Climate Change and Carbon Markets: Implications for Developing Countries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Potential for Biofuels Alongside the EU-ETS

The potential for biofuels alongside the EU-ETS Stefan Boeters, Paul Veenendaal, Nico van Leeuwen and Hugo Rojas-Romagoza CPB Netherlands Bureau for Economic Policy Analysis Paper for presentation at the Eleventh Annual GTAP Conference ‘Future of Global Economy’, Helsinki, June 12-14, 2008 1 Table of contents Summary 3 1 The potential for biofuels alongside the EU-ETS 6 1.1 Introduction 6 1.2 Climate policy baseline 7 1.3 Promoting the use of biofuels 10 1.4 Increasing transport fuel excises as a policy alternative from the CO 2-emission reduction point of view 22 1.5 Conclusions 23 Appendix A: Characteristics of the WorldScan model and of the baseline scenario 25 A.1 WorldScan 25 A.2 Background scenario 27 A.3 Details of biofuel modelling 28 A.4 Sensitivity analysis with respect to land allocation 35 References 38 2 Summary The potential for biofuels alongside the EU-ETS On its March 2007 summit the European Council agreed to embark on an ambitious policy for energy and climate change that establishes several targets for the year 2020. Amongst others this policy aims to reduce greenhouse gas emissions by at least 20% compared to 1990 and to ensure that 20% of total energy use comes from renewable sources, partly by increasing the share of biofuels up to at least 10% of total fuel use in transportation. In meeting the 20% reduction ceiling for greenhouse gas emissions the EU Emissions Trading Scheme (EU-ETS) will play a central role as the ‘pricing engine’ for CO 2-emissions. The higher the emissions price will be, the sooner technological emission reduction options will tend to be commercially adopted. -

Paving the Way to Carbon-Neutral Transport: 10-Point Plan To

Paving the way to carbon-neutral transport 10-point plan to help implement the European Green Deal January 2020 CONTEXT The transport sector is responsible for 22.3% of total EU greenhouse gas (GHG) emissions, with road transport representing 21.1% of total emissions. Breaking this down further, passenger cars account for 12.8% of Europe’s emissions, vans for 2.5%, while heavy-duty trucks and buses are responsible for 5.6%. Transport is therefore a key focus and driver for climate protection measures. The European Automobile Manufacturers’ Association (ACEA) strongly believes that carbon-neutral road transport is possible by 2050. This however will represent a seismic shift, requiring a holistic approach with increasing efforts from all stakeholders. * All CO2 equivalent ** Industry = ‘Manufacturing industries and construction’ + ‘Industrial processes and product use’ Source: European Environment Agency (EEA) AUTO INDUSTRY CONTRIBUTION Investing €57.4 billion in R&D annually, the automotive sector is Europe's largest private contributor to innovation, accounting for 28% of total EU spending. Much of this investment is dedicated to clean mobility solutions. The automobile industry embraces the Paris Agreement and its goals. Manufacturers also support the climate protection initiatives of the European Commission, such as the ‘Clean Planet for All’ strategy, provided all stakeholders contribute their share and the achievements to date are taken into account. ACEA’s 10-point plan to help implement the European Green Deal – January 2020 1 ACEA members are fully committed to deliver the ambitious 025 and 030 C2 reduction targets. In order to provide legal certainty for the industry as it moves towards carbon neutrality in 050, the 2022/2023 timeline for the revies of the regulations should be adhered to (as as endorsed by the European Council in December 201). -

Benefits of Emissions Trading

BENEFITS OF EMISSIONS TRADING E M I S S I O N S T R A D I N G A C H I E V E S T H E E N V I R O N M E N T A L O B J E C T I V E – R E D U C E D E M I S S I O N S – A T T H E L O W E S T C O S T Cap and trade is designed to deliver an environmental outcome; the cap must be met, or there are sanctions such as fines. Allowing trading within that cap is the most effective way of minimising the cost – which is good for business and good for households. Determining physical actions that companies must take, with no flexibility, is not guaranteed to achieve the necessary reductions. Nor is establishing a regulated price, since the price required to drive reductions may take policy-makers several years to determine. Cap and trade also provides a way of establishing rigour around emissions monitoring, reporting and verification – essential for any climate policy to preserve integrity. E M I S S I O N S T R A D I N G I S B E T T E R A B L E T O R E S P O N D T O E C O N O M I C F L U C T U A T I O N S T H A N O T H E R P O L I C Y T O O L S Allowing the open market to set the price of carbon translates to better flexibility and avoids price shocks or undue burdens. -

Analytical Environmental Agency 2 21St Century Frontiers 3 22 Four 4

# Official Name of Organization Name of Organization in English 1 "Greenwomen" Analytical Environmental Agency 2 21st Century Frontiers 3 22 Four 4 350 Vermont 5 350.org 6 A Seed Japan Acao Voluntaria de Atitude dos Movimentos por Voluntary Action O Attitude of Social 7 Transparencia Social Movements for Transparency Acción para la Promoción de Ambientes Libres Promoting Action for Smokefree 8 de Tabaco Environments Ações para Preservação dos Recursos Naturais e 9 Desenvolvimento Economico Racional - APRENDER 10 ACT Alliance - Action by Churches Together 11 Action on Armed Violence Action on Disability and Development, 12 Bangladesh Actions communautaires pour le développement COMMUNITY ACTIONS FOR 13 integral INTEGRAL DEVELOPMENT 14 Actions Vitales pour le Développement durable Vital Actions for Sustainable Development Advocates coalition for Development and 15 Environment 16 Africa Youth for Peace and Development 17 African Development and Advocacy Centre African Network for Policy Research and 18 Advocacy for Sustainability 19 African Women's Alliance, Inc. Afrique Internationale pour le Developpement et 20 l'Environnement au 21è Siècle 21 Agência Brasileira de Gerenciamento Costeiro Brazilian Coastal Management Agency 22 Agrisud International 23 Ainu association of Hokkaido 24 Air Transport Action Group 25 Aldeota Global Aldeota Global - (Global "small village") 26 Aleanca Ekologjike Europiane Rinore Ecological European Youth Alliance Alianza de Mujeres Indigenas de Centroamerica y 27 Mexico 28 Alianza ONG NGO Alliance ALL INDIA HUMAN -

IFC Carbon Neutrality Committment Factsheet

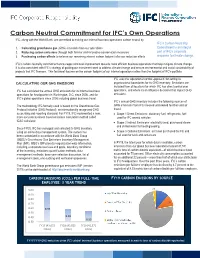

Carbon Neutral Commitment for IFC’s Own Operations IFC, along with the World Bank, are committed to making our internal business operations carbon neutral by: IFC’s Carbon Neutrality 1. Calculating greenhouse gas (GHG) emissions from our operations Commitment is an integral 2. Reducing carbon emissions through both familiar and innovative conservation measures part of IFC's corporate 3. Purchasing carbon offsets to balance our remaining internal carbon footprint after our reduction efforts response to climate change. IFC’s carbon neutrality commitment encourages continual improvement towards more efficient business operations that help mitigate climate change. It is also consistent with IFC’s strategy of guiding our investment work to address climate change and ensure environmental and social sustainability of projects that IFC finances. This factsheet focuses on the carbon footprint of our internal operations rather than the footprint of IFC’s portfolio. IFC uses the ‘operational control approach’ for setting its CALCULATING OUR GHG EMISSIONS organizational boundaries for its GHG inventory. Emissions are included from all locations for which IFC has direct control over IFC has calculated the annual GHG emissions for its internal business operations, and where it can influence decisions that impact GHG operations for headquarters in Washington, D.C. since 2006, and for emissions. IFC’s global operations since 2008 including global business travel. IFC’s annual GHG inventory includes the following sources of The methodology IFC formally used is based on the Greenhouse Gas GHG emissions from IFC’s leased and owned facilities and air Protocol Initiative (GHG Protocol), an internationally recognized GHG travel: accounting and reporting standard. -

Trade and Environment: a Resource Book

TRADE AND ENVIRONMENT – Trade and Environment A Resource Book Trade and environment policy is increasingly intertwined and the stakes are nearly always high in both trade and environmental TRADE AND terms. These issues are often complex and discussions tend to become very specialized, challenging policy practitioners to understand and follow all the various sub-strands of trade and ENVIRONMENT environment debates. This Resource Book seeks to demystify these issues without losing the critical nuances. A RESOURCE BOOK This collaborative effort of some 61 authors from 34 countries provides relevant information as well as pertinent analysis on a broad set of trade and environment discussions while explaining, A RESOURCE BOOK as clearly as possible, what are the key issues from a trade and environment perspective; what are the most important policy debates around them; and what are the different policy positions Edited by that define these debates. Adil Najam The volume is structured and organized to be a reference document Mark Halle that is useful and easy to use. Our hope is that those actively involved in trade and environment discussions—as practitioners, Ricardo Meléndez-Ortiz as scholars and as activists—will be able to draw on the analysis Meléndez-Ortiz Najam, Mark Halle and Ricardo Adil Edited by and opinions in this book to help them advance a closer synergy between trade and environmental policy for the common goal of achieving sustainable development. T&E Resource.qx 10/17/07 4:39 PM Page i TRADE AND ENVIRONMENT A RESOURCE BOOK Edited by Adil Najam Mark Halle Ricardo Meléndez-Ortiz T&E Resource.qx 10/17/07 4:39 PM Page ii Trade and Environment: A Resource Book © 2007 International Institute for Sustainable Development (IISD), International Centre for Trade and Sustainable Development (ICTSD) and the Regional and International Networking Group (The Ring). -

Carbon Emission Reduction—Carbon Tax, Carbon Trading, and Carbon Offset

energies Editorial Carbon Emission Reduction—Carbon Tax, Carbon Trading, and Carbon Offset Wen-Hsien Tsai Department of Business Administration, National Central University, Jhongli, Taoyuan 32001, Taiwan; [email protected]; Tel.: +886-3-426-7247 Received: 29 October 2020; Accepted: 19 November 2020; Published: 23 November 2020 1. Introduction The Paris Agreement was signed by 195 nations in December 2015 to strengthen the global response to the threat of climate change following the 1992 United Nations Framework Convention on Climate Change (UNFCC) and the 1997 Kyoto Protocol. In Article 2 of the Paris Agreement, the increase in the global average temperature is anticipated to be held to well below 2 ◦C above pre-industrial levels, and efforts are being employed to limit the temperature increase to 1.5 ◦C. The United States Environmental Protection Agency (EPA) provides information on emissions of the main greenhouse gases. It shows that about 81% of the totally emitted greenhouse gases were carbon dioxide (CO2), 10% methane, and 7% nitrous oxide in 2018. Therefore, carbon dioxide (CO2) emissions (or carbon emissions) are the most important cause of global warming. The United Nations has made efforts to reduce greenhouse gas emissions or mitigate their effect. In Article 6 of the Paris Agreement, three cooperative approaches that countries can take in attaining the goal of their carbon emission reduction are described, including direct bilateral cooperation, new sustainable development mechanisms, and non-market-based approaches. The World Bank stated that there are some incentives that have been created to encourage carbon emission reduction, such as the removal of fossil fuels subsidies, the introduction of carbon pricing, the increase of energy efficiency standards, and the implementation of auctions for the lowest-cost renewable energy. -

Emissions Trading Worldwide

Emissions Trading Worldwide International Carbon Action Partnership (ICAP) Status Report 2017 Emissions Trading Worldwide International Carbon Action Partnership (ICAP) Status Report 2017 Editorial Team Marissa Santikarn, Alexander Eden, Lina Li, Johannes Ackva, William Acworth, Martina Kehrer, Oliver Lübker, Julia Melnikova, Mariza Montes de Oca, Kateryna Stelmakh, Charlotte Unger, Kristian Wilkening and Constanze Haug. Cite as ICAP. (2017). Emissions Trading Worldwide: Status Report 2017. Berlin: ICAP. The ICAP Secretariat expresses its gratitude to policymakers from the ICAP membership and further collaborators from the emis- sions trading field, who provided insightful, written contributions and carefully reviewed the report: Marco Aurélio dos Santos Araujo (Brazil), Jean-Yves Benoit (Québec), Chen Zhibin (Sinocarbon), Mary Jane Coombs (California), Matthew Cowie (New Zealand), Lynda Danquah (Canada), Sean Donavan (Mexico), Johannes Enzmann (European Commission), Victor Escalona (Mexico), Jason Hollett (Nova Scotia), Huang Xiaochen (Sinocarbon), Cécile Goubet (France), Huang Dayue (Chonqging Low Carbon Consulting), Ai Kaibu (Japan), Sun-Yeong Kim (Republic of Korea), Marat Latypov (Russia), Stéphane Legros (Québec), Pongvipa Lohsomboon (Thailand), Vivian Vieira de Macedo (Brazil), Anaïs Maillet (France), Akiko Miura (Tokyo Metropolitan Government), Antje Mosler (Switzerland), Nicolas Muller (UNFCCC), Sachiko Nakamura (Tokyo Metropolitan Government), Il-Young Oh (Republic of Korea), Megan O’Toole (Vermont), Heather Pearson (Ontario), Saul Pereyra (Mexico), Qian Guoqiang (Sinocarbon), Huy Luong Quang (Vietnam), Kathleen Rich (Canada), Juan Pedro Searle (Chile), Gulmira Sergazina (Kazkahstan), William Space (Massachusetts), Sophie Wenger (Switzerland), Tony Usibelli (Washington State), Zeren Erik Yasar (Turkey), Alfred Alexandre Yameogo (Québec), Olga Yukhymchuk (Ukraine) The ICAP Secretariat is grateful to the German Federal Ministry for Environment, Nature Conservation, Building and Nuclear Safety (BMUB) for funding this report. -

Carbon Cycling, Privatization and the Commons

***draft for comment***draft for comment***draft for comment***draft for comment*** Carbon Cycling, Privatization and the Commons Larry Lohmann The Corner House Station Road Sturminster Newton Dorset DT10 1YJ UK [email protected] I Traditionally, the earth’s ability to keep greenhouse gas proportions within the atmosphere within a certain range has been what is known as “open access”. Anybody has been free to dump carbon dioxide into the atmosphere, with no rules being applicable except ones incidentally relating to accompanying pollutants. Because nothing has been at stake, the world’s carbon-cycling capacity has never until recently been a resource. And it will always remain too unwieldy and unbounded to be treated as, by contrast, a commons.1 Yet through familiar processes of overuse and skewed use, global carbon-cycling capacity has recently begun to be treated as economically scarce. For over 150 years, industrial societies have been transferring excessive amounts of carbon from underground deposits of coal and oil, where it is more or less sealed off from the atmosphere, to the air. Today, the amount of carbon in the atmosphere increases by six billion tons every year. The earth's carbon dioxide dump is now perceived as overflowing, with potentially disastrous climatic consequences.2 Precise quantification is impossible, but it may not be too far off the mark to say that the US alone, with five per cent of the world’s people, is hogging roughly all of it. Stabilizing atmospheric chemistry while keeping US access to the dump fully open would leave an enormous majority of the world’s people unable to release any carbon dioxide at all. -

22Nd August 2020

22nd August 2020 22nd August 2020 | Matt Mimms 22nd August might seem like a pretty unremarkable day on the face of it. It will of course be the birth date, the death date, the wedding anniversary for countless millions around the world. Notably, it is the birth date of Claude Debussy and Deng Xiaoping, and in death, for Jomo Kenyatta and Richard III. James Cook landed in Australian in 1770, Yacht America won the first America’s Cup regatta in 1851, Theodore Roosevelt was the first US President to ride in a car in 1902, and the BBC began their first TV broadcast on this day in 19321. However, 22 August in 2020 marks an important milestone. Known as Earth Overshoot Day2, “it marks the date when humanity’s demand for ecological resources and services in a given year exceeds what Earth can regenerate in that year”. From now til the rest of the year, we will in effect be depleting the earth’s natural resources over and above the earth’s ability to regenerate, and accumulating waste over and above the earth’s ability to absorb, mainly in the form of carbon dioxide. This is according to the Global Footprint Network3, an award-winning international research organisation focussed on developing and promoting tools for advancing sustainability. So how does this work? First developed in the early 1990s, the Global Footprint Network assesses the relationship between humankind’s Ecological Footprint and its Biocapacity. Put simply, that is the relationship between the ecological assets and resources that a given population requires to produce what it consumes (e.g. -

Application of the EU Emissions Trading Directive Analysis of National Responses Under Article 21 of the EU ETS Directive in 2014

EEA Technical report No 3/2015 Application of the EU Emissions Trading Directive Analysis of national responses under Article 21 of the EU ETS Directive in 2014 ISSN 1725-2237 EEA Technical report No 3/2015 Application of the EU Emissions Trading Directive Analysis of national responses under Article 21 of the EU ETS Directive in 2014 Cover design: EEA Cover photo: http://pl.wikipedia.org/wiki/Grafika:Belchatow-elektrownia.jpg Layout: EEA/Pia Schmidt Legal notice The contents of this publication do not necessarily reflect the official opinions of the European Commission or other institutions of the European Union. Neither the European Environment Agency nor any person or company acting on behalf of the Agency is responsible for the use that may be made of the information contained in this report. Copyright notice © European Environment Agency, 2015 Reproduction is authorised provided the source is acknowledged. More information on the European Union is available on the Internet (http://europa.eu). Luxembourg: Publications Office of the European Union, 2015 ISBN 978-92-9213-639-0 ISSN 1725-2237 doi:10.2800/814207 European Environment Agency Kongens Nytorv 6 1050 Copenhagen K Denmark Tel.: +45 33 36 71 00 Web: eea.europa.eu Enquiries: eea.europa.eu/enquiries Contents Contents List of figures and tables ............................................................................................................ 5 Acknowledgements ................................................................................................................... -

Carbon Pricing – Using Market-Based Mechanisms to Mitigate Climate

Carbon Pricing Using Market-based Mechanisms to Mitigate Climate Change Imprint Published by Federal Ministry for the Environment, Nature Conservation, Building and Nuclear Safety (BMUB) Division KI I 6 · 11055 Berlin · Germany Email: [email protected] · Website: www.bmub.bund.de/english Edited by Dr. Silke Karcher, BMUB, Head of Division KI I 6 · Malin Ahlberg, BMUB, Division KI I 6 Technical editing Wuppertal Institute for Climate, Environment and Energy (Wuppertal Institut für Klima, Umwelt, Energie gGmbH) Research Group: Energy, Transport and Climate Policy Text Nicolas Kreibich and Lukas Hermwille Design Selbach Design, Lohmar Printed by Rautenberg Verlag, Troisdorf Picture credits Front page: Flickr.com | Philippe Roos 'Ain-Beni-Mathar-2010-10-27-005' (CC BY-SA 2.0 –www.flickr.com/photos/elisaphi/ 5860954697/); page 3: Flickr.com | UNFCCC: 'Country Flags outside the conference venue' (CC BY-NC-SA 2.0 – www.flickr.com/photos/unfccc/30563098030/); page 4: Flickr.com | UNFCCC: 'Her Excellency Ms. Angela Merkel, Chancellor of Germany' (CC BY 2.0 – www.flickr.com/photos/unfccc/23129752020/); page 5: Flickr.com | World Bank | Jutta Benzenberg : 'Green Energy' (CC BY-NC-ND 2.0 – www.flickr.com/photos/worldbank/32519834310/); page 6: Flickr.com | World Bank | Dana Smilie: 'Thermo-solar power plant' (CC BY-NC-ND 2.0 – www.flickr.com/photos/worldbank/4842168024/); page 7: Flickr.com | World Bank | Graham Crouch: 'Northwest Kabul Breshna Sub Station' (CC BY-NC-ND 2.0 – www.flickr.com/photos/worldbank/8120062723/); page 8: Flickr.com | BASF: