Investment Strategy on the Zagreb Stock Exchange Based on Dynamic DEA Croatian Economic Survey : Vol

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FIMA Daily Insight

FIMA Daily Insight IN FOCUS - ZAGREB STOCK EXCHANGE January 8, 2013 Stocks on ZSE traded higher today. CROBEX increased 0.24% to ZSE STOCK MARKET 1,808.40 pts while blue chip CROBEX10 gained 0.21% to 1,010.86 pts. CROBEX Last 1.808,4 Regular stock turnover amounted to HRK 14.4 million. % daily 0,24% Integrated telecom HT (HTRA CZ) topped the liquidity board collecting % YTD 3,91% HRK 4.3 million in turnover. The price increased 0.9% to HRK 210.70. CROBEX10 last 1010,9 Fertilizers producer Petrokemija (PTKMRA CZ) also came to focus again % daily 0,21% with HRK 1.5 million in turnover while price gained 5.5% to HRK 240.0. % YTD 4,05% Petrokemija was in investors’ focus few months ago, after speculations on Government selling its share of 1.7 million shares (50.6% of capital). Stock Turnov er (HRK m) 14,37 A few days ago Mladen Pejnović, head of the State Office for State Total MCAP (HRK bn) 194,39 Property Management confirmed government’s plans to privatize Source: w w w .zse.hr Petrokemija. Auto-parts producer AD Plastik (ADPLRA CZ) came to focus trading in -4,0% -2,0% 0,0% 2,0% 4,0% 6,0% blocks. The price advanced 1% to HRK 115.99 on HRK 1.3 million in PTKM-R-A ATPL-R-A turnover. AD Plastik currently trades at P/E=7.7, P/S=0.7 and DDJH-R-A P/Bv=0.7. VPIK-R-A LKPC-R-A Tobacco and tourism Adris group preferred share (ADRSPA CZ) was VIRO-R-A KORF-R-A also in investors’ focus with HRK 0.7 million in turnover while price KNZM-R-A slipped 1.3% to HRK 262.20. -

Market Commentary Portfolio Performance Vs Benchmark

Feb. FKHR1 Monthly Fund Update 2016 Market Commentary Following the publication of Q4 results, the share price jumped by 7.06% in one day. Viadukt operated with a net profit of HRK 3.2m in After a tumultuous start of the year, February brought on a reversal 2015, but this is still 36% less profit compared to the previous year. of trends in most of our largest holdings. This is in line with the rest Revenue fell by 9.1%, which is the consequence of an overall of European and global markets, which reached a bottom in mid- reduction in total investment in the Republic of Croatia, from which February, only to recover by the end of the month. The Croatian Viadukt achieves 99% of its total revenue. However, the growth in market started this recovery even sooner, having reached its lowest share price after the announcement of financial results might have point during January. However during February, the benchmark been due to the optimistic expectations for the rest of the year. The CROBEX index stayed mostly at the same level from the start of the construction industry expects a slight recovery and increased month, with only slight fluctuations. In the meantime, our fund investment from contracting authorities. managed to achieve a return of almost 4% MoM, beating the A third position that we want to emphasize is Đuro Đaković Holding market by a large margin. (ĐĐ). After having an amazing January, on the 15th and 19th of The most important contributor was our largest holding, the Adris February it was announced that Đuro Đaković signed contracts with Group, with common stock growing by over 10%. -

Stoxx® All Europe Total Market Index

TOTAL MARKET INDICES 1 STOXX® ALL EUROPE TOTAL MARKET INDEX Stated objective Key facts The STOXX Total Market (TMI) Indices cover 95% of the free-float » With 95% coverage of the free-float market cap of the relevant market cap of the relevant investable stock universe by region or investable stock universe per region, the index forms a unique country. The STOXX Global TMI serves as the basis for all regional benchmark for a truly global investment approach and country TMI indices. All TMI indices offer exposure to global equity markets with the broadest diversification within the STOXX equity universe in terms of regions, currencies and sectors. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX All Europe Total Market Index 13,768.8 10,453.0 7.2 1.7 250.9 0.0 2.4 0.0 3.0 STOXX Global Total Market Index 54,569.6 44,271.7 6.1 1.3 618.0 0.0 1.4 0.0 3.4 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX All Europe Total Market Index 0.3 2.0 18.1 43.3 55.0 3.8 3.0 17.7 12.4 8.9 STOXX Global Total Market Index 2.3 7.7 21.7 49.4 78.4 30.7 11.5 21.2 13.9 11.9 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 STOXX All Europe Total Market Index 11.0 11.2 11.6 19.9 21.1 -1.0 0.3 1.3 0.6 0.4 STOXX Global Total Market Index 8.2 7.9 8.1 12.8 22.5 1.1 1.4 2.3 1.0 0.5 Index to benchmark Correlation Tracking error (%) STOXX All Europe Total Market Index 0.9 0.9 0.9 0.9 0.9 5.8 6.1 6.3 10.0 10.2 Index to benchmark Beta Annualized information ratio STOXX All Europe Total Market Index 1.2 1.2 1.2 1.4 1.3 -3.5 -1.3 -0.6 -0.0 -0.2 1 For information on data calculation, please refer to STOXX calculation reference guide. -

CEE CIS Committee Decision

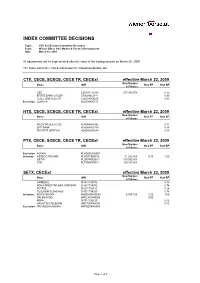

INDEX COMMITTEE DECISIONS Topic: CEE & CIS Index Committee Decisions From: Wiener Börse AG / Market & Product Development Date: March 18, 2009 All adjustments will be implemented after the close of the trading session on March 20, 2009 The Index Committee has decided upon the following adjustments: CTX, CECE, SCECE, CECE TR, CECExt effective March 23, 2009 New Number Name ISIN New FF New RF of Shares CEZ CZ0005112300 537.989.759 0,32 ERSTE BANK GROUP AT0000652011 0,90 TELEFONICA O2 CR CZ0009093209 0,97 Exclusion ZENTIVA NL0000405173 HTX, CECE, SCECE, CECE TR, CECExt effective March 23, 2009 New Number Name ISIN New FF New RF of Shares MAGYAR OLAJ GAZI HU0000068952 0,71 OTP BANK HU0000061726 0,95 RICHTER GEDEON HU0000067624 0,95 PTX, CECE, SCECE, CECE TR, CECExt effective March 23, 2009 New Number Name ISIN New FF New RF of Shares Exclusion AGORA PLAGORA00067 Inclusion ASSECO POLAND PLSOFTB00016 71.292.980 0,75 1,00 GETIN PLGSPR000014 710.930.354 TVN PLTVN0000017 169.159.984 SETX, CECExt effective March 23, 2009 New Number Name ISIN New FF New RF of Shares GORENJE SI0031104076 0,78 NOVA KREDITNA BKA. MARIBOR SI0021104052 0,78 PETROL SI0031102153 0,78 TELEKOM SLOVENIJE SI0031104290 0,78 Inclusion ADRIS GRUPA HRADRSPA0009 6.784.100 1,00 1,00 DALEKOVOD HRDLKVRA0006 0,50 KRKA SI0031102120 0,42 HRVATSKI TELEKOM HRHT00RA0005 0,73 Exclusion PRIVREDNA BANKA HRPBZ0RA0004 Page 1 of 5 NTX effective March 23, 2009 New Number Name ISIN New FF New RF of Shares ANDRITZ AT0000730007 0,99 Exclusion BANCA TRANSILVANIA ROTLVAACNOR1 ERSTE GROUP BANK AT0000652011 0,99 OMV AG AT0000743059 0,99 RAIFFEISEN INTERNATIONAL AT0000606306 0,99 Exclusion CENTRAL EUROP. -

CROBEX® and Crobextr® CROBEX10® and Crobex10tr

September 8th, 2020 CROBEX® and CROBEXtr® ISIN Trading Issuer Free float Number of Weighting code factor listed shares factor 1 HRADPLRA0006 ADPL AD PLASTIK d.d. 70% 4.199.584 1,00000000 2 HRADRSPA0009 ADRS2 ADRIS GRUPA d.d. 95% 6.784.100 0,36528752 3 HRARNTRA0004 ARNT Arena Hospitality Group dd 50% 5.128.721 1,00000000 4 HRATGRRA0003 ATGR ATLANTIC GRUPA d.d. 45% 3.334.300 0,48953990 5 HRATPLRA0008 ATPL ATLANTSKA PLOVIDBA d.d. 85% 1.395.520 1,00000000 6 HRDDJHRA0007 DDJH ĐURO ĐAKOVIC GRUPA d.d. 50% 10.153.230 1,00000000 7 HRDLKVRA0006 DLKV Dalekovod, d.d. 40% 24.719.305 1,00000000 8 HRERNTRA0000 ERNT ERICSSON NIKOLA TESLA d.d. 55% 1.331.650 0,98709462 9 HRHT00RA0005 HT HT d.d. 45% 80.766.229 0,15037086 10 HRIGH0RA0006 IGH INSTITUT IGH d.d. 50% 613.709 1,00000000 11 HRINGRRA0001 INGR INGRA d.d. 95% 13.545.200 1,00000000 12 HRKOEIRA0009 KOEI KONČAR d.d. 100% 2.572.119 0,59493974 13 HRKRASRA0008 KRAS KRAŠ d.d. 12% 1.498.621 1,00000000 14 HROPTERA0001 OPTE OT-OPTIMA TELEKOM d.d. 40% 69.443.264 1,00000000 15 HRPODRRA0004 PODR PODRAVKA d.d. 85% 7.120.003 0,35950401 16 HRRIVPRA0000 RIVP Valamar Riviera d.d. 55% 126.027.542 0,55422898 17 HRSAPNRA0007 SAPN Saponia d.d. 13% 658.564 1,00000000 18 HRTPNGRA0000 TPNG TANKERSKA NEXT GENERATION 50% 8.733.345 1,00000000 19 HRZABARA0009 ZABA Zagrebačka banka d.d. 4% 320.241.955 1,00000000 CROBEX10® and CROBEX10tr® ISIN Trading Issuer Free float Number of Weighting code factor listed shares factor 1 HRADPLRA0006 ADPL AD PLASTIK d.d. -

2019 Transparency Report Deloitte D.O.O. Date Published 30 April 2020 Updated 20 October 2020

2019 Transparency Report Deloitte d.o.o. Date published 30 April 2020 Updated 20 October 2020 00 2019 Transparency Report | Contents Contents Contents 1 Deloitte leadership message 2 Deloitte network 4 What Deloitte Audit & Assurance brings to capital markets 7 External and internal audit quality monitoring 12 Independence, ethics, and additional disclosures 15 Appendices Error! Bookmark not defined. Appendix A | EU EEA audit firms 20 Appendix B | Financial information 22 Appendix C | Public interest entities 23 01 2019 Transparency Report | Deloitte d.o.o. leadership message 1 Deloitte d.o.o. leadership message This report sets out the practices and processes that are currently employed by Deloitte d.o.o., in accordance with the requirements of the Audit Act (Official Gazzete 127/2017) and the European Union’s Regulation 537/2014 on specific requirements regarding statutory audit of public-interest entities. All information provided in this report relates to the situation of Deloitte Croatia on 31 December 2019, except if indicated otherwise. We are witnesses to the conduct of business activities, including the procedures for auditing financial statements and related services at times that are out of the ordinary, but we also remain responsible for meeting our professional obligations to the community, our employees and our clients. As the effects of the coronavirus epidemic become more apparent, Deloitte emphasizes a key responsibility to the capital markets, which is to carry out top quality audits. In today's environment, investors and stakeholders are seeking an impartial opinion on the financial statements of companies more than ever before. The main priority of Deloitte's leadership is the safety and well-being of Deloitte's professionals, as well as the quality of the professional practices performed, which is why major areas of action have been established that are coordinated both globally and locally. -

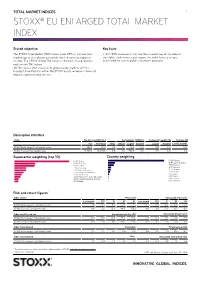

Stoxx® Eu Enlarged Total Market Index

TOTAL MARKET INDICES 1 STOXX® EU ENLARGED TOTAL MARKET INDEX Stated objective Key facts The STOXX Total Market (TMI) Indices cover 95% of the free-float » With 95% coverage of the free-float market cap of the relevant market cap of the relevant investable stock universe by region or investable stock universe per region, the index forms a unique country. The STOXX Global TMI serves as the basis for all regional benchmark for a truly global investment approach and country TMI indices. All TMI indices offer exposure to global equity markets with the broadest diversification within the STOXX equity universe in terms of regions, currencies and sectors. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX EU Enlarged Total Market Index 266.7 121.0 0.6 0.1 10.3 0.0 8.5 0.0 N/A STOXX Europe Total Market Index 12,763.5 10,020.5 9.5 2.6 250.9 0.0 2.5 0.0 3.0 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX EU Enlarged Total Market Index 1.2 -3.4 6.4 0.1 1.7 14.7 -4.9 6.3 0.0 0.3 STOXX Europe Total Market Index 0.4 2.0 18.3 44.5 55.2 4.8 2.9 17.9 12.7 8.9 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 STOXX EU Enlarged Total Market Index 15.1 15.0 16.3 23.2 25.3 -0.1 -0.4 0.4 0.0 -0.0 STOXX Europe Total Market Index 11.0 11.1 11.5 20.0 21.6 -0.9 0.3 1.3 0.6 0.4 Index to benchmark Correlation Tracking error (%) STOXX EU Enlarged Total Market Index 0.7 0.7 0.7 0.8 0.9 10.3 10.7 11.9 12.3 12.7 Index to benchmark Beta Annualized information ratio STOXX EU Enlarged Total Market Index 1.0 0.9 1.0 1.0 1.0 0.8 -0.8 -0.8 -1.0 -0.6 1 For information on data calculation, please refer to STOXX calculation reference guide. -

Market Commentary Portfolio Performance Vs

May 2017 FKHR1 Monthly Fund Update Market Commentary May was the third month in a row in which CROBEX saw a decline ATLN-R-A price has been increasing since it published invitation to of 7% due to the Agrokor crisis and it's heavy impact on Croatian the general assembly that should be on 27 June. In the first economy. The extraordinary manager for Agrokor ensured a loan quarter of 2017 the company has achieved the increase in for liquidity for the concern to continue its operations and now revenues of 1.3%, compared to the same period last year. This the analysts are saying that a few American funds and some increase in revenues was caused by a 3.6% increase in consumer Croatian banks are prepared to give new credit to Agrokor. demand and increased ticket prices for cable cars transportation. Restructuring of the concern will start in fall, and the revenues Expenditures are roughly the same as the last year, but this year is from operating business will be enough to ensure Agrokor's day- marked by increased investment used for modification of cable to - day business. Also, the Vice-Chairman of Sberbank, the bank car transportation. There were few key factors, that were crucial which is the biggest creditor of Agrokor, said that the for positive price movement. Firstly, on the agenda of the General continument of financing will depend on communication and co- Assembly, the suggestion was accepted for increasing share operation with the government and Agrokor itself. In May, capital for about 3.5 million HRK. -

October 2017 FKHR1 Monthly Fund Update

October 2017 FKHR1 Monthly Fund Update Market Commentary While world stock exchanges reached record highs, primarily US Grupa and opened a bankruptcy procedure. After the ZSE decided stock market indexes, which are at the highest levels, the Croatian to remove the stock from its listings on 26th of October, the stock stock exchange index, CROBEX grew by 3.7% and is far from a soared by 68.43%. The stock ended the month trading at the all- significant recovery. US economy grew by 3% in the Q3 while time low since its listing. There is yet to see what is going to Amazon, Microsoft and Alphabet smashed forecasts and sent happen with this civil engineering firm, but the company NASDAQ to new record high. At the same time, the Fed did not announced in its annual report that their revenues fell by 82.3% raise its benchmark interest rate from its current 1% to 1.25% since last year. Also, the company said in a statement that they target, but indicated that one more hike is likely this year. Officials will sue Croatian government and that they will start the arbitrage also projected one rate hike less than initially forecasted between process because of the bridge Čiovo in Croatia. The government now and 2019. The World Bank held its assessment of the growth decided to break the contract with Viadukt d.d. for unknown of the Croatian economy this year at 2.9% and also said that risks reasons and employed an Austrian contractor. to the economy are moderate. The additional risks are posed by a still high level of indebtedness of the private sector, the Agrokor Hrvatski Telekom d.d. -

Agency Problems and Debt Financing

AGENCY PROBLEMS AND DEBT FINANCING Marina Klačmer Čalopa1 Karolina Kokot2 Ivana Đunđek Kokotec3 DOI: https://doi.org/10.31410/EMAN.2019.325 Abstract: The main objective of this paper is to examine correlation between agency costs meas- ured by identified approximation of variables and debt financing as one of the corporate governance mechanisms for reducing these costs. In a modern corporation where ownership is separated from management, many benefits are viewed primarily through an increasing efficiency. The issue of the separation of ownership and management is related to potential conflict between principals (stakehold- ers) and agents (managers). Theoretically possible solution to the agency problem is defined through the agency theory. The most significant problem are agency costs. Agency costs do not have a directly quantifiable value, therefore the approximation of measures such as asset turnover ratio and operat- ing expense ratio (company’s operating expenses divided by its revenues) will be used in this research paper. According to the previous empirical studies, between asset turnover ratio and debt financing positive correlation was determined, while negative correlation was determent between operating ex- pense ratio and debt financing. This research was conducted on Croatian companies whose shares have been listed on the Zagreb Stock Exchange continuously from January 2009 to December 2017. In the analysis, from a total of 154 companies that shares have been listed on the Zagreb Stock Exchange, 31 most actively traded shares measured by the average monthly trading rank in the observed period were taken. Results obtained in this research indicate that debt financing is significant corporate governance mechanism for reducing agency costs where the direction obtained from the correlation is in line with the theoretical expectation. -

Crobexplus© and SECTORAL INDICES

February 11, 2013 NEW ZAGREB STOCK EXCHANGE EQUITY INDICES – CROBEXplus© AND SECTORAL INDICES In accordance to the provisions of the Zagreb Stock Exchange resolution on the CROBEXplus© index and sectoral indices from February 7, 2013 the Index Committee has determined, at the meeting on February 7, 2013, an initial composition of the CROBEXplus© index and sectoral indices based on the trading data from August 1, 2012 to January 31, 2013. CROBEXplus© and sectoral indices are equal weight indices meaning that all constituent shares will have equal weight in the indices. To be included into the CROBEXplus© index share has to be traded at least 70% trading days in the previous six months period with free float market capitalization greater then 10 m HRK. Number of shares in CROBEXplus© index is unlimited. Indices will be calculated in Croatian Kunas (HRK). As of February 22, 2013 Zagreb Stock Exchange starts calculating new equity indices which include CROBEXplus© index and five sectoral indices. CROBEXplus© Symbol Issuer 1 ACI-R-A ACI d. d. 2 ADPL-R-A AD plastik d.d. 3 ADRS-P-A Adris grupa d. d. 4 ARNT-R-A Arenaturist d. d. 5 ATGR-R-A Atlantic grupa d.d. 6 ATPL-R-A Atlantska plovidba d.d. 7 BD62-R-A Badel 1862 d.d. 8 BLJE-R-A Belje d.d. Darda 9 DDJH-R-A Đuro Đaković holding d.d. 10 DIOK-R-A Dioki d.d. 11 DLKV-R-A Dalekovod d.d. 12 ERNT-R-A Ericsson Nikola Tesla d.d. 13 HDEL-R-A Hidroelektra niskogradnja d.d. -

9Th International Fund Management Conference & 25Th Zagreb Stock

9th International Fund Management Conference & 25th Zagreb Stock Exchange Conference - Raising regional attractiveness - October 2015 Volumes traded on ZSE from 2007 were continuously declining Average daily turnover on ZSE in EURm 11,6 9,3 3,9 3,0 2,8 1,6 1,6 1,6 1,5 2007 2008 2009 2010 2011 2012 2013 2014 9M 2015 Source: ZSE 2 ...while the most traded shares were from cyclical industries... TOP 20 shares on ZSE in 2007 turnover in EUR ’000 Ina HT Adris (pref.) Ericsson Nikola Tesla Atlantska Plovidba Ingra Dalekovod IGH Podravka Viro ZABA IPK Kandit Koncar Jadroplov Jadransko osiguranje Tehnika Hidroelektra niskogradnja Duro Dakovic Ledo PBZ 0 200 400 600 800 1.000 1.200 1.400 1.600 Source: ZSE 3 ... talking abt. „limited downside and huuuge upside”... 4 ... but broad regional story made it all up... Regional average daily turnover now vs. ZSE 2007 in EURm 11.7 0.4 10.6 0.4 0.9 1.5 7.3 Romania Croatia Slovenia Bulgaria Serbia Total Region ZSE 2007 Source: Bloomberg 5 Local names got lost in the „crowd”... TOP 20 shares on ZSE in 2007 TOP 20 shares on the regional stock exchanges turnover in EUR ’000 turnover in EUR ’000 Ina Fondul Proprietaea HT Banca Transilvania Adris (pref.) Romgaz Ericsson Nikola Tesla BRD Atlantska Plovidba Electrica Ingra Krka Dalekovod OMV Petrom IGH Transelectrica Podravka Transgaz Viro AIK Banka ZABA HT IPK Kandit SIF Banat Crisana Koncar SIF Moldova Jadroplov Adris (pref.) Jadransko osiguranje Zavarovalnica Triglav Tehnika Valamar Riviera Hidroelektra niskogradnja Telekom Slovenije Duro Dakovic Pivovarna Lasko