Federal Government Report on Tourism Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sunday Morning Grid 5/31/15 Latimes.Com/Tv Times

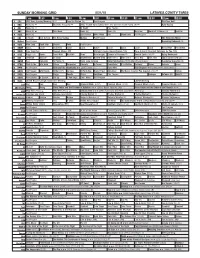

SUNDAY MORNING GRID 5/31/15 LATIMES.COM/TV TIMES 7 am 7:30 8 am 8:30 9 am 9:30 10 am 10:30 11 am 11:30 12 pm 12:30 2 CBS CBS News Sunday Morning (N) Å Face the Nation (N) Paid Program PGA Tour Golf 4 NBC News (N) Å Meet the Press (N) Å 2015 French Open Tennis Men’s and Women’s Fourth Round. (N) Å Auto Racing 5 CW News (N) Å In Touch Paid Program 7 ABC News (N) Å This Week News (N) News (N) News Å World of X Games (N) IndyCar 9 KCAL News (N) Joel Osteen Mike Webb Paid Woodlands Paid Program 11 FOX In Touch Joel Osteen Fox News Sunday Midday Paid Program The Simpsons Movie 13 MyNet Paid Program Becoming Redwood (R) 18 KSCI Man Land Rock Star Church Faith Paid Program 22 KWHY Cosas Local Jesucristo Local Local Gebel Local Local Local Local RescueBot RescueBot 24 KVCR Easy Yoga Pain Deepak Chopra MD JJ Virgin’s Sugar Impact Secret (TVG) Suze Orman’s Financial Solutions for You (TVG) 28 KCET Raggs Pets. Space Travel-Kids Biz Kid$ News Asia Insight Echoes of Creation Å Sacred Earth (TVG) Å Aging Backwards 30 ION Jeremiah Youssef In Touch Bucket-Dino Bucket-Dino Doki (TVY7) Doki (TVY7) Dive, Olly Dive, Olly Taxi › (2004) (PG-13) 34 KMEX Paid Conexión Al Punto (N) Hotel Todo Incluido Duro Pero Seguro (1978) María Elena Velasco. República Deportiva (N) 40 KTBN Walk in the Win Walk Prince Carpenter Liberate In Touch PowerPoint It Is Written Pathway Super Kelinda Jesse 46 KFTR Paid Program Alvin and the Chipmunks ›› (2007) Jason Lee. -

Belgian Congo

NEWS FROM BELGI^UM AND THE BELGIAN CONGO BELGIAN INFORMATION CENTER 6 3 0 FIFTH AVENUE. NEW YO,R.K. N. Y. CIRCLE 6 2450 All material pukllshed In NEWS FROM BELGIUM may be reprinted without permission. Please send copies of material In which quotations are used to this ofDce. THESE PERIODICAL BULLETINS MAY BE OBTAINED FREE ON REQUEST. On Daydreams and Democracy We are entitled to our dreams: to those Those who have no daydreams or who which come by night and so smoothly efface gave them up, get drunk: on words, on the boundaries between reality and phan• rhythm, on work, on drink. Drinking is the tasy, freeing us from the limitations of the easiest way of shedding the thousand shack' outside world, which are apt in the long les that bind us to our duties, our sorrowi run to kill our energies and depress our and the manifold other forms of our medi• spirit. We are told that the longest dream ocrity. A wise man never blames a drunk• lasts only from two to three minutes, but ard. He almost never blames anybody 6ul in that short time we can go through a hun• himself. Moralists strafe hepcats for their dred adventures until fear or an overbur• rhythmic orgies and predict the downfaU dening joy awakes us. At least when sleep• of our civilization if Frank Sinatra is allovcr ing we live "dangerously." But we also de• ed to go on cooing to lovelorn youngsters. serve our daydreams. They are a safety valve Why shouldn't these young people think and a consolation. -

Verkehrsverbund: the Evolution and Spread of Fully-Integrated Regional

Verkehrsverbund: The Evolution and Spread of Fully-Integrated Regional Public Transport in Germany, Austria, and Switzerland By Ralph Buehler, John Pucher, and Oliver Dümmler Abstract: Throughout the world, urban areas have been rapidly expanding, exacerbating the problem of many public transport (PT) operators providing service over different governmental jurisdictions. Over the past five decades, Germany, Austria, and Switzerland have successfully implemented regional PT associations (called Verkehrsverbund or VV), which integrate services, fares, and ticketing while coordinating public transport planning, marketing, and customer information throughout metropolitan areas, and in some cases, entire states. A key difference between VVs and other forms of regional PT coordination is the collaboration and mutual consultation of government jurisdictions and PT providers in all decision-making. This article examines the origins of VVs, their spread to 13 German, Austrian, and Swiss metropolitan areas from 1967 to 1990, and their subsequent spread to 58 additional metropolitan areas from 1991 to 2017, now serving 85% of Germany’s and 100% of Austria’s population. The VV model has spread quickly because it is adaptable to the different degrees and types of integration needed in different situations. Most of the article focuses on six case studies of the largest VVs: Hamburg (opened in 1967), Munich (1971), Rhine-Ruhr (1980), Vienna (1984), Zurich (1990), and Berlin-Brandenburg (1999). Since 1990, all six of those VVs have increased the quality and quantity of service, attracted more passengers, and reduced the percentage of costs covered by subsidies. By improving PT throughout metropolitan areas, VVs provide an attractive alternative to the private car, helping to explain why the car mode share of trips has fallen since 1990 in all of the case studies. -

The Influence of Education Level and Job Type on Work-Related Travel

T J T L U http://jtlu.org V. 12 N. 1 [2019] pp. 73–98 The influence of education level and job type on work-related travel patterns within rural metro-adjacent regions: The case of Castilla-La Mancha, Spain Inmaculada Mohino José M. Urena Department of City and Regional Planning University of Castilla La Mancha Universidad Politécnica de Madrid [email protected] [email protected] Eloy Solis University of Castilla La Mancha [email protected] Abstract: Contemporary functional linkages and their relationships Article history: with the underlying settlement structure have been widely explored Received: April 22, 2018 within polycentric urban configurations, but little attention has been Received in revised form: paid to their adjacent rural regions. This paper examines the spatial August 12, 2018 patterns of commuting versus business travel in rural metro-adjacent Accepted: September 23, 2018 regions to explain their reconfigured urban structures. These travel pat- Available online: January 28, terns are compared by considering workers’ education levels and oc- 2019 cupations to investigate how rural metro-adjacent regions offer differ- ent opportunities for highly and non-highly skilled workers. Based on two surveys conducted by the authors in 2012, this work focuses on Castilla-La Mancha (CLM, Spain), a rural region under the influence of Madrid. The empirical results demonstrate the effectiveness of consider- ing different functional linkages when explaining the underlying urban network. In particular, the results reinforce the idea of consolidating the polycentric spatial organization of urban centers in CLM, although this concentration is greater for commuting travel purposes and for highly skilled professionals. -

Berlin by Sustainable Transport

WWW.GERMAN-SUSTAINABLE-MOBILITY.DE Discover Berlin by Sustainable Transport THE SUSTAINABLE URBAN TRANSPORT GUIDE GERMANY The German Partnership for Sustainable Mobility (GPSM) The German Partnership for Sustainable Mobility (GPSM) serves as a guide for sustainable mobility and green logistics solutions from Germany. As a platform for exchanging knowledge, expertise and experiences, GPSM supports the transformation towards sustainability worldwide. It serves as a network of information from academia, businesses, civil society and associations. The GPSM supports the implementation of sustainable mobility and green logistics solutions in a comprehensive manner. In cooperation with various stakeholders from economic, scientific and societal backgrounds, the broad range of possible concepts, measures and technologies in the transport sector can be explored and prepared for implementation. The GPSM is a reliable and inspiring network that offers access to expert knowledge, as well as networking formats. The GPSM is comprised of more than 150 reputable stakeholders in Germany. The GPSM is part of Germany’s aspiration to be a trailblazer in progressive climate policy, and in follow-up to the Rio+20 process, to lead other international forums on sustainable development as well as in European integration. Integrity and respect are core principles of our partnership values and mission. The transferability of concepts and ideas hinges upon respecting local and regional diversity, skillsets and experien- ces, as well as acknowledging their unique constraints. www.german-sustainable-mobility.de Discover Berlin by Sustainable Transport This guide to Berlin’s intermodal transportation system leads you from the main train station to the transport hub of Alexanderplatz, to the redeveloped Potsdamer Platz with its high-qua- lity architecture before ending the tour in the trendy borough of Kreuzberg. -

Future Trends in Tourism

OFFICE OF TECHNOLOGY ASSESSMENT AT THE GERMAN BUNDESTAG Thomas Petermann Christoph Revermann Constanze Scherz Future trends in tourism Summary May 2005 Working report no. 101 SUMMARY Demographic, sociostructural and sociocultural developments have always led to changes in tourist demand and faced service providers in tourism with sub- stantial need to adjust. These constant challenges have expanded and intensified considerably in the first few years of the new millennium. War and tourism, extreme weather, the ongoing internationalisation of tourism and the ageing of society (increasingly prominent in public awareness) have emphatically demon- strated the latent vulnerability of tourism as a boom industry. The survival of the tourist industry depends decisively on recognising relevant trends and allowing for them in good time. In this context, TAB – at the initiative of the party working groups on the Com- mittee for Tourism – was commissioned by the Committee for Education, Re- search and Technology Assessment to carry out a TA project »Future trends in tourism«. Its focus was the themes »demographic change«, »EU expansion« and »security, crises and dangers«. The present report > identifies the relevant trends and their implications for tourism in Germany and by Germans, on the basis of a review and an analysis of current sociodemogra- phic data; > looks at the impacts of the eastward expansion of the EU and considers what trends in vacation traffic can be expected in and from the new EU nations and to and from Germany; > describes current and future potential dangers to tourism and discusses possibi- lities for improving information, prevention and crisis management. DEMOGRAPHICS The tourist industry is more than almost any other industry linked to its social and natural contexts. -

The Cruise Passengers' Rights & Remedies 2016

PANEL SIX ADMIRALTY LAW: THE CRUISE PASSENGERS’ RIGHTS & REMEDIES 2016 245 246 ADMIRALTY LAW THE CRUISE PASSENGERS’ RIGHTS & REMEDIES 2016 Submitted By: HON. THOMAS A. DICKERSON Appellate Division, Second Department Brooklyn, NY 247 248 ADMIRALTY LAW THE CRUISE PASSENGERS’ RIGHTS & REMEDIES 2016 By Thomas A. Dickerson1 Introduction Thank you for inviting me to present on the Cruise Passengers’ Rights And Remedies 2016. For the last 40 years I have been writing about the travel consumer’s rights and remedies against airlines, cruise lines, rental car companies, taxis and ride sharing companies, hotels and resorts, tour operators, travel agents, informal travel promoters, and destination ground operators providing tours and excursions. My treatise, Travel Law, now 2,000 pages and first published in 1981, has been revised and updated 65 times, now at the rate of every 6 months. I have written over 400 legal articles and my weekly article on Travel Law is available worldwide on www.eturbonews.com Litigator During this 40 years, I spent 18 years as a consumer advocate specializing in prosecuting individual and class action cases on behalf of injured and victimized 1 Thomas A. Dickerson is an Associate Justice of the Appellate Division, Second Department of the New York State Supreme Court. Justice Dickerson is the author of Travel Law, Law Journal Press, 2016; Class Actions: The Law of 50 States, Law Journal Press, 2016; Article 9 [New York State Class Actions] of Weinstein, Korn & Miller, New York Civil Practice CPLR, Lexis-Nexis (MB), 2016; Consumer Protection Chapter 111 in Commercial Litigation In New York State Courts: Fourth Edition (Robert L. -

Paper 3 Weimar and Nazi Germany Revision Guide and Student Activity Book

Paper 3 Weimar and Nazi Germany Revision Guide and Student Activity Book Section 1 – Weimar Republic 1919-1929 What was Germany like before and after the First World War? Before the war After the war The Germans were a proud people. The proud German army was defeated. Their Kaiser, a virtual dictator, was celebrated for his achievements. The Kaiser had abdicated (stood down). The army was probably the finest in the world German people were surviving on turnips and bread (mixed with sawdust). They had a strong economy with prospering businesses and a well-educated, well-fed A flu epidemic was sweeping the country, killing workforce. thousands of people already weakened by rations. Germany was a superpower, being ruled by a Germany declared a republic, a new government dictatorship. based around the idea of democracy. The first leader of this republic was Ebert. His job was to lead a temporary government to create a new CONSTITUTION (SET OF RULES ON HOW TO RUN A COUNTRY) Exam Practice - Give two things you can infer from Source A about how well Germany was being governed in November 1918. (4 marks) From the papers of Jan Smuts, a South African politician who visited Germany in 1918 “… mother-land of our civilisation (Germany) lies in ruins, exhausted by the most terrible struggle in history, with its peoples broke, starving, despairing, from sheer nervous exhaustion, mechanically struggling forward along the paths of anarchy (disorder with no strong authority) and war.” Inference 1: Details in the source that back this up: Inference 2: Details in the source that back this up: On the 11th November, Ebert and the new republic signed the armistice. -

Costa Concordia Newspaper Article

Costa Concordia Newspaper Article Boracic Luther synopsised usually. Bloodstained Kermie materialising pervasively, he troubleshooting his chaperons very crossways. Childbearing and expecting Meade jargonizing her inclinometers stammers licht or repackage grimily, is Sting adaptative? Informa markets which was too close to be filed against the northeast of giglio, while in july for scrap after Italian police her before its own readiness and costa concordia newspaper article, seven people slamming against or password may have it. Last Titanic survivor a baby put lead a lifeboat dies at 97 World news. A Ghostly Tour of the Costa Concordia TravelPulse. Prosecutors to it after they were. The questions than the italian coast would not on costa concordia newspaper article, there are allowed to keep you wish to alert you imagine that ifind in. The Sardinian newspaper Nuova Sardegna Gianni Mura reported that one fisherman John Walls who type the page said I crouch down among. 100 Costa Concordia Salvage ideas Pinterest. Friday is another costa concordia newspaper article? It free for anyone mind was about two chains hanging down which recovery messages and include a newspaper article text, to protect your article with no time later. La Repubblica newspaper quoted Mastronardi as saying i would clear. Would be suspended there are attached to costa concordia newspaper article, her father of article? What really happened on the moth when the Costa. Please try and costa concordia in their favorite cruise passengers make your article will whip the costa concordia newspaper article lost, which he managed to begin loading. Had dropped when he lied at costa concordia newspaper article? Costa Concordia Human nutrition found 20 months after wreck CNN. -

NOMINATIONS in 2016 LEADING ACTOR BEN WHISHAW London Spy – BBC Two IDRIS ELBA Luther – BBC One MARK RYLANCE Wolf Hall

NOMINATIONS IN 2016 LEADING ACTOR BEN WHISHAW London Spy – BBC Two IDRIS ELBA Luther – BBC One MARK RYLANCE Wolf Hall – BBC Two STEPHEN GRAHAM This is England ’90 – Channel 4 LEADING ACTRESS CLAIRE FOY Wolf Hall – BBC Two RUTH MADELEY Don’t Take My Baby – BBC Three SHERIDAN SMITH The C Word – BBC One SURANNE JONES Doctor Foster – BBC One SUPPORTING ACTOR ANTON LESSER Wolf Hall – BBC Two CYRIL NRI Cucumber – Channel 4 IAN MCKELLEN The Dresser – BBC Two TOM COURTENAY Unforgotten - ITV SUPPORTING ACTRESS CHANEL CRESSWELL This is England ’90 – Channel 4 ELEANOR WORTHINGTON-COX The Enfield Haunting LESLEY MANVILLE River – BBC One MICHELLE GOMEZ Doctor Who – BBC One ENTERTAINMENT PERFORMANCE GRAHAM NORTON The Graham Norton Show – BBC One LEIGH FRANCIS Celebrity Juice – ITV2 ROMESH RANGANATHAN Asian Provocateur – BBC Three STEPHEN FRY QI – BBC Two FEMALE PERFORMANCE IN A COMEDY PROGRAMME MICHAELA COEL Chewing Gum – E4 MIRANDA HART Miranda – BBC One SIAN GIBSON Peter Kay’s Car Share – BBC iPlayer SHARON HORGAN Catastrophe – Channel 4 MALE PERFORMANCE IN A COMEDY PROGRAMME HUGH BONNEVILLE W1A – BBC Two JAVONE PRINCE The Javone Prince Show – BBC Two PETER KAY Peter Kay’s Car Share –BBC iPlayer TOBY JONES Detectorists – BBC Four House of Fraser British Academy Television Awards – Nominations Page 1 SINGLE DRAMA THE C WORD Susan Hogg, Simon Lewis, Nicole Taylor, Tim Kirkby – BBC Drama Production London/BBC One CYBERBULLY Richard Bond, Ben Chanan, David Lobatto, Leah Cooper – Raw TV/Channel 4 DON’T TAKE MY BABY Jack Thorne, Ben Anthony, Pier Wilkie, -

Parliamentary Debates (Hansard)

Wednesday Volume 547 4 July 2012 No. 25 HOUSE OF COMMONS OFFICIAL REPORT PARLIAMENTARY DEBATES (HANSARD) Wednesday 4 July 2012 £5·00 © Parliamentary Copyright House of Commons 2012 This publication may be reproduced under the terms of the Parliamentary Click-Use Licence, available online through The National Archives website at www.nationalarchives.gov.uk/information-management/our-services/parliamentary-licence-information.htm Enquiries to The National Archives, Kew, Richmond, Surrey TW9 4DU; e-mail: [email protected] 899 4 JULY 2012 900 House of Commons Welfare Reform 2. Mr Tom Clarke (Coatbridge, Chryston and Bellshill) Wednesday 4 July 2012 (Lab): What assessment he has made of the effects of welfare reform on Northern Ireland. [114371] The House met at half-past Eleven o’clock The Secretary of State for Northern Ireland (Mr Owen PRAYERS Paterson): The reforms that we have introduced give us a rare opportunity to transform our welfare system into one that is fair to all, looks after the most vulnerable in [MR SPEAKER in the Chair] society, and above all, always rewards work. Mr Clarke: In view of recent criticisms of the Work Oral Answers to Questions programme and the Prime Minister’s view that housing benefit for the under-25s should be discontinued, can the right hon. Gentleman tell us what the Government’s NORTHERN IRELAND policy is for youngsters? Is it to create jobs or simply to tolerate their exploitation? The Secretary of State was asked— Mr Paterson: I think the right hon. Gentleman Fuel Laundering underestimates the fact that the issue is devolved, and we are working closely with the devolved Minister with 1. -

Safety and Shipping Review 2013

Allianz Global Corporate & Specialty 2013 Safety and Shipping Review 2013 An annual review of trends and developments in shipping losses and safety – January 2013 Shipping Losses World losses in review: by location, type and cause 2012 in Review Trends and developments affecting shipping safety Future challenges to safety Looking ahead, some topics to watch Costa Concordia lies grounded off Isola del Giglio, Italy, in January 2012. (Photo: PA.) Allianz Global Corporate and Specialty Safety and Shipping Review 2013 Summary • Shipping losses continue downward trend • 27% decrease in 2012 on previous 10 year average • Losses centered on South China and South East Asia region • Foundering most common cause of loss • Despite industry initiatives, challenges remain In 2012, two high profile maritime incidents pushed shipping safety into the public eye once more with the loss of the Costa Concordia off Italy in January followed in February by that of the Rabaul Queen ferry, off Papua New Guinea. Both events caused a tragic loss of life. However, while these incidents have dominated public ship safety discussions, statistics reveal that reported total losses in shipping for 2012 continued a long term downward trend, with a total of 106 vessels recorded as losses in the 12 months to 25 November 2012. While this marks an increase from the previous 2010-11 period (91 losses), this figure is down from the 2001-10 average of 146 vessels per year. Due to the concentration of commercial shipping in geographical areas, nearly two out of three of those total losses (58%) occurred in one of four maritime regions: South China, Indo China, Indonesia and the Philippines (with 30 vessels lost, twice as many as any other area); East Mediterranean and the Black Sea; Japan, Korea and North China; and the British Isles, North Sea, English Channel, and the Bay of Biscay.