thought and used innovative expressive forms in order to disrupt the “grand perspective” espoused by men in every field (Adorno 206). Feminist student activists often put their own female bodies on display to disrupt the disembodied “objective” thinking that still seemed to dominate the academy. The philosopher Theodor Adorno responded to one such action, the “bared breasts incident,” carried out by his radical students in Germany in 1969, in an essay, “Marginalia to Theory and Praxis.” In that essay, he defends himself against the students’ claim that he proved his lack of relevance to contemporary students when he failed to respond to the spectacle of their liberated bodies. He acknowledged that the protest movements seemed to offer thoughtful people a way “out of their self-isolation,” but ultimately, to replace philosophy with bodily spectacle would mean to miss the “infinitely progressive aspect of the separation of theory and praxis” (259, 266). Lisa Yun Lee argues that this separation continues to animate contemporary feminist debates, and that it is worth returning to Adorno’s reasoning, if we wish to understand women’s particular modes of theoretical ii insight in conversation with “grand perspectives” on cultural theory in the twenty-first century. -

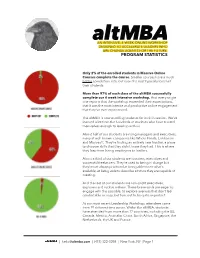

Program Statistics

AN INTENSIVE, 4-WEEK ONLINE WORKSHOP DESIGNED TO ACCELERATE LEADERS WHO ARE CHANGE AGENTS FOR THE FUTURE. PROGRAM STATISTICS Only 2% of the enrolled students in Massive Online Courses complete the course. Smaller courses have a much better completion rate, but even the best typically lose half their students. More than 97% of each class of the altMBA successfully complete our 4 week intensive workshop. And every single one reports that the workshop exceeded their expectations, that it was the most intense and productive online engagement that they’ve ever experienced. The altMBA is now enrolling students for its fifth session. We’ve learned a lot from the hundreds of students who have trusted themselves enough to level up with us. About half of our students are rising managers and executives, many at well-known companies like Whole Foods, Lululemon and Microsoft. They’re finding an entirely new frontier, a place to discover skills that they didn’t know they had. This is where they leap from being employees to leaders. About a third of our students are founders, executives and successful freelancers. They’re used to being in charge but they’re not always practiced at being able to see what’s available, at being able to describe a future they are capable of creating. And the rest of our students are non-profit executives, explorers and ruckus makers. These brave souls are eager to engage with the possible, to explore avenues that don’t feel comfortable or easy, but turn out to be quite important. At our most recent Leadership Workshop, attendees came from 19 different time zones. -

REPORT the Barron's Bears

GILDER February 2006 / Vol. XI No. 2 T E C H N O L O G Y R E P O R T The Barron’s Bears ur Celestial Empire possesses all things in abundance “ and lacks no products within its border. There is there- O fore no need to import the manufactures of outside barbarians.” —Emperor Qian Long, 1793, to King George III’s Ambassador (quoted in Fast Boat to China by Andrew Ross). It’s mid-winter, snowing again outside my window. After some 60 days of cross country skiing so far in Western Massachusetts, two schusses to Silicon Valley, and my son Richard a newly instrument rated pilot, I feel pretty good. With Dick Sears’ Gilder Technology Index (www.GTIndex.com) up some 325 percent since the crash and 27 percent in the last Power-One is the 52 weeks, I feel pretty fl ush. But as I prepare for another day of Nordic sweltering up and swooping down, something nags in the back of my mind. leader in digital What could it be? Flaws in the Linley Group’s projection of EZchip’s (LNOP) coming three year revenue ramp? A slow IPTV (Internet protocol television) transition dragging power solutions, (CONTINUED ON PAGE 2) with some 50 FEATURED COMPANY: NetLogic (NETL) design wins for Whoa! It seems the only thing fl ying faster than NetLogic’s processor speeds these days is the company’s stock price, up by a whopping third so far in the fi rst month or so of the year. But after listening to CEO Ron Jankov, it’s hard to be anything but buoyant. -

My Bloody Valentine's Loveless David R

Florida State University Libraries Electronic Theses, Treatises and Dissertations The Graduate School 2006 My Bloody Valentine's Loveless David R. Fisher Follow this and additional works at the FSU Digital Library. For more information, please contact [email protected] THE FLORIDA STATE UNIVERSITY COLLEGE OF MUSIC MY BLOODY VALENTINE’S LOVELESS By David R. Fisher A thesis submitted to the College of Music In partial fulfillment of the requirements for the degree of Master of Music Degree Awarded: Spring Semester, 2006 The members of the Committee approve the thesis of David Fisher on March 29, 2006. ______________________________ Charles E. Brewer Professor Directing Thesis ______________________________ Frank Gunderson Committee Member ______________________________ Evan Jones Outside Committee M ember The Office of Graduate Studies has verified and approved the above named committee members. ii TABLE OF CONTENTS List of Tables......................................................................................................................iv Abstract................................................................................................................................v 1. THE ORIGINS OF THE SHOEGAZER.........................................................................1 2. A BIOGRAPHICAL ACCOUNT OF MY BLOODY VALENTINE.………..………17 3. AN ANALYSIS OF MY BLOODY VALENTINE’S LOVELESS...............................28 4. LOVELESS AND ITS LEGACY...................................................................................50 BIBLIOGRAPHY..............................................................................................................63 -

Conceptions of Authenticity in Fashion Blogging

“They're really profound women, they're entrepreneurs”: Conceptions of Authenticity in Fashion Blogging Alice E. Marwick Department of Communication & Media Studies Fordham University Bronx, New York, USA [email protected] Abstract Repeller and Tavi Gevinson of Style Rookie, are courted by Fashion blogging is an international subculture comprised designers and receive invitations to fashion shows, free primarily of young women who post photographs of clothes, and opportunities to collaborate with fashion themselves and their possessions, comment on clothes and brands. Magazines like Lucky and Elle feature fashion fashion, and use self-branding techniques to promote spreads inspired by and starring fashion bloggers. The themselves and their blogs. Drawing from ethnographic interviews with 30 participants, I examine how fashion bloggers behind The Sartorialist, What I Wore, and bloggers use “authenticity” as an organizing principle to Facehunter have published books of their photographs and differentiate “good” fashion blogs from “bad” fashion blogs. commentary. As the benefits accruing to successful fashion “Authenticity” is positioned as an invaluable, yet ineffable bloggers mount, more women—fashion bloggers are quality which differentiates fashion blogging from its overwhelmingly female—are starting fashion blogs. There mainstream media counterparts, like fashion magazines and runway shows, in two ways. First, authenticity describes a are fashion bloggers in virtually every city in the United set of affective relations between bloggers and their readers. States, and fashion bloggers hold meetups and “tweet ups” Second, despite previous studies which have positioned in cities around the world. “authenticity” as antithetical to branding and commodification, fashion bloggers see authenticity and Fashion bloggers and their readers often consider blogs commercial interests as potentially, but not necessarily, to be more authentic, individualistic, and independent than consistent. -

ARIA Charts, 1996-04-21 to 1996-06-02

Enjoy CifqrZ ria a TRADE MARK REGD CHART AUS TR A LIAN SINGLES CHA VMS CHART TW LW TI TITLE / ARTIST 1W LW TI TITLE / ARTIST 1 1 8 HOW BIZARRE O.M.C. HUH/POL 5776202 1 1 35 JAGGED LITTLE PILL Alanis Morissette A3 WEA/WAR 9362459012 2 2 10 MISSING THE REMIX EP Everything But The Girl • WEA/WAR 2 3 27 (WHAT'S THE STORY) MORNING GLORY Oasis A4 CRE/SONY 481020.2 3 4 8 FATHER & SON Boyzone PDR/POL 5776792 3 2 5 FALLING INTO YOU Celine Dion A EPI/SONY 483792.2 4 3 12 ONE OF US Joan Osborne A MER/POL 8523682 4 6 16 PRESIDENTS OF THE U.S.A. Presidents Of The U.S.A. A COL/SONY 481039.2 5 6 3 CALIFORNIA LOVE 2Pac ISUPOL 8545692 5 4 21 THE MEMORY OF TREES Enya A3 WEA/WAR 0630128792 6 7 9 ANYTHING 3T EPI/SONY 662696.2 6 8 9 TENNESSEE MOON Neil Diamond A COUSONY 481378.2 7 5 9 SPACEMAN Babylon Zoo • EMI 8826492 7 7 20 NEW BEGINNING Tracy Chapman A WEA/WAR 7559618502 8 10 5 IRONIC Alanis Morissette WEA/WAR 93624365 8 9 25 MELLON COLLIE &THE INFINITE SADNESS Smashing Pumpkins A VIR/EMI 8408642 9 8 12 POWER OFA WOMAN Eternal EMI 8825142 9 5 3 TINY MUSIC... FROM THE VATICAN GIFT SHOP Stone Temple Pilots EW/WAR 7567828712 * 10 NEW SALVATION The Cranberries ISUPOL 8546172 10 11 2 GREATES ITS VOLUME 1 Take That BMG 4321355582 11 9 9 GET DOWN ON IT Peter Andre (Feat. -

“Punk Rock Is My Religion”

“Punk Rock Is My Religion” An Exploration of Straight Edge punk as a Surrogate of Religion. Francis Elizabeth Stewart 1622049 Submitted in fulfilment of the doctoral dissertation requirements of the School of Language, Culture and Religion at the University of Stirling. 2011 Supervisors: Dr Andrew Hass Dr Alison Jasper 1 Acknowledgements A debt of acknowledgement is owned to a number of individuals and companies within both of the two fields of study – academia and the hardcore punk and Straight Edge scenes. Supervisory acknowledgement: Dr Andrew Hass, Dr Alison Jasper. In addition staff and others who read chapters, pieces of work and papers, and commented, discussed or made suggestions: Dr Timothy Fitzgerald, Dr Michael Marten, Dr Ward Blanton and Dr Janet Wordley. Financial acknowledgement: Dr William Marshall and the SLCR, The Panacea Society, AHRC, BSA and SOCREL. J & C Wordley, I & K Stewart, J & E Stewart. Research acknowledgement: Emily Buningham @ ‘England’s Dreaming’ archive, Liverpool John Moore University. Philip Leach @ Media archive for central England. AHRC funded ‘Using Moving Archives in Academic Research’ course 2008 – 2009. The 924 Gilman Street Project in Berkeley CA. Interview acknowledgement: Lauren Stewart, Chloe Erdmann, Nathan Cohen, Shane Becker, Philip Johnston, Alan Stewart, N8xxx, and xEricx for all your help in finding willing participants and arranging interviews. A huge acknowledgement of gratitude to all who took part in interviews, giving of their time, ideas and self so willingly, it will not be forgotten. Acknowledgement and thanks are also given to Judy and Loanne for their welcome in a new country, providing me with a home and showing me around the Bay Area.