Namibia State of Logistics 2018 Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Digital Terrestrial Television Infrastructure Rollout

Digital Terrestrial Television Infrastructure Rollout Environmental Impact Assessment - Nakop - 1 1. ENVIRONMENTAL IMPACT ASSESSMENT: NAKOP 1.1 INTRODUCTION The farm Nakop is privately owned, belonging to Mr and Mrs Tonnemacher. The farm is located approximately 5km east of the Namibian Border post and approximately 6km east of the nearest settlement which is called Ariamsvlei. The presence of the Namibian border post en route to South Africa contributes to a large average number of tourists passing through the town annually. 1.2 RATIONALE FOR SITE The position of the existing microwave tower at Nakop has very good coverage even beyond the Namibian border into South Africa, covering large parts of the south-eastern extremities of Namibia (Figure 1-1). This microwave tower is however very visible from the B3 road to South Africa. For this reason the proposed site is located close to the existing infrastructure but further back from the edge of the plateau to ensure that it is not quite as visible as the existing infrastructure. Figure 1-1: Predicted coverage of the existing microwave tower at Nakop. Digital Terrestrial Television Infrastructure Rollout – NBC EIA - Nakop August 2013 2 1.3 SITE DESCRIPTION Ariamsvlei is located at the foot of a plateau and as one approaches the Orange River approximately 40km south of the town, there is a sharp decrease in elevation. The surrounding area forms part of the Nama Karoo biome and comprises of a combination of small succulents and grass species. Although not particularly high in faunal diversity, the rocky side slopes of the plateau are an optimal niche for the occurrence of a variety of reptiles and birds. -

Namibia Handbook

TABLE OF CONTENTS LIST OF TABLES ................................................................................................................. 2 LIST OF ACRONYMS .......................................................................................................... 3 1. OVERVIEW OF NAMIBIA ............................................................................................. 4 2. TRANSPORT SYSYEM ................................................................................................. 4 2.2 Border posts ............................................................................................................................... 4 3. ROAD TRANSPORT LEGISLATION ............................................................................ 6 3.1 Speed Limits ............................................................................................................................... 6 3.2 Traffic Fines ................................................................................................................................ 6 4. CROSS BORDER ROAD TRANSPORT PERMITS ....................................................... 7 5. ECONOMIC OUTLOOK ................................................................................................ 7 5.1 Trade Environment .................................................................................................................... 7 5.2 Trade Agreements .................................................................................................................... -

Environmental Scoping Assessment

ENVIRONMENTAL IMPACT ASSESSMENT FOR THE PROPOSED CONSTRUCTION OF FACILITIES AND STORAGE AND HANDLING OF OIL AND PETROLEUM PRODUCTS IN ARIAMSVLEI, //KHARAS DISTRICT 2020 GREEN EARTH Environmental Consultants 1 ENVIRONMENTAL IMPACT ASSESSMENT FOR THE PROPOSED CONSTRUCTION OF FACILITIES AND STORAGE AND HANDLING OF Project Name: OIL AND PETROLEUM PRODUCTS IN ARIAMSVLEI, //KHARAS DISTRICT XBFS (Extreme Bulk Fuel Services) The Proponent: P.O. Box 4152 Walvis Bay Prepared by: Release Date: March 2020 C. Du Toit C. Van Der Walt Consultant: Cell: 081 127 3145 Fax: 061 248 608 Email: [email protected] GREEN EARTH Environmental Consultants 2 EXECUTIVE SUMMARY Green Earth Environmental Consultants were appointed by the proponent, XBFS (Extreme Bulk Fuel Services), to conduct an environmental impact assessment for the proposed construction of facilities and storage and handling of oil and petroleum products on Portion 1 of the Remainder of Portion 36 of the Farm Ukumas No. 69, located in the Village of Ariamsvlei, //Kharas District. In accordance with the Environmental Impact Assessment Regulations (GN 30 in GG 4878 of 6 February 2012) of the Environmental Management Act (No. 7 of 2007) the activities listed below, which forms part of the proposed operations, may not be undertaken without an Environmental Clearance: ENERGY GENERATION, TRANSMISSION AND STORAGE ACTIVITIES - The construction of facilities for the refining of gas, oil and petroleum products; HAZARDOUS SUBSTANCE TREATMENT, HANDLING AND STORAGE - The storage and handling of dangerous goods, including petrol, diesel, liquid petroleum gas or paraffin, in containers with a combined capacity of more than 30 cubic meters at any one location. - Construction of filling stations or any other facility for the underground and aboveground storage of dangerous goods, including petrol, diesel, liquid, petroleum, gas or paraffin. -

Walvis Bay - Ndola - Lubumbashi Development Corridor the Gateway Terminal for Handling Bulk and Breakbulk Commodities

WALVIS BAY - NDOLA - LUBUMBASHI DEVELOPMENT CORRIDOR THE GATEWAY TERMINAL FOR HANDLING BULK AND BREAKBULK COMMODITIES Oshikango Katima Mulilo In Namibia, TransNamib is the only Livingstone Oshakati Bagani rail operator capable of handling Bulk Opuwo Rundu Volumes at the most competitive price. Ondangwa Cape Fria Tsumeb Our Grootfontein Corridor Business Otavi Grootfontein Development Hub offers distinctive Outjo rail-road-rail transport and logistics Otjiwarongo services that includes freight handling, Omaruru administration, warehousing, temporary Kranzberg storage for onward transit and outright Okahandja Trans Kalahari export, customs documentations & Swakopmund Hosea Windhoek Kutako Gobabis clearing and storage facilities. Our Walvis Bay freight focus includes Containerised Business, Building Materials, Bulk Fuel, Bulk Liquid, Mining, Agriculture and Mariental General. Keetmanshoop Our rail transportation train capacity is Seeheim Luderitz equivalent to more than 30 trucks en- Aus route the Walvis Bay – Grootfontein Karasburg Upington – Livingstone - Ndola - Lubumbashi Corridors on a daily basis. Ariamsvlei ROUTES WALVIS BAY – OTJIWARONGO – OTAVI – SERVICES OFFERED: GROOTFONTEIN 631 KILOMETRES OSHIKANGO – ONDANGWA – TSUMEB – GROOTFONTEIN 308 KILOMETRES • Offloading and unloading and storage of imported and WINDHOEK – OTJIWARONGO – OTAVI – 468 KILOMETRES exported goods. GROOTFONTEIN • Packing and unpacking (stuffing WALVIS BAY – GROOTFONTEIN – RUNDU – KATIMA and destuffing) of containerized MULILO – LIVINGSTONE 1593 KILOMETRES export -

Government Gaze'i.I'e Republic of Namibia

GOVERNMENT GAZE'I.I'E OF THE REPUBLIC OF NAMIBIA N$2,20 WINDHOEK - 27 January 1994 No. 787 CONTENTS: Page ROAD CARRIER PERMITS .................................................................. 1 ROAD CARRIER PERMITS The under-mentioned applications for Public Road Carrier Permits indicate (1) reference number and the area within which the proposed road trans port will be undertaken, (2) name of applicant and nature of application, (3) number and type of vehicles, ( 4) nature of proposed road transportation and (5) points between and routes over or area within which the proposed road transportation is to be effected and are published in terms of section 14(1) of the Road Transportation Act, 1977 (Act 74 of 1977). Represen tations which interested parties wish to make in respect of the applications must comply with the provisions of regulation 4(1) of the Road Trans portation Regulations, 1977 and must be in quadruplicate in respect of each application and must be delivered by hand or sent by registered post to the Secretary, Road Transportation Board, Private Bag Xl3187, Windhoek to reach that office not later than 21 days after the date of publication of this Government Gazette. 2 Government Gazette 27 January 1994 No. 787 (1) 10/10/91 910P0722 (2) COUNTY CARRIERS CC., WINDHOEK - New application repu blication of application. (3) CY 115407 S/trailer 40000 kg CY 116416 S/trailer 40000 kg CAR 4080 S/trailer 40000 kg CAR 8093 S/trailer 33000 kg CAR 1389 S/trailer 42000 kg CV 22133 S/trailer 40000 kg CV 3434 S/trailer 45000 kg (4) (a) Frozen fish. -

Namibia, Chobe and Victoria Falls 2019

Wonderbag Exploratory Tour: Namibia, Chobe and Victoria Falls 2019 Name of Group Africa’s Gift Namibia-Wonder Group Details Destination Namibia, Botswana, Zimbabwe. Number of Adults 10+ Date of Proposal 12 October 2018 Date of Travel 1 -17 August 2019 Trip reference NAMIB19 Version v1.00 Proposed itinerary for Africa’s Gift tour to Namibia, Chobe and Victoria Falls Day 1 Route: Johannesburg – Upington. Activities: In transit Day 2 Route: Upington – Ai-Ais, via Ariamsvlei, Karasburg and Grünau. Activities: Border crossing into Namibia at Nakop Border Post Lunch time stop at Canyon Road House Road Stall. Visit Fish River Canyon viewpoints. Hike along the edge of the Canyon. Enjoy hot springs resort at Ai-Ais with hot water indoor swimming pools. Overnight: Ai-Ais resort Day 3 Route: Ai-Ais – Lüderitz, via Rosh Pinah and Aus. Activities: Experience the scenery of the Ai-Ais Richtersveld Transfrontier Park along the northern bank of the Gariep River. Stop to view the feral horses of the Namib near Garub. Experience the desolated scenery of the transitional desert in the South of Namibia. Explore historic town of Lüderitz on foot. Visit the historic Dias Cross at Dias Point – replica of cross erected in 1488. Overnight: Obelix Village Guest House Day 4 Route: Lüderitz – Maltahöhe, via Aus and Helmeringhausen. Activities: Visit the historic ghost town at Kolmanskoppe where diamonds were discovered in 1908 (guided tour). Opportunity again to see the feral horses of the Namib. Visit Duwisib Castle (time permitting). Experience the scenery of the Namib on the east of the dune belt. Overnight: Hammerstein Lodge Day 5 Route: Hammerstein – Solitaire, via Sesriem and Sossusvlei. -

Namibian Tour Bookings: 2021

NAMAKWA TOERE &AKKOMMODASIE PTY LTD 2020/895816/07 T/A NAMAQUA TOURS Adventure to: Namibia Start: Cape Town – Windhoek Windhoek – Cape Town Pretoria – Windhoek Windhoek –Pretoria Pretoria - Pretoria Type: Luxury bus travel & Lodging Reference: NAM 4 A basic level of fitness is required to be able to enjoy this trip Physical: to the fullest. Suitable for people under the age of 85 years – please feel free to contact the office for more info. Is this the right trip for you? • This itinerary features some long travel days which can be even longer due to the bumpy African roads. • Namibia temperatures rise in the summer months, (September – November) before the rain comes, to 34 - 38° C. • What you see on your trip may not be the same as seen by other or in pictures, due to it being a seasonal destination and migratory patterns of animals are not interrupted by fencing. • As the early bird catches the worm, there might be a few early morning starts to make sure of best safari times or to miss morning traffic on long travel days. • This trip is mainly lodging in 2-4 star facilities that complement the setting and location we are in. All of the chosen facilities were visited and inspected beforehand to make sure it is up to our standard. • This trip is operated in a 22 seated luxury 4x4 bus. We endeavour not to take more than 20 people at a time. Single accommodation is therefore limited. • In the case where we have less than 11 bookings the tour will be done with a 14 seater Toyota Quantum. -

4. Logistics Network in SADC and Namibia

4. Logistics Network in SADC and Namibia 4. Logistics Network in SADC and Namibia 4.1 Regional cargo flows in SADC 4.1.1 Logistics network in SADC Figure 4.1 shows an overall picture of the current logistics network in SADC, including ports, airports, railways and corridors (trunk roads). Business people look at the picture when they need to provide logistics services in SADC and consider which route fits their needs in terms of cost, time, security, and additional)"" services and functions. )"" )"" Mouila Masuku )"" Kigali RwanDa Mwanza Somalia Tchibanga Bubanza Kenya Congo Bandundu Bujumbura Arusha Moshi )"" Shinyanga Gabon Brazzaville Kinshasa BurunDi Mombasa )"" Madingou Ki"nkala Kigoma Singida Z Tabora Tanga Wete Cabinda Mkoani Matadi Koani Mbanza Congo Congo, DRC Morogoro Kibaha Dar es Salaam Tanzania )"" Kahemba Z"(!P Uige Iringa Sumbawanga Luanda Lucapa )"" Mbeya (!Z"P Caxito Malange Saurimo Ndalatando Lindi Kasama Songea Mtwara Ngunza Mansa Mzuzu Luena )"" Solwezi (!BPenguela Huambo Angola Ndola Pemba Malawi Lilongwe )"" Kabwe ChipZ"ata Menongue (!P Zambia Mocambique (!PNamibe Mongu Lusaka )""Z Mozambique Tete Blantyre Onjiva Kasane Harare )"" Quelimane Livingstone Z" Mutare Zimbabwe Otavi Chimoio Maun Beira Outjo Bulawayo Gweru (!P Otjiwarongo Francistown Masvingo Ghanzi " Karibib )" National Capital Windhoek Serowe )""" Botswana (!P Port W(!aPlvis Bay Z Gobabis Namibia " Airport Rehoboth Pietersburg (Polokwane) Inhambane Z Mochudi Gaborone Railway Maltahohe " Kany)"e Xai-Xai Primary road Lobatse Pretoria )"" Maputo Local road -

Export of Manganese Ore Via the Port of Lüderitz Environmental

EXPORT OF MANGANESE ORE VIA THE PORT OF LÜDERITZ ENVIRONMENTAL ASSESSMENT SCOPING REPORT Assessed by: Assessed for: May 2019 EXECUTIVE SUMMARY Pektranam Logistics (Pty) Ltd wish to realise the export of manganese ore, originating from the Northern Cape, South Africa, through the Port of Lüderitz. Geo Pollution Technologies (Pty) Ltd was requested to undertake an environmental assessment for all activities associated with the proposed transport, storage and handling of the manganese ore. The project will develop in a phased approach. Initial volumes to be exported are 30,000 tons per month as one shipment. Based on available port capacity, and depending on other port users, this can be increased to three shipments per month (90,000 tons). During the environmental assessment process, and based on public and authority consultation, a significant shift in the proposed project plan occurred. Therefore, the original project plan that that was communicated to the public when the project was initiated, differs from the current project as proposed in this assessment. Some of these changes were communicated to the registered interested and affected parties and authorities, during the assessment process, via electronic communication and a second public meeting. However, since then, and based on more public input and objections and authority recommendations, more changes to the project plan were made. These are presented in the current report, which will also serve to inform registered interested and affected parties and authorities of the changes, as well as allow for another round of review and commenting. The current plan will allow for the transport of the ore in either bulk bags, containerised, or as loose ore, and will be by rail and / or road. -

Polling Stations 2019 Presidential and National Assembly Elections

PRESIDENTIAL AND NATIONAL PRESIDENTIALASSEMBLY ANDELECTIONS NATIONAL ASSEMBLY ELECTIONS POLLING STATIONS OPEN 27 NOVEMBER 2019 07H00POLLING - 21H00 STATIONS OPEN 27 NOVEMBER 2019 07H00 - 21H00 NAMIBIA PROMOTING INCLUSIVE 2019 PARTICIPATIONPROMOTING INCLUSIVE 2019 PARTICIPATION GO VOTE, YOUR VOTE COUNTS! 27 NOVEMBERGO 2019 VOTE, YOUR VOTE COUNTS! ECN_ENGLISH ECN_ENGLISH www.facebook.com/ElectoralCommisionOfNamibia twitter: @ECN_Namibia GO VOTE, YOUR VOTE COUNTS www.ecn.na 2 NAMIBIA VOTES 2019 CEOs Message In a representative democracy, inclusive The period of Submission of Nominations of Services who are required to be on duty on elections are the entry point for political candidates for the 2019 Presidential elections the 27th of November 2019 will also cast processes that reflect the genuine will of all and members of the National Assembly their votes on 13th November 2019 as per the people. Without this condition, political commenced on the 1st and was completed Section 64 (2) (a-c) of the Electoral Act in all processes remain exclusive and geared on18th October 2019. The submissions the 121 constituencies countrywide at the towards addressing specific individual and/or for the nominations of candidates for the 133 designated polling stations countrywide. group interests. The Electoral Commission of Presidential elections as well as members Namibia’s (ECN) theme for this years’ electoral of the National Assembly is governed by The 2019 Presidential and National Assembly process is aptly titled: Promoting Inclusive Sections 72, 73 and 77 of the Electoral Act, elections are scheduled to take place on 27th Participation. This theme underscores the Act 5 of 2014. November 2019. Polling stations will open importance of raising awareness so as to from 07h00 – 21h00. -

The Establishment of Truck Stops Along the Walvis Bay Corridors

HXA-NO93 The Establishment of Truck Stops Along the Walvis Bay Corridors An Interactive Qualifying Project submitted to the Department of Infrastructure and the Faculty of Worcester Polytechnic Institute in partial fulfillment of the requirements for the Degree of Bachelor of Science Sponsoring Agency: Walvis Bay Corridor Group Submitted to: On-Site Liaison: Gilbert Boois, WBCG Projects & Funding Project Advisor: Holly K. Ault, WPI Professor Project Co-advisor: R. Creighton Peet, WPI Professor Submitted by: _______________________________ Brian Earley _______________________________ Craig Jones _______________________________ Anthony Laine _______________________________ Bryan Rickard Date: 8 May 2009 This report represents the work of four WPI undergraduate students submitted to the faculty as evidence of completion of a degree requirement. WPI routinely publishes these reports on its web site without editorial or peer review. Keywords: transportation, infrastructure, truck stops ABSTRACT We created this report to help the Walvis Bay Corridor Group create truck stops in Namibia to improve the country’s transportation infrastructure for truck drivers. We conducted a survey of truck drivers and numerous interviews with relevant companies to determine what services truck stops in Namibia should feature and where they should be located. Furthermore, we made recommendations about how to expand our plan to install truck stops in additional locations in the future. ii ACKNOWLEDGEMENTS We would like to thank Gilbert Boois, our on-site liaison, and everyone else at the Walvis Bay Corridor Group who guided and helped us throughout our time in Namibia. Johny Smith Edward Shivute Mbahupu ―Hippy‖ Tjivikua Sylvia Maketo Thanks must also go to those at the Polytechnic of Namibia’s Centre for Entrepreneurial Development who provided valuable suggestions for our report. -

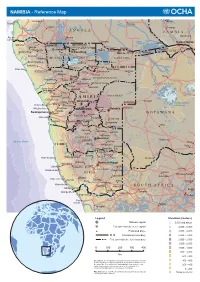

Reference Map

NAMIBIA - Reference Map Chiange Mongu Tombus Mavinga Cahama Senanga A N G O L A Z A M B I A Z am Mulobezi Foz do Ondjiva b e Cunene mene z Ku Katwitwi i Otue Luiana Katima Mulilo Otjihende Uutapi Eenhana O kav Etanga OHANGWENA ango Kaiango Zilitene Orotjitombo Oshakati Nepara Kongola Otjiwarongo Katanda CAPRIVI Omuthiya Rundu Ndonge Linona Bagani Oruwanje OSHANA Ongango OMUSATI OSHIKOTO KAVANGO Etosha Tsintsabis Otjozongombe Pan Namutoni Sesfontein Tsumeb Okaukuejo Abenab Möwe Bay Moroeloboom KUNENE Kamanjab Otavi Grootfontein Tsumkwe Otjikondo Guchab Maun Outjo OTJOZONDJUPA Fransfontein Okaputa Tutara Okave Khorixas Otjiwarongo Otumborombonge Lake Ngami Erundu Okakarara Sorris-Sorris Kalkfeld Ugab Uis Omatjette Sukses Okombahe OMAHEKE Omaruru N A M I B I A ERONGO Ghanzi Usakos Karibib Okahandja Rietfontein Makgadikgadi Ebony Henties Bay Wilhelmstal (salt pans) Omitara Mamuno Wlotzkas Baken Trekkopje WINDHOEK Gobabis Arandis Witvlei Swakopmund Namib B O T S W A N A KHOMAS Brack Walvis Bay Dordabis Great Ums Rehoboth Rooibank Rostock Isabis Noasanabis Tsumis Kang Derm Aminuis Kalkrand Hoachanas Aranos Kub N Stampriet os so HARDAP Mariental b Maltahöhe Khakhea Atlantic Ocean Gochas Kanye Gibeon Witbooisvlei Akanaus Tsatsu Asab Eindpaal Sud Brukkaros A uo Berseba Presopes b Tses Hottentotspunt Helmeringhausen Koës Tshabong Bethanien Haalenberg Keetmanshoop Goageb Lüderitz Ausweiche Aroab Vryburg Elizabeth Bay Seeheim Noord Vredeshoop KARAS Hotazel Schweizer-Reneke Tsaraxaibis Kuruman Witputs Angra-Juntas Grünau Chameis Ai-Ais Nabas Christiana