Semiconductor Contract Manufacturing Worldwide, 1997

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PART I ITEM 1. BUSINESS Industry We Are

PART I ITEM 1. BUSINESS Industry We are the world’s largest semiconductor chip maker, based on revenue. We develop advanced integrated digital technology products, primarily integrated circuits, for industries such as computing and communications. Integrated circuits are semiconductor chips etched with interconnected electronic switches. We also develop platforms, which we define as integrated suites of digital computing technologies that are designed and configured to work together to provide an optimized user computing solution compared to ingredients that are used separately. Our goal is to be the preeminent provider of semiconductor chips and platforms for the worldwide digital economy. We offer products at various levels of integration, allowing our customers flexibility to create advanced computing and communications systems and products. We were incorporated in California in 1968 and reincorporated in Delaware in 1989. Our Internet address is www.intel.com. On this web site, we publish voluntary reports, which we update annually, outlining our performance with respect to corporate responsibility, including environmental, health, and safety compliance. On our Investor Relations web site, located at www.intc.com, we post the following filings as soon as reasonably practicable after they are electronically filed with, or furnished to, the U.S. Securities and Exchange Commission (SEC): our annual, quarterly, and current reports on Forms 10-K, 10-Q, and 8-K; our proxy statements; and any amendments to those reports or statements. All such filings are available on our Investor Relations web site free of charge. The SEC also maintains a web site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. -

Micron Technology Inc

MICRON TECHNOLOGY INC FORM 10-K (Annual Report) Filed 10/25/11 for the Period Ending 09/01/11 Address 8000 S FEDERAL WAY PO BOX 6 BOISE, ID 83716-9632 Telephone 2083684000 CIK 0000723125 Symbol MU SIC Code 3674 - Semiconductors and Related Devices Industry Semiconductors Sector Technology Fiscal Year 08/30 http://www.edgar-online.com © Copyright 2011, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended September 1, 2011 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 1-10658 Micron Technology, Inc. (Exact name of registrant as specified in its charter) Delaware 75-1618004 (State or other jurisdiction of incorporation or organization) (IRS Employer Identification No.) 8000 S. Federal Way, Boise, Idaho 83716-9632 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code (208) 368-4000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, par value $.10 per share NASDAQ Global Select Market Securities registered pursuant to Section 12(g) of the Act: None (Title of Class) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Intel® 80331 I/O Processor Design Guide Contents

Intel® 80331 I/O Processor Design Guide March 2005 Order Number:273823-003 Intel® 80331 I/O Processor Design Guide Contents INFORMATION IN THIS DOCUMENT IS PROVIDED IN CONNECTION WITH INTEL® PRODUCTS. NO LICENSE, EXPRESS OR IMPLIED, BY ESTOPPEL OR OTHERWISE, TO ANY INTELLECTUAL PROPERTY RIGHTS IS GRANTED BY THIS DOCUMENT. EXCEPT AS PROVIDED IN INTEL'S TERMS AND CONDITIONS OF SALE FOR SUCH PRODUCTS, INTEL ASSUMES NO LIABILITY WHATSOEVER, AND INTEL DISCLAIMS ANY EXPRESS OR IMPLIED WARRANTY, RELATING TO SALE AND/OR USE OF INTEL PRODUCTS INCLUDING LIABILITY OR WARRANTIES RELATING TO FITNESS FOR A PARTICULAR PURPOSE, MERCHANTABILITY, OR INFRINGEMENT OF ANY PATENT, COPYRIGHT OR OTHER INTELLECTUAL PROPERTY RIGHT. Intel products are not intended for use in medical, life saving, life sustaining applications. Intel may make changes to specifications and product descriptions at any time, without notice. Contact your local Intel sales office or your distributor to obtain the latest specifications and before placing your product order. Copies of documents which have an order number and are referenced in this document, or other Intel literature, may be obtained by calling1-800-548- 4725, or by visiting Intel's website at http://www.intel.com. AlertVIEW, AnyPoint, AppChoice, BoardWatch, BunnyPeople, CablePort, Celeron, Chips, CT Connect, CT Media, Dialogic, DM3, EtherExpress, ETOX, FlashFile, i386, i486, i960, iCOMP, InstantIP, Intel, Intel logo, Intel386, Intel486, Intel740, IntelDX2, IntelDX4, IntelSX2, Intel Create & Share, Intel GigaBlade, Intel -

Micron Technology Inc

MICRON TECHNOLOGY INC FORM 10-K (Annual Report) Filed 10/26/10 for the Period Ending 09/02/10 Address 8000 S FEDERAL WAY PO BOX 6 BOISE, ID 83716-9632 Telephone 2083684000 CIK 0000723125 Symbol MU SIC Code 3674 - Semiconductors and Related Devices Industry Semiconductors Sector Technology Fiscal Year 03/10 http://www.edgar-online.com © Copyright 2010, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended September 2, 2010 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 1-10658 Micron Technology, Inc. (Exact name of registrant as specified in its charter) Delaware 75 -1618004 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 8000 S. Federal Way, Boise, Idaho 83716 -9632 (Address of principal executive offices) (Zip Code) Registrant ’s telephone number, including area code (208) 368 -4000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, par value $.10 per share NASDAQ Global Select Market Securities registered pursuant to Section 12(g) of the Act: None (Title of Class) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Normal File for Office 2009 & 2010

Intel Corporation, incorporated in 1968, designs and manufactures integrated digital technology platforms. A platform consists of a microprocessor and chipset. The Company sells these platforms primarily to original equipment manufacturers (OEMs), original design manufacturers (ODMs), and industrial and communications equipment manufacturers in the computing and communications industries. The Company’s platforms are used in a range of applications, such as personal computers (PCs) (including Ultrabook systems), data centers, tablets, smartphones, automobiles, automated factory systems and medical devices. The Company also develops and sells software and services primarily focused on security and technology integration. In February 2013, it acquired ProFUSION-Comercio e Prestacao de Servicos em Tecnologia da Informacao Ltda. In May 2013, Intel Corp acquired Aepona Ltd. Effective July 16, 2013, Intel Corp acquired Omek Interactive Ltd. Effective August 15, 2013, Intel Corp acquired Fujitsu Semiconductor Wireless Products Inc, from Fujitsu Semiconductor Ltd, a wholly owned subsidiary of Fujitsu Ltd. In February 2014, M/A-COM Technology Solutions Holdings Inc announced that its subsidiary Mindspeed Technologies Inc completed the sale of assets of its wireless infrastructure business unit to Intel Corporation. On January 31, 2011, the Company acquired Wireless Solutions (WLS) business of Infineon Technologies AG. On February 28, 2011, the Company acquired McAfee, Inc. In August 2011, the Company formed a wholly owned subsidiary, Intel Federal LLC. During the year ended December 31, 2011, it sold the remaining interest in Micron. On February 2012, QLogic Corp. sold the product lines and certain assets associated with its InfiniBand business to the Company. In May 2012, Cray Inc. completed the sale of its interconnect hardware development program and related intellectual property to the Company. -

Linux Hardware Compatibility HOWTO

Linux Hardware Compatibility HOWTO Steven Pritchard Southern Illinois Linux Users Group / K&S Pritchard Enterprises, Inc. <[email protected]> 3.2.4 Copyright © 2001−2007 Steven Pritchard Copyright © 1997−1999 Patrick Reijnen 2007−05−22 This document attempts to list most of the hardware known to be either supported or unsupported under Linux. Copyright This HOWTO is free documentation; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free software Foundation; either version 2 of the license, or (at your option) any later version. Linux Hardware Compatibility HOWTO Table of Contents 1. Introduction.....................................................................................................................................................1 1.1. Notes on binary−only drivers...........................................................................................................1 1.2. Notes on proprietary drivers.............................................................................................................1 1.3. System architectures.........................................................................................................................1 1.4. Related sources of information.........................................................................................................2 1.5. Known problems with this document...............................................................................................2 1.6. New versions of this document.........................................................................................................2 -

2012 Intel Annual Report

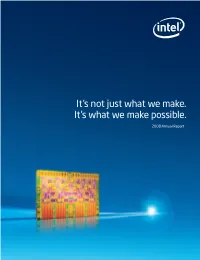

Financial Results “ We made tremendous progress across the business in 2012 as we entered the market for smartphones and tablets, worked with our partners to reinvent the PC, and drove continued innovation and growth in the data ® center. Our strong product pipeline has us well-positioned to bring a new wave of Intel innovations across the spectrum of computing.” Paul S. Otellini, President and Chief Executive Officer Net Revenue Diluted Earnings Per Share Dividends Per Share Paid Dollars in billions Dollars Dollars 60 2.50 1.00 2.39 54.0 53.3 0.87 50 2.13 2.00 2.01 0.80 0.78 43.6 40 38.8 38.3 37.6 0.63 35.4 35.1 1.50 0.60 34.2 0.55 0.56 30 30.1 1.00 0.92 0.40 20 0.77 10 0.50 0.20 ™ 03 04 05 06 07 08 09 10 11 12 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 www.intel.com News and information about Intel® products and technologies, customer Capital Additions to Property, Cash from Operations Plant and Equipment Research and Development support, careers, worldwide locations, Dollars in billions Dollars in billions Dollars in billions and more. 25 12.0 12.0 10.8 11.0 21.0 10.1 20 18.9 9.0 9.0 8.4 16.7 15 6.6 6.0 6.0 5.7 5.7 10.9 11.2 5.2 5.2 10 4.5 3.0 3.0 5 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 www.intc.com Stock information, earnings and conference webcasts, annual reports, and corporate governance and Past performance does not guarantee future results. -

2014 Annual Report Letter from Your CEO

2014 Annual Report Letter From Your CEO For 2014, Intel reported record revenue of $55.9 billion, up 6% from 2013. Net income rose 22% to $11.7 billion, and earnings per share were $2.31. Our operating income of $15.3 billion was up 25% over 2013. We achieved record annual unit shipments for PCs, servers, tablets, phones, and the Internet of Things. Our strategy for growth is playing out well. We are driving our core businesses in personal computing and the enterprise, building on those assets to move into new areas such as the Internet of Things and wearables, strengthening Intel’s position in mobile, and continuing our relentless pursuit of Moore’s Law. The diversity and scale of Intel products today put us in a unique position to compete across the breadth of devices that compute and connect. Growing our core businesses In PC clients, revenue of $34.7 billion was up 4% over 2013. Operating income of $14.6 billion was up 25%. We introduced the Intel® Core™ M processor family, designed to enable superior compute and graphics performance and long battery life in razor-thin, fanless mobile devices. In Chromebooks*, Intel now leads in market segment share. In data center products, revenue was $14.4 billion, up 18% over 2013, and operating income increased 31% as we capitalized on the growth of cloud computing and big data. We introduced next-generation Intel® Xeon® processors that enhance performance, efficiency, and security for compute, storage, and network workloads in cloud environments. Our core businesses are also providing valuable intellectual property to help us compete in diverse computing markets. -

Fabless: the Transformation of the Semiconductor Industry

DANIEL NENNI PAUL MCLELLAN FABLESS: THE TRANSFORMATION OF THE SEMICONDUCTOR INDUSTRY Foreword by Dr. Cliff Hou, VP of R&D, TSMC A SEMIWIKI.COM PROJECT FABLESS: The Transformation of The Semiconductor Industry DANIEL NENNI PAUL MCLELLAN WITH FOREWORD BY CLIFF HOU, VP OF R&D, TSMC A SEMIWIKI.COM PROJECT Fabless: The Transformation of the Semiconductor Industry Copyright 2013 by SemiWiki.com LLC. All rights reserved. Printed in the United States of America. Except as permitted under the United States Copyright Act of 1976, no part of this publication may be reproduced or distributed in any form or by any means, or stored in a data base or retrieval system without the prior written consent of the publisher. Authors: Daniel Nenni and Paul McLellan Editors: Beth Martin and Shushana Nenni ISBN: 978-1-4675-9307-6 BISAC: Business & Economics / General Fabless: The Transformation of the Semiconductor Industry Table of Contents Foreword .................................................................................................. iv Preface ......................................................................................................vi Chapter 1: The Semiconductor Century ............................................10 Chapter 2: The ASIC Business ............................................................21 In Their Own Words: VLSI Technology ......................................29 In Their Own Words: eSilicon Corporation .................................36 Chapter 3: The FPGA ..........................................................................44 -

View Annual Report

Financial Results “Our fundamental business strategies are more focused than ever. Intel has weathered difÀ cult times in the past, and we know what needs to be done to drive our success moving forward. Our new technologies and products will help us ignite market growth and thrive when the economy recovers.” Paul S. Otellini, President and Chief Executive OfÀ cer It’s not just what we make. Net Revenue Diluted Earnings Per Share Geographic Breakdown of Revenue It’s what we make possible. Dollars in billions Dollars Percent 40 38.8 1. 60 100 38.3 37.6 7% 9% 2008 Annual Report 35.4 1.40 10% Japan 33.7 34.2 80 30 30.1 1. 20 1.18 28% 23% 19% 29.4 1.16 Europe 26.5 26.8 0.92 60 20% Americas 0.86 20 0.80 28% 40 45% 10 0.40 51% $VLD3DFLÀF 20 40% 20% 010099 02 080706050403 2004 2005 2006 2007 2008 1998 2003 2008 Capital Additions to Property, Dividends Per Share Paid Plant and Equipment Research and Development** Dollars Dollars in billions Dollars in billions 0.60 6.0 5.9 5.9 6.0 5.9 5.8 5.7 0.55 5.2 5.0 5.1 4.8 0.45 0.45 4.5 4.5 0.40 3.8 0.32 0.30 3.0 3.0 0.15 0.16 1. 5 1. 5 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 **Excluding purchased in-process research and development For news and information about Intel® products For stock information, earnings and conference and technologies, customer support, careers, webcasts, annual reports, and corporate gover- worldwide locations, and more, visit nance and historical À nancial information, visit Financial results for 2006 and thereafter include the effects of share-based compensation. -

2013 Annual Report Letter from Your CEO

2013 Annual Report Letter From Your CEO I am very excited to be Intel’s sixth CEO. In my first letter to you, I would like to share how we are building on Intel’s strengths to accelerate innovation and drive growth. But first, let’s look at the results for fiscal year 2013. Intel delivered revenue of $52.7 billion, net income of $9.6 billion, and earnings per share of $1.89. Client computing products generated $33 billion in revenue and approximately $12 billion in operating profits. Our datacenter business revenue grew to more than $11 billion, driven by rising demand for cloud services, high- performance computing, storage, and networking. We generated almost $21 billion in cash from operations and returned $6.6 billion to our stockholders in the form of dividends and share repurchases. These are solid results in a time of rapid industry transformation, but we must do better. We are refocusing our efforts to reignite growth by driving Intel innovation to market faster. Leading in the pursuit of Moore’s Law The relentless pursuit of Moore’s Law is Intel’s foundation and continues to be our driving force. We lead the industry as the only semiconductor manufacturer in the world offering Tri-gate transistors and 22-nanometer (nm) technology-based products. The benefits of Moore’s Law can be seen across our product lines in the form of higher performance, lower energy requirements, and lower cost per transistor. In 2013, we introduced our 4th generation Intel® Core™ processors, which deliver the largest generation-over-generation gain in battery life in Intel’s history, and a new family of low-power Intel® Atom™ processor-based System-on-Chips (SoCs) designed for high-performance mobile devices. -

Amazing Things Happen with Intel Inside®

Amazing things happen ® with Intel Inside. 2010 Annual Report Financial Results Net Revenue Diluted Earnings Per Share Geographic Breakdown of Revenue Dollars in billions Dollars Percent 50 2.00 2.01 100 9% 10% 10% Japan 43.6 40 80 13 % Europe 38.8 38.3 37.6 1. 50 24% 21% 34.2 35.4 35.1 20% Americas 30 30.1 1.18 60 26.8 19 % 26.5 1. 0 0 0.92 0.86 41% 20 0.77 40 0.50 57% \ 10 20 50% 26% 01 02 09080706050403 10 2006 2007 2008 2009 2010 2000 2005 2010 Capital Additions to Property, Dividends Per Share Paid Plant and Equipment Research and Development Dollars Dollars in billions Dollars in billions 0.80 6.0 5.9 8.0 5.2 5.2 5.0 6.6 0.63 0.60 4.5 4.5 6.0 5.9 5.8 0.55 0.56 5.7 5.7 0.45 0.40 0.40 3.0 4.0 0.20 1. 5 2.0 2006 2007 2008 2009 2010 20062007 2008 2009 2010 20062007 2008 2009 2010 On the cover: (Q generation Intel® Core™ processor family features P! built-in graphics that and gross margin were all the highest in Intel’s history. Growth opportunities, our enable a richer, higher performance computing strong product lineup, and our industry lead in manufacturing process technology '\ !\Q managing power use for longer battery life. #$#%&'\ Past performance does not guarantee future results. This Annual Report to Stockholders contains forward-looking statements, and actual results could differ materially.