Responsible Banking

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WAKE up CALL: Navigating New Pathways for Corporate Community Investment in Canada 1 Contents

Navigating New Pathways WAKE for Corporate Community UP CALL: Investment in Canada WAKE UP CALL: Navigating New Pathways for Corporate Community Investment in Canada 1 Contents Acknowledgments 3 Foreword 5 Introduction 6 Social shifts impacting community investment from our research 8 1 The Uneven Pandemic: Profound inequalities exacerbated by COVID-19 9 2 Time for Racial Justice: The role of companies in supporting racial equity 13 3 The Great Cataclysm: Nonprofits during COVID-19 19 4 The Constant Pivot: COVID-19 reaped a fertile ground for nonprofit innovation 22 5 Unrestricted Funding during COVID-19: Building on what’s worked 27 6 Companies Stepped Up: Funding flowed during COVID-19 but could be cut-off 32 7 Engaging Virtual Employees: New challenges, new opportunities 35 8 The CEO as Social Advocate: Increasing expectations on Corporate Canada 40 9 Partnering for Impact: Problems too big to tackle on our own 43 10 COVID-19 and Climate Change: Learning from the pandemic 48 Conclusion 53 Endnotes 56 WAKE UP CALL: Navigating New Pathways for Corporate Community Investment in Canada 2 Acknowledgements We would like to acknowledge the following individuals who were quoted, interviewed, provided feedback, or otherwise had significant influence on this report. The opinions expressed in this report are those of the author, and do not necessarily reflect those quoted, acknowledged, or otherwise supporting the research. Author: Steven Ayer Eugenia Addy, CEO, Visions of Science Project Managers: Devon Hurvid & Émilie Pontbriand Brent Barootes, -

2014 Graduates

Congratulations to The Directors College 2014 Chartered Director* Program Graduates Ann Adair Kim L. Baker Linda S. Beairsto Heather Bell Riz Matthew Blair Brynn Boback-Lane Pierre M. Bocti Roseline Brennan Brian Brown Siemens Canada Ltd. Central Local Health Algonquin Power & NAV CANADA Siemens Canada Ltd. Children’s Hospital Certified General Certified General Canadian Grain Integration Network Utilities Corp. Foundation of Accountants of Ontario Accountants Commission Saskatchewan Edward Carter Barry Cheal Laurel Clark Pierre Côté Nancy Cuelenaere Matthew D. Davies Andrew Day Jacqueline De Gagné Melinda Diebel Certified General Grand River Hospital Jazz Aviation LP Ontario Secondary School Alberta Treasury Board Ciena Canada Inc. Rogers Communications Bayer Inc. Automodular Corporation Accountants of Ontario Teachers’ Federation and Finance Inc. Eldon H. W. Dixon Anna Dopico Doug Elliott Michael Fenn Frank D. Finn Larry Flynn Brian Friedrich David T. Fung Cory Furman Veridian Connections Inc. Corporate Director Corporate Director OMERS Administration McCain Foods Ontario Lottery & Gaming friedrich & friedrich CSA Group Furman IP Law & Strategy Corporation Corporation corporation PC Rose Marie Gage James Harries Ronald Harvey Peter F. J. Heffernan Daniel Johnson Paul G. Keane Jan A. C. Klakurka Martine Leben Jeff M. Leclerc Ag Energy Property and Casualty Certified General Scotiabank Innovation Credit Union CSA Group Huron University College, The Martinique Group Pty University of Manitoba Co-operative Ltd. Insurance Compensation Accountants of Ontario Western University Ltd. (Aus) Corporation (UWO) Carol MacCulloch Gayle MacDonald Diana MacKay Paul Manias Sarah Marriott Scott A. McDonald Dave McPherson Candice J. Molnar George Murphy Independent G-Mac’s AgTeam Inc. The Conference Board OMERS Strategic KWG Resources Inc. -

Innovation Credit Union 2012 Annual Report

Innovation Credit Union 2012 Annual Report Innovation Credit Union 2012 Annual Report Contents Board and Executive ..............................................1 Co-operative Principles .........................................5 Board President Message .....................................2 Our Company............................................................6 CEO Message ............................................................3 CUDGC Message ......................................................7 Purpose, Desired Future State, and Measuring Performance - Vision Story ...............................................................4 2012 Strategic Intents ............................................8 2012 Innovation Credit Union Board of Directors Gord Lightfoot Ian Twidale Mike Davis Bruce Sack Russ Siemens Jerome Bru Bill Volk Audrey Yee Betty Goddard Darlene Kingwell i Executive Team Daniel Johnson Earl Hanson Sheldon Hess Kent Jesse Tim Sletten Chief Executive Officer Chief Risk Officer Chief Financial Officer Chief Innovation and People Chief Retail Officer Officer Annual Report 2012 • 1 Innovation Credit Union 2012 Annual Report A Message from Your Board President Innovation is all about how we serve our members’ financial needs. As a financial cooperative we stay in touch with our members through the democratic process of board elections. Our board is committed to providing the best financial service to our membership. Planning is an important board function. Our board developed a plan for our credit union that will build -

Banking Needs for Leaders January 17, 2019 Presented by Chris Sicotte

Banking Needs for Leaders January 17, 2019 Presented by Chris Sicotte Financial Services Professional with over 26 years of experience Experience in both consumer & commercial banking Board Member of AFOA Saskatchewan & Former Board Chair of AFOA Canada Also member of the following Boards & Committees: Greater Saskatoon Chamber of Commerce (1st Vice Chair) City of Saskatoon Cultural Diversity & Race Relations Committee (Chair) Saskatchewan First Nations Family & Community Institute Inc. Provincial Métis Housing Corporation AIDS Saskatoon Kitotaminawak Parent/Community Council – Oskayak High School What makes the financial institutions different? Banks Governed under the Bank Act Personal deposits insured by Canada Deposit Insurance Corporation up to $100,000 Generally speaking commercial deposits are not covered under CDIC insurance For profit corporations, little or no Indigenous representation on Boards. Trust Companies Governed under Provincial legislation Generally operate the same as Banks (i.e CDIC insurance) Some restrictions on lending practices Also for profit corporations Credit Unions in Saskatchewan Operate under the Credit Union Act Provincially regulated All deposits are 100% insured by Credit Union Deposit Guarantee (“CUDG”) Financial co-operatives, founded on Co-operative values Recent changes have allowed Credit Unions to be Federally regulated. Main change = move to CDIC insurance vs. CUDG Main Services Regardless of whether it’s a Bank, Trust Company, or Credit Union all 3 offer the same core -

A Guide to Canada Emergency Business Account (CEBA)

A Guide to Canada Emergency Business Account (CEBA) Overview: Originally launched on April 9, 2020, CEBA is intended to support businesses by providing financing for their expenses that cannot be avoided or deferred as they take steps to safely navigate a period of shutdown, thereby helping to position businesses for successful relaunch when the economy reopens. This $55 billion program provides interest-free loans of up to $40,000 to small businesses and not-for-profits. Repaying the balance of the loan on or before December 31, 2022 will result in loan forgiveness of 25 percent (up to $10,000). As of June 26, 2020, businesses eligible for CEBA now include owner-operated small businesses that do not have a payroll, sole proprietors receiving business income directly, as well as family-owned corporations remunerating in the form of dividends rather than payroll. This means that more small businesses can access it. Applicants with $20,000 or less in payroll in 2019 will have to demonstrate having Eligible Non-Deferrable Expenses between Cdn.$40,000 and Cdn.$1,500,000 in 2020. Expenses are considered “Eligible Non-Deferrable Expenses” if they were already incurred in January and/or February 2020, or are due to a legal or contractual obligation as at March 1 and cannot be avoided or deferred beyond 2020 even during a period of shut down and depressed revenues as a result of COVID. CEBA is not intended to provide income support, or support for variable operating expenses to businesses. CEBA applicants agree that the government may conduct audits to confirm the nature of the expenses applicants use to establish their eligibility for CEBA, and acknowledge that inaccuracies may lead to legal consequences. -

Second Report of the Interim Receiver – November 14, 2019.Pdf

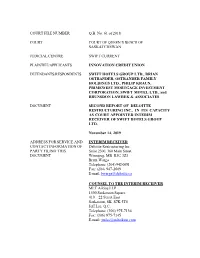

COURT FILE NUMBER Q.B. No. 61 of 2018 COURT COURT OF QUEEN’S BENCH OF SASKATCHEWAN JUDICIAL CENTRE SWIFT CURRENT PLAINTIFF/APPLICANTS INNOVATION CREDIT UNION DEFENDANTS/RESPONDENTS SWIFT HOTELS GROUP LTD., BRIAN OSTRANDER, OSTRANDER FAMILY HOLDINGS LTD., PHILIP KRAUN, PRIMEWEST MORTGAGE INVESTMENT CORPORATION, SWIFT MOTEL LTD., and BRUNSDON LAWREK & ASSOCIATES DOCUMENT SECOND REPORT OF DELOITTE RESTRUCTURING INC., IN ITS CAPACITY AS COURT APPOINTED INTERIM RECEIVER OF SWIFT HOTELS GROUP LTD. November 14, 2019 ADDRESS FOR SERVICE AND INTERIM RECEIVER CONTACT INFORMATION OF Deloitte Restructuring Inc. PARTY FILING THIS Suite 2300, 360 Main Street DOCUMENT Winnipeg, MB R3C 3Z3 Brent Warga Telephone: (204) 942-0051 Fax: (204) 947-2689 E-mail: [email protected] COUNSEL TO THE INTERIM RECEIVER MLT Aikins LLP 1500 Saskatoon Square 410 – 22 Street East Saskatoon, SK S7K 5T6 Jeff Lee, Q.C. Telephone: (306) 975-7136 Fax: (306) 975-7145 E-mail: [email protected] TABLE OF CONTENTS INTRODUCTION .............................................................................................................. 1 TERMS OF REFERENCE ................................................................................................. 2 ACTIVITIES OF THE INTERIM RECEIVER SINCE THE FIRST REPORT ................ 3 BANK ACCOUNT REVIEW ............................................................................................ 4 TD INVESTMENT ACCOUNTS ...................................................................................... 8 OPERATIONS ................................................................................................................... -

Section Ii Geographical List Members / Liste Géographique Des Membres 1

SECTION II GEOGRAPHICAL LIST MEMBERS / LISTE GÉOGRAPHIQUE DES MEMBRES 1 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 100 MILE HOUSE, BC 080925020 25020-809 WILLIAMS LAKE AND DISTRICT CREDIT UN 100 Mile House Branch, 295 Cariboo Highway 97, P.O. Box 1781, 100 Mile House, BC V0K 2E0 ABBOTSFORD, BC 080929060 29060-809 ALDERGROVE CREDIT UNION Abbotsford Community Branch, 100 - 2600 Gladys Avenue, Abbotsford, BC V2S 3X7 080911110 11110-809 Matsqui Community Branch, 5824 Riverside Street, Abbotsford, BC V4X 1V1 080929050 29050-809 Mt. Lehman centre Branch, #100-3224 Mt. Lehman Road, Abbotsford, BC V4X 2M9 080917120 17120-809 COAST CAPITAL SAVINGS CREDIT UNION Clearbrook Branch, 2611 Clearbrook Road, Abbotsford, BC V2T 2Y6 080917140 17140-809 Seven Oaks Branch, 2611 Clearbrook Road, Abbotsford, BC V2T 2Y6 080937930 37930-809 ENVISION FINANCIAL A DIVISION Of First West Credit Union, 2090 Sumas Way, Abbotsford, BC V2S 2C7 080937920 37920-809 Of First West Credit Union, 32711 South Fraser Way, Abbotsford, BC V2T 3S3 080937910 37910-809 Of First West Credit Union, Unit F120, 3122 Mt. Lehman Road, PO Box 2095, Abbotsford, BC V2T 0C5 080946430 46430-809 KHALSA CREDIT UNION Abbotsford Branch, 32112 South Fraser Way, Abbotsford, BC V2T 3Y3 080910980 10980-809 PROSPERA CREDIT UNION ABO Funds Transfer, #500-32071 South Fraser Way, Abbotsford, BC V2T 1W3 080942520 42520-809 Abbotsford Branch, 34630 Delair Road, Abbotsford, BC V2S 2C9 080910970 10970-809 Agent Deposit Branch, -

Make a Difference!

Make a difference! Board of Directors Nomination Package Contents Introduction .............................................................................................................................................................2 Federal Continuance ..........................................................................................................................................2 About Innovation Credit Union – Purpose, Vision, Mission, Values .......................................2 Purpose: ......................................................................................................................................................................2 Vision: ...........................................................................................................................................................................2 Mission:........................................................................................................................................................................2 Responsible Banking - Doing the Right Thing....................................................................................3 Board Responsibilities ........................................................................................................................................4 Director Profile ........................................................................................................................................................5 Board Diversity ........................................................................................................................................................5 -

Responsible Banking™

Responsible Banking™ 2020 ANNUAL REPORT Contents Board President Message .................................................................................................................................................................................2 2020 Board Members ..........................................................................................................................................................................................3 CEO Message ...........................................................................................................................................................................................................4 CEO Message and 2020 Executive Team ................................................................................................................................................5 Product and Service Enhancements .........................................................................................................................................................6 Acknowledgements and Accomplishments .......................................................................................................................................7 Our Company ..........................................................................................................................................................................................................8 Co-operative Principles ......................................................................................................................................................................................9 -

Bare Trustee Agreements Approved Fund Managers As Ofapril 30, 2021 Fund Manager Region Type of Products Funds Covered by Agreement 1 1832 Asset Management L.P

Bare Trustee Agreements Approved Fund Managers as ofApril 30, 2021 Fund Manager Region Type of Products Funds covered by agreement 1 1832 Asset Management L.P. (Dynamic Funds) Canada Mutual Funds / Hedge Funds / LSF's Includes Deposit accounts 2 3IQ CORP. Canada Pooled Fund 3IQ Corp. 3 Aberdeen Global Services S.A. Overseas Mutual Fund Aberdeen Global Funds Aberdeen Global II Funds 4 Accilent Capital Management Inc. Canada Mutual Fund/Pooled Fund/Ltd. Partnership Capsure Hedged Oil and Gas Income & Growth Trust 5 Acker Finley Asset Management Inc. Canada Mutual Fund QSATM Funds 6 ACM Advisors Ltd. Canada Mortgage Investment Fund ACM Commercial Mortgage Fund 7 Addenda Capital Inc. Canada Pooled Fund Addenda Pooled Funds 8 ADS Canadian Bank Canada GIC's / Investment Savings Accounts 9 AGAWA Fund Management Inc. Canada Limited Partnership AGAWA Fund I Limited Partnership 10 AGF Investments Inc. Canada Mutual Fund / Pooled Fund Acuity Pooled funds AGF Pooled funds AGF Elements family of mutual funds Harmony family of mutual funds AGF family of mutual funds Acuity family of mutual funds 11 AHF Capital Partners Inc. Canada Mutual Fund/Hedge Fund/Pooled Fund AHF Credit Opportunities Fund - Series A, F and I 12 AIP Asset Management Inc. Canada Limited Partnership AIP Convertible Private Debt Fund LP 13 Aldergrove Credit Union Canada GIC's 14 Algonquin Capital Corporation Canada Limited Partnership 15 Alignvest Capital Management Inc. Canada Hedge Fund 16 Alignvest Investment Management Corporation Canada Pooled Fund 17 Alitis Investment Counsel Inc. Canada REIT Listing of Approved Fund Managers by Name Page 1 of 23 Fund Manager Region Type of Products Funds covered by agreement Alitis Private REIT Alitis Mortgage Plus Fund 18 AlphaFixe Capital Inc. -

GULF WINDS Credit Union Adjusts Its Sails to Meet Member Expectations

Credit union DECEMBER 2019 TRACKER® New study shows CUs' net incomes declining due to falling interest rates News and Trends (Page 11) How CUs gain an advantage with emotional marketing Deep Dive (Page 16) GULF WINDS Credit Union Adjusts Its Sails To Meet Member Expectations FEATURE STORY (Page 7) TABLE OF CONTENTS WHAT’S INSIDE CUs are leveraging a variety of tactics, including emotional marketing and innovative engagement efforts, to compete 03 in the rapidly evolving financial industry FEATURE STORY An interview with Haley Murph, vice president of eServices and payments for Gulf Winds Credit Union, about how the CU is 07 adapting its engagement and retention strategies to address high member expectations NEWS AND TRENDS The latest headlines from around the space, including a new 11 blockchain identity paltform from CULedger DEEP DIVE An in-depth examination of emotional marketing, including how CUs can leverage it to compete with larger banks and 16 FinTechs ACKNOWLEDGMENT The Credit Union Tracker® was done in collaboration with PSCU, and PYMNTS is grateful for the company’s support ABOUT and insight. PYMNTS.com retains full editorial control over the findings presented, as well as the methodology and data 19 Information on PYMNTS.com and PSCU analysis. 3 WHAT'S INSIDE Credit unions (CUs) remain strong despite the many banking’s omnipresent status is even changing how challenges they face. The recently released G-19 Con- members want to interact with their CUs, though regula- sumer Credit Report found that CUs held $64.4 billion in tory and compliance issues often mean that consumers credit card debt as of September — a 6.9 percent year- cannot reasonably expect the same lightning-fast inter- over-year increase. -

THE SASKATCHEWAN GAZETTE, January 20, 2012 73 (REGULATIONS)/CE NUMÉRO NE CONTIENT PAS DE PARTIE III (RÈGLEMENTS)

THIS ISSUE HAS NO PART III THE SASKATCHEWAN GAZETTE, JANUARY 20, 2012 73 (REGULATIONS)/CE NUMÉRO NE CONTIENT PAS DE PARTIE III (RÈGLEMENTS) The Saskatchewan Gazette PUBLISHED WEEKLY BY AUTHORITY OF THE QUEEN’S PRINTER/PUBLIÉE CHAQUE SEMAINE SOUS L’AUTORITÉ DE L’ImPRIMEUR DE LA REINE PART I/PARTIE I Volume 108 REGINA, FRIDAY, JANUARY 20, 2012/REGINA, VENDREDI, 20 JANVIER 2012 No. 3/nº 3 TABLE OF CONTENTS/TABLE DES MATIÈRES PART I/PARTIE I PROGRESS OF BILLS/RAPPORT SUR L’éTAT DES PROJETS DE LOI (First Session, Twenty-seventh Legislative Assembly/Première session, 27e Assemblée législative) ............................................. 74 ACTS NOT YET PROCLAIMED/LOIS NON ENCORE PROCLAMÉES ..................................................................................... 75 ACTS IN FORCE ON SPECIFIC EVENTS/LOIS ENTRANT EN VIGUEUR À DES OCCURRENCES PARTICULIÈRES..... 78 ACTS PROCLAIMED/LOIS PROCLAMÉES (2011) ........................................................................................................................ 78 ACTS PROCLAIMED/LOIS PROCLAMÉES (2012) ........................................................................................................................ 79 MINISTERS’ ORDERS/ARRÊTÉS MINISTÉRIELS ...................................................................................................................... 79 The Highways and Transportation Act, 1997 ......................................................................................................................................... 79 The Municipalities